Financial markets have never had to reckon with a speculative asset mania, unsustainable bubbles in consumer, corporate, and sovereign debt, and structurally high inflation – all at the same time. The potential for significant economic turmoil is arguably greater than at any time in memory.

Why Most Americans (Especially the Middle Class) Are About to be Wiped Out

The Only Solution for America’s Massive Debts

Important Note: Summer Vacation starts now!

This is our last “regular” Big Secret issue until Friday, September 1.

Porter & Co. is a work hard & play hard, anti-woke place. After all, we work in a barn! But August is when we shut our engines down, recharge our batteries and give ourselves a break.

As long-time subscribers know, we don’t work in August! This is our policy. Call us European Socialists if you must, but we firmly believe that August is meant for time with friends and family. So, we give our staff extra time off this month to have their summer vacations and to work on other projects.

As for me (Porter), I’ll be with my new wife Shannon in her hometown (Halifax, Nova Scotia) enjoying a break from Baltimore’s stifling heat. I’ll be working on our next big project at Porter & Co… something we’re calling Activist Investor for now. We’ve hired yet another world class analyst with decades of experience to follow all of the ongoing proxy fights and activist campaigns in the market. Our goal: identify 3-4 excellent opportunities each year for big, near-term capital gains by following the world’s leading activist investors. These are situations with real catalysts that can earn you 50% – 100% in only a few months’ time. (See the big gains we made in Salesforce.com in Distressed Investing as an example of the kind of activist situations we’re looking for…)

There’s nothing like this kind of research product being published anywhere else and… because it’s coming from us… you’ll recognize the obsessive amount of research involved in each new campaign we cover for you.

Can’t wait to unveil everything for you in September. But, until then, our weekly standard (The Big Secret on Wall Street) will consist of some carefully selected classic material. We know you’ll enjoy seeing what we’ve picked for you. And we will see you again soon – on September 1. Let us know what you think: [email protected].

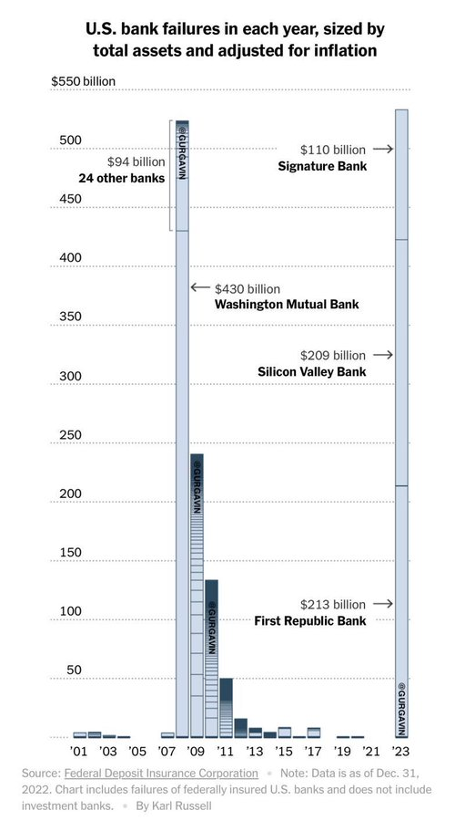

“They’re probably the tip of the iceberg.”

Stanley Druckenmiller – who famously earned 30% annualized returns for three decades without a single losing year – was explaining our country’s incredibly dire economic situation to Bloomberg.

He wasn’t describing a minor issue. He was talking about the largest bank failures since the Great Depression and the growing number of bankruptcies.

“Our central case is there’s more shoes to drop, particularly – in addition to the asset markets – economically. There’s a lot of stuff under the hood when you go from this kind of environment – the biggest, broadest asset bubble ever – and then you jack interest rates up 500 basis points in a year. I think the probability is that [the recent failure of] Silicon Valley Bank, [the bankruptcy of] Bed Bath & Beyond – they’re probably the tip of the iceberg.”

Nobody seems to care that our economy is falling apart and that our government has completely lost control of its finances. Why? Because with endless fiscal deficits and a never-ending stream of Washington’s free money policies, nobody has lost their jobs yet. What the poor saps haven’t figured out is that all of that free money is destroying our purchasing power and will soon completely wipe out the middle class.

