Issue #112, Volume #2

How To Invest Like Warren Buffett Did In The 1950s – Today

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| You don’t have to guess… Buy $1 for 20 cents… Buffett and Graham and a Pennsylvania railroad… a master at unlocking shareholder value… Japanese trading firms… The first of a series of Journals… A government shutdown looms… Tariffs, tariffs, tariffs… |

Trying harder won’t help.

It’s not that the door is stuck. It’s that you’re pushing on the wrong door.

You believe if you back the right new artificial-intelligence (“AI”) firm, the next generation of big tech profits will be yours (innovation). Or you believe that if you buy a stock when it’s down 90% that when it eventually goes back up, your fortune will be made (turnarounds).

Or when that next well gushes oil… or when that new product drops… or when that buyout offer hits…

You’re betting on ifs and whens.

You’re taking risks – risks that are so large, you can’t measure them accurately. And you might not tell your wife how these gambles work out, but your net worth tells the tale all the same: you’re a lousy investor.

And you’re losing the most precious asset of all – time.

There’s a better way.

There’s a door that’s wide open. And it’s always there, for anyone who will simply bother to walk through it. You don’t have to guess. And you never have to lose money or waste time again. There’s a simple way to take all of the risk and all of the guesswork out of your investing – forever.

My good friend Brett Gardner laid it all out for us in his remarkable new book, Buffett’s Early Investments. I’d urge you to buy the book and read it.

It’s the best guide to sure thing investing that I have ever read.

You don’t buy anything that might work. Or that could pan out. You only buy what you know is worth $1. And – this is the important part – you only pay about $0.20.

I’m sure you don’t believe that’s possible. You think all of these incredible opportunities disappeared in the bull markets of the 1960s, the 1980s, or the 1990s. But over the next two weeks, I’m going to show you exactly how investors are using Warren Buffett’s strategy – right now – to make enormous, life-changing profits in stocks that are sure things.

They’re not guessing.

To show you how this works, I’m going to use an example that Brett detailed for the audience at our Annual Conference last week, at my farm. This is the story of the Philadelphia & Reading (“P&R”) Railroad. Please, pay close attention. Later this week (on Wednesday and Friday here in the Journal) I’ll show you situations just like this in today’s markets. Remember: they’re not guessing.

Chartered in 1833, the P&R Railroad was built to haul anthracite coal – “black diamonds” – from Pennsylvania’s rugged hills to Philadelphia’s bustling ports and factories. Over the next 75 years, this railroad would become the most valuable economic engine in the United States.

Anthracite, a hard, clean-burning coal, powered the nation’s energy revolution in the 19th century. It fueled steam engines, heated homes, and smelted iron during the Civil War. At its peak, the P&R’s coal supplied nearly one-fifth of all U.S. energy, with production soaring to over 100 million tons by 1917. All of this from a 500-square-mile coal field in northeastern Pennsylvania.

The P&R Railroad was an economic miracle, built with colossal capital outlays. By the early 1900s, the company had outstanding bonds totaling $135 million – that’d be about $5 billion today.

P&R’s coal production peaked in 1917. Its dominance attracted anti-trust actions and, in 1920, the U.S. Supreme Court ruled railroads couldn’t also own coal mines. P&R was forced to divest its railroad. Meanwhile, anthracite’s energy dominance faded as cheaper and more convenient alternatives emerged: bituminous coal for industry, oil for heating and transport, and natural gas for homes.

Coal production plummeted 70%. And then the Great Depression hit. P&R declared bankruptcy in 1937 and didn’t emerge from restructuring until 1945. But being shorn of its debts didn’t solve the insurmountable decline in its core business: there was no more demand for its core product. By 1954, return on assets hovered near zero, with stranded capital in depleted mines and “culm banks” – toxic waste piles.

In 1954, P&R traded at $13.38 per share, a $18.8 million market cap – but it had millions and millions in stranded capital. Buffett’s mentor Ben Graham bought 5% of the company and became its chairman. He installed his nephew, Mickey Newman, as CEO. And Buffett made the stock his largest holding, buying in under $10 a share.

Mickey Newman got P&R out of the coal business.

Renamed the Philadelphia & Reading Corporation it liquidated excess inventory and abandoned unprofitable mines, generating $7.3 million in tax losses. These tax-loss carryforwards and the cash these sales generated funded diversification outside of anthracite. First came Union Underwear in 1955 for $15 million – a steal at 5x pre-tax earnings of $3 million. How’d he make the deal? He used the $5 million in cash (from Union’s own coffers) and non-interest-bearing notes tied to excess profits. Acme Boots followed in 1956 – $3.2 million (4x earnings) with similar terms.

Unlocking the trapped capital through diversification saw earnings explode: $7.06 per share in 1956, nearly equaling Buffett’s entire cost basis.

