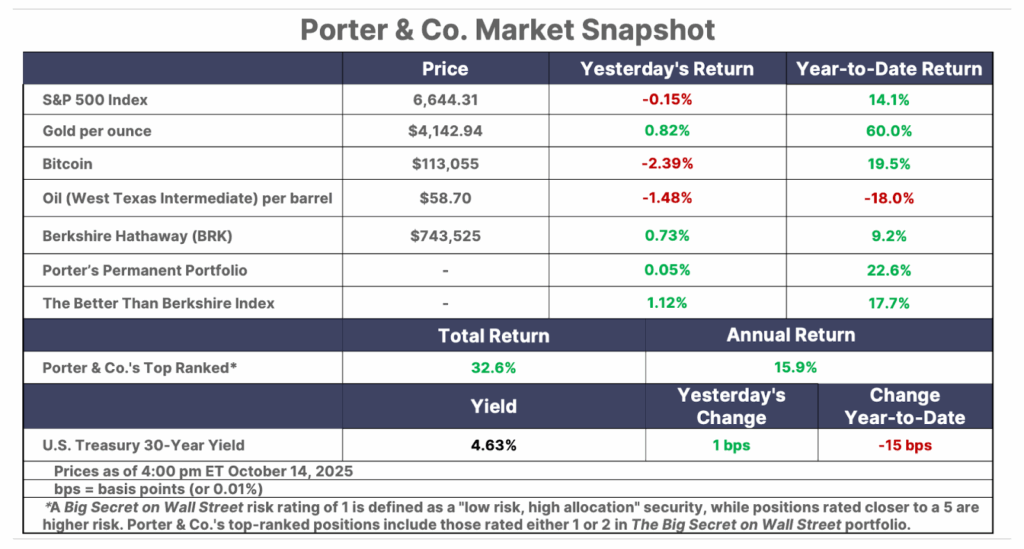

Issue #119, Volume #2

The Case For Owning Ethereum And The Best Way To Do It

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| The birth of Ethereum… A Forever Portfolio of blockchain assets… Institutional investors will soon pour in… A core “must own”… Everyone’s all-in on Mag-7… Leveraged ETFs… |

Today, Porter turns the Journal over to Erez Kalir, editor of Porter & Co.’s Tech Frontiers. Five of the 12 open positions in the Tech Frontiers portfolio are up 2x or more since he recommended them. There are three more that doubled before he suggested selling them to take gains. Overall, the portfolio is up 54% since he launched it last year.

Erez has degrees from Stanford, Yale, and Oxford, has studied biology, finance, and law, and has worked at McKinsey & Co. and for Julian Robertson at Tiger Management. Porter & Co. has recently expanded the domain of Erez’s investment research to include tech stocks, the blockchain, and science beyond his original focus of biotech.

Here’s Erez…

January 2014 was a big time for Bitcoin…

The price of the fledgling cryptocurrency was just below its then-all-time high of $1,150.

The U.S. Senate was beginning to explore what Bitcoin was and whether it should be regulated.

And the annual North American Bitcoin Conference in Miami was bustling with excited attendees.

But, oddly enough, the most tantalizing invite in Miami during that year’s Bitcoin conference was to a meeting at a rented beach house where a small group of developers was working on an idea that sounded both preposterous and inevitable: a blockchain that could run software. Weeks before, the group’s leader, a wiry, intense, 20-year-old named Vitalik Buterin, had circulated a white paper outlining the project. He named the new protocol Ethereum.

Today, Buterin is widely recognized as Ethereum’s founder… while a handful of other key players – all present at the Miami beach house that year – are credited as co-founders.

More than a decade since that fateful gathering in Miami, Ethereum has firmly established itself as the second most valuable blockchain protocol in the world. Its market capitalization of $500 billion dwarfs all other blockchains except Bitcoin, which has a market cap of $2.25 trillion.

For context, one of the cluster of chains vying to be the next most valuable – XRP, which readers of both the Daily Journal and my Tech Frontiers advisory will recognize as the token associated with Ripple Labs and Tech Frontiers SBI Holdings (Tokyo: 8473 JT) recommendation – has a market cap of $140 billion.