Just look at the soaring cost of buying a car or buying a home. The average monthly payment for a new car is now $733, compared to just $562 in 2019, according to auto appraiser Edmunds. The average mortgage payment has nearly doubled over the same period.

If you think our politics are toxic now, just wait another decade. By that point, no one but the very rich will be able to afford a home or a decent car. By that point, virtually every new neighborhood will be owned by a New York bank and the entire middle class will be transformed into lifetime renters… and car sharers.

The stage is being set for the largest legal transfer of wealth in history: from the middle class to the rich, all courtesy of politicians who wouldn’t understand the first thing about economics if you wrote it on their foreheads.

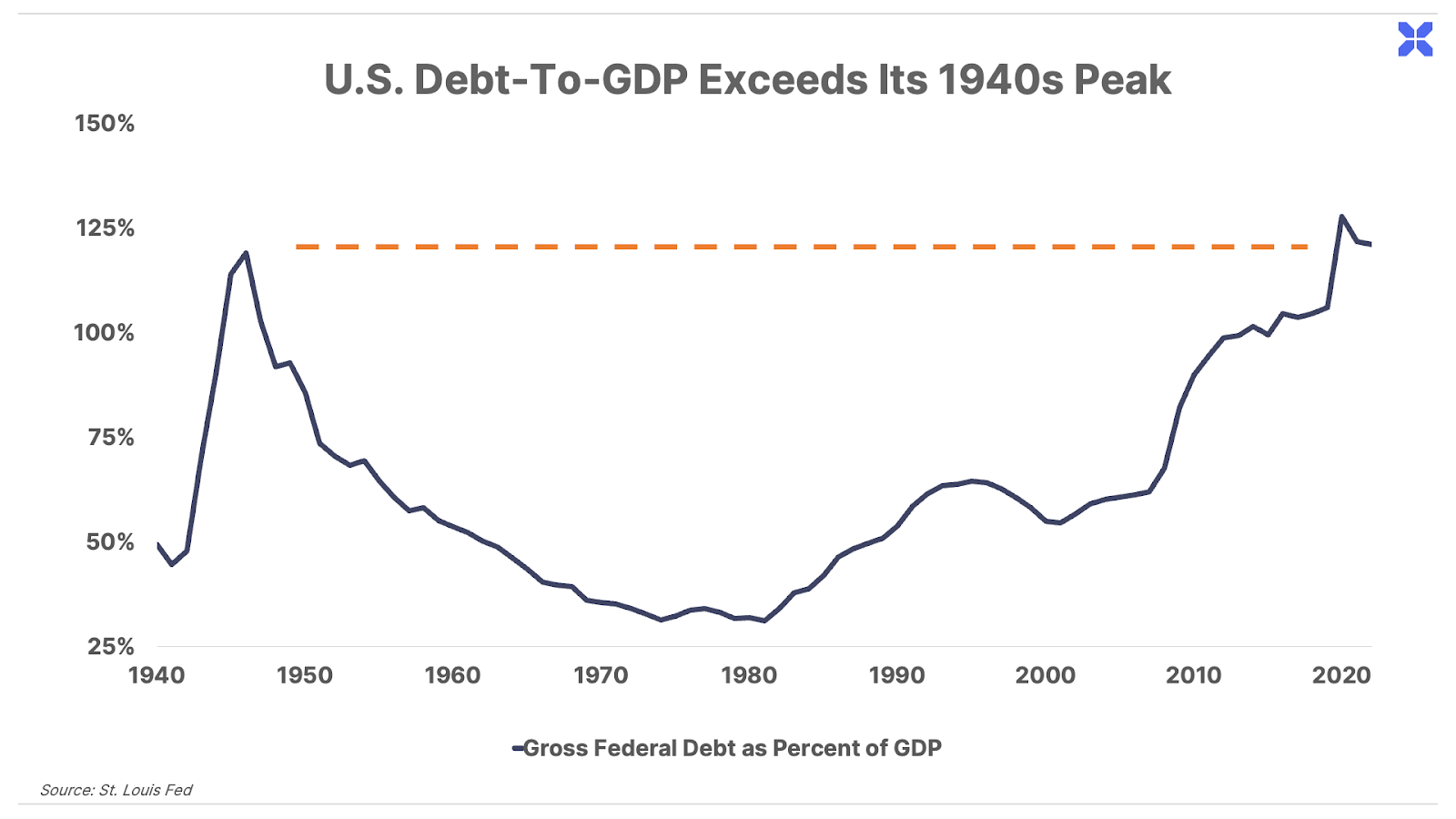

Total federal debt has nearly tripled since the Great Financial Crisis, from just over $11 trillion in early 2009 to almost $32 trillion today. And with annual deficits expected to exceed $1 trillion indefinitely, there is no end to this trend in sight.

At these levels, the U.S. government’s debt burden represents roughly 120% of gross domestic product (GDP) – down from a peak of 130% in 2020. That is a rare extreme seen only one other time in American history – in the immediate aftermath of World War II.

Of course, that debt was largely the result of a history-defining conflict for the very existence of the Commonwealth. The latest binge went toward fueling two decades of pointless wars in the Middle East, bailing out Wall Street banks, covering the tab for promised (yet unfunded) entitlements like Social Security and Medicare, and financing the bloated bureaucracy in Washington, D.C.