Mickey Newman was a master at unlocking shareholder value. He engineered tax-efficient asset sales, like transferring properties to subsidiary Reading Anthracite for equity and debt, enabling tax-free distributions to shareholders. And the acquisitions rolled on: clothing firms, toys, and in 1961, Fruit of the Loom itself, saving $700,000 in royalties.

Buffett helped put together the biggest acquisition of all: Lone Star Steel in 1963. Newman borrowed to buy 73% of the company for $64 million. Long Star’s earnings doubled by 1967. And by 1968, when Northwest Industries acquired P&R, the stock had moved from under $10 to over $200 per share.

It took Mickey about 13 years to extract almost $400 million in value from P&R. But the result was never in doubt. The capital was sitting right there. It simply had to be unlocked.

This, of course, is the exact blueprint that Buffett would employ at Berkshire Hathaway. And it is the same blueprint he is following again today with his recent massive investments into several Japanese trading firms.

This kind of investing isn’t about luck. It is simply mastering capital allocation.

Today, huge Korean chaebols and Japanese keiretsu – large business conglomerates – are going through this same evolution, divesting non-core units amid massive economic transformation.

And over the next few Daily Journals, I’ll detail these opportunities for you.

No more guessing.

Just buy $1s for $0.20.

It’s not hard.

From Tiny To Titan: Decoding The DNA Of The Next 100-Bagger

Discover the 94 companies that contain the seven DNA markers of a potential 100-bagger…

And the exact ones Porter’s guest is about to invest $500,000 into.

Click here to watch the interview before it disappears this Tuesday at 11:59 PM PT.

Three Things To Know Before We Go…

1. Government shutdown looms. The U.S. government is less than 36 hours away from a partial shutdown. If Congress fails to pass funding legislation for the 2026 fiscal year (which begins on October 1), the shutdown will begin at midnight tomorrow, September 30. And, at least so far, the market is shrugging off the threat. The upside is that such a shutdown – the 15th since 1981 – would effectively give President Donald Trump carte blanche to slash federal programs and employees, which could make a much-needed dent in Uncle Sam’s ballooning budget deficits.

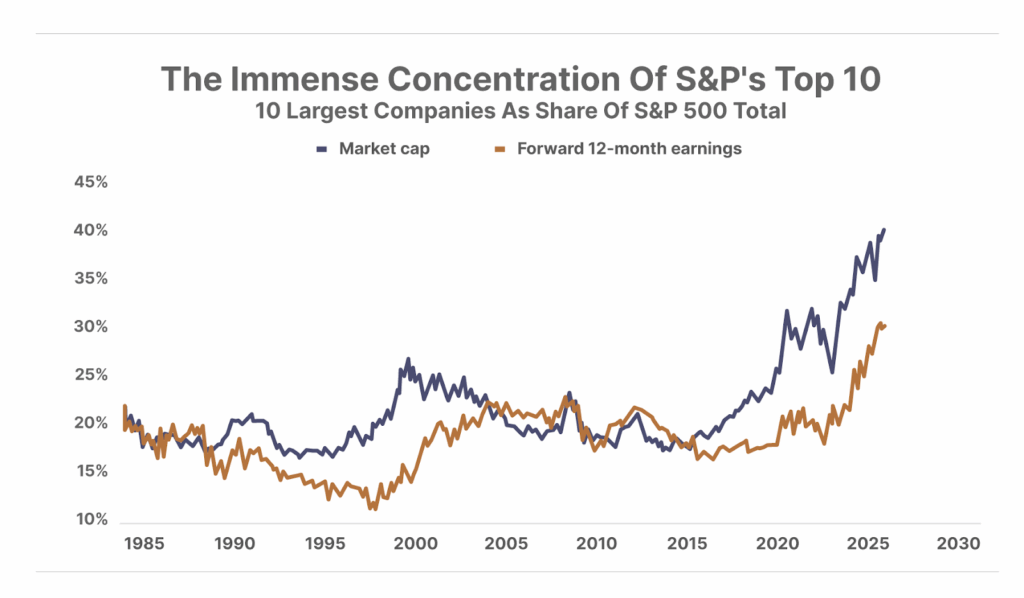

2. The S&P 500 or S&P 10? The S&P 500 is meant to track the performance of America’s 500 largest companies. Today the top 10 stocks account for 40% of the index’s weight – yet those same companies represent only 30% of the index’s projected earnings over the next year. This widening gap highlights how concentrated the index has become – and how richly valued the largest 10 names are compared to the other 490. If growth in the hyperscalers falters, the illusion of broad market strength could quickly unravel.

3. Trump issues a new wave of tariff announcements. Late last week, President Trump announced steep new tariffs on a slew of items made outside the U.S. set to go into effect on October 1. These include a 100% tariff on pharmaceuticals… a 50% tariff on kitchen cabinets, bathroom vanities, and associated products… a 30% tariff on upholstered furniture… and a 25% tariff on heavy trucks. He followed up these announcements this morning with a promise to impose a 100% tariff on any movies made outside of the U.S. As we’ve noted before, regardless of their intent, tariffs are a tax – plain and simple… and it remains to be seen what the ultimate effects will be as higher taxes work their way through the economy and begin impacting U.S. consumers and corporate profits.