But Ethereum’s position as the second-largest blockchain by market cap understates its true importance. That’s because the world’s dominant stablecoins – including USDC (Circle Internet) and USDT (Tether) – settle on the Ethereum protocol. As we’ll see in today’s Journal, the tsunami of growth in stablecoin adoption will almost inevitably mean parallel growth in Ethereum.

Subscribers familiar with Porter’s work know his belief in building a stock portfolio that consists of the world’s best businesses, then holding those businesses “forever.” The time is right to expand this concept to include not only stocks, but also blue-chip blockchain assets. I’m not talking about speculative cryptocurrencies or meme coins. Instead, I’m describing the blockchain equivalent of The Hershey Company (HSY) – assets you can buy today and hold with an intention to pass them on to your children and grandchildren.

Your Forever Portfolio needs to encompass blockchain assets today for three crucial reasons:

#1: Blue-Chip Blockchain Assets As Digital Gold

Longstanding readers of our work at Porter & Co. know that the U.S. government’s debt trajectory has entered a danger zone from which there is no painless exit. Federal debt now exceeds $35 trillion, rising nearly $1 trillion every 100 days – a pace unprecedented in peacetime. The problem is not merely the magnitude of the debt, but its arithmetic: with nominal GDP growth below the blended interest rate on Treasury securities, the debt can no longer compound sustainably.

Historically, nations in this position have faced two choices: default or debasement. Default is politically unthinkable, and because the U.S. dollar is still the global reserve currency, also not a position another government could force Uncle Sam into. That leaves monetization – the quiet form of default in which the central bank prints the difference.

In the short run, debt monetization takes the form of stimulus and liquidity support. Over the long run, it manifests as fiat currency debasement, structurally higher inflation, and erosion of real purchasing power – all trends that are becoming entrenched in the U.S. today. For investors, this unfolding reality marks a generational turning point: one that will favor scarce, hard, or self-securing assets and penalize unanchored paper money.

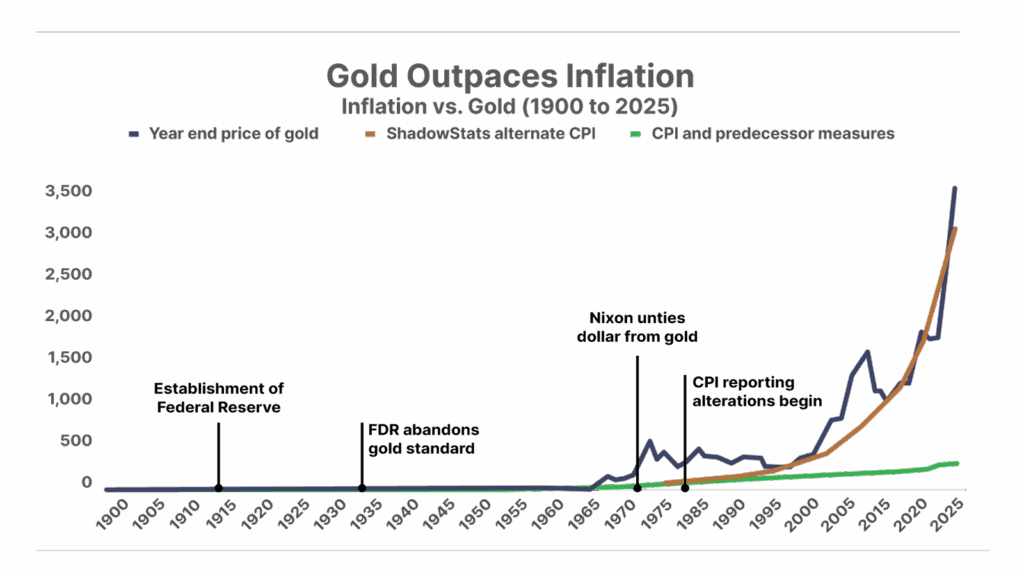

We need only recognize gold’s recent all-time high above $4,200 per ounce to understand how far along we already are in this sad story. Gold, of course, is the oldest hedge against paper money debasement, and it’s an effective one. But it is important to identify other hedges besides gold that are similarly effective.

