| Below, you’ll find the latest market update and portfolio review from Porter & Co.’s Director of Distressed Investing, Martin Fridson. We release a full report with a new recommendation on the second Thursday of each month, and an update like this one two weeks later.

Marty also provides the “Top 3 Best Buys” – a regular feature that highlights what he views as the three most attractive positions to focus on in the portfolio, to help those who are new to distressed investing get started. As always, please call Lance James, our Director of Customer Care, with any questions. You can reach him and his team at 888-610-8895, or internationally at +1 443-815-4447. |

Distressed bonds don’t necessarily perform inversely to interest rate moves, as many bonds do. Distressed bond prices (in aggregate) rose sharply in 2024, but the benchmark 10-year Treasury yield also rose, jumping from 3.89% to 4.58%. As the Wall Street Journal frequently reminds its readers, when interest rates go up, bond prices go down. It seems that corollary doesn’t apply quite as strictly to the distressed category.

For distressed bonds, which have a real near-term risk of default, an important development of 2024 was a growing perception that the Fed had achieved the fabled soft landing – cooling inflation without bringing the economy into recession. The probability of recession within one year, according to economists surveyed by Bloomberg, dropped from 45% to 20% over the course of 2024. That mounting optimism was reflected in key statistics on credit performance.

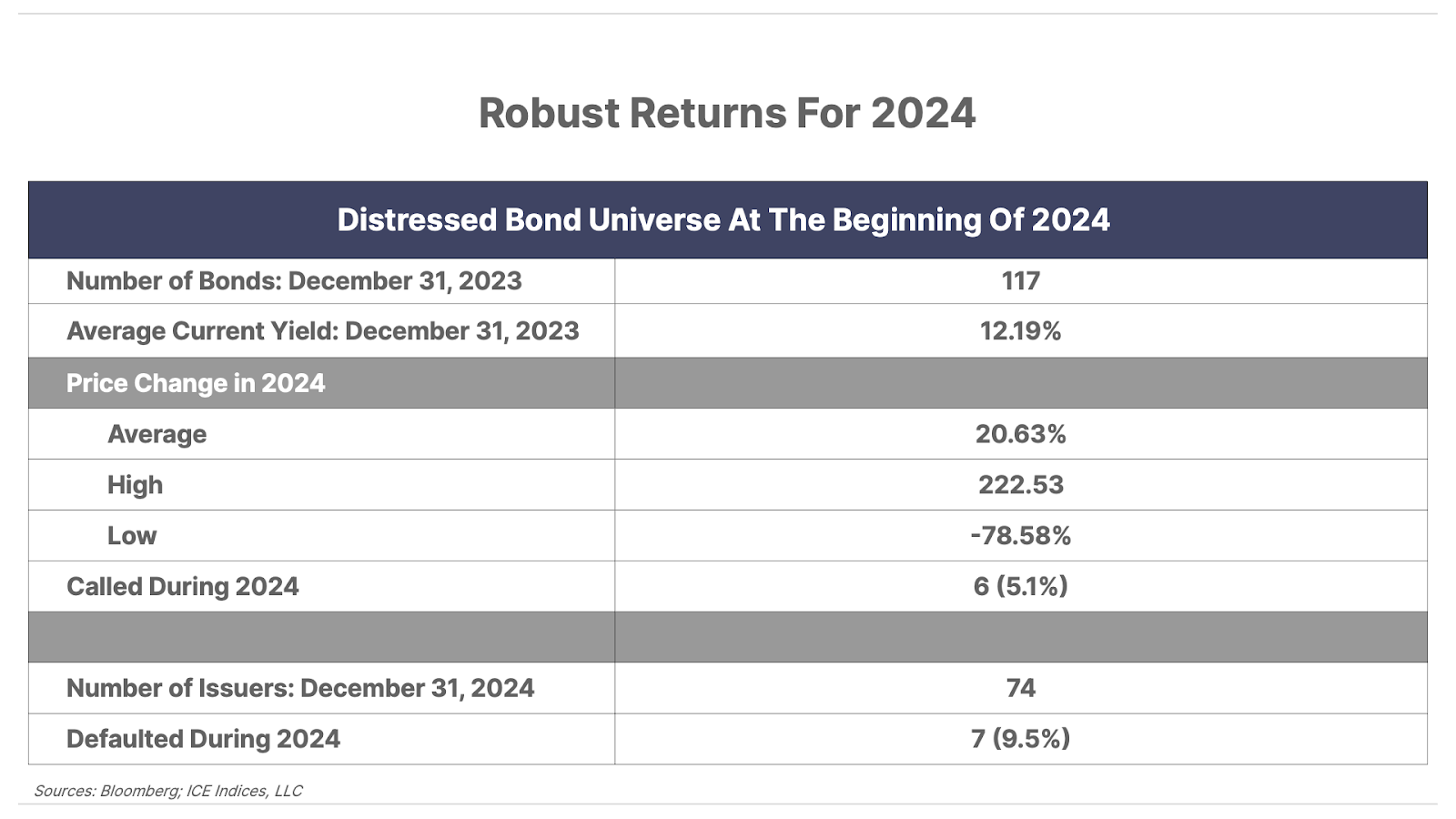

At the start of 2024, the ICE BofA U.S. Distressed High Yield Index included 117 bonds. Inclusion is based on a yield exceeding Treasury rates by 10 percentage points or more (subject to a minimum dollar amount outstanding). The 2024 credit performance of the index bonds is representative of the range of returns experienced by either individual or institutional distressed-debt investors.

