Issue #141, Volume #2

Why You Should Always “Check Your Pockets”

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

|

Google’s investment in SpaceX… Visa owns some of Stripe… Honeywell built up quantum computing… Private companies hiding on public balance sheets… The Fed raises rates… Hi-ho, silver… |

Have you ever found a wad of cash in a weird place…?

I think “Oh man, I just found a bunch of money.” Then, of course, I realize: “Yep, it’s your money, dummy. You put it here 10 years ago and then you forgot about it. Now it’s worth half as much…”

Investing can sometimes be like that too. Sometimes you own a lot more than you realize.

In January 2015, Google (GOOG), now Alphabet (alongside Fidelity), invested $1 billion into SpaceX – Elon Musk’s private aerospace manufacturer. I doubt anyone noticed or cared. In that year, Google earned more than $15 billion. And it was holding almost $100 billion in cash on its balance sheet.

Meanwhile, after Google’s critical cash infusion, SpaceX completed the first (ever) successful landing of an orbital-class rocket. Over the next decade it completed 84 Falcon 9 booster launches and landings, allowing it to build the world’s first cost-effective, low-earth orbiting satellite constellation, Starlink.

Starlink provides wireless internet access to people around the world who otherwise have no good way to connect. Starlink’s user base continues to double annually – growing from 1 million subscribers in December 2022 to almost 10 million today. Starlink is, in my opinion, the single most valuable piece of global infrastructure ever created and, in time, will substantially reshape the way most people on earth live.

And Google’s stake? It went mostly unmentioned for a decade. I doubt any investors attributed much, if any value, to that 2015 investment. In fact, I’d bet that even today most investors don’t know that Alphabet is a shareholder of SpaceX.

But, suddenly, last April, Alphabet was required (by accounting rules) to disclose its SpaceX stake: then valued at $8 billion. Today, it still owns 7% of the company, which is rumored to be going public next year at around a $1.5 trillion valuation. That means Alphabet’s stake would be worth over $100 billion. That’s a 100x return in roughly a decade.

That’s a heck of a lot better than finding a small wad of cash in your pocket!

Alphabet also owns 12% of Databricks, which has become one of the largest technology companies in the world, valued at over $130 billion in its current funding round. Its technology uses artificial intelligence (“AI”) to solve the complexities arising from massive cloud-computing operations, something it calls the Data Lakehouse.

And it’s not only Alphabet that’s hiding some very big businesses on its balance sheet.

Visa (V) owns 10% of Stripe, the $100 billion private payments processor. It bought its stake in a 2015 funding round that included American Express (AXP) and venture firm Sequoia Capital – at a $5 billion valuation.

Amazon (AMZN) and Microsoft (MSFT) own big stakes in AI start-ups. Amazon owns 15% of Anthropic, and Microsoft owns 27% of OpenAI.

If these private companies decide to sell shares to the public, the resulting windfalls could lead to substantial gains for investors.

And, if you’ll recall, GOOG shares were trading below 20x earnings this year. Seems pretty clear investors don’t typically value stakes in very valuable private companies accurately. Public companies tend to be valued only by the earnings from operations… even when their balance sheets are hiding gold mines.

Best example: Honeywell International (HON).

Honeywell, as I’m sure you know, is a huge industrial conglomerate. It builds all kinds of control systems in virtually every industry in the world. The business came to life in 1885 when founder Albert Butz patented the “furnace regulator and alarm,” to automate home-heating control. (If you know of my fondness for “forever” investing, it won’t surprise you to learn that I follow Honeywell closely…)

Today, Honeywell has a market cap of $129 billion. But investors have, more or less, left the company for dead. Its shares are down about 5% over the last five years.

But… look what’s in Honeywell’s “pocket.”

The company has been investing heavily in quantum computing since 2014.

In 2018, these quantum research-and-development (R&D) projects became a business unit – Honeywell Quantum Solutions. Honeywell’s engineers have focused on developing trapped-ion quantum computers, which are known for high-fidelity (low-error) qubits.

In March 2021, the company’s trapped-ion quantum computers produced a two-qubit gate fidelity of 99.9%, one of the highest ever recorded.

Honeywell developed this technology for its own various business units, but there are many other possible applications outside of its core businesses. To accelerate the development of a commercial quantum computer in June 2021 Honeywell merged the business with a leading quantum software developer (Cambridge Quantum Computing) and spun out the combined entity as a new company, Quantinuum.

Honeywell still owns 54% of Quantinuum. And its most recent funding round occurred at a $10 billion valuation. While I don’t know how much of Honeywell’s R&D budgets have gone into Quantinuum, its total R&D budgets in the period were around $1 billion annually. So nothing close to $10 billion.

I’ve got no idea who will win the race to a commercially viable quantum computer. But I know I’d much rather own a company like Honeywell and get half a leading quantum-computer business for free, then try to guess which one of its half a dozen poorly funded publicly traded competitors might survive the next bear market.

Investors – don’t forget to “check your pockets.”

In this advertisement from our friends at Paradigm Press, former CIA insider and best-selling author Jim Rickards believes a $150 trillion mineral boom is about to begin.

