Issue #122, Volume #2

And Win At It Before Anyone Else Knows It Exists

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| The world’s greatest investor… Hired PhDs not MBAs… Played a different game… He cracked the code… Two biotech gems… Amazon hires robots… Philip Morris shares drop… |

Today, Porter turns the Journal over to Erez Kalir, editor of Porter & Co.’s Tech Frontiers.

Erez has degrees from Stanford, Yale, and Oxford, has studied biology, finance, and law, and has worked at McKinsey & Co. and for Julian Robertson at Tiger Management. Porter & Co. has recently expanded the domain of Erez’s investment research to include tech stocks, the blockchain, and science beyond his original focus of biotech.

Four of the 12 open positions in the Tech Frontiers portfolio are up 2x or more since he recommended them. There are three more that doubled before he suggested selling them to take gains. Overall, the portfolio is up 57% since he launched it last year. In today’s Journal, Erez discusses two of those biotech gems…

Who is the greatest professional investor of all time?

Ask the average person and they’ll likely answer Warren Buffett. Buffett, after all, built Berkshire Hathaway into a trillion-dollar global empire based on successful investments, compounding its stock at roughly 20% annually for nearly six decades – a feat few have matched, especially with the huge amount of capital that Buffett has to manage. A savvier interlocutor might suggest Stan Druckenmiller, who compounded the funds he managed at 30% annually over three decades without a single down year.

But true professionals know there is only one correct answer: the late Jim Simons, the legendary mathematician who founded and built Renaissance Technologies (“RenTech”). Since its inception in 1988, Simons’ Medallion Fund has compounded at 66% annually before fees – an almost mythical return that has never been matched or even approached by any hedge fund in history. His achievement is so extraordinary it lives in a different statistical universe.

Jim Simons was no ordinary hedge fund titan. Before turning to finance, he had already achieved more than most academic scientists do in a lifetime. Simons earned his PhD in math at U.C. Berkeley, taught at MIT and Harvard, then became the chairman of the math department at Stony Brook University in New York. Along the way, he made major contributions to differential geometry – most famously the Chern-Simons theory, still widely cited in theoretical physics and string theory today.

When he eventually turned his primary focus to investing, Simons adopted a principle that would define his career: Renaissance Technologies would not hire anyone with a traditional background in business or finance. Instead, Simons recruited scientists – PhDs in fields like astrophysics, computer science, and symbolic systems. Many were tenured academics. Others were codebreakers, mathematicians, and natural language experts poached from America’s top private-sector research labs, such as IBM.

As Gregory Zuckerman chronicles in The Man Who Solved The Market, his biography of Simons, the culture at RenTech evinced no trace of Wall Street. Instead, it resembled a close-knit university department. Traders and analysts were replaced by physicists and cryptographers who spent their days building models to decode patterns buried deep in market data.

Simons’ success can be distilled into one lesson: find a different game.

For nearly a century, most investors have fought the same battles. They’ve divided themselves into tribes – value investors, growth investors, momentum traders – and competed to identify cheap or promising companies faster than the next guy. Buffett’s disciples alone number in the tens of thousands. But as Buffett himself has acknowledged often, every one of these games has grown brutally efficient, crowded with competitors armed with the same information and fighting for the same marginal edge.

Simons ignored all of it. He treated the market not as a story of human psychology, value, or growth – but instead as a code that could be cracked, a set of mathematical patterns and probabilities hidden in plain sight. His firm’s weapons weren’t analysts pouring over financial statements to identify capital efficient businesses that the market underpriced. Instead, they were cryptographers interrogating reams of data, then formulating and testing algorithms with code. In short, Simons found a different game, one that he could (and did) dominate.

That same principle – find a different game – is perhaps the most powerful investment lesson of all. And it applies far beyond hedge funds.

Take the AI mania unfolding in markets today. Most investors chasing artificial intelligence (“AI”) are focused on the obvious plays. The first group are the AI builders – companies like OpenAI, Anthropic, and Mistral, each racing to build the most powerful foundation models. These companies already command staggering valuations that will likely prove challenging for them to justify over the long run. For example, OpenAI’s last private financing round valued it at north of $500 billion, but the company is still a hybrid non-profit – making the path to an attractive return for its recent investors uncertain to say the least.

A second well-known group are the AI enablers, the picks-and-shovels plays. These include Nvidia (NVDA), whose GPUs are the chip-based engines of the AI revolution, and the cloud hyperscalers like Microsoft (MSFT) and Amazon (AMZN) that power AI infrastructure. These companies, too, already command astronomical valuations.