Over 15 years, Bitcoin has evolved from a cryptographic experiment into the current answer to gold, a borderless store of value that no central bank can print or manipulate, with a fixed supply capped at 21 million coins. Because Bitcoin can be owned and transacted anonymously and moved across borders in minutes, it’s arguably much harder for governments to confiscate. Little surprise that many now refer to Bitcoin simply as “digital gold.”

But Bitcoin is only part of the story. Other blockchain protocols have, like Bitcoin, sought to immunize themselves against inflationary manipulation. And in the years since its founding, Ethereum has quietly evolved into a form of digital hard money in its own right.

Unlike fiat currencies whose supply expands at the whim of central bank policymakers, Ethereum’s issuance is mathematically constrained and transparently governed by code. Since its 2022 transition to proof-of-stake – a consensus mechanism in which validators lock up (“stake”) their Ether to secure the network and earn rewards – new ETH is created only to compensate those validators for their work.

At the same time, the network burns a portion of each transaction fee, permanently removing that Ether from circulation. Because of this, Ethereum is a self-balancing monetary system: When network activity is low, ETH supply expands modestly. When usage surges, burned fees exceed issuance, making ETH net deflationary. Because its supply cannot spiral out of control and its economic rules are open, verifiable, and enforced by decentralized consensus rather than political decree, Ethereum now functions as a programmable form of hard money.

Bitcoin remains the digital analogue to gold itself. But the broader family of blue-chip blockchain assets, led by Ethereum, offer complementary forms of digital hard money – each immune from central bank manipulation of their supply and each poised to benefit from the transition away from paper currencies.

#2: Blockchain Blue Chips Will Grow In Institutional Asset Allocation

One of my all-time favorite investing books is the 1974 classic Dance Of The Money Bees, written by legendary investor John Train. In it, Train describes how institutional capital, like a swarm of bees, never rests – it simply moves from one blooming field of opportunity to the next. Half a century later, that same migration is underway again: this time toward the blockchain ecosystem, where the world’s next great field of financial opportunity is coming into its season.

At present, blockchain assets represent a small fraction of global institutional capital. The combined market capitalization of all cryptocurrencies stands at roughly $4 trillion. Yet the world’s total financial assets – including equities, bonds, and professionally managed funds – exceed $300 trillion. Taking a conservative measure of assets that are being institutionally managed (about $125 trillion) and the institutional share of crypto ownership (5% to 7%), blockchain assets today account for less than 0.2% of total institutional capital.

Over the coming decade, blockchain’s share of institutional capital is likely to expand dramatically as the asset class becomes normalized within large portfolios. A reasonable estimate is that blockchain assets will represent 5% to 10% of global institutional assets by 2035 – conservatively, $15 trillion to $30 trillion in value. Two complementary forces will drive this growth: the migration of existing financial instruments (e.g., bonds, funds, currencies) onto blockchain rails, and the accelerating adoption of Bitcoin, Ethereum, and other blue-chip blockchain assets as inflation hedges and strategic reserves.

For individual investors, this represents a once-in-a-generation realignment in the global asset allocation framework. Those who secure meaningful exposure now – before institutions fully re-weight toward blockchain – will stand to benefit from an epochal trend.

#3: Finance Will Run On Blockchain

The final reason to add blockchain blue chips to your Forever Portfolio is the simplest and ultimately the most transformative: Blockchain is becoming the infrastructure on which the next generation of global finance will run.

Just as the internet provided the rails for information to move freely and instantly around the world, blockchain increasingly provides the rails for value – money, securities, credit, and contracts – to move with similar efficiency. Governments, banks, and payment networks are no longer experimenting on the margins: They are actively migrating core functions to blockchain-based systems because these systems are faster, cheaper, more transparent, and inherently able to be audited.

Stablecoins already settle more transactions each day than digital payment processor PayPal (PYPL). The tokenization of traditional financial instruments – U.S. Treasuries, money-market funds, corporate debt, and stocks – is expanding rapidly, bringing trillions of dollars of legacy assets on chain. In this quiet but decisive transition, blockchain is ceasing to be an alternative technology and gradually becoming the plumbing of modern finance.