Jim recorded this interview containing all the details, including how you can sign up to receive his research on The American Birthright: Phase II, including 3 small stocks that skyrocket if he’s right.

Keep in mind, we only accept advertising from publishers we know to offer well-researched ideas vetted by a legal team, excellent customer service, and reasonable refund policies. Paradigm Press is one such partner. We do not, however, under any circumstances make any representations about its investment ideas or strategies, nor will we warrant them as equal to our own. We do recognize that the markets can be tempestuous and, at times, ideas that we may not endorse prove valuable.

Three Things To Know Before We Go…

1. Silver’s record run continues. Silver is the best-performing commodity of 2025, with the precious metal up over 100% so far this year, and trading above $60 per ounce for the first time ever. One ounce of silver is now more expensive than a barrel of oil for only the second time in history (the first occurring during the COVID-19 oil price panic, when crude oil briefly traded into negative territory). And we saw this coming… In the October 11, 2024, Daily Journal, we noted that the historically elevated gold-to-silver ratio was due to narrow, leading “silver to be one of the best-performing commodities of 2025.” Congrats to all who captured this move.

2. The Fed cuts rates as expected, but its next move is less certain. The central bank’s Federal Open Market Committee (“FOMC”) cut its overnight borrowing rate by 25 basis points (“bps”) for the third consecutive meeting, bringing it to a range of 3.5% to 3.75%. However, the decision featured three dissenting votes – one for a larger 50 bps cut and two for no cut at all – for the first time since September 2019, as well as an additional four “soft dissents” that didn’t fully agree with today’s decision. Seven of the 12 FOMC voting members indicated that they are currently not in favor of any additional rate cuts next year. On a more “dovish” note, the FOMC did say it will resume buying $40 billion of short-term Treasury debt each month to support the overnight funding markets, beginning this Friday.

3. Home Depot (HD) braces for a slow 2026. While the home-improvement giant reaffirmed its 2025 guidance of roughly 3% sales growth, its 2026 outlook calls for flat to a slight 2% uptick – effectively negligible real growth for a retailer of its scale. The message is clear – big-ticket projects remain frozen, and consumers are still sticking to essentials. The bottom line: Home Depot’s real recovery likely arrives only after the broader cycle breaks – and consumers aren’t currently showing signs of that.