Both games are crowded. Both have already attracted trillions of dollars in capital.

The different game is being played elsewhere – by companies that are neither building AI nor selling the tools to build it… but instead applying AI to transform their existing businesses and deepen their moats.

Take Vinted, the European online marketplace for secondhand fashion. On its surface, Vinted looks like a niche resale platform, a continental cousin to Poshmark. But its real strength lies beneath the hood: Vinted is applying AI to translate listings between dozens of languages in real time, enabling a Lithuanian seller to transact seamlessly with a French or German buyer. Even more powerfully, Vinted has trained machine-learning models to assess millions of live listings and generate real-time pricing recommendations for sellers.

That means buyers see fairer prices, sellers move inventory faster, and Vinted takes a larger share of a growing pie.

By applying AI not to invent something new but to supercharge its existing business, Vinted is carving out a moat that’s invisible to most competitors. Investors seeking a different game in the domain of AI should be focusing on these kinds of companies – “AI appliers” that are using the power of AI to cement their status as winners.

The opportunity to find a different game exists in biotech as well.

The traditional biotech game is discovering, developing, and commercializing new drugs. Not surprising, this is a brutally competitive field, dominated by Big Pharma giants and populated with thousands of smaller biotech companies chasing similar targets. Hundreds of these smaller companies fail every year.

But a tiny handful of firms have found a different game – an exceptionally lucrative one that’s virtually devoid of players.

Two of these companies are in the Tech Frontiers portfolio.

Instead of trying to discover new drugs, these two players treat the entire research-and-development (R&D) ecosystem of global pharma as their hunting ground. Their strategy is simple but brilliant: sift through the discard piles of Big Pharma and academic research labs – the thousands of drug candidates gathering dust on the shelves for non-scientific reasons – and identify the overlooked gems.

Big Pharma spends over $350 billion a year on R&D. Yet only a minuscule fraction of these efforts ever reach the market. Many abandoned compounds “fail” not because they’re scientifically unsound, but because they fall out of strategic favor, lose an internal champion, or get shelved after a merger.

The two companies in our portfolio have each built proprietary databases of these discarded compounds and use rigorous analytics to rank their potential. But their method of search is about to greatly improve.

Today, their efforts to catalog, sort, and sift through the “drug-ome” – the universe of therapeutic compounds worldwide that already exists – is being supercharged by AI. When these companies find a promising discard-pile candidate that meets their criteria, they seek to negotiate a license at a compelling price. Because, by definition, they’re focusing on shelved compounds, they’re often able to do so.

In 2021, for instance, one of these two companies licensed a stalled Pfizer (PFE) compound for $45 million. Ten months later, after a successful Phase II trial, they flipped that compound to Pfizer’s Big Pharma competitor Roche (RHHBY) for $7.1 billion – a greater than 100x return in less than a year.

When you earn more than 100x on a $45 million investment in less than a year, you’ve clearly found a different game.

Most of us, alas, cannot emulate Jim Simons and build our own RenTech. But we can learn from his success and apply his most essential lesson to the domains of AI, biotech, the blockchain, and beyond: In markets, as in life, “edge” rarely comes from being slightly better at the same game as everyone else. It comes from finding an entirely different one.

The mathematician who became the world’s greatest investor understood that first. Whether you’re building a hedge fund, a technology business like Vinted, or a biotech empire, the playbook is the same:

- Find the unplayed game

- Play it with precision and discipline

- Win it before everyone else notices it exists

If you want to succeed in investing – or in any field where competition is fierce – take a page from Jim Simons’ book.

Find a different game.

