Issue #16, Volume #2

How Philip Morris Turns Debt Into Brand Value

This is Porter & Co.’s free e-letter, the Daily Journal. Paid-up members can access their subscriber materials, including our latest recommendations and our “3 Best Buys” for our different portfolios, by going here. Recent issues of the Daily Journal are here.

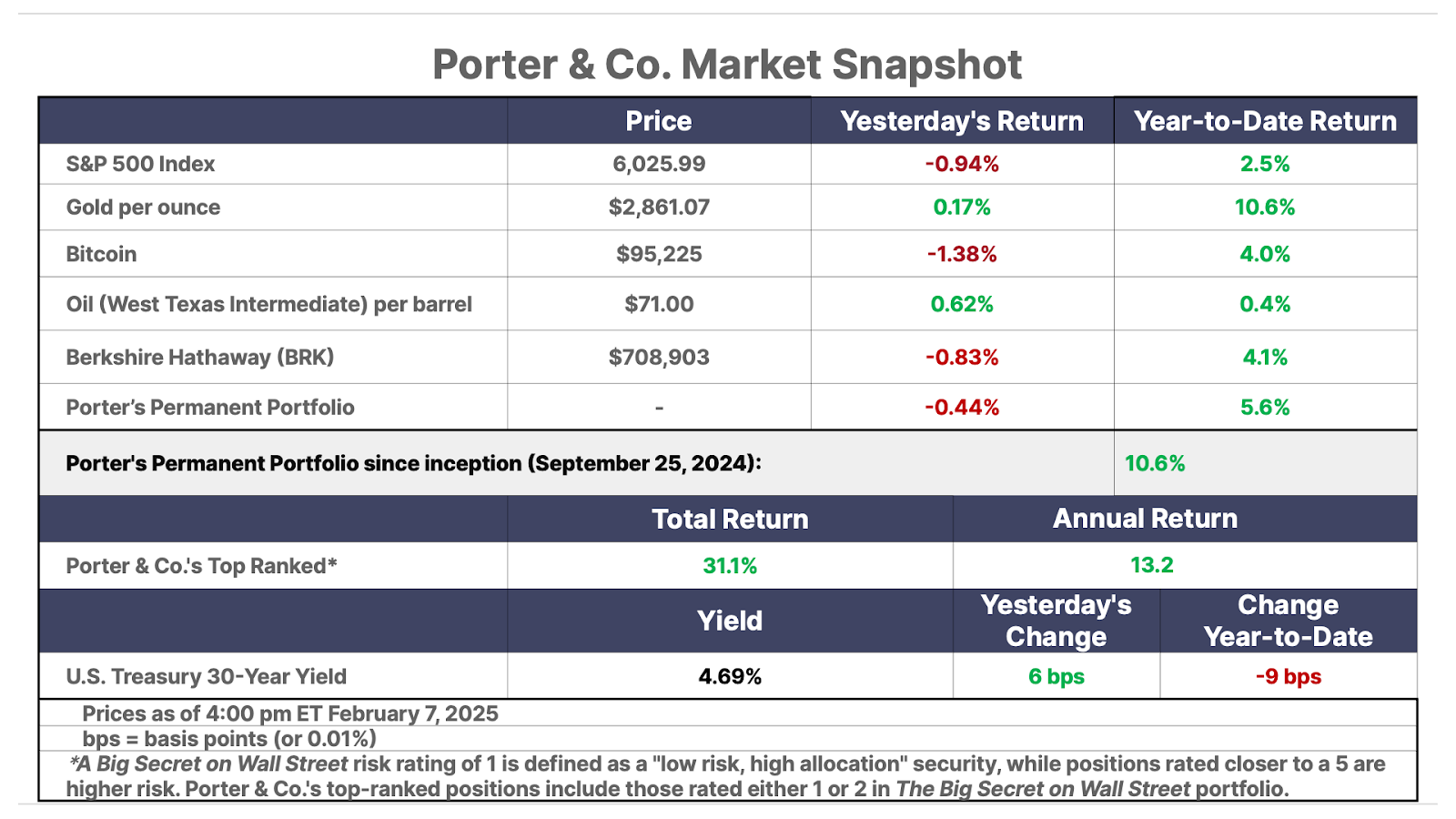

| Explaining return on equity (“ROE”) and why it matters to Philip Morris’ debt… Why Philip Morris’ debt is not as large as it seems… The China-U.S. trade war escalates – for now… The price of gold nears $3,000 per ounce… |

