Editor’s Note: On Tuesdays we turn the spotlight outside of Porter & Co. to bring you exclusive access to the research, the thinking, and the investment ideas of the analysts Porter follows personally.

If you’re new to Porter & Co. and want to find out more about The Spotlight or want access to all past issues, click here.

Today, we turn the Spotlight over to Stansberry Asset Management Chief Investment Officer Austin Root.

Stansberry Asset Management (“SAM”) is an SEC-registered investment advisory firm with more than $1.1 billion in assets under management. SAM is separate and distinct from Porter & Co., and helps families and individuals across the country invest their wealth and achieve their long-term financial goals.

Austin has an investment pedigree grounded in real-world experience and a track record of delivering results. He ran a successful hedge fund with a strategic backing from Julian Roberston and Tiger Management… He was a portfolio manager for billionaire investor Steve Cohen… He was an investment banker for Blackstone… He has an MBA from Stanford… And before becoming CIO at SAM, he was the director of research for the former company I founded, Stansberry Research.

I (Porter) have often said that if you have $1 million or more in investable assets, having a professional asset manager is a huge advantage. And that’s especially true, if that asset manager has the skills and experience of the investment team at SAM.

Here’s Austin…

I want to share with you what I believe are the 56 most important minutes of video to watch if you want to become a great investor in today’s world.

That’s 56 minutes – spread across two different videos – that I’m confident will change your investment life for the better, forever.

Sound interesting?

Before you answer, I should note that while it won’t cost you anything to access these enlightening 56 minutes, it does require your time.

And after recently celebrating Father’s Day with my wonderful wife and kids – and not being able to spend it with my own father who passed away too young – I know just how valuable one’s time truly is. And I’m certain you do, too.

Still… if you’re willing to share those 56 minutes with me – and more specifically, to give your truly undivided time and attention – I’m confident you’ll receive far more in return.

So, with that, let’s get to it. As I noted above, these 56 minutes are spread across two separate and distinct videos. The first video is short, old, and full of timeless advice. It’s a stage-setter. The second video is longer, brand-new, and full of both timeless and timely advice for investors looking to get ahead in the market starting right now.

More specifically on the first video… It’s only seven minutes long and was filmed more than 40 years ago. And yes, the video quality is a little grainy. But it’s worth viewing, as it’s jam-packed with some of the most insightful investment thoughts that I believe have ever been caught on film.

Here’s the link. (I encourage you to get out a pen and paper and take notes.)

Now, once you’ve watched that first video… I’d be willing to bet that you not only recognized a much younger Warren Buffett but that you were also familiar with at least one of the many points he made about investing in that short span.

I find this video incredible for three reasons. First, this was filmed in 1984 and was the first major television interview Warren ever gave. And yet it sounds more like a nonstop, “greatest hits” version of Buffett investment advice. Second, on a related point, I find it remarkable how broadly consistent his message on investing has stayed over the past four decades since this was filmed.

Third, I’m amazed that the very first comment he makes – in his first-ever TV interview – might be his most famous quote of all time.

To paraphrase, Buffett states that there are only two rules of investing: the first rule is don’t lose money. And the second rule is don’t forget the first rule. (Over the years, as he’s repeated the line, he’s often swapped “don’t” for “never.”)

But truth be told, when reflecting about this quote, I’ve often asked myself, why?

Why is the greatest investor in the world best known for a quip about not losing money, rather than making it?

Over the course of more than two decades of professional investing, I have come to find the answer. Or more accurately, answers. Specifically, there are two main reasons why I believe Buffett is so adamant about avoiding big drawdowns in your portfolio.

First, big losses in your portfolio limit your ability to make the best investment decisions in the future. This happens most often because losing money creates either financial limitations or emotional limitations.