Good investing,

Porter Stansberry Stevenson, Maryland

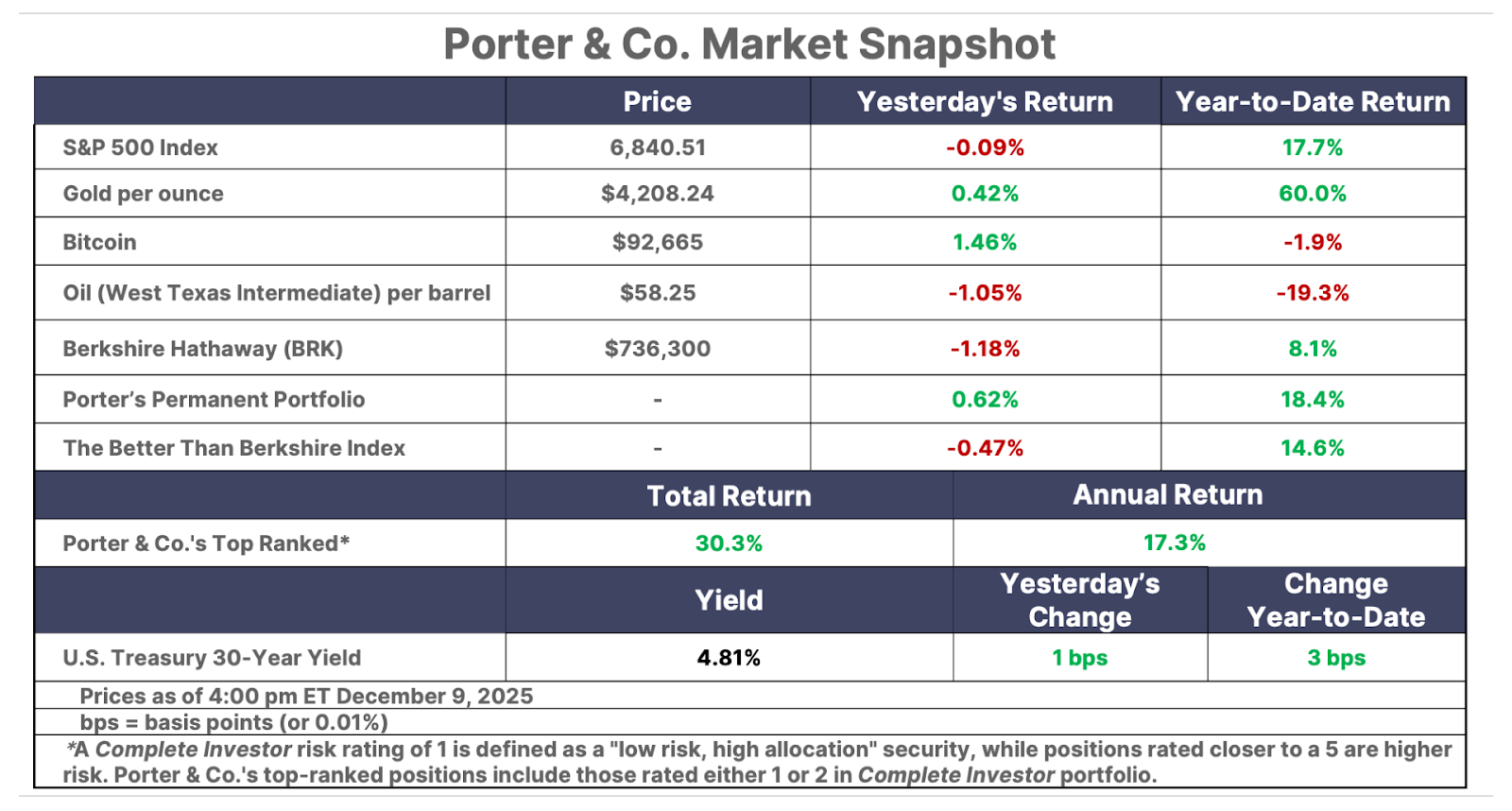

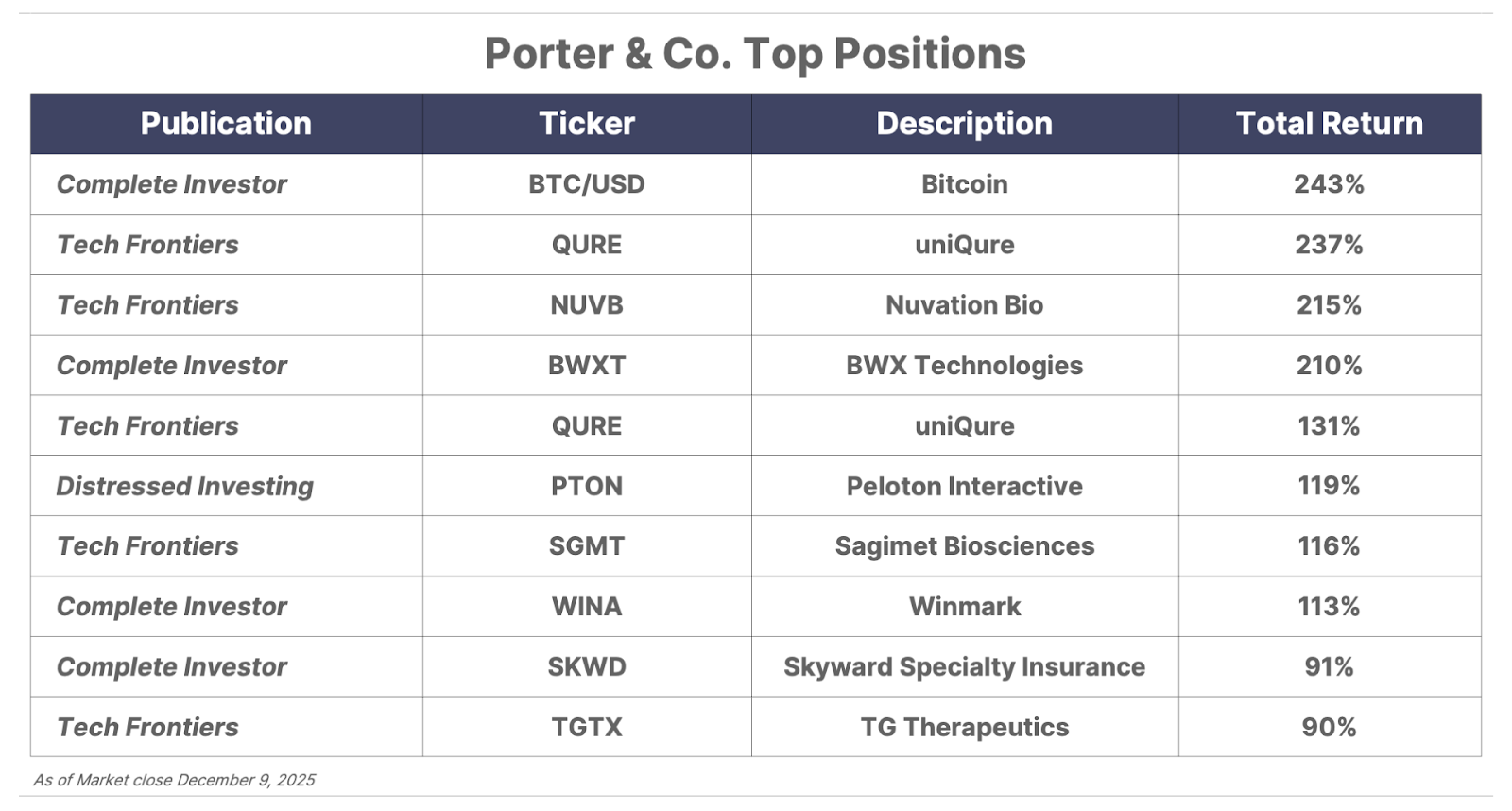

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call our Customer Care team at 888-610-8895 or internationally at +1 443-815-4447.