These debts will never be repaid.

According to a 2020 study from value-focused hedge-fund Hirschmann Capital, since 1800, 51 out of 52 countries with similarly high debt-to-GDP ratios have ultimately defaulted, either through restructuring, devaluation, high inflation, or outright default.

The only exception is modern-day Japan, where the debt-to-GDP ratio is currently above 200%, and has exceeded 150% since 2009. (Though a cynic may argue it’s simply too soon to “call.”)

Inflation was the “solution” in the U.S. in the early 1940s. The Federal Reserve held short- and long-term interest rates at 0.375% and 2.5%, respectively, for most of the next decade as consumer prices rose as much as 20% annually. This inflation – along with the post-war return to government fiscal restraint – helped cut the debt-to-GDP ratio in half by the mid-1950s.

Today, the government’s vast – and growing – unfunded entitlement obligations make even modest cuts to spending politically impossible. And that means, when it comes to inflation, we haven’t seen anything yet.

Over the past couple of years, we’ve seen consumer prices rise at the fastest pace since the 1970s. And while inflation has been slowing recently following the Fed’s aggressive rate hikes (more on this in a moment), it will likely remain a persistent, recurring problem for the next decade or more, regardless of Fed policy.

History shows that any of these issues in isolation can potentially trigger a crisis. What is genuinely unprecedented (and scary) is that they are now occurring simultaneously.

Financial markets have never had to reckon with a speculative asset mania, unsustainable bubbles in consumer, corporate, and sovereign debt, and structurally high inflation – all at the same time.

