Issue #50, Volume #2

A Way To “Reset” Berkshire, Reward Its Investors, And Go Out With A Legendary Exit

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| What investors should be asking at Berkshire Hathaway’s annual meeting… The “I can’t make money in oil” investor hotline… They’d be better off in an index fund… Break it up and run it as three businesses… Dropping the mic: Warren Buffett’s $300 billion gift… McDonald’s is just for the rich… |

Berkshire Hathaway’s annual meeting is tomorrow.

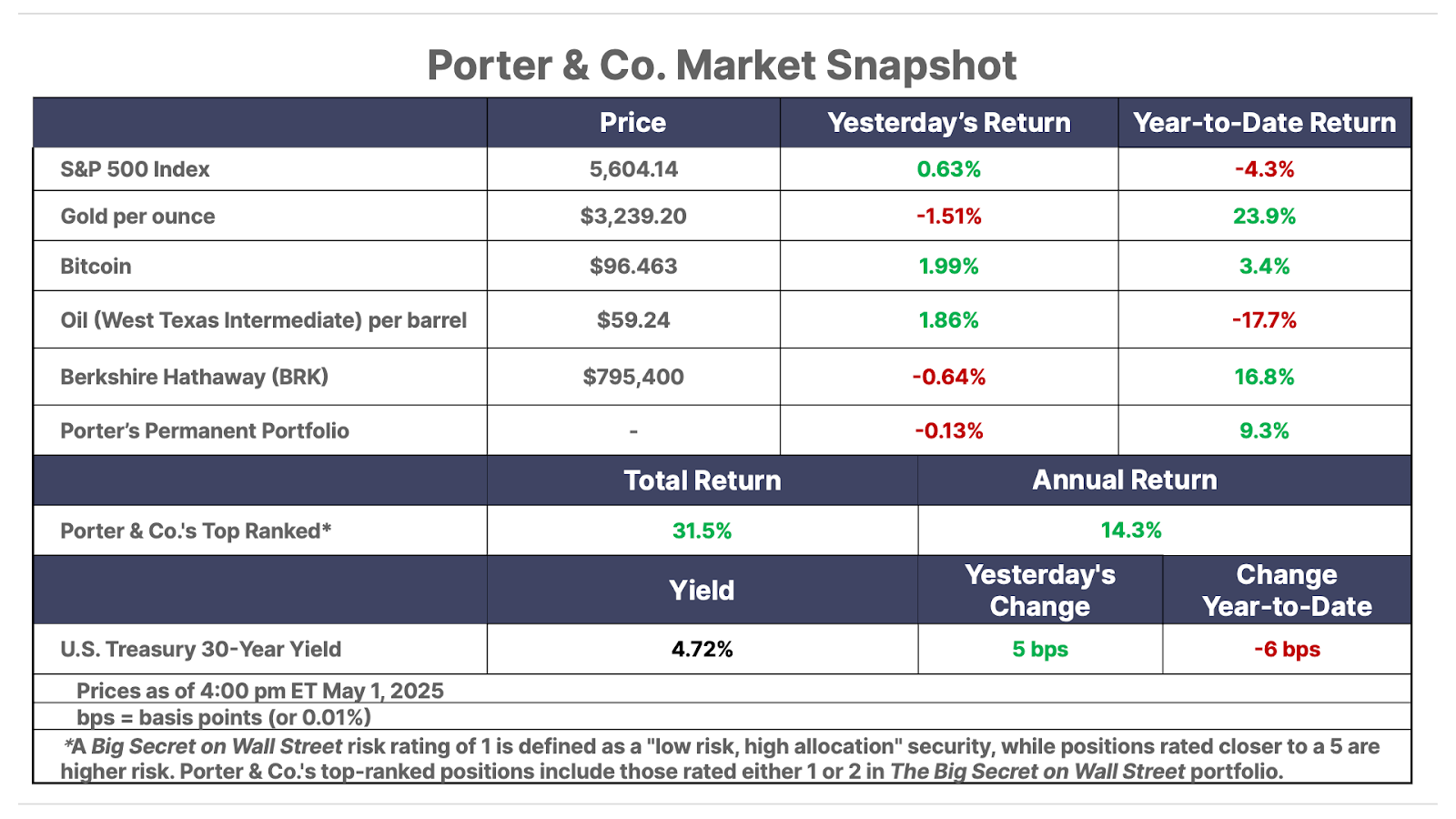

As I wrote recently, “Berkshire Hathaway: It’s Over,” I believe Berkshire Hathaway (BRK) is facing a crisis at its Berkshire Hathaway Energy (“BHE”) business that will lead to a major capital loss. I also know that virtually all of Warren Buffett’s biggest investments since 2000 have been busts, with the notable exception of Apple (AAPL).

Today, with over $300 billion in cash, the biggest question that investors must answer when considering the value of the business is how this cash hoard will eventually be invested.

My answer may surprise you…

Here’s what investors should be asking at the meeting tomorrow.

#1: Why does Berkshire keep buying oil at the top and selling at the bottom?

Buffett’s latest major investment – $19 billion into Occidental Petroleum (OXY) – has been a debacle. Berkshire purchased about 265 million shares for around $14 billion. It also purchased $10 billion in preferred shares with an 8% dividend. And as part of these purchases, it got 83.9 million warrants to buy shares at a $59 strike price. Even though this is the type of deal only Warren Buffett could get, and even though he’s done much better than regular investors, Buffett is still down $3.8 billion on the common stock. His warrants are now deeply out of the money and thus have zero intrinsic value. The preferred stock helps – he’s gotten $4.5 billion in dividends and he redeemed $1.5 billion of these shares in 2022. When you add all of this together, you find that Berkshire has made about $55 million, in total, since 2019. That’s a compound annual growth rate of 0.04%. It would have done better owning Treasury bills.

This is part of a trend.

Buffett has done poorly with his oil and gas investments historically (see ConocoPhillips 2006-2015), perhaps because he’s long endorsed a “peak oil,” neo-Malthusian worldview. Berkshire would be better off if Buffett would call the “I can’t make money in oil” investor hotline before he buys another oil company.

And yes, I know what you’re thinking, “but what about Chevron?” The results are better – Chevron (CVX) is a much better business – but the results are marginal at best. And Buffett is, once again, selling as oil falls (159 million shares down to 126 million shares). He’s made about $2 billion on the shares he sold and still owns about $17 billion worth. He’s gotten about $3 billion in dividends. When you add it all up… he’s made 6.3% a year. That’s about half what you could have made in an S&P 500 index fund over the same period.

So if Berkshire Hathaway decides to invest its $300 billion cash hoard in oil… the BRK stock is a sell.

#2: What’s the plan for Berkshire Hathaway Energy – why have you put more than $100 billion into regulated utilities with very low returns on invested capital and never-ending capital expenditures?

Buffett has invested over $100 billion into regulated energy utilities over the past 25+ years. Today these assets are managed as BHE, which began with a $4.3 billion investment in MidAmerican Energy in 2000. Since then, Buffett has invested another $22 billion acquiring the following:

- Northern Natural Gas (a $1 billion pipeline that once belonged to Enron)

- PacifiCorp ($5 billion electric utility serving notoriously liberal Oregon)

- Kern River Gas Transmission ($1 billion gas pipeline)

- NV Energy ($5 billion electric utility in Nevada)

- Dominion Energy ($10 billion gas pipeline)

And that’s only the cash Buffett invested. Those totals don’t include assumed debt.

The input costs of these businesses are driven by market forces, like interest rates and commodity prices. But the prices these company’s set for their energy and transportation services are regulated. That puts Berkshire at the mercy of politicians. And that, I’d suggest, is a very poor position to be in. This entire area of the market is like a blind canyon: once you fly in, there’s no way out.

And that could lead to a huge problem for Berkshire. S&P Global estimates BHE is only worth $80 billion today – not including any wildfire liabilities – implying a substantial loss for Berkshire over the last 25 years. (Note: Berkshire famously refused to take any dividends from BHE, preferring to reinvest all the group’s earnings until 2023, when it took $1 billion.) Meanwhile, current litigation relating to wildfire damage could lead to a huge ($10 billion to $40 billion) write-off.

#3: Why has virtually every major investment Berkshire’s made over the past 25 years led to poor – and even catastrophic – results?

Berkshire bought $11 billion worth of IBM stock in 2011. It began selling in 2016 and sold all the shares by 2018. Ironically, given Buffett’s long friendship with Bill Gates, it was competition from Microsoft’s cloud offerings that hurt IBM the most. The result? Berkshire made about 4% over seven years! That’s a disaster in one of Berkshire’s largest-ever investments.

Bank of America? Sure, Berkshire got lots of dividends from the preferred shares from 2011 to 2016, and the common shares from 2017 to 2025 – for a total of $6.5 billion – but the stock was a marginal performer at best. Total return? Berkshire earned 7.5% annually – far below the market’s return – on its huge $17.6 billion investment.

The other major investments since 2000:

- $37 billion invested into Precision Castparts (2019) led to a $10 billion write-off and a major capital loss of at least $3 billion

- $23 billion invested into Kraft Heinz (2013) led to a $2.7 billion write-off and subpar annual returns (7.5% annually)

- $10 billion invested into Verizon (2020-2021), which declined as interest rates rose, making Verizon’s (VZ) dividend less attractive – Berkshire exited the position in 2022 with a loss of $1.3 billion

- $9 billion invested in Lubrizol (2011) has produced very poor results – a 4.7% annual return

- $8 billion invested into airlines – American (AAL), Delta (DAL), Southwest (LUV), and United (UAL) in 2016 – led to a sale at the bottom of the COVID panic, creating 50%+ losses ($4 billion)

- $7 billion invested into ConocoPhillips (2006) – which Buffett later admitted was a “major mistake” – led to a $1.9 billion write-off in 2009 and then was sold off as oil crashed in 2014, creating a roughly $400 million loss

- $2.3 billion invested in Tesco PLC (2006) was sold in 2014 after an accounting scandal, resulting in a $1 billion loss

For decades Buffett told his investors that because he could produce better results by retaining all of Berkshire’s earnings than he could make by investing in an index fund, it was logical for Berkshire not to pay a dividend.

Thanks mainly to the outstanding results in its insurance companies and its investment into Apple, Berkshire has outperformed the S&P 500 over the last year, the last five years, and the last 10 years.

If the stock market continues to trend lower, Berkshire will, most likely, continue to outperform, because of its huge cash hoard. Berkshire holds over $330 billion worth of Treasury bills, equal to roughly a third of its market capitalization. Thus, over the longer term, Berkshire’s ability to continue to beat the market depends on how this cash hoard is eventually deployed. In that regard, Buffett’s track record over the last 25 years isn’t reassuring, nor is his age (94 years old) likely to make this challenge easier.

Given this scenario, I believe the board of Berkshire Hathaway has a fiduciary obligation to break up the company.

