Issue #97, Volume #2

Make Berkshire Great Again

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

Editor’s note: We will not be publishing the Saturday Stock Screen and Sunday Investment Chronicles for the remainder of August. Both will resume on September 6 and 7.

| Social Security is merely a tax… Tariffs are an illegal tax and will be rescinded… Warren Buffett lost his touch in the early 2000s… Better Than Berkshire is the way to go… Walmart eats tariffs and wins market share… Powell speaks, and markets rally… |

“Porter, you pooped in their Cheerios…”

It’s a gift. I consistently find new and better ways of upsetting powerful people. And plenty of subscribers, too.

There have been dozens of times in my career when I’ve very calmly, very gently (not really) pointed out that the emperor has no clothes. Especially regarding our political leaders and the various business models of the most powerful financial firms in America.

Simple truth: the “wealth management” industry doesn’t exist to help you build wealth. It exists to extract your wealth.

And regarding the government, nothing tends to make people angrier than explaining that Social Security is just a tax, nothing more. No, it isn’t a contribution. No, you don’t own it. And no, it was never invested. If you’re receiving Social Security benefits, you’re on the dole.

You can disagree with me all you want, but that won’t change the facts. Social Security is, and always was, merely a tax that funded the government. It was passed by telling everyone that it was a social welfare fund and that you’d have the right to its benefits. But those were all lies. Read Flemming v. Nestor (1960) – volume #363 of the United States Reports, page 603. Or you can read a plain-English explanation here.

I’ve pissed the Trumpers off too. Tariffs are clearly taxes – duh. Taxes increase the cost of production. The costs of production are inevitably borne by consumers. These tariffs are the largest tax increases of my lifetime, and they will cause both higher prices and lower economic growth, just as sure as the sun will rise in the east tomorrow.

TANSTAAFL. (If you don’t know what that means, I’d encourage you to look it up and read the novel it comes from.)

One other point about Trump’s tariffs: There’s no way they’re legal.

Thus, they will all be rescinded – guaranteed. How do I know? Because the U.S. Constitution says so, in plain English. Only Congress has the power to levy taxes, including tariffs, as stated in the U.S. Constitution (Article I, Section 8, Clause 1).

You can also read J.W. Hampton, Jr. & Co. v. United States (1928). That’s volume #276 of the United States Reports, starting on page 394. The Supreme Court ruled Congress has exclusive power to levy taxes and duties, including tariffs and reaffirmed that those powers belong solely with Congress. Any executive action regarding taxes or tariffs must be authorized by congressional legislation.

As you can imagine, reminding the Trumpers of these clear facts leads to lots of anger and consternation. My favorite reply is when they say “You don’t know everything, Porter.” I never said I did. I said that only Congress has the power to levy taxes.

But… let’s not get bogged down in little things like taxes that impact our entire economy and our Constitution. Let’s talk about something that offends virtually everyone: Warren Buffett’s move into mostly private investments (and taking public companies private) has been an unmitigated disaster.

About 90 days ago, I committed the unpardonable sin of explaining that, on a cumulative basis, Buffett has probably lost money by investing in private businesses and buying whole public companies. That’s mostly because of Buffett’s humongous investments into public-regulated utilities, like PacifiCorp, through its Berkshire Hathaway Energy division (“BHE”). Outside analysts peg current wildfire liabilities in these businesses at $50 billion, but the companies have only reserved $2.75 billion for potential losses.

But that’s not the whole story. This isn’t merely the case of a good business getting trapped in a tort-law nightmare. This is the story of poor capital allocation. But consistently favoring buying cheaper, lower-quality businesses that he could take private (or that were private), Buffett badly underperformed the market with these investments.

In fact, if he’d simply bought the largest and most obvious public-company analog – like buying McDonald’s (MCD) instead of Dairy Queen; or buying NVR (NVR) instead of Clayton Homes; or buying The Home Depot (HD) instead of Nebraska Furniture Mart; or buying ExxonMobil (XOM) instead of BHE’s holdings – Berkshire Hathaway would be twice as big as it today.

Yes, my analysis is rear looking, but in many cases (like McDonald’s) Buffett sold shares in the large public company to buy shares of the smaller firms. And, in every case, he had access to information (annual reports) on the public companies that proved, year after year, he’d made a mistake.

I’ve been warning investors for almost a decade now that Buffett’s Berkshire Hathaway isn’t what it used to be.

Berkshire used to be a free way to beat the S&P 500. As an investment fund, it was enormously valuable: you didn’t have to know anything about the markets. You could just buy Berkshire and go to sleep. And you’d never pay any taxes or fees, because Berkshire didn’t pay dividends. It was genuinely the greatest investment alternative in the entire world. A free “call” on the entire stock market.

But that changed post-2000. Buffet’s investing out of the financial crisis from 2009 until he began buying shares of Apple (AAPL) in 2016 was the worst stretch of his entire career.