As the blockchain infrastructure matures, demand for the assets that secure and govern it – Bitcoin, Ethereum, and other blue-chip protocols – will inevitably grow in tandem. Every stablecoin transaction, tokenized security, or on-chain payment ultimately relies on one or more of these foundational networks for settlement and security. Their tokens are not speculative instruments. They are the fuel and collateral of the new financial system taking shape. As the world’s payments, capital markets, and financial data increasingly flow through these decentralized networks, ownership of the core assets that power them will become as essential – and as obvious – as owning equity in the companies that built the first generation of the internet.

A Blockchain Blue-Chip Portfolio Must Include Ethereum

If Bitcoin is the cornerstone of any blockchain portfolio, then Ethereum must be its next foundation stone. Where Bitcoin was conceived as a decentralized, government-resistant, immutable store of value, Ethereum was built to be something broader: a programmable blockchain capable of running self-executing digital agreements known as “smart contracts.”

Ethereum’s programmability has given rise to entirely new asset classes that could not have existed without it. One is non-fungible tokens (“NFTs”) – digital certificates of ownership that have transformed the economics of art, gaming, and digital property. Another, far larger and more consequential, is stablecoins – digital dollars and euros that trade on the blockchain while maintaining a one-to-one peg with a fiat currency. The vast majority of these – including Tether’s USDT and Circle’s USDC, which together dominate the stablecoin ecosystem – operate on Ethereum or on Ethereum-compatible networks.

Stablecoins are well on their way to becoming the plumbing of global digital finance: They allow individuals and institutions to move dollar-denominated value instantly across borders, 24/7, outside the friction of the traditional banking system. In 2025, these instruments processed more than $12 trillion in on-chain settlements, surpassing the annual throughput of Visa, the largest payment processor. Each of those transactions burns a small amount of Ether for fees – meaning that the growth of stablecoins reinforces demand for Ethereum’s native currency.

Ethereum’s incumbency as the foundation for stablecoins and tokenized assets makes it not only a technology platform but also a monetary engine. As stablecoin usage, tokenized assets, and decentralized finance applications expand, every unit of Ethereum network activity translates into more fees, more ETH burned, and – over time – greater scarcity for Ether.

This feedback loop has pointed implications for Ether’s potential price appreciation. Reasonable estimates for Ethereum’s network growth suggest its market capitalization could plausibly increase from about $500 billion today to $2 trillion to $4 trillion over the next five years and $8 trillion to $10 trillion over 10 years. Such market capitalizations imply ETH prices of $16,000 to $32,000 over the coming five years and north of $50,000 over a decade.

But while ETH’s price appreciation potential is tantalizing, investors should focus even more on the Big Picture take away: Over the coming decade, as stablecoins, tokenized assets, and digital securities become mainstream, Ethereum will be a major winner – almost certainly joining gold, Bitcoin, and U.S. Treasuries as a core monetary asset of the modern era. For investors building a Forever Portfolio of blockchain blue chips, Ethereum isn’t an optional speculation but instead a core “must own.”

If you would like to get access to all of Erez Kalir’s recommendations, archives, and full Tech Frontiers portfolio, call our Customer Care team at 888-610-8895 or internationally at +1 443-815-4447.

Reagan’s Tech Prophet Issues October 16 Warning

Presented by Banyan Hill Publishing

George Gilder handed President Reagan the first microchip that helped create $6.5 trillion in wealth over the last 40 years. Now he’s stepping forward with an even bigger prediction about what’s being built in the Arizona desert.

He believes 3 little-known companies will explode when a bombshell announcement just days from now. Smart investors are already positioning themselves.

Click here to see what’s coming before the story goes mainstream.