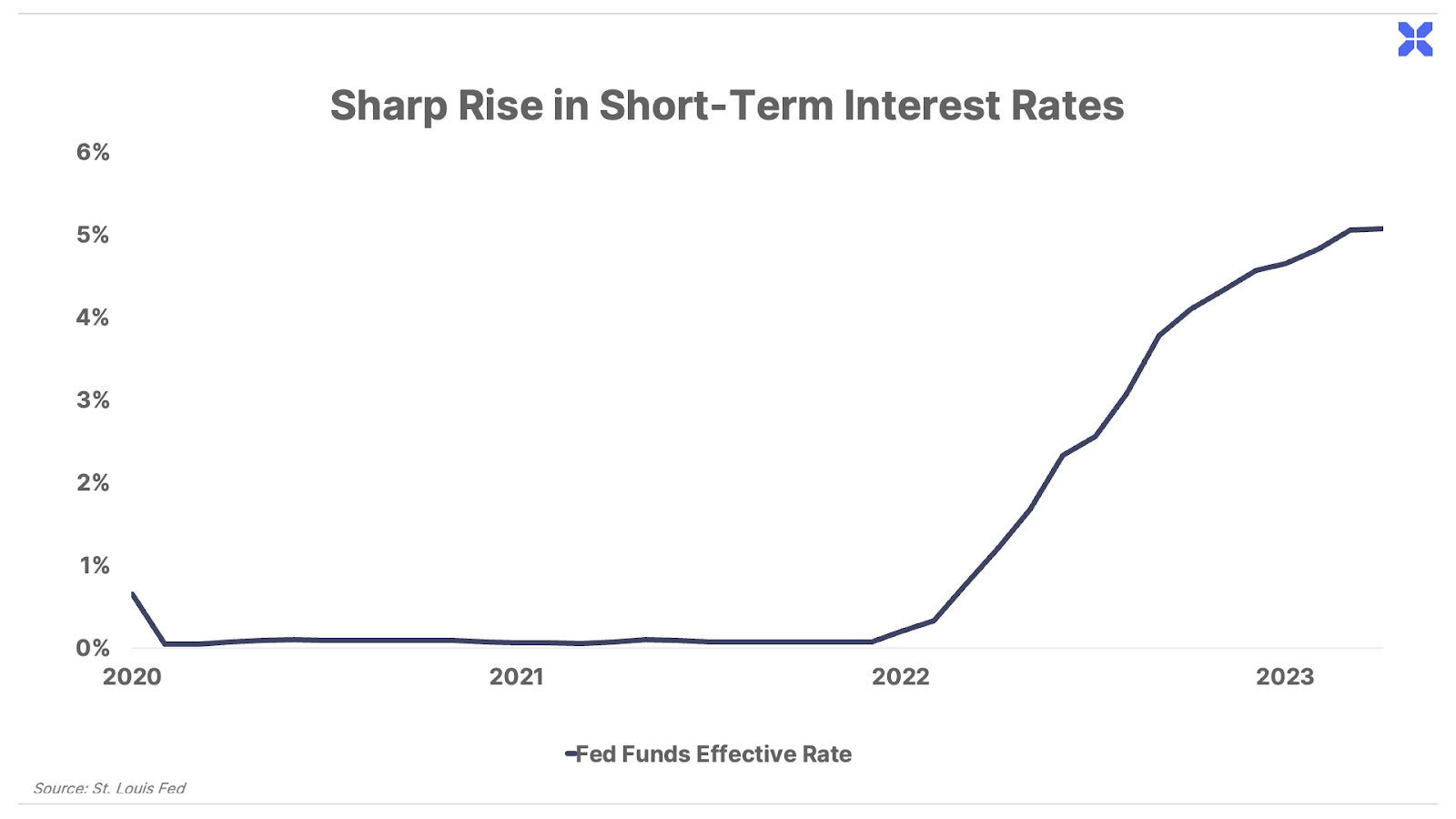

And the Federal Reserve is compounding these risks with its most aggressive tightening cycle in history. Following its latest 0.25% hike this week, the Fed has increased short-term rates from 0.25% last March to 5.50% today – a 2,100% increase in just 16 months.

Sharply rising interest rates can cause problems in any economic environment. But the Fed’s frenzied hikes are akin to dropping Mentos into a can of Diet Coke when debt levels are this high. And the series of rapid-fire explosions has only just begun.

We’ve seen several significant bank failures in the past several months, including Silicon Valley Bank, First Republic, and Credit Suisse. In the U.S. alone, the size of the losses to date has already exceeded those during the Great Financial Crisis, and more are likely to come.

Meanwhile, we’re also seeing all the usual telltale signs of an impending recession, including weakness in the housing market, a slowdown in manufacturing, falling corporate profits, and a deeply inverted yield curve, among others. And a recession would only compound these risks further.

In short, the potential for significant economic and market turmoil is arguably greater than at any time in memory – and that’s the good news!

“Don’t Be One Of Them”

Given all of these facts, you’ve got a simple choice to make.

You can continue to hold your wealth in U.S. dollars. You can continue to try and earn enough money in wages. You can believe that Social Security is funded (lol) instead of realizing that it is a worthless Ponzi scheme. You can be among the millions of Americans who are going to see their standard of living evaporate over the next decade.

Just keep believing what you hear on CNN and read in The New York Times. Keep voting for more government. You’ll get what you deserve, good and hard.