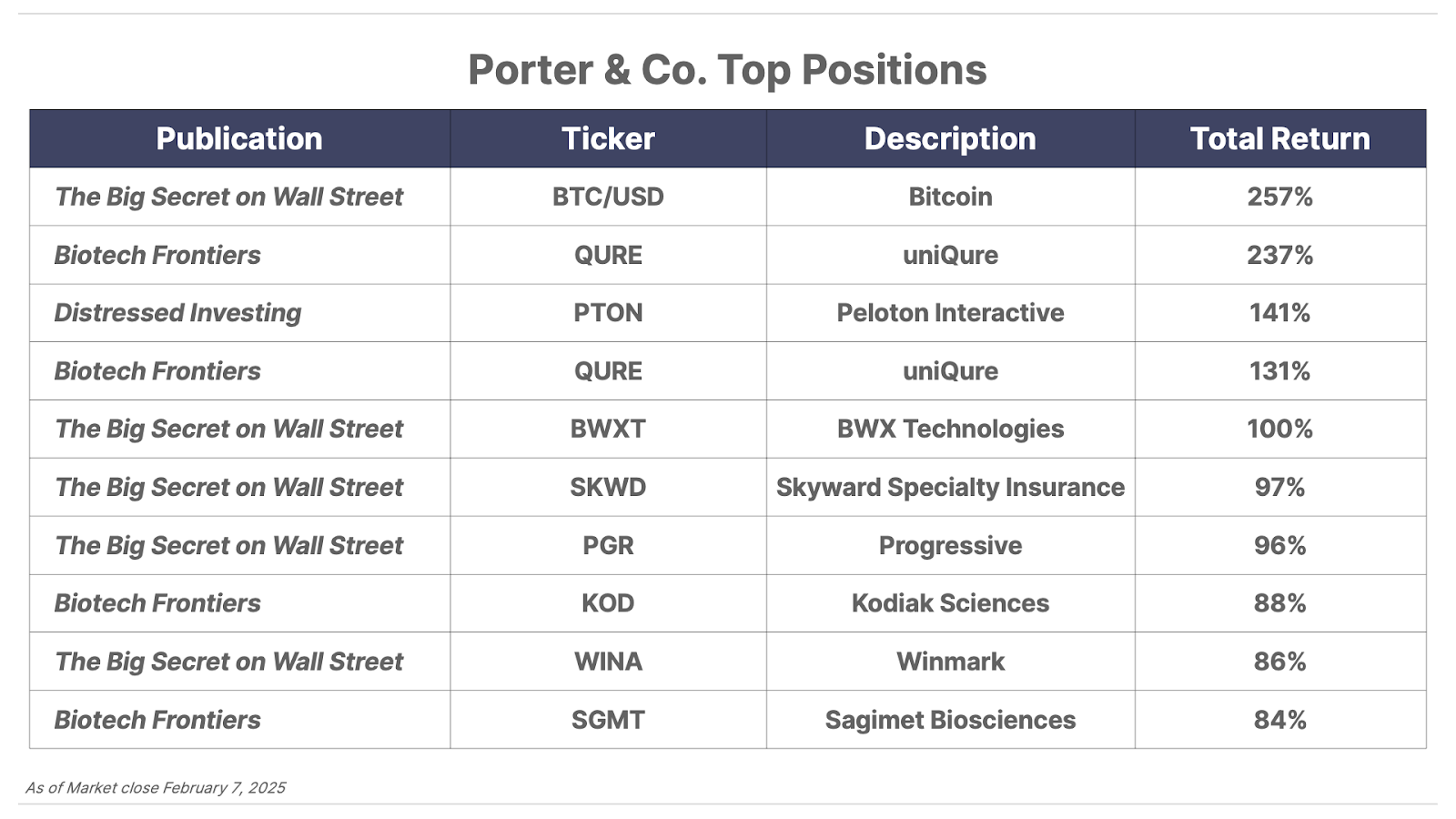

In The Big Secret on Wall Street, Porter & Co.’s flagship publication, we focus on capital efficient stocks. The core of our portfolio is world-class businesses that prioritize returning significant cash to shareholders. In our view, this is the simplest and surest road to permanent wealth. And one of the most important indicators of capital efficiency is return on equity (“ROE”).

Some of our most popular issues of the Daily Journal are those in which Porter leads a masterclass in investment analysis (see, for example, his dissection last week of Google’s recent earnings results – and the comparison of the high-tech titan to a boring old bricks-and-mortar business). Longtime readers will recall one of Porter’s favorite sayings: “There’s no such thing as teaching – there’s only learning…”