Three Things To Know Before We Go…

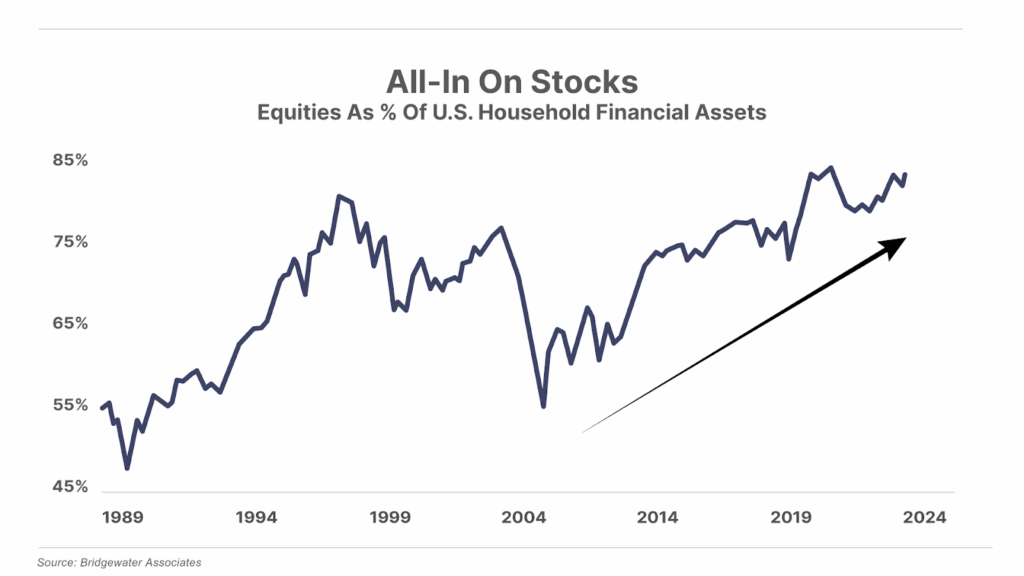

1. Americans’ financial futures have become tied to stocks. Following the financial crisis, U.S. households held around half of their financial assets in equities. Today, that amount has risen above 80% – higher than it was at the peak of the dot-com bubble – meaning the average American’s financial health has never been more dependent on the stock market.

2. A little more of every paycheck flows to the Magnificent 7. On average, American workers contribute approximately $8,500 per year to their 401(k)s, with 71% of those funds allocated to equities. Given that the Magnificent 7 stocks now represent almost 40% of the S&P 500’s market cap, this means that more than $2,300 annually – 28% of all new 401(k) equity contributions – flow into these seven stocks – Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla. In essence, the Mag-7 have become the core holding of Americans’ nest eggs, underscoring the increasing concentration of market returns in a shrinking group of companies.

3. A new kind of liquid crack is now trading on the stock market. Yesterday, exchange-traded fund (“ETF”) issuer Volatility Shares filed to launch a suite of 27 3x and 5x bull-leveraged ETFs tied to highly volatile assets such as Nvidia (NVDA), Tesla (TSLA), Bitcoin, Ethereum, Solana, XRP, and the CBOE Volatility Index (VIX). This follows just two weeks after Direxion filed to launch 10 leveraged 3x single-stock ETFs. Leveraged ETFs represent just 1% of the total ETF market, yet they now account for roughly 33% of all new launches. History suggests that when investors start piling into leverage, it rarely ends well.

And One More Thing… Is The American Dream No Longer?

Nearly 70% of people said they believe the American dream – if you work hard, you will get ahead – no longer holds true… the highest level in 15 years. The same Wall Street Journal survey finds that only 25% of people say they have a good chance of improving their lot in life, the lowest number dating to the first survey in 1987. These are the early warning signs of a broken society and of a larger terrifying phenomenon. Porter calls this The Final Displacement… a documentary detailing the full story can be found here.

Tell me what you think: [email protected]

Mailbag

In Monday’s Journal, we reported that last week’s $19 billion crypto liquidation “was triggered by President Trump’s threat to impose 100% tariffs on Chinese imports, sparking a global risk-off move that briefly rattled digital assets.” Some readers had other views on the selloff.