When asked what we should do about the poor, Ayn Rand offered sage advice: “Don’t be one of them.”

You have the same option when facing our country’s looming financial collapse and the economic and political chaos that will follow.

Just don’t be one of them.

You don’t have to keep your wealth in dollars. You can still buy gold or Bitcoin. You don’t have to depend on your wages to safeguard your financial security – you can wisely invest in growing businesses, whose assets (and dividend payments) will soar in value as inflation continues to increase. You don’t have to keep all of your assets in America. You can legally buy foreign real estate or even establish a business (like rental properties) in foreign markets. You can keep all of your liquid wealth in offshore banking centers.

You can use your knowledge that tens of trillions or even hundreds of trillions of dollars will have to be printed to close the gaps in the government’s giant ponzi scheme (Social Security) and position yourself to profit from the inevitable collapse of our society. You can get a second passport and make sure you have some place to get away to if a civil war erupts here. Don’t laugh – it’s coming. The Covid lockdown was just the warm-up. But the next time they try that, people will fight back.

Don’t forget, there are over 300 million legally owned firearms in this country. When the inflation gets so bad that people can’t afford food – and many people are at that point already – there’s going to be an unprecedented amount of violence. Just visit San Francisco, Chicago, New Orleans, or Baltimore to see what this looks like. It’s coming to your town soon.

Ironically, while these problems will spell doom for most people in our country – anyone foolish enough to believe anything the government tells them – for anyone who understands economics and investing, there’s hardly been a better time in history.

As the middle class disappears, our portfolios will soar.

That’s because – along with riots and rampant inflation – we’ll also see the rise of an even bigger, unstoppable force…

The more money the government prints, the bigger the relative advantage of high-quality, capital efficient businesses – companies that have the ability to raise prices without the corresponding increase to their own costs.

This philosophy was perhaps best summed up by Warren Buffett – Chairman and CEO of Berkshire Hathaway and the world’s most successful long-term investor – in his 1996 letter to investors:

“Your goal as an investor should simply be to purchase, at a rational price, a part interest in an easily understandable business whose earnings are virtually certain to be materially higher five, ten, and twenty years from now. Over time, you will find only a few companies that meet these standards – so when you see one that qualifies, you should buy a meaningful amount of stock… Though it’s seldom recognized, this is the exact approach that has produced gains for Berkshire shareholders.”

In other words, we aim to buy ultra-high-quality businesses at fair prices and hold them for the long term. This strategy works in virtually any economic environment. But… in a roaring inflationary environment, it works best.