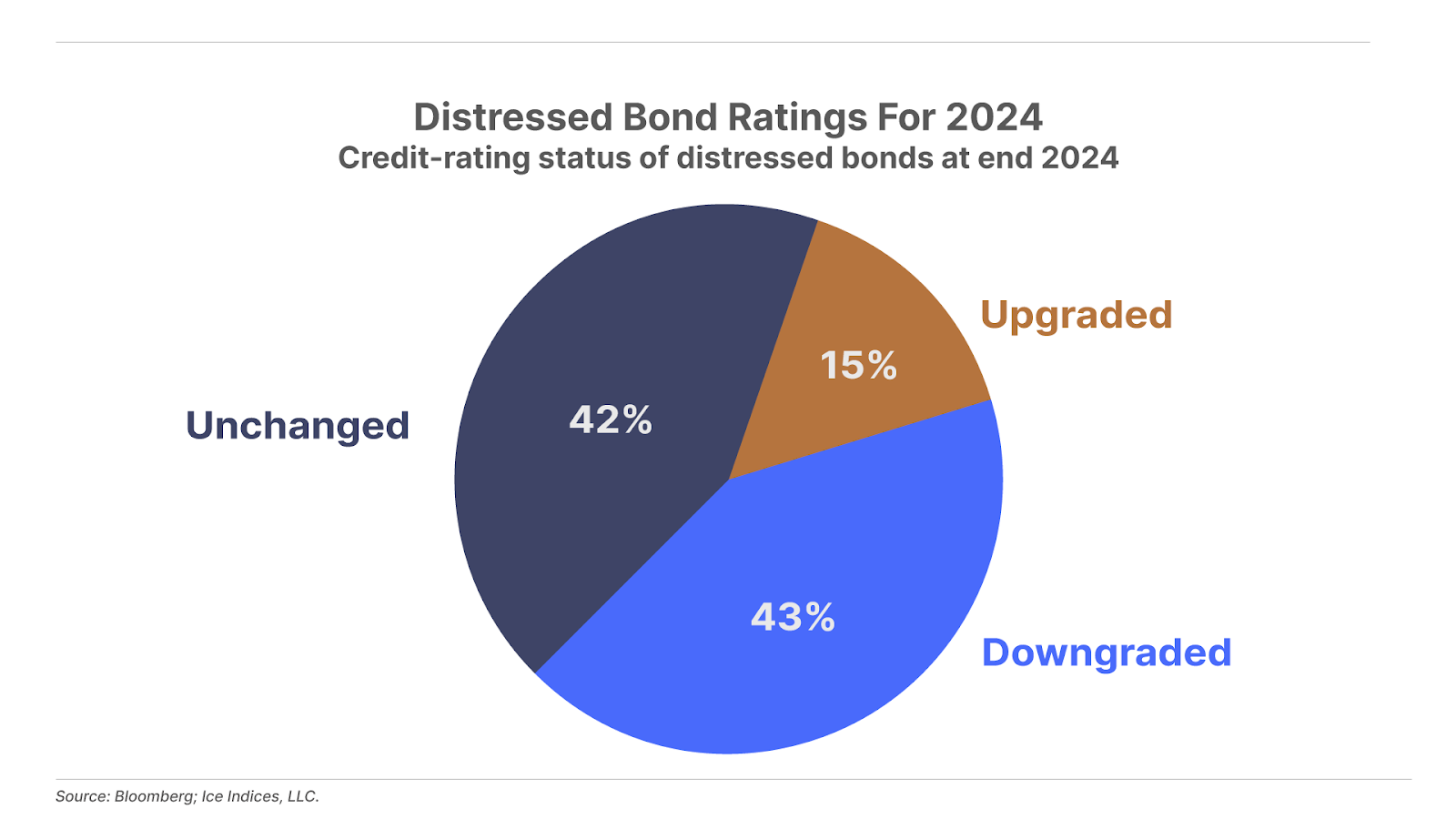

As detailed in the chart below, the majority (57%) of distressed bonds either held their credit ratings throughout 2024 (unchanged) or were upgraded. An upgrade is typically associated with a reduction in an issue’s yield spread over Treasury bonds and, ultimately, with a price increase. The market doesn’t always agree with the opinions of Moody’s, Standard & Poor’s, and Fitch, but 73.3% of the distressed bonds that received rating upgrades in 2024 went up in price.

For the 117 in the distressed-bond universe as a whole, 85 issues, or 72.6%, posted gains for the year. The table below shows that counting both the gainers and the losers, distressed bonds posted a robust 20.6% average price gain in 2024. A small but welcome contribution to that highly favorable outcome consisted of gains on bonds that were called during the year. To strengthen their financial positions, some companies exercised their contractual option to redeem bonds at par ($1,000 per bond) or a bit higher. Those decisions produced hefty gains on distressed bonds that began the year trading at deep discounts to par.

The 2024 price gains were sweetened by the fact that the 117 distressed bonds began the year with an average current yield of 12.19%. (Current yield equals coupon rate divided by price.) So even if you owned an average bond that delivered no price gain in 2024, you still earned a far-from-shabby 12.19% from interest alone. And if your bond delivered the average price gain on top of the average current yield, your total return exceeded 30% – in a year in which the S&P 500 stock index’s total return was well above its own historical average, at 25%.

One more noteworthy statistic in the table above is the 9.5% default rate. (This measure of credit performance is conventionally calculated on the basis of issuers, of which there were 74 at the start of 2024.) The annual default rate on all high-yield bonds averages between 4% and 5% over time, but almost all of the defaults occur within the typically small number that qualify for the distressed category. So at 9.5%, the 2024 default rate represents a low percentage for distressed bonds.