Buying BNSF Railway, IBM (IBM), and Bank of America (BAC) were some of the worst investments he ever made. Just imagine if he’d simply bought more shares of Berkshire instead! Or American Express (AXP). Or Moody’s (MCO). Or any number of high-quality businesses that were selling for peanuts in 2009-2014 – including, of course, Apple.

Today, I do not believe Berkshire can reliably beat the market. Not just because of its foolish preference for lower-quality, private companies instead of market-dominating public companies. Today, the problem with Berkshire is structural.

Berkshire’s insurance companies are the best, overall, in the world. And about half of Berkshire’s assets are insurance companies. These businesses, while very capital efficient, must still be funded with equity capital – not debt. Their ability to pay huge claims during a crisis is paramount. Historically, Buffett paired these equity-funded insurance companies with investments in very capital-light companies, like Coke (KO), The Washington Post, Moody’s, and most famously, American Express. The result was an unprecedented money machine, the best business in the history of capitalism.

Starting in about 2000 with Berkshire’s purchase of MidAmerica Energy, Buffett began to significantly alter Berkshire’s asset mix. Rather than owning capital-light businesses that could supply Berkshire with more and more cash flows, Buffett began acquiring “heavy” capital businesses, like manufacturing, a national railroad, and regulated energy infrastructure that returned little – or even no – capital to Berkshire. To optimize these company’s returns on equity, investing typically relied on debt financing, not equity financing.

For example, Union Pacific (UNP) currently has $33 billion in debt and only holds $1 billion in cash. It has a 33x debt-to-cash ratio, showing that it funds virtually its entire operation with debt. Debt has a much lower cost of capital than equity. Railroads are a tough business, but by using lower-cost debt instead of higher-cost equity, the result is a good business: a 10% return on equity.

Berkshire holds $344 billion in cash and only has $127 billion in debt – it has roughly 3x as much cash as debt. It is mostly funded with equity, not with debt. (And that must always be the case because of its potential insurance obligations.) Thus, even with its dozens of great businesses and Buffett’s legendary investment into Apple, Berkshire’s return on equity is only 10% – the same as a railroad’s!

To “Make Berkshire Great Again!” the solution is obvious: spin off (or distribute, tax-free, to shareholders) all of the capital-heavy businesses like the railroad, the manufacturing, and the regulated utilities. These businesses would all be far better off if they were primarily funded with debt. And to attract investors, these kinds of slow-growth, low-return businesses should pay hefty dividends.

Berkshire should also do an honest assessment of its holdings. I’d put together every one of Berkshire’s private businesses that isn’t producing at least a 20% return on invested capital. I’d spin off those holdings into a separate company with an aggressive management team that would be compensated for either fixing these businesses or selling them and buying better ones – essentially creating a new conglomerate.

And then, I’d do what Buffett did in 1967: I’d weld the world’s best insurance company onto a portfolio of the world’s finest businesses. But instead of taking the Buffett path into private companies and buying entire public companies, I’d just stick with partial shares of the world’s best companies. When those aren’t available at a reasonable price, I’d buy more of my own shares.

There isn’t a better strategy than owning high-quality insurance companies and recycling the “float” into the world’s best businesses.

I’m fairly confident that after Buffett retires at the end of the year, these obvious changes will happen.

But until then, or until those changes do occur, consider holding our Better Than Berkshire Index instead. We’ve taken Berkshire’s allocations and then, wherever possible, replaced Berkshire’s holdings with a higher-quality, publicly traded alternative. There is some overlap with Berkshire if there’s not a better publicly traded alternative, like, for example, American Express (AXP).

How’s that working out? Well, year to date Berkshire is up 7.7%. And our Better Than Berkshire Index is up 16.8%.

Wait a minute, you’ll say. You didn’t publish your Better Than Berkshire Index until May. Yes, quite correct. We wanted to use the same time frame in our comparison chart (that’s at the bottom of every Daily Journal for an apples-to-apples look at the different investment vehicles). But, just to be clear, since we launched in May, Better Than Berkshire Index is up 7.0% and Berkshire is down 4.9%.

One more question you might have. How does Better Than Berkshire compare to Porter’s Permanent Portfolio?

Short answer: it doesn’t.

Porter’s Permanent Portfolio is designed to be non-correlated to the stock market – and to Berkshire Hathaway.

It isn’t designed to beat the market.

Porter’s Permanent Portfolio is an ultra-low-risk alternative to investing solely in the stock market. It’s designed to weather any storm, to be very low volatility, and to earn adequate returns – but not market-beating returns – over time.

If you’ve got any more questions, let me have them. And, if you disagree with anything I’ve written here, I’d love to know why. Send rants here: [email protected]

The Man Who Called Bitcoin At $240… Tesla At A Split-Adjusted $20… Nvidia At A Split-Adjusted 66 Cents … Just Issued His Biggest Alert Ever

Presented by Brownstone Research

Jeff Brown’s personal track record speaks for itself: 31 different 1,000%+ winners. Gains as high as 259x.

Now he’s calling what could be the most profitable period in tech history.

“The U.S. stock market is entering Hyper Acceleration,” says Brown. “Wall Street projects