Wayne H. wrote in with this point of view:

There’s actually some pretty strong evidence that the crypto liquidation had nothing to do with Trump’s tariff announcement. Instead, it was a planned heist initiated against a publicly known bug in how Binance handles its USD stablecoin. There was a brief window of a few days in which to take advantage of the bug, and those involved executed a basically perfect crypto-crime. Basically, a bunch of short positions appeared just before the attack, then they attacked Binance’s USD stablecoin using millions of dollars that drove the stablecoin down to $0.65 (it’s supposed to stay near $1). Stablecoins on other exchanges were virtually unaffected, but the brief foray into $0.65 on binance caused a huge cascade of margin calls on traders using 10x to 20x leverage, back-stopped by the supposedly stable stablecoin. The liquidations on binance in turn caused the margin-call cascade to automatically propagate out of binance, affecting many “shitcoins” and eventually even Bitcoin, as noted.”

And then there’s this one…

The crypto crash on Friday, October 10, 2025, was the result of market manipulation, due to the crypto market being unregulated. Binance has been accused of manipulation in the past. Several strange anomalous things all happened together as if a coordinated effort this time. This crash needs to be fully investigated and legislation enacted to prevent recurrence. Until the crypto market becomes regulated like the stock market, unethical criminals will continue to wipe out leveraged investors.

Michael I.”

Porter’s comment: Meh. Doesn’t bother me.

Fools and their money are soon parted.

Also in Monday’s Journal, we reported that the Nobel Prize for economics was awarded to three professors whose work over the past few decades has established that innovation and free trade lead to economic growth and higher standards of living. Readers shared their views…

Great news that Nobel awarded free market thinkers. People’s grasp of history normally begins with the 21st century. It’s the age of very important people convincing the masses that their eyes are lying to them. They redefine terms like capitalism to represent the perversion we see today.

The best quote about our system I’ve heard is from John Adams. “Our constitution was made only for moral and religious people. It is wholly inadequate to the government of any other.” The speech it comes from is even better. Freedom takes work. We’re addicted to comfort and we have a morality problem. It’s how we’ve got a true central-planning Republican in the White House.

Freedom and immorality cannot coexist.

Thanks for what you do.

Jason B.”

Good investing,

Porter & Co.

Stevenson, Maryland

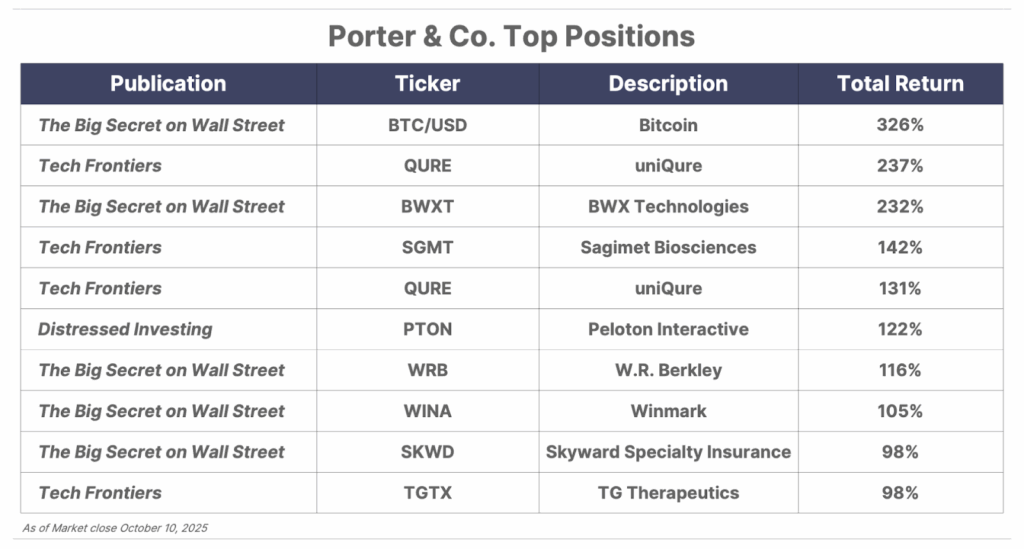

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call our Customer Care team at 888-610-8895 or internationally at +1 443-815-4447.