Furthermore, the 9.5% rate is dramatically lower than the 58% that should have been expected to default, based on a model I’ve developed. My model is based on historical data showing that the lower the distress ratio (the percentage of bonds in the high yield index that yield at least 10 percentage points more than Treasury issues), the higher the percentage that default over the succeeding year. The December 31, 2023, distress ratio of 6.4% was just about half the 1996-2024 average of 12.7%, implying that a comparatively high percentage of distressed issues would have been expected to default last year.

By way of explanation, when there aren’t very many bonds trading at distressed levels, it means that the few that are in the category deserve to be priced that way. You can therefore expect that a fairly large percentage of them will in fact default. On the other hand, when the distress ratio reaches a recession-level peak of 30% or more, many of them are depressed by investors’ flight to safety and aren’t likely to default.

All in all, the beginning of 2024 was a good time to be looking for opportunities in distressed bonds. But the table above contains one additional essential statistic. While the average price change was a gain of 20.63%, price changes on particular bonds within the group were as low as negative 78.58%. For those bonds, the fact that you began 2024 with a high current yield wasn’t anywhere near close to being enough to salvage the year.

So even in a year full of good news like 2024, picking your spots is absolutely essential in distressed-debt investing. From reading our recommendations, you know that the selection process involves deep digging into the company’s markets, its management, and the nitty-gritty details of its debt, ability to generate cash from operations, and fallback strategies for meeting its obligations if earnings fall short. If anything, this sort of rigorous analysis will be even more important in 2025 than 2024. There are some clouds on the economic horizon that could shift the balance of winners and losers in an unfavorable direction versus 2024’s results.

This content is only available for paid members.

If you are interested in joining Porter & Co. either click the button below now or call our Customer Care team at 888-610-8895.