And One More Thing… Conference Stand-Out Presentation

There is always one presentation that sucks all the air out of the room at Porter & Co.’s Annual Conference, held last week on my farm outside Baltimore… This year that was Pieter Sleger’s talk about small-cap stocks. Since his speech, we’ve been hounded by attendees asking for a copy of the recording. While that’s not available now, we’re currently running a special partnership with Pieter that provides many of the details he shared at the conference, plus access to his new Tiny Titans advisory on exclusive terms only available to Porter & Co. readers. Hint: he says don’t go after any small cap. Go after the right company. The mini-Buffett stocks with a real shot at significant returns… not through luck or hype but exceptional operations. Click here to check it out before it expires.

Tell me what you think: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland

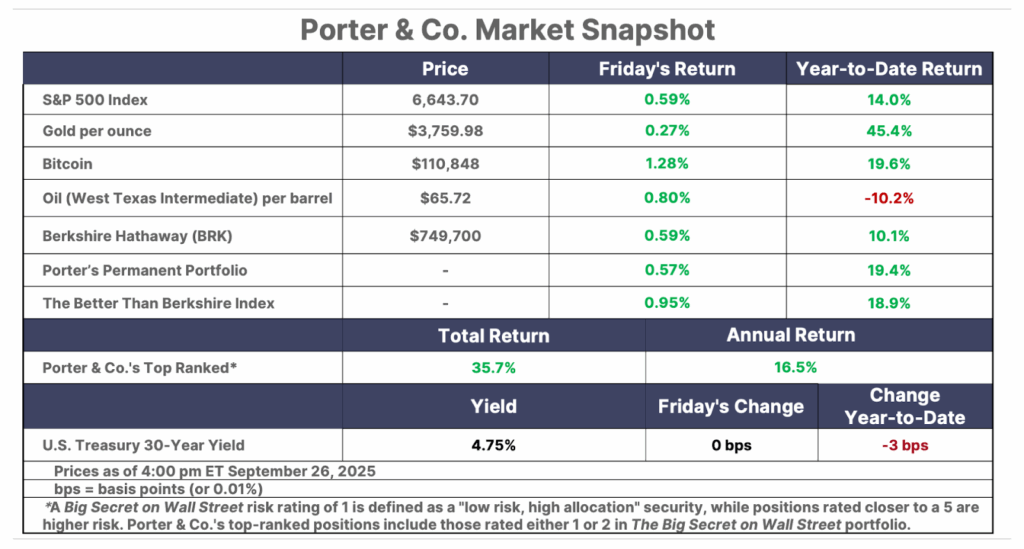

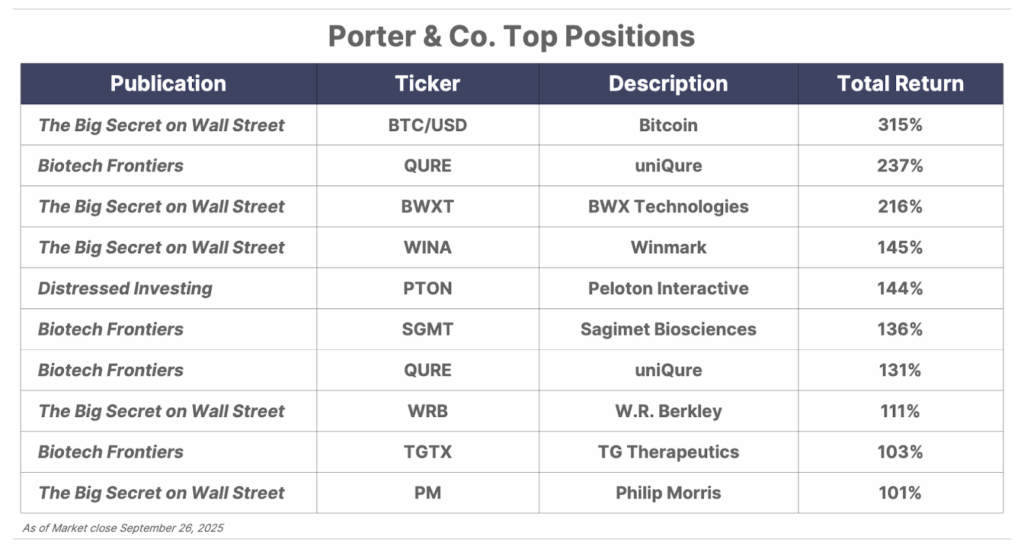

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call our Customer Care team at 888-610-8895 or internationally at +1 443-815-4447.