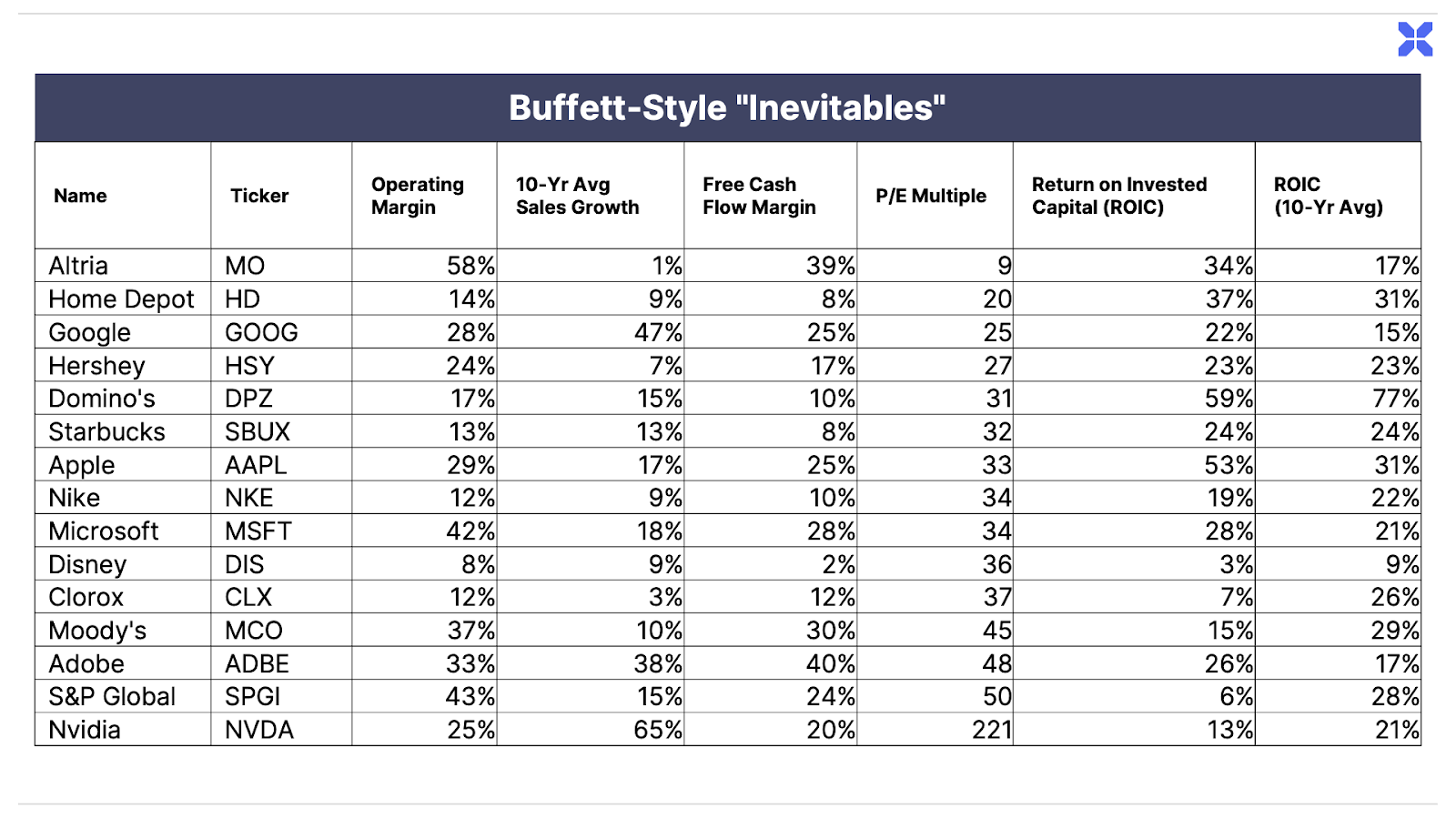

Buffett describes these kinds of companies as “Inevitables.”

These businesses have such powerful internal economics and entrenched competitive advantages that they are likely to continue to dominate their industries – and compound investors’ wealth at high rates of return – over the long term… regardless of what is going on in the economy or markets. The key to success is simply not to pay too much for them.

In that same letter, Buffett cited the examples of Coca-Cola and Gillette – two of his favorite long-term investments – to highlight these traits:

“Forecasters may differ a bit in their predictions of exactly how much soft drink or shaving-equipment business these companies will be doing in ten or twenty years… In the end, however, no sensible observer – not even these companies’ most vigorous competitors, assuming they are assessing the matter honestly – questions that Coke and Gillette will dominate their fields worldwide for an investment lifetime. Indeed, their dominance will probably strengthen. Both companies have significantly expanded their already huge shares of market during the past ten years, and all signs point to their repeating that performance in the next decade.”

Beloved chocolate maker Hershey is another classic example of this kind of business. Longtime followers of Porter’s work may recall he initially recommended shares in November 2007.

That was right at the last big peak in stock prices before the Global Financial Crisis – arguably one of the worst times to buy stocks in modern history. Yet readers who followed his advice still did incredibly well.

Like most companies, Hershey’s share price did move lower during that time (though it fell significantly less than the broad market). But its underlying business weathered the crisis without a hitch. And it has since produced total returns of nearly 800% (15% annually), or more than three times the total return of the S&P 500 over the same period.

The reasons behind these extraordinary returns are as simple as they are certain: Hershey is a remarkably high-quality, capital efficient business, and Porter recommended buying it when it was trading at a reasonable price.

It is our confidence in great companies to perform well for investors despite challenging macroeconomic conditions that is the hallmark of our approach to investing.

