Issue #111, Volume #2

Small Caps, Leverage, Stock-Bond Combos, And A New Way To Finance

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| Marty Fridson’s stock-bond combos… Porter re-balances Porter’s Permanent Portfolio… A new way to finance payments… Pieter Slegers’ small-cap stocks… Porter & Co. editors talk… |

Porter & Co.’s two-day Annual Conference finished up yesterday at Porter’s farm just outside Baltimore. Partner Pass members gathered for food, conviviality, and A-list financial presentations. The agenda for day two included more than a dozen presentations, a panel discussion with Porter & Co. editors, and a live recording of the Black Label podcast.

Better known for his poetry than his stand-up, Distressed Investing senior analyst Marty Fridson (above) started off his presentation by asking the audience if anyone knows why the government is not investigating the fact that only one company makes the board game Monopoly…

Marty comes to Porter & Co. with decades of experience in the world of distressed investing… having led research teams at leading Wall Street banks, including Salomon Brothers and Morgan Stanley. To date, the eight open bond positions in the Distressed Investing portfolio are up 26%.

Marty shared with attendees the concept of topping off a bond purchase with a stock purchase.

The topping-up strategy he discussed follows this path. When a distressed company rights itself and gets on the road to recovery, the price of its distressed bonds quite often follows suit and moves up in price. However, he says, it takes months for the stock market to take notice. So on at least five occasions, Marty and his team have recommended shares of companies whose bond has rebounded. The stocks, on cue, have soared shortly after. The most recent example is that of ethanol producer Green Plains (Nasdaq: GPRE).

Marty recommended both the bond and stock in May of this year. Three months later, in August, he recommended selling the bond, after it rose 26%, then in September, he recommended selling half of the shares, after the stock rose more than 100%.

Marty will be releasing a new bond Distressed Investing recommendation on October 9.

All the way from Belgium, Compounding Quality’s Pieter Slegers shared with attendees the following comment from Berkshire Hathaway’s Warren Buffett:

I think I could make you 50% a year on $1 million. No, I know I could do that.”

And it makes perfect sense, Pieter said. Because it all comes down to one thing: size. Buffett could not earn 50% returns with Berkshire Hathaway. It’s way too big. It has a $1 trillion market cap. But he could earn 50% a year if he was running a small portfolio.

He said:

The law of large numbers states that the larger you get, the harder it is to grow at very high rates. It’s way easier for a company that earns $1 million to double in size compared to a company that earns $50 billion.”

As an example, he offered this… If Apple were to grow at a compound annual growth rate of 10% for the next 20 years, it would be worth roughly $20 trillion (current market cap: $3 trillion). To justify this market cap, every person on earth would have to own multiple iPhones!

He went on to tout the long-term investment returns in small-cap stocks. He said that between 1926 and 2006, the smallest decile stocks compounded at a CAGR of 14.0% compared to 10.3% for the S&P 500.

To get specific, he said:

We see the same trend in our Compounding Quality portfolio: Our smallest business, Kelly Partners Group (KPG), has produced the strongest returns. It’s a company I pitched at Porter & Co.’s Annual Conference last year. The stock is up almost 40% since then.”

And Porter addressed the audience for a second time… this time sharing how he has infused his own version of Porter’s Permanent Portfolio with leverage – and year to date is up 103%. With a two-to-one leverage ratio, he credits his selection of high-quality stocks, property and casualty insurance stocks taking the place of bonds, and a strong year for Bitcoin and gold contributing to his returns. Plus, he said, he has been long on The Hershey Company (HSY)… but not by owning it, rather by selling puts.

Porter & Co. analyst Jared Simons brought a big idea to attendees, telling the story of a fledgling finance, credit-card startup that emerged from the PayPal mafia.

Most people know the PayPal success story. Jared shared the story of the engineer who saved it when it was on its death bed.

That engineer’s new company tackles what PayPal never did: it underwrites credit itself.

Today, more than 60% of U.S. e-commerce runs through this company’s merchants. His business has transformed credit into a growth lever for merchants. Because outcomes and repayments feed back into the network – compounding value for merchants and generating huge returns for the company.

The stock is down 15% in the last week – and Simons sees this as a buying opportunity. In fact, he sees long-term upside… 20% or more annualized return if execution continues.