Erez Kalir

Berkeley, California

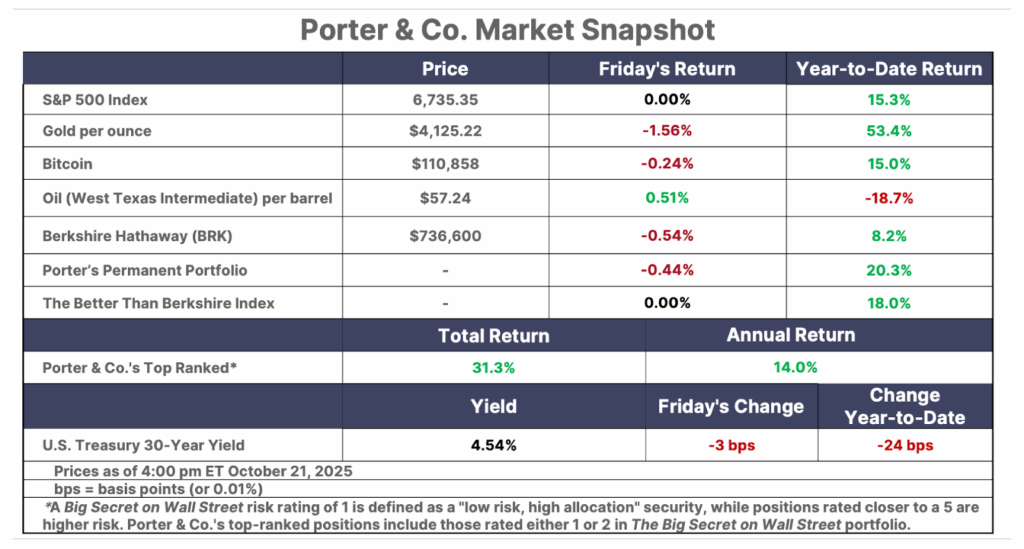

You too can play a different game… While everyone’s been transfixed by gold’s record-breaking run above $4,000 per ounce, and the trillion-dollar race to dominate AI – another bull market, hiding in plain sight, has been forming, which, months ago, Erez predicted would happen… Yet most investors are completely blind to it.

Porter & Co. CEO Jared Kelly sat down with Erez to explore why he predicted that this forgotten corner of the market was about to turn…

And, more important, why he believed it was about to unleash “one of the most powerful periods of wealth creation we’ve ever seen”… And why it will continue to run.

Click here to watch the conversation now.

“Biggest Breakthrough In the History Of Stock Trading”

A Maryland computer whiz recently unveiled a new form of “Super AI” that can foresee the future prices of any 2,334 stocks – to the day and even the penny – with 85% backtested accuracy. It’s led to a huge anomaly that turned every $100,000 into $702,190 in the last year alone in one study.

Click here to see how it works, including 2 free recommendations.

Three Things To Know Before We Go…

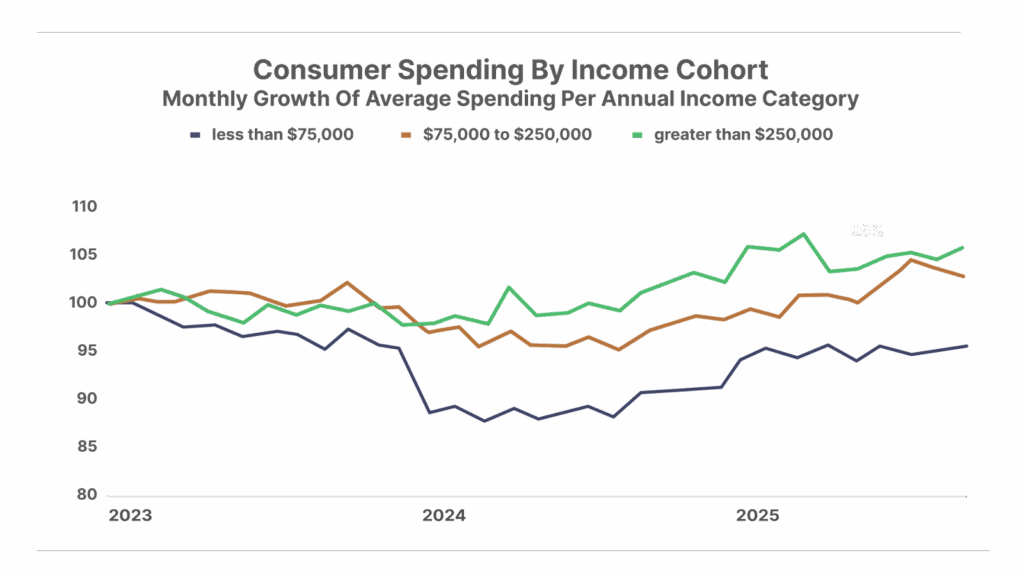

1. The “K-shaped” economy chugs along. Recent data suggest that the average U.S. consumer is doing OK, with consumer spending rising a better-than-expected 0.6% month-over-month in August. However, the rosy headline number masks a concerning divergence beneath the surface… As the chart below highlights, all the spending growth over the past two years has come from those with higher incomes – especially those earning more than $250,000 per year. Meanwhile, those earning less than $75,000 per year have cut their spending significantly.

2. Amazon brings in the robots. Amazon (AMZN) says robotic automation will cut down on 600,000 potential hires to its U.S. work force in the coming years, even though it expects to sell twice as many products by 2033. It plans to automate 75% of U.S. operations, with some warehouses not employing any humans at all. Amazon’s current work force has tripled to 1.2 million over the last seven years.