Throughout my career, I have seen many times how losing money can become a financially limiting factor for investors. In the extreme cases, it ends in disaster. One of the most memorable examples came early on in my career while I was an investment banker at Blackstone. Our banking group specialized in helping companies either avoid bankruptcy or emerge from it, ideally as a healthy and more viable business.

In the fall of 2000, we began working with medical diagnostics company Dade Behring or, more accurately, with the private equity firm that owned it, Bain Capital (this included meetings with the head of Bain Capital at the time, Mitt Romney). Bain had acquired Dade through a leveraged buyout in 1995, and then, over the next few years, added more debt to the company to “bolt on” other diagnostics and testing businesses to Dade.

By 1998, sales had more than doubled and Bain executives began a process to see if they could sell the business and generate a quick profit. When no satisfactory offer emerged, Bain decided in 1999 to lever the company up even more and pay itself and other shareholders a “special dividend” of more than $400 million. These combined transactions increased Dade’s debts more than fivefold to $2 billion.

Then came the losses… The economy went into a recession, Dade experienced delays in production facilities and product launches, lost sales to competitors, faced currency headwinds and cost overruns, and all while the cost of its large debt balances soared.

By 2001, the best long-term decision for Dade was to invest back into the business. But Dade’s debts were coming due, and no other lenders were coming to the rescue. In a last-ditch effort, Bain and Blackstone tried again to sell the company. But the market value had dropped so much that Dade was now worth less than the sum of its liabilities.

In 2002, Dade Behring filed for bankruptcy.

Experiencing big losses in your investments can also be limiting emotionally. I’m sure you’ve felt it before. You own a stock that’s hit with terrible news and the price craters. Oftentimes, that news is so bad that it should invalidate your investment thesis and the right move is to sell the stock and move on. But all too often, investors let their emotions get the better of them. They do not want to realize the loss and confirm a mistake. They’d rather hold on and hope that the story changes and the stock recovers. But as we all know, hope is not a profitable investment strategy.

The emotional toll that big losses create can impair the decisions of every investor, even some of the best. I saw this vividly while working with legendary investor Julian Robertson, founder of Tiger Management. As markets sank during the financial crisis of 2008, Julian asked another hedge fund manager (who will remain nameless) how he was going to handle the huge losses his fund was experiencing. Wasn’t it time to sell and move on, or at least more properly hedge bets and protect the fund from future losses? The rest of us in the room at that time knew the answer was emphatically “yes”. But this proud investor could not bring himself to do it. His emotions limited his ability to make the right decision in the face of huge losses.

By the end of 2008, his fund lost more than half its value. In 2009, the fund shut down.

The second major reason why avoiding big losses is so important is one of simple math. It is mathematically very hard to recover from large losses in your portfolio. And the larger the loss, the more difficult the recovery is.

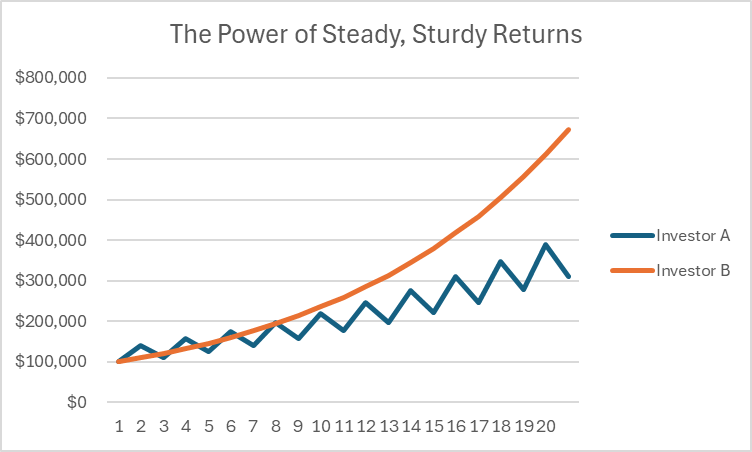

The simple example that I remind analysts who work for me about is that when you lose 50% in an investment, it takes double that percentage or a 100% gain, just to get back to even. But that only tells part of the story. The real mathematical power of loss avoidance comes from consistently doing so. Consider the following example of two investors, A and B.