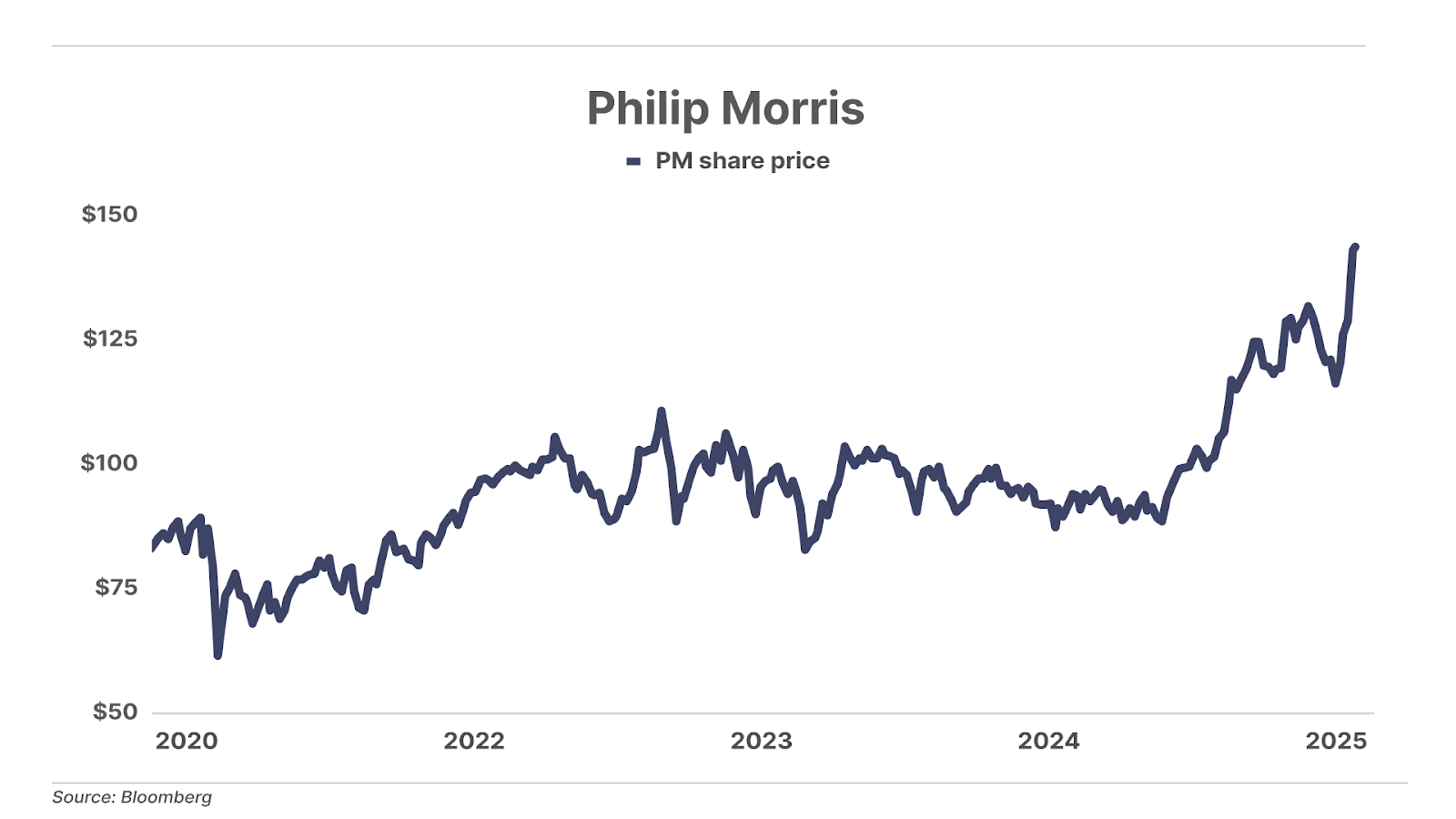

Today, Porter delves into the ways that companies can increase ROE – and in particular, the role of debt. Nicotine company Philip Morris International (NYSE: PM), a stock that we recommended in July 2022 in The Big Secret (the shares are up 75% since then), is one of Porter’s all-time favorite companies… and it has a high level of debt, and negative equity. Porter explains what it all means, and why debt comes in different flavors, in response to a question from paid-up Big Secret subscriber Jay R.

This is from Jay R.:

Hi Porter,

This is my first time writing to you. I am a Big Secret lifetime member and have really enjoyed the six months since I signed up. I’ve learned quite a lot in addition to being thoroughly entertained by your colorful and refreshing writing style. I am new to trying to actively manage my assets (I used to be an S&P 500 indexer, 100%). So, the educational side of what you do is much appreciated.

At any rate, I’ve acted on three of your stock recommendations, including Philip Morris International. That is obviously working out quite well, so….many thanks!

There is one aspect of Philip Morris, however, that is nagging me: its rather large debt load and negative equity. I’m a big fan of Warren Buffett (who isn’t?) and, of course, he’s all about return on equity (“ROE”), as are you. So, it makes me nervous to have a sizable bet on a company, even one with the storied profits history of Philip Morris, with $49 billion in debt (not quite 4x earnings), which includes an $8 billion debt increase since 2023.

I know ROE isn’t everything, and can be “gamed” like any other stat. For example, I suppose Philip Morris could easily have super-high ROE simply by paying down just enough debt to have, say, $2 billion in equity, at which point its ROE would go through the roof, right?

