Issue #132, Volume #2

Nvidia Is Cheaper Today Than It Was Before ChatGPT

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| Nearly half a trillion in capex… Nvidia’s growth is astronomical… Shares haven’t kept up with earnings… Huang’s Law outpaces Moore’s Law… It isn’t a bubble for Nvidia… Credit delinquencies soar… Bankruptcies rise… |

It’s not a bubble.

Last year we published The Parallel Processing Revolution. This is the most important piece of research I’ve ever written. If you haven’t read it yet, I’d urge you to do so. And if you haven’t read it recently, I’d urge you to review it again now.

In the last three years, Microsoft (MSFT) has invested about $100 billion in 15 major new computer centers around the world and is rebuilding its existing Azure infrastructure, using parallel computing. Amazon (AMZN) has spent substantially more, about $200 billion, on 20 new computer centers and revamping the existing Amazon Web Services infrastructure. Google (GOOG), in part because it’s been using its own, proprietary chips, has “only” spent $75 billion on 12 new centers. And Meta (META) has spent roughly the same amount, while adding seven major new centers.

In total, just from these four companies, that’s almost half a trillion dollars! And believe it or not, investments in this new technology are accelerating. Microsoft plans to invest another $300 billion by 2030, to build more than 50 new centers each year. Amazon is being even more aggressive: it plans to double its compute capacity by 2027, while spending $400 billion by 2030. Google and Meta both say they will spend $300 billion through 2030. In total, this is an additional $1.5 trillion in compute capex through 2030.

Of all the AI applications being developed (like ChatGPT, Grok, and Gemini), powerful data centers aren’t the only result of these huge investments. AI is merely one application of the ongoing parallel processing revolution. By 2030, there will be new applications that we can’t even imagine today – wholly autonomous transportation, human-like robots, unprecedented increases in productivity in virtually every industry, but most notably in education, finance, and medicine.

What’s driving all these “magical” applications is a revolutionary computer architecture – which I spelled out in great detail in The Parallel Processing Revolution report.

Rather than processing data serially (one computation at a time), Nvidia (NVDA) developed an entirely new, and vastly more powerful way, to process data: in parallel, with thousands of computations completed at the same time. Instead of trying to make computers faster (to process more data), Nvidia’s chips achieve vastly more performance by linking an ever-larger number of processors, called GPUs (tens of thousands), together, working in parallel.

During the serial era of computing (“CPUs”), Moore’s Law accurately predicted that increasing transistor density on chips would improve their performance steadily, doubling their performance every two years (1.4x annually). For Nvidia’s GPUs, “Huang’s Law” (coined in 2018, named after its CEO Jensen Huang) predicts performance will increase much faster: 2x every two years (~1.71x annually). And empirically this has proven to be true. Since 2006, Nvidia has been outpacing Moore’s Law by 40% a year, unleashing a previously unimaginable amount of computer power.

As a result, computers can now take on tasks that were previously far beyond their capabilities. And the existing installed base of computer data centers must be rebuilt, from the ground up, using parallel computer systems – the best of which are built by Nvidia.

Finally, there’s one aspect of this ongoing revolution that most investors still do not understand. Nvidia doesn’t merely build the best parallel chip systems (the hardware). It also controls the software (CUDA) that’s necessary to apply these massively more powerful computers to applications.

If you think about the last great computer revolution (the internet boom), there were multiple companies that controlled the key enabling technologies. Intel (INTC) made the best chips. Cisco (CSCO) dominated the interconnects. And there were dozens of software providers: Microsoft, Apple (AAPL), Oracle (ORCL), etc.

With the parallel processing revolution, all of the best hardware and the dominant software platform is owned and controlled by only one company: Nvidia. As a result, the overwhelming majority of the profits have accrued onto its financial statements.

Just three years ago, Nvidia was merely a successful computer hardware business. It dominated the market for GPUs, which back then were primarily used in video games (40%) and in crypto mining data centers (50%).

In the 3Q 2022 (just before the release of ChatGPT), Nvidia’s total revenue was almost $6 billion, with net income of $1.6 billion, producing earnings per share (split-adjusted) of a nickel ($0.05). Gross margins were impressive, but not unprecedented, at 65.1%. The stock wasn’t cheap: Nvidia’s stock traded at a split-adjusted $13 per share, implying a $320 billion market cap – 45x forward earnings projections.

Today Nvidia trades at almost $200 per share, implying a $5 trillion total market value, up more than 1,000% in only three years!

The scope of this value creation (~$4 trillion in three years) is unprecedented in the history of the financial markets, leading to cries of “bubble.”

But look at the business results.

In this year’s 3Q, revenue was $60.5 billion, up $54.5 billion (642%) since the advent of ChatGPT. Data-center-specific revenue was over $50 billion, up 1,334% since 3Q 2021. Gross margins are now almost unbelievable: 78%. Net income in the most recent quarter was over $30 billion, producing earnings per share of $1.28, up 2,270%.

Looking at the business results shows the stock price increase (1,418%) hasn’t kept pace with the increase to earnings. As a result, the stock is actually cheaper today than it was in 2022 – it’s trading at a forward P/E ratio of 32.