Investor A is a boom-or-bust investor. In the good years, A generates 40% on his investments, and in the bad years, he loses 20%. If we assume that his good and bad years are split evenly, that means his simple average return is 10% per year (40 minus 20 divided by 2). If we further assume that these good and bad years alternate every year, here is what his returns would look like over 20 years assuming he started with $100,000.

After 20 years, Investor A will have more than tripled his money. Not bad. But let’s now look at Investor B. And let’s assume that B invests in assets that produce the same simple average return of 10%, except that she generates those consistently, year in and year out, with no big-loss years. This is what her return stream would look like:

In 20 years, Investor B makes more than six times her money, finishing with more than double Investor A’s haul. So why is this? Why the discrepancy between two investors who both produce simple average annual returns of 10%? The answer lies in the mathematical challenge of overcoming large losses. Here are their return streams plotted against one another:

As you can see, avoiding losses has a huge, positive impact on one’s performance. And the magnitude of that impact is far greater than most investors realize. Here’s why… Up to this point, I have described Investor A’s returns as having a “simple” average of 10%. But as investors, that’s not what we care about. We care about how much money we end up with relative to how much we start with. And to calculate that, we’re in search of the compounded average of our returns over time. In other words, if we started with $100,000 and we ended with a little more than $300,000 as Investor A did, what rate of return, compounded annually, would produce that result?

As it turns out, for Investor A, his compound average annual return was just 5.8%. Those large loss years were such deep holes from which to dig out, that he couldn’t nearly keep up with Investor B’s steady-Eddie results (and since she had no down years, her compound average returns were also 10%, same as her simple average returns).

Said differently, avoiding losses is so powerful to long-term gains that even if Investor B only made a steady 6% per year, she still would have outperformed Investor A’s boom-or-bust return stream.

Avoiding risk is a crucial thing. But it is far from the only thing. And stuffing cash under the proverbial mattress isn’t going to help most investors reach their financial goals. Not with rampant inflation and a federal government who thinks the only way out of its deficit spending problem is to debase its currency and “grow” its way out.

For most, generating robust, real returns isn’t a luxury, it is a necessity.

Taken together, these two goals represent the single toughest task in all of investing: how can you generate high returns with low risk no matter what the market throws at us?

It’s frankly something that’s been confounding investors for centuries.

That brings us to the other 49 minutes I mentioned…

I recently sat down with Porter Stansberry to discuss how to do just that. You see, as Chief Investment Officer at Stansberry Asset Management (“SAM”), I lead a team of investment managers whose main goal is to help our clients reach their financial goals in up markets and down. And managing risk while generating robust returns is a huge part of that process.

I’ve known Porter for nearly two decades. And I consider him not only a close friend but also a brilliant investment mind. That doesn’t mean we always agree on everything (we don’t). But in our recent, unscripted conversation, we found that we both feel strongly about one crucial point:

Investors need a better way to invest and balance risk and return than the traditional, set-it-and-forget-it approach.

And that’s exactly what this conversation covers – it’s a thoughtful discussion between Porter and me on what it really takes to build a resilient, high-performing portfolio in today’s environment.

The world is changing, and so are the financial markets. A more thoughtful investment approach is essential if you’re looking to generate meaningful returns (while never forgetting Mr. Buffett’s two rules).

Thankfully, there’s a way to prepare for what’s to come. And like Buffett said, you don’t need tons of IQ to do it. But you do need to have a plan.

That’s exactly what you’ll walk away with after viewing my talk with Porter. It’s free. All you need to do is <click here>.

In short, these 49 minutes show a way to finally answer that age-old question: How can I generate high returns with low risk?

You’ll find out soon. Enjoy the video.

Good investing,

Austin Root