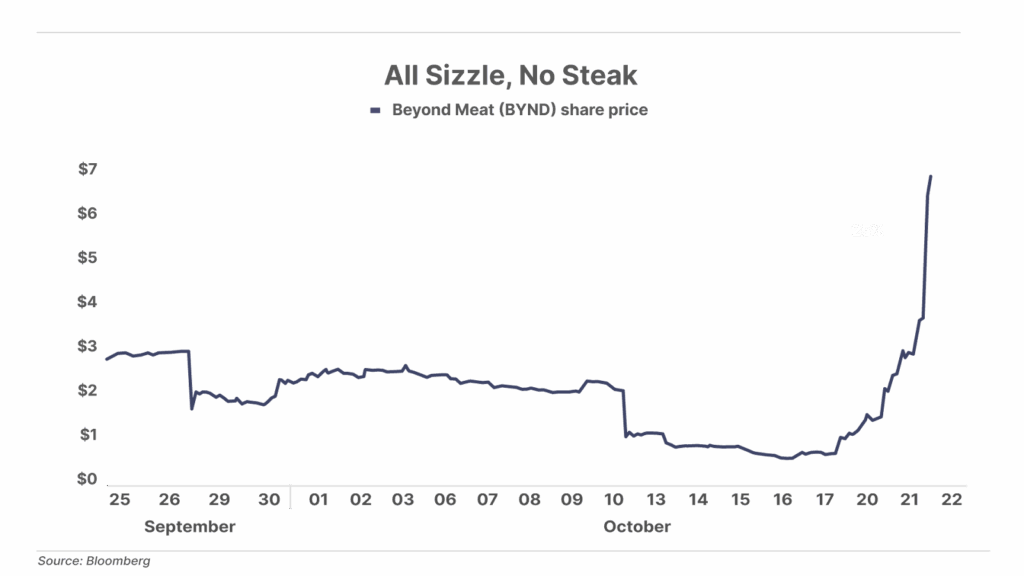

3. Beyond Meat – not beyond the bubble. Just six days ago, shares of Beyond Meat (BYND) hit an all-time low of $0.52. Since then, the stock has jumped more than 1,000%, trading above $7 this morning, though shares have retreated significantly since then. The initial surge was sparked by news of an expanded Walmart distribution deal – now reaching over 2,000 stores – and Beyond Meat’s addition to the Roundhill Meme Stock ETF (MEME). Despite the explosive rally, the underlying business remains weak: Beyond Meat is burning cash, burdened with over $1.1 billion in net debt, and has no clear path to profitability. The rise of Beyond Meat as a meme stock is just another classic sign of speculative excess – and a sign of a top.

Today’s Poll…

And One More Thing… Many More Puffs For Philip Morris

Yesterday, shares of Philip Morris International (NYSE: PM) dropped by as much as 10% despite reporting stellar Q3 earnings that included:

- Revenue of $10.8 billion, up 9.4% year-on-year (YOY)

- Earnings per share of $2.24, up 17% YOY

- Increase of full-year earnings guidance

- An 8.9% dividend increase

Investors appeared concerned about a modest $100 million increase in sales expense for a new ZYN nicotine-pouch marketing campaign in the U.S. that included price discounts, raising fears of a price war. We view this as an extreme overreaction for one of the world’s best businesses that delivered excellent results on both the top and bottom line. Shares recovered from the initial decline to close 4% lower on the day, and now trade at less than 20x next year’s free cash flow. We consider the recent decline to be a tremendous buying opportunity for long-term investors.

Tell me what you think: [email protected]

Mailbag

Monday’s Daily Journal focused on tariffs – leading with recent news that tariffs will add $1.2 trillion in new expenses for U.S. businesses this year.

Readers had varying points of view, some of which we share here.

Porter,

I don’t always agree with things you espouse but your tariff presentation is right on. Why the American public doesn’t understand this is just sickening and I guess the MAGA crowd is blind as a bat… Keep up the good work with trying to educate the many and the minority few.

Karl S.”

Why the hell Trump would impose tariffs on any country, especially our allies, other than the obvious reason when all it creates is a massive mess?

Colby O.”

Isn’t your explanation of who pays a little opaque? Who pays is a bit more complex. It is true that the importer pays to get the goods out of customs. But then could (and probably does if the manufacturer wants more orders) take a credit for that off of the manufacturer’s invoice. In the end, it is still a negotiation about margins at the source materials, manufactured goods, wholesale and retail levels. It is not as simple as you describe. The consumer is unlikely to absorb all of the tariff cost.