Therefore, and somewhat paradoxically, we don’t look at the economic storm clouds on the horizon with trepidation. We look forward to the uncertainty of these problems. These problems will cause other investors to panic, creating opportunities for us. While most investors understand this strategy in their heads, few investors have the fortitude in their hearts to step up and buy when others won’t.

That’s why we believe it’s important to keep your “shopping list” ready. Ideally you’ll have been following a business for years and you’ll know it inside and out – that’s why you’ll have the confidence to buy when others won’t. And, as you’ll discover if you become a life-long connoisseur of great businesses, the trick to achieving outstanding long-term results lies in only buying when the price is reasonable.

Last July we first published our list of the “Inevitables” we’d most like to own, noting that Altria (which we recommended buying), Google, and Home Depot were approaching prices that made them excellent long-term investments.

And, as the market continued to decline into last fall, we ended up making three extraordinary recommendations – some of the best Porter has seen in his 25-plus-year career…

While other investors were panicking and the market was in a freefall, we recommended buying an absolutely incredible business, Winmark Corporation (WINA), in mid-September at just over $200 (now $350+).

We were able to scoop up shares of Novo Nordisk (NVO) – with its amazing new weight loss drugs – at the end of October at just over $100 (now over $160).

And, most extraordinary of all, we were able to get our subscribers into a Bitcoin-backed, convertible bond from Microstrategy (MSTR) at well under par ($758). It’s now trading well over (!) par at $1,280. When was the last time you made 70% on a bond – in less than a year?!

But the very best example of our strategy, and the discipline that’s required to execute it, is undoubtedly our recent recommendation of Domino’s (DPZ) – one of the names on our “Inevitables” list that we most wanted to own.

Here’s what we wrote about the company when we highlighted this opportunity in November of last year:

“There’s rarely been a more challenging macroeconomic environment facing investors. Inflation has been running hot at 40-year highs, interest rates are on the rise, the economy is slowing and virtually every asset class is bleeding red ink.

We have little faith in our ability to predict what the stock market or the economy does over the next 12 months. But we have very high confidence that Domino’s will be serving more pies, and will be more profitable, 10 years from now.

For long-term investors, we believe Domino’s will offer the opportunity to earn 15-20% compounded returns over the next decade.”

But we didn’t get the chance to buy it until late February, when the stock finally tripped below our buy below price of $300. It’s now trading over $400.

The One Reason We Don’t Ignore Macro Entirely

Most investors would do much better if they paid far less attention to the broad market and the economy and simply focused on following Buffett’s guidance above.

That said, you’ll notice that we do still keep an eye on the macro outlook here at Porter & Co.

While macro worries generally don’t concern us as long-term investors, they can create tremendous opportunities. As Buffett himself has noted, “Every decade or so, dark clouds will fill the economic skies, and they will briefly rain gold.”

Though we can’t predict exactly when these periods will arrive, we can identify times – like today – when they are far more likely to occur.

These rare periods of turmoil can offer patient (and prepared) long-term investors the opportunity to buy world-class businesses at unusually low prices.

This combination can produce truly mind-boggling long-term returns. And given the unprecedented risks facing the economy and the markets today, we believe the coming opportunities could be among the best in history.

To help you prepare, we’ve updated our “wish list” of our favorite Buffett-style “Inevitables” to keep on your radar.

For our paid-up subscribers, implementing our strategy couldn’t be much easier. You can count on us to warn you about the macro economic problems that are going to occur… and you can count on us to tell you exactly when to buy the world’s best businesses.

If you’re not a paid-up subscriber yet… seems reasonable to ask why not? You’re not going to find a better investment strategy. This approach absolutely works. It can give you outstanding results of between 15% and 20% total returns, over very long periods of time. And it can do so with virtually zero risk of capital loss.

If you’ve got a better strategy, let us know. And, if not, we hope you’ll join us. It works. To join the fun, just click here.

Porter & Co.

Stevenson, MD

P.S. If you’d like to learn more about the Porter & Co. team – all of whom are real humans, and many of whom have Twitter accounts – you can get acquainted with us here – or email our “Mailbag” address at any time: [email protected].