The Porter & Co. editorial team took the stage to answer reader questions… on how Tylenol will hit the share price of Kenvue (KVUE), the story behind Nvidia’s (NVDA) investment in Intel (INTC) and other businesses, will Porter & Co. launch an exchange-traded fund (“ETF”), and why does Porter & Co. not have a crypto newsletter…

Partners and Big Secret On Wall Street subscribers will receive the video recordings from the entire two-day conference. For non-subscribers who want to experience all that was shared on Porter’s farm, click here to get access.

Good investing,

Porter & Co.

Stevenson, Maryland

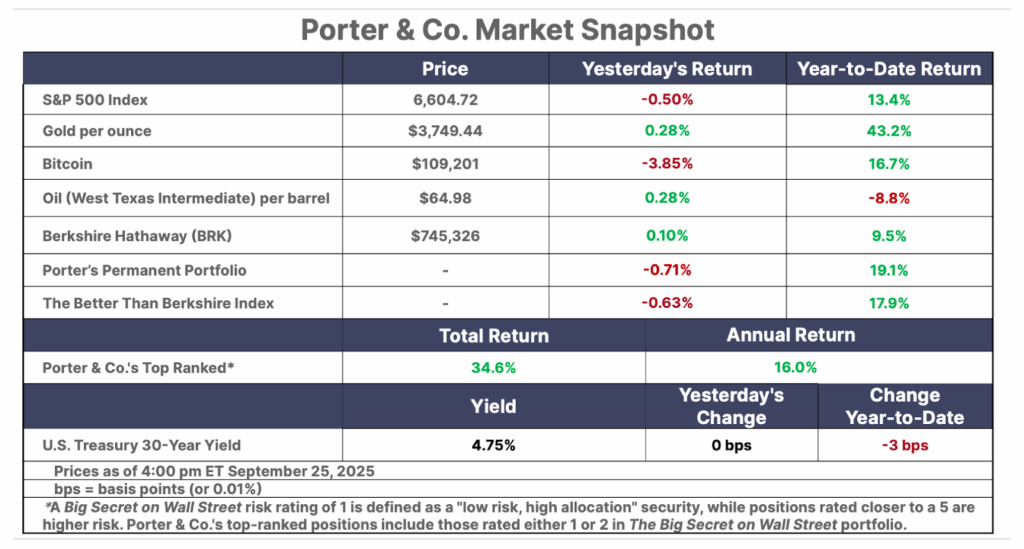

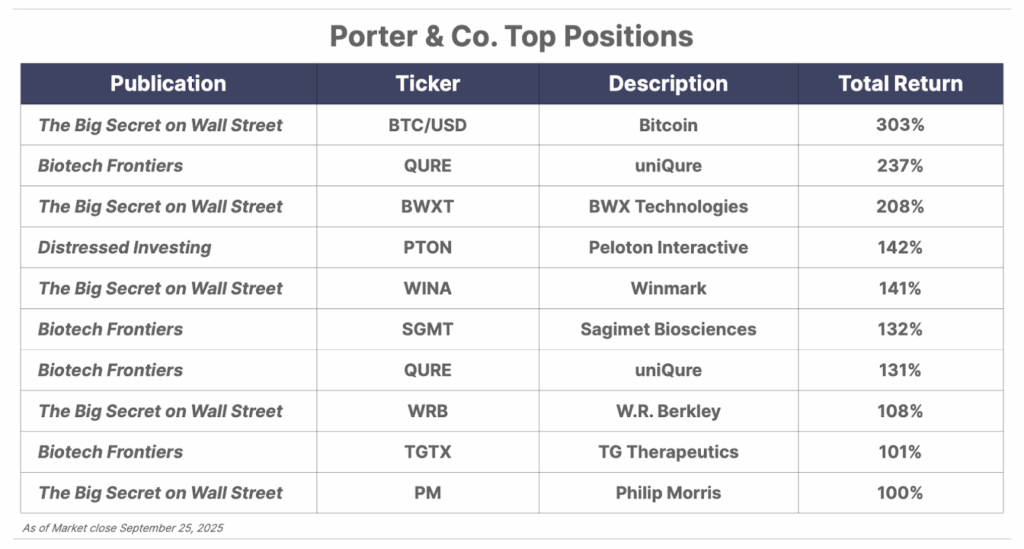

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call our Customer Care team at 888-610-8895 or internationally at +1 443-815-4447.