Roy A.”

Porter’s comment: Roy, I don’t think economics has ever crossed your mind. This is an immutable fact of economics: consumers pay all costs of production. Every last cent. All labor costs. All capital costs. And all taxes. Or else, production ceases. TANSTAAFL.

Continued solid work on the tariff issue. But there are some key points that are being missed:

In our chemical business, I can tell you that every single tariff has been eaten by the Chinese manufacturers. The likely reason is that they need to keep their facilities going and not open up the market to other countries.

The end goal is to bring more jobs back to the USA (as you know) to avoid the ongoing hollowing out of the middle class. When a company manufactures domestically, it opens up all sorts of opportunities, from manufacturing jobs to businesses that are generated around the manufacturing plant, sales jobs, technical jobs, etc. I’ve been in manufacturing businesses for 40 years and I’ve seen this play out consistently.

I’m not saying that the tariff policy has no downside, but I’m taking issue with your stance that it has virtually no upside.

Kevin L.”

Porter’s comment: How could there ever be any upside to a tax? In regards to your specific claim that these tariffs have a noble purpose (bringing jobs back to America) and so therefore they should be embraced, I’d be willing to bet every last penny of my net worth that the net impact of these tariffs (and the inevitable matching retaliatory tariffs) is a substantial loss in U.S. employment. Increasing the cost of production will not lead to more business activity – only less. And that means all forms of business activity, including, obviously, employment.

One final point. The purpose of the economy isn’t employment. That’s like saying the purpose of your car is to run the motor. The purpose of the economy is the creation of wealth through the elimination of our wants via production and distribution.

The economy that does this most efficiently wins – and also employs the most people in productive, profitable activities. Erecting barriers to more efficient means of production might produce more employment in certain segments of the economy, but they cannot possibly create more employment in total.

There are two core problems in the U.S. economy: paper money and the size of our government. The two problems are related. There’s no way to afford our government without a paper-money-based system of money and credit.

The middle class wasn’t destroyed through trade. It was destroyed by paper money and the relentless growth of wasteful government spending. In fact, it is deeply (and sadly) ironic that you (and many others) conflate the greatest source of our wealth (global trade) with the cause of our misery. The real cause of our country’s social decline and descent into radicalism and violence is a government that’s about 40% of GDP and a paper-money system that turns workers into debt slaves.

Good investing,

Porter Stansberry

Stevenson, Maryland

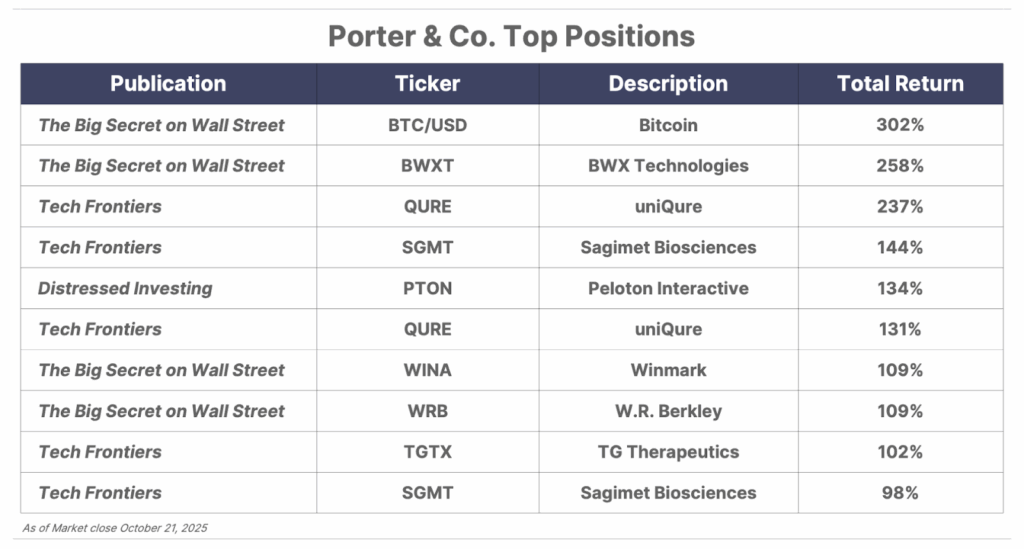

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call our Customer Care team at 888-610-8895 or internationally at +1 443-815-4447.