I understand that it’s hard to believe that this amount of growth (and wealth creation) can be sustained. But I believe it will be. In fact, I think Nvidia will see a larger increase in value by 2030 than it has seen so far.

All this wealth is fundamentally being driven by an unprecedented increase to computing power. And what that will unleash will change our world more in the next decade than all of the innovation we’ve seen in the last 1,000 years.

Nvidia lies at the center of all of this value creation.

Jim Rickards: “One Executive Order Changes My Entire ‘Birthright’ Thesis…”

In his original ‘Birthright’ presentation, Jim Rickards conservatively projected this $150 trillion mineral boom to transpire over 4 years… But Trump has just completely accelerated this timeline. What happens next will shock most Americans. Jim just recorded an urgent interview with all the new details.

Watch his full analysis of The American Birthright: Phase II HERE.

Three Things To Know Before We Go…

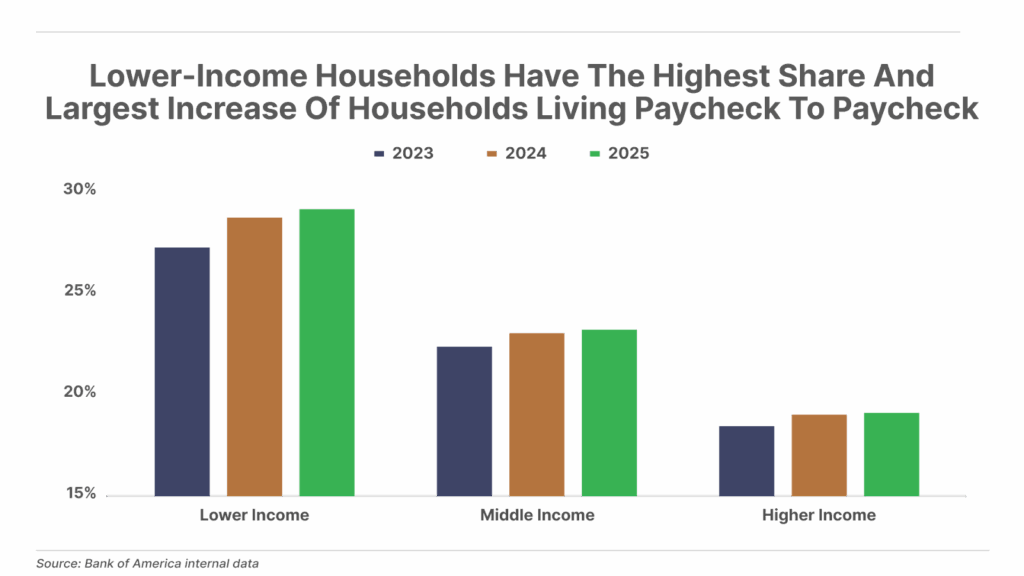

1. The “K-Shaped” economy is taking a toll. According to Bank of America internal data, nearly one in four Americans is currently living paycheck to paycheck – defined as spending 95% or more of their income on necessities. However, those with the lowest incomes are disproportionately affected, with both the largest share and largest increase in households living paycheck to paycheck over the past three years.

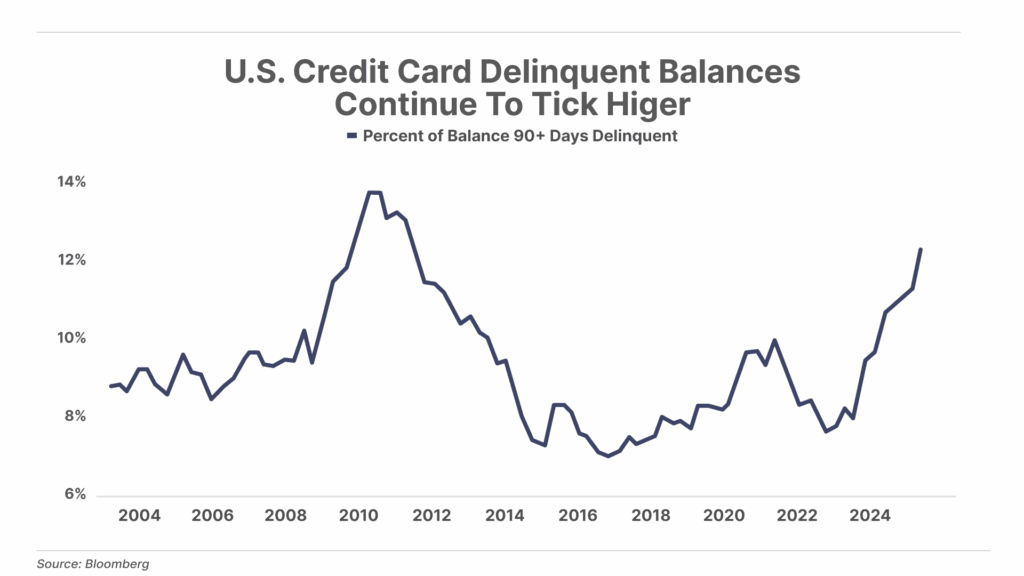

2. Credit and auto delinquencies are soaring as the consumer continues to struggle. Subprime auto-loan delinquencies just hit 6.65% – the highest level since Fitch rating agency began tracking the data in 1994, signaling growing stress among the most financially vulnerable households. Credit card delinquencies are also climbing to multi-year highs, reflecting broader deterioration across consumer credit. At the same time, the low-income cohort is expanding as AI-driven efficiency gains slow hiring. Add persistent inflation to this, which continues to erode purchasing power, and the result is a worsening financial squeeze that is pushing more borrowers toward default and exposing growing fragility in the consumer economy.

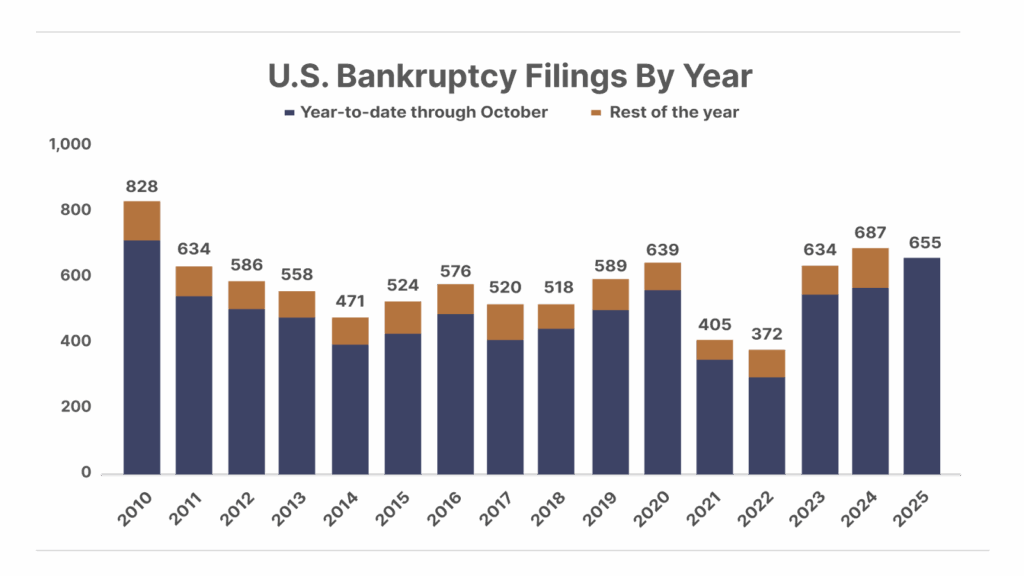

3. Corporate bankruptcies hit 15-year high. A total of 655 U.S. corporations have filed for bankruptcy so far this year, based on the latest data through the end of October. – the highest year-to-date total since 2010. This is the latest warning sign that the credit cycle has turned, and we expect more to come.

And One More Thing… Poll Results

After the Trump administration floated the idea of a 50-year mortgage as a way to get more people into the housing market, we asked readers if they thought it was a good idea:

The result was decisive: 92% of survey takers selected “no,” a 50-year mortgage is not a good idea.

Tell us what you think of today’s Daily Journal or anything else that is on your mind: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland

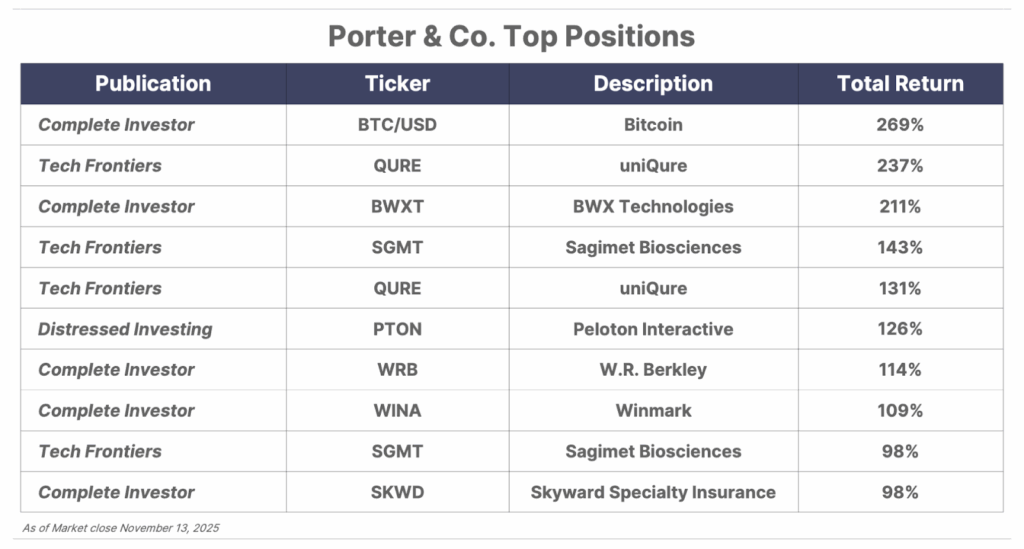

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call our Customer Care team at 888-610-8895 or internationally at +1 443-815-4447.