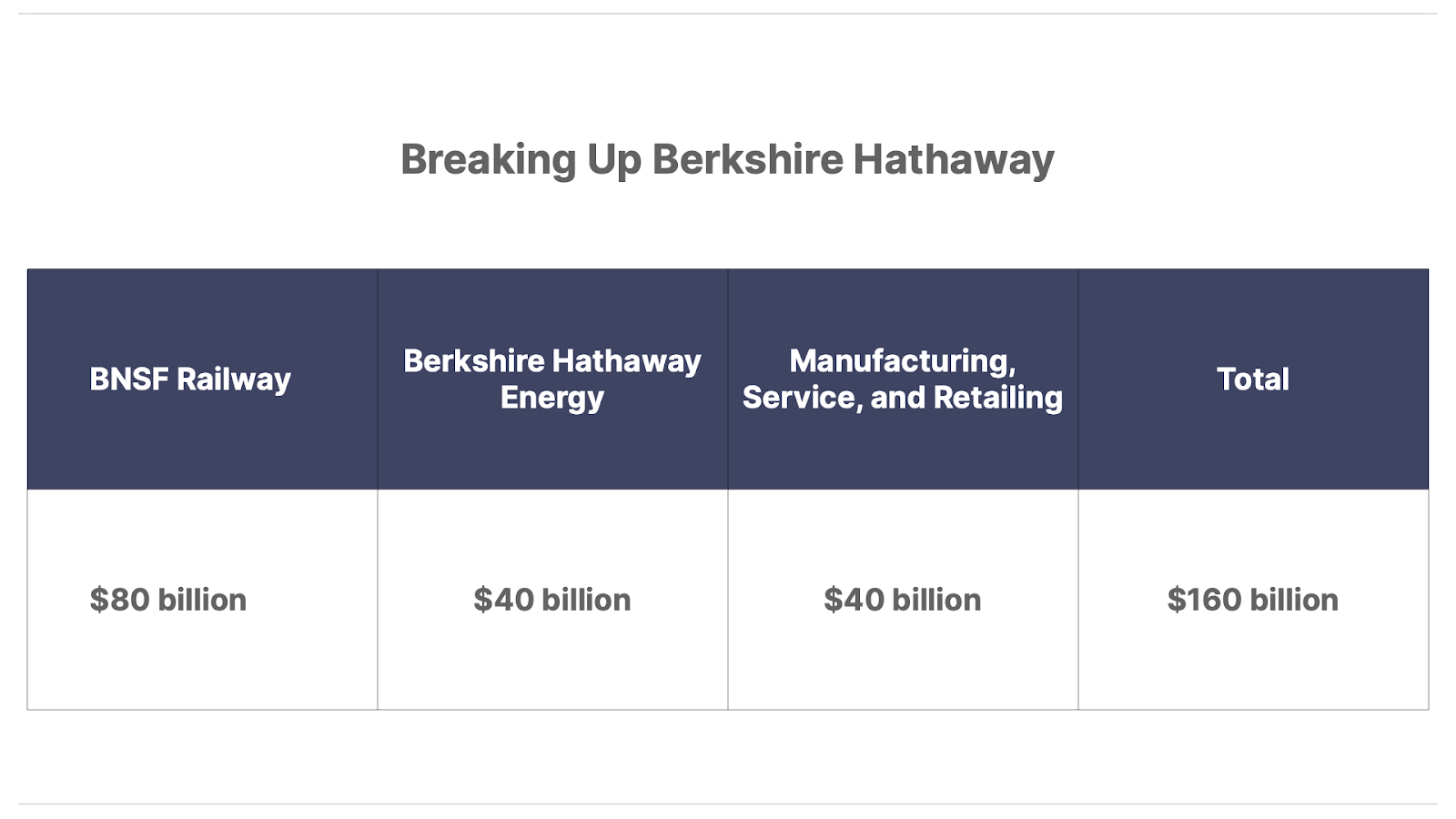

There are three units that could easily become independent businesses: BHE, BNSF Railway, and its Manufacturing, Service, and Retailing segment (“MSR”). The MSR unit is dominated by Precision Castparts, Marmon, and Lubrizol.

These business units could all be financed with debt, which would lower their costs of capital and increase their return on equity making them more valuable as independent businesses than they are today as units of Berkshire. (Because of Berkshire’s focus on property-and-casualty (P&C) insurance, it must retain large amounts of cash and remain primarily an equity-financed business.)

Spinning these companies off would allow Berkshire to return to its foundation as the world’s top P&C business and to focus on making great, long-term investments in capital efficient businesses, like Coca-Cola (KO), Apple (AAPL), and American Express (AXP). Doing so would allow Berkshire to vastly increase its return on invested capital, driving up its return on equity. That would push annual equity returns back to their previous 20%+ range and give investors a virtually guaranteed way to beat the market.

And because selling these businesses would generate so much cash ($80 billion for BNSF, $40 billion for BHE, and $40 billion for MSR = $160 billion in total), Berkshire could afford to pay a huge dividend, something around $300 billion.

Wouldn’t that be a wonderful way for Warren Buffett to retire? Paying a 30% dividend and “resetting” Berkshire for the next generation! That would be the greatest “drop the mic” moment in the history of the capital markets.

The “Buffett Indicator” Predicts Gold Is Set To Dominate For Next Decade

Each time the Buffett Indicator has hit extremes, it’s spelled doom for stocks – and soaring gains for gold. Today, the indicator is flashing a historic all-time high. Meanwhile, Buffett is quietly hoarding $325 billion in cash – and insiders believe he’s about to make a gold move big enough to shock Wall Street. Garrett Goggin has the names of four companies likely to benefit – if you move fast.

See why gold could dominate for the next 10 years — and how to get ahead of Buffett’s next big move.

Three Things To Know Before We Go…

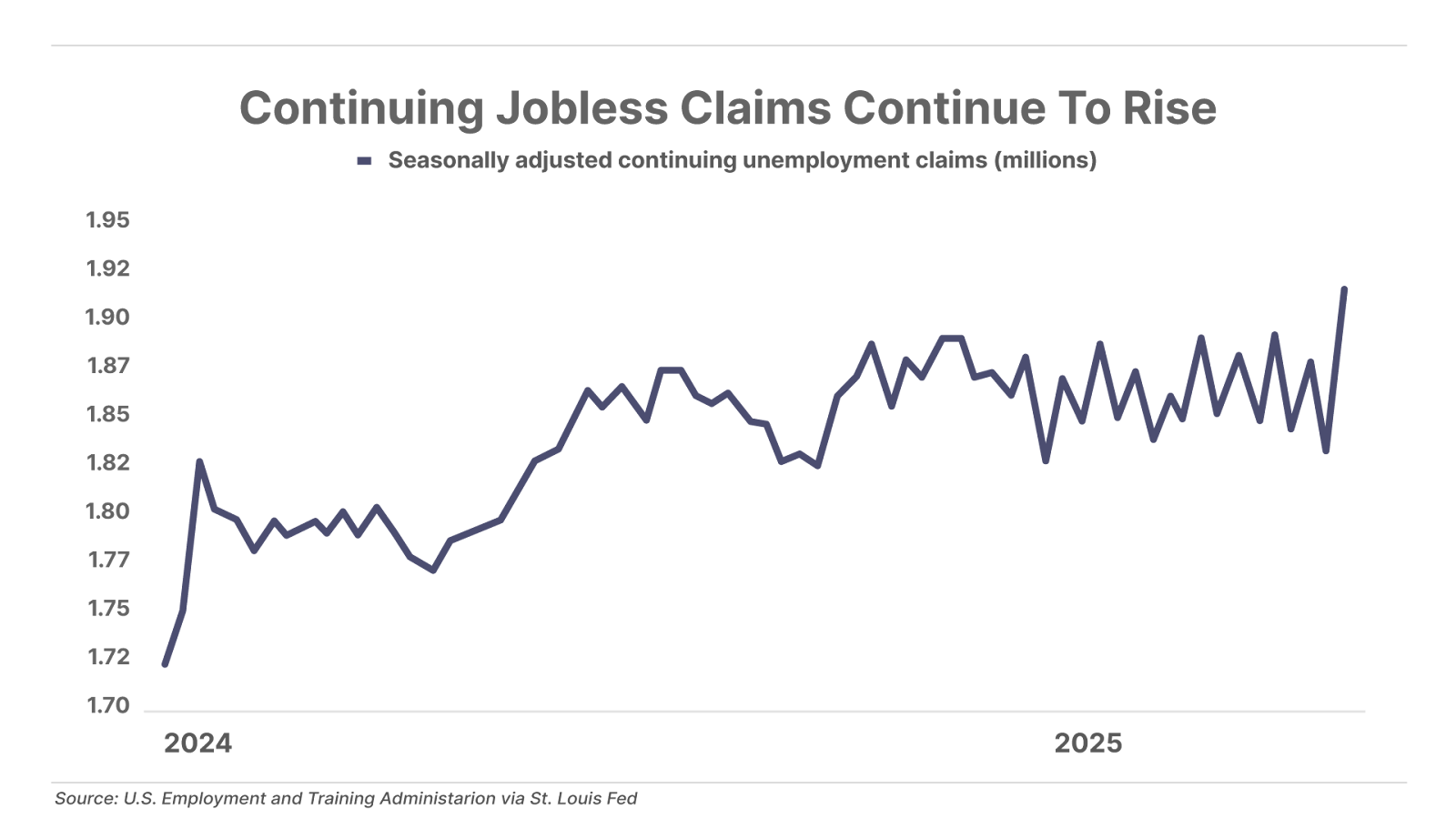

1. Rising unemployment reduces consumer spending. Jobless claims surged to their highest level since 2021, with continued claims rising to 1.92 million in April – a new post-pandemic high. Initial claims jumped by 18,000 to 241,000, well above the 223,000 forecast, showing that more people are entering unemployment. As job seekers struggle to find work, prolonged unemployment is slowing consumer spending, adding pressure to the economy amid growing uncertainty.

2. Only the rich can afford McDonald’s. In its latest Q1 earnings results, McDonald’s (MCD) reported a 3.6% decline in customer visits to their stores – the largest decrease since the 8.7% drop during the peak of the pandemic in Q2 2020. For the last few years, the fast-food chain has struggled with weak demand from low-income consumers. But in Q1, consumer weakness spread into middle-income burger eaters, where traffic fell by near double-digits. Now, the only demographic with stable demand for a Big Mac and fries is the high-income consumer. If only the rich can afford low-cost McDonald’s, it doesn’t bode well for the rest of the U.S. economy.

3. Another high-profile Boeing blunder. During his first term, President Donald Trump tapped Boeing (BA) to build two new Air Force One 747s – with the $3.9 billion planes expected to begin flying in 2024. Now the project is billions over budget and as much as a decade behind schedule, so Trump is looking to get Florida-based airplane-systems contractor L3Harris to retrofit a Qatari government 747 in the interim. Just the latest high-profile mishap from this once-great U.S. manufacturer, which most recently left two astronauts stranded on the International Space Station, only to be rescued by an Elon Musk SpaceX capsule.

And One More Thing… Today’s Survey – Trading Platforms

Mailbag

Dear Porter,

I am so excited by Wednesday’s Daily Journal about selling puts on shares of The Hershey Company (HSY).

I have used this in the past but have never had complete confidence to pursue it on my own.

Your precise explanation of how you analyzed this trade made it so clear to me. Thank you very much for that!

Your “sense of proportion for position sizing” is also extremely helpful.

I am really looking forward to the Porter & Co Trading Club.

Sincerely,

Bob J.”

I will never forget the articles about selling puts you wrote years ago. It changed my investing life. I would say that 95% of the investments I make now are puts. I end up buying very few shares of stock.

Thank you. Neil S.”

I went into my Fidelity account and followed your instructions. I had to do an application online to get approval for options trading, which took less than a day. I followed your directions, and it was very easy and simple to sell Viper Energy (VNOM) August 15, 2025, contracts. I appreciate the advice and can’t wait until Porter & Co. Trading Club starts.

Thanks, Jeff F.”

As always, tell me what you think: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland

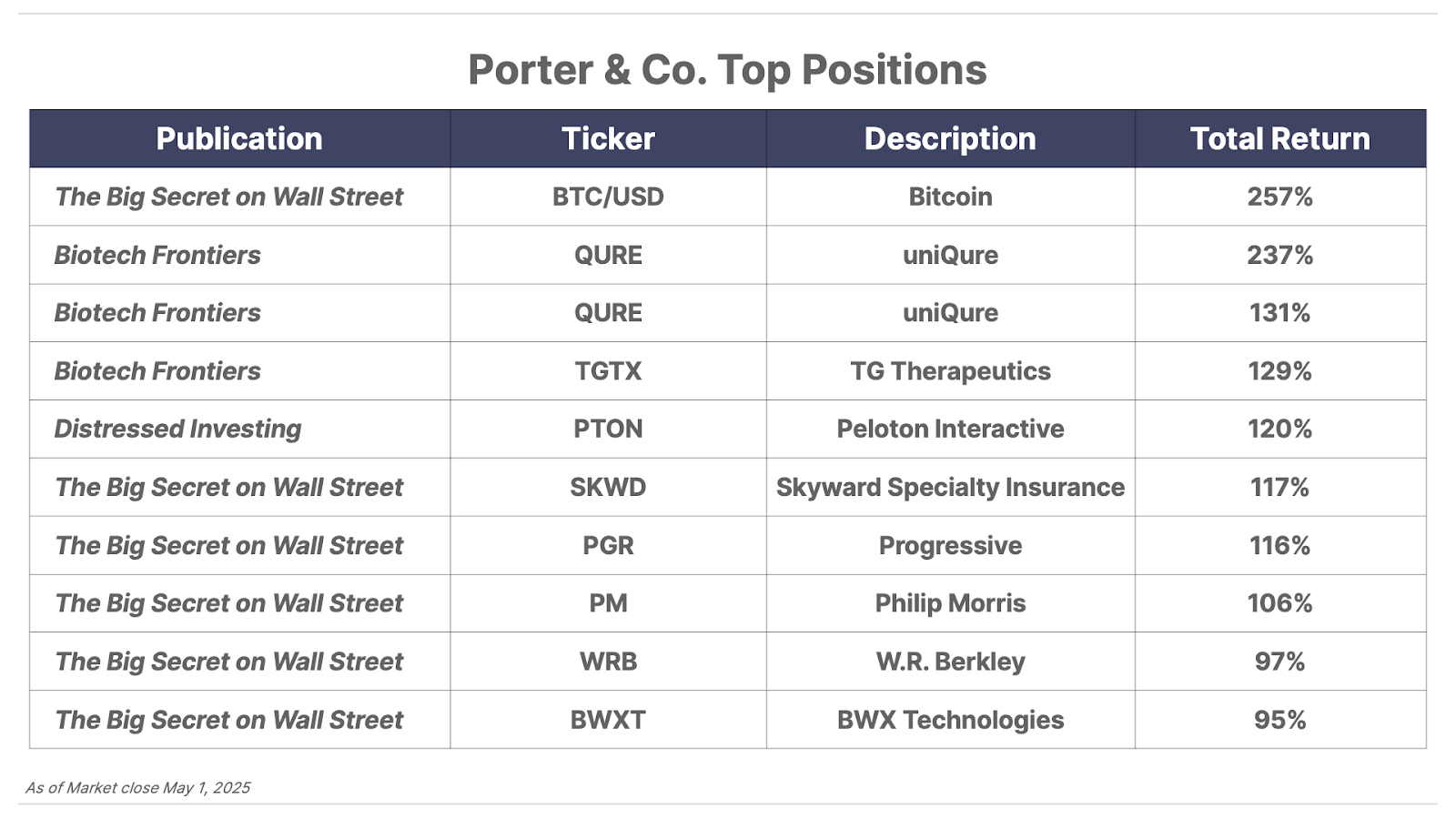

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.