So, I’m just trying to think through the relative importance of its debt and wondered if you have any thoughts, since you have such a high conviction about it?

Jay R.”

Porter replied…

Jay –

This is a great question and I appreciate the opportunity to discuss finance with an intelligent and thoughtful subscriber.

ROE is supposed to measure the rate at which a company’s equity is compounding. Great businesses have the ability to compound their equity at a fast pace… which leads to a rising share price.

As I’ve mentioned, there are three well-understood ways to produce higher returns on equity: increase gross margins, improve asset turns (meaning, increase sales volume relative to assets), or add leverage to the balance sheet, which has the impact of reducing equity.

Lots of consultants over the years have made fortunes by telling CEOs to cut overhead by 50%, cut prices by 25%, and add 33% of debt to the balance sheet.

Those steps will immediately increase margins, increase sales volume, and decrease net assets — resulting in soaring ROE.

In regards to debt, investors should look carefully at how it is being used and whether or not it can be repaid.

The first question must always be: is the company growing? A company that’s only increasing ROE because it’s simply buying its own stock with debt (like GE did for many years) is a situation that will not end well.

On the other hand, a company that’s investing heavily in growth (like Philip Morris) will spend a lot on capital investments and acquisitions, etc. If that company can maintain its margins and its returns against a growing asset base, that’s a good business. And if a company can do that while using debt to grow, then it’s probably a great business.

In the case of Philip Morris, their core business is so attractive that they’re able to finance all of their growth and most of their overhead with debt.

This isn’t Enron-style debt. There are long-term, fixed-rate bonds… that cost the company almost nothing.

I’m going to give you a bunch of details. I hope these details will help you understand what’s so special about this business. But, all you need to know is: PM turns debt into brand value. And that’s a heck of a business.

The big increase in debt you noted at Philip Morris is related to the 2022 purchase of Swedish Match (which developed the blockbuster nicotine pouch Zyn). PM bought Swedish Match for $16 billion. It also bought the U.S. rights to IQOS, a device that heats tobacco without burning it, from Altria for $2 billion in the same year. Adding $18 billion in debt is a big deal.

But… since then, Philip Morris has already repaid over $34 billion in debt and continues to reduce debt loads by $10 billion a year. (No, that’s not a net figure, it has added debt too. But overall, debt is falling.)

Okay, so why so much debt? Because this company requires a lot of capital.

PM owns $10 billion in inventory. And it keeps almost $5 billion in cash. It requires a lot of working capital. It also owns lots of real estate all around the world – almost $10 billion worth of property and improvements. So, that’s $25 billion in real, tangible capital. It also owns $25 billion worth of intangible capital – brands, customer lists, purchase agreements, etc.

PM finances most of these operating assets with “float” – short-term loans from suppliers.

It has at any given time, about $16 billion “on the street,” meaning obligations it owes in 90 days.

Using vendors and suppliers for so much capital is a huge advantage for Philip Morris – an advantage it gets because of its scale, the quality of its brands, and its long history of operating successfully. This $16 billion counts as debt, but it carries zero interest rate. So… using “float” Philip Morris finances most (64%) of its tangible capital needed for operations. That’s a big advantage in business.

On top of that, Philip Morris carries $42 billion in long-term debt.

As I mentioned, about half of this was added in ’22 and ’23 and is related to key acquisitions – Zyn and IQOS in the U.S., plus a handful other small deals.

These are growth investments.

And here, once again, Philip Morris is able to use debt, instead of equity. Total shares outstanding (1.5 billion shares) haven’t moved in more than a decade. That means that Philip Morris shareholders aren’t being diluted. And PM won’t have to pay extra dividends to new shareholders forever. All it has to do to grow its earning base substantially is repay the debt. It gets to repay the debt with the assets (Zyn, IQOS) it now owns.

Think of the amount of capital that PM controls like a form of financial gravity.

The more capital, the stronger the firm’s gravity. The more suppliers, retailers, inventory, salespeople, products … and revenue and profits.

The question is, how cheaply can PM add to that “gravity.”

What Philip Morris does is take debt (tangible capital) and transform it into brand value and other forms of intangible capital.

And that explains the business’s incredible ROE.

Looking at all of the debt – short-term, long-term, deferred taxes, current taxes, current portion of long-term debt, etc. – that all adds up to a total debt load of $71 billion!

That’s a huge amount of “gravity.” But the thing to focus on is the stuff that Philip Morris actually pays interest on, and that figure is around $45 billion. And is dropping at $10 billion per year. After another year or two, PM will stop reducing debt. Why?

Because, on $71 billion in total debt, it is only spending $1.1 billion on interest, on a net basis. That’s a 1.5% blended interest rate.

Looking only at tangible capital (not including goodwill and intangibles) PM is earning $7 billion a year on tangible assets of $25 billion. That’s 28% a year.

In other words, PM makes a great return on its tangible assets. And it buys them with very cheap debt.

That’s a great business – probably the best in the world.

Hope this helps!

(A major focus of the portfolio of The Big Secret is on companies similar to Philip Morris: world-beating, capital-efficient powerhouses that we often recommend buying (… at the right price…) and holding forever. To learn more about The Big Secret, go here, or contact Lance James, our Director of Customer Care, at 888-610-8895, internationally at +1 443-815-4447, or via email at [email protected].)

Three Things To Know Before We Go…

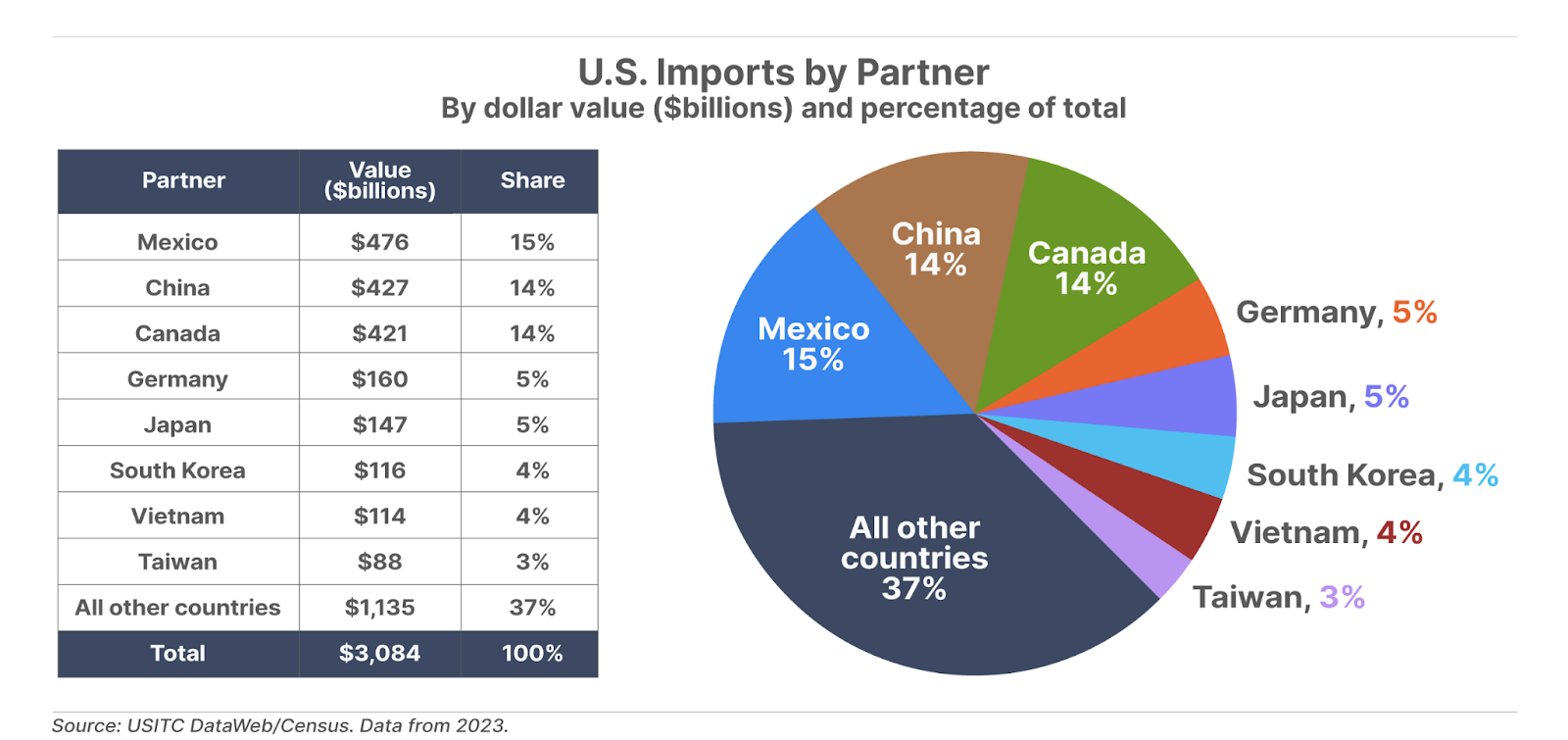

1. Trump escalates trade war. Yesterday, President Donald Trump announced plans to implement a 25% tariff on imports of steel and aluminum to the U.S., though he didn’t say when. This followed last week’s imposition of tariffs on imports from Canada, Mexico, and China – though deals were announced to pause tariffs on Mexico and Canada. Trump also said he will announce reciprocal tariffs on any countries that impose import taxes on U.S. goods flowing into foreign countries. This sets the stage for a trade war with China, which in 2023 was the second-largest importer of goods into the U.S. (followed by Canada… Mexico was the largest).

2. China hits back. In response to the U.S.’s newly imposed tariffs on Chinese imports into the U.S., China vowed to impose retaliatory tariffs of 10% to 15% on U.S. imports of crude oil, natural gas, farming equipment, and other products. Both countries could be setting the stage for a deal. China, for one, appears open to lowering tensions. In a news conference earlier today, Chinese Foreign Ministry spokesman Guo Jiakun said that there are no winners in a trade war, and noted the need for “dialogue and consultations based on equality and mutual respect.” (In last week’s The Big Secret On Wall Street, we explained why tariffs are a terrible idea… and how to protect your portfolio.)

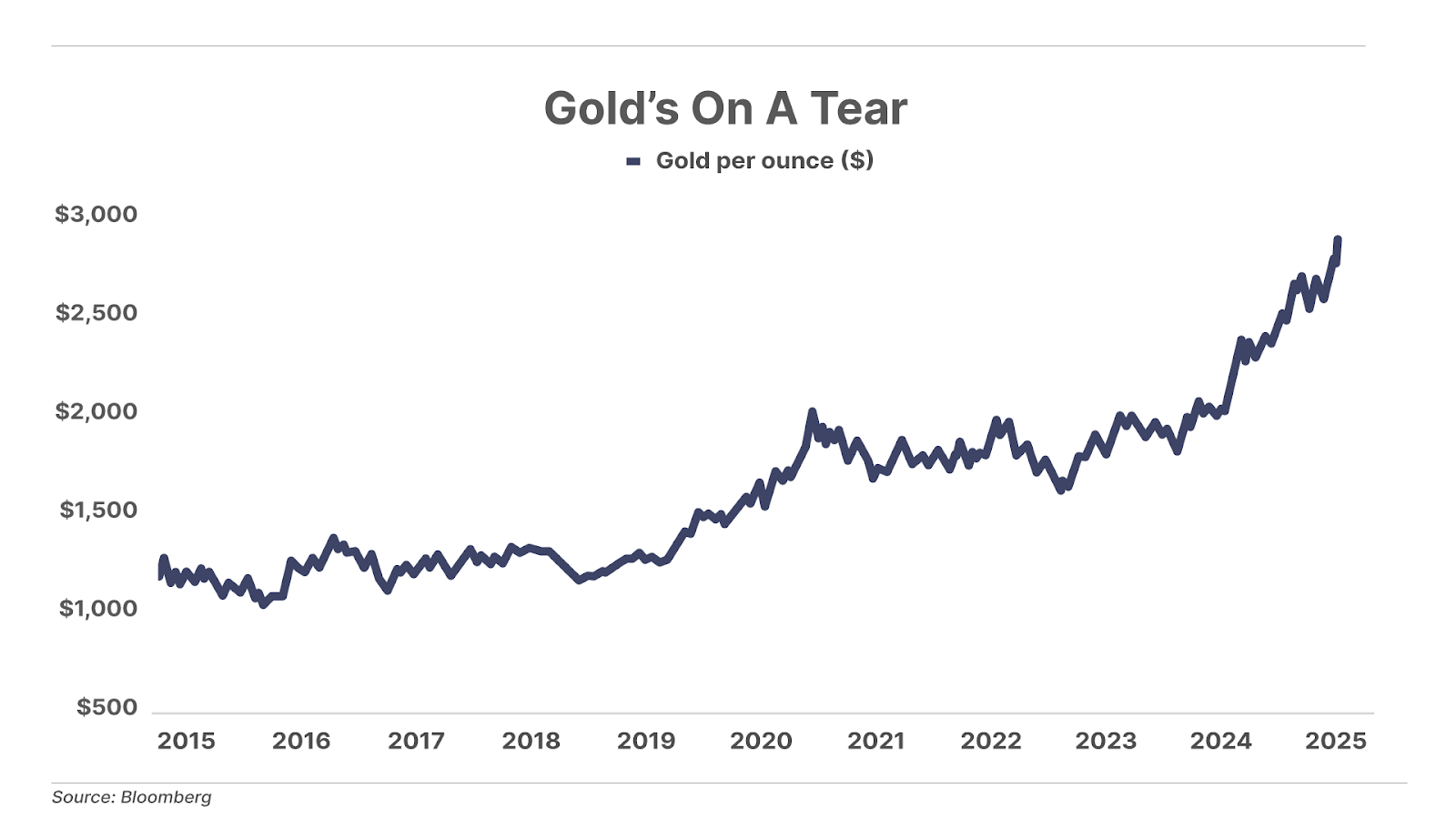

3. Gold rally continues. Gold traded above $2,900 per ounce for the first time in history today. The precious metal is now up 43% over the past 12 months – roughly double the returns of the S&P 500 (+21%) and Nasdaq 100 (+23%) indexes over the same period – and is quickly closing in on $3,000 per ounce. Gold is benefiting from a “perfect storm” of inflation fears, runaway government debt, and potential tariffs.

And one more thing… Today’s Poll

Philip Morris International was the best-performing stock from 1927 through 2021 generating a 16% annual return. According to Jeremy Siegel’s sixth edition of Stocks For The Long Run, this makes Philip Morris the best-performing stock of original stocks that were public in 1926, and significantly better than the 10% average return of the S&P 500 since its inception in 1926 (Philip Morris was a subsidiary of parent company Altria until March 2008 when the two companies split). Since 2021, Philip Morris’s strong performance has continued, as the shares have risen by 79% (compared to the S&P 500’s rise of 33%).

Coming up this week: Inflation data and rates intel.

On Wednesday the Bureau of Labor Statistics will release January consumer price index (CPI) numbers, which are expected to show a modest rise in inflation (up 0.3% on a monthly basis) – but probably not enough to impact Fed policy. On Tuesday and Wednesday, Fed Chairman Jerome Powell offers his two-day congressional testimony, where he’ll discuss the impact of Trump policies and tariffs on potential rate changes. Futures traders are pricing in a 92% chance that rates will remain steady at the next Fed meeting on March 18. Finally, on Friday, January retail sales data is expected to show an increase of about 0.4%, down from 0.5% growth in December.

In Case You Missed It…

In Monday’s Daily Journal, Porter tackled a question we’ve been getting a lot: In light of the California wildfires and other events that cost a lot of money… are insurance companies in trouble? Porter explained why he continues to invest in property & casualty insurance companies…

In Wednesday’s Daily Journal, Porter dug into the recent earnings of Google (GOOG) to discover that the search-engine giant isn’t so profitable after all… and Porter revealed one boring, old-school company that is startlingly capital efficient will be a better long-term investment.

On Thursday, Erez Kalir in Biotech Frontiers took a break from the biotech sector – where he’s served up a long list of incredible picks, with the portfolio up 41% in 2024 – to focus on a crypto-related company that he calls “the next MicroStrategy.”

In Friday’s Daily Journal, Porter wrote that it’s not inconceivable for both weight-loss-drug maker Novo Nordisk (NVO) and chocolate maker Hershey (HSY) to co-exist… and for both to succeed.

And check out our new weekend editions… Saturday Stock Screen, this time featuring Porter’s 3x Screen, and Sunday Investment Chronicles, which digests all the financial research and insight we’ve consumed from the previous week into this 2025 version of the Sunday paper.

Good investing,

Porter Stansberry

Stevenson, MD

P.S. In October 1987, Mason Sexton made a ridiculously good prediction about the Black Monday crash – 11 days before it happened.

The Economist said that he “could be the new guru.”

Mason, though, wasn’t interested in the notoriety that goes along with that kind of fame, though. So… he vanished from the public eye.

Meanwhile, though, continued to make astonishing market calls for his private clients. In March 2008, called the bottom of the Global Financial Crisis crash.

And in early 2020, he warned that the top was in, and that it was time to sell… right before the Nasdaq collapsed by 36%.

And now… Mason has agreed to return to talking about his calls in public. And he believes that something big – very big – is brewing in markets within the next two months.

So big… that he’s calling it The Prophecy. He reveals in a special interview what he sees happening… when it all will start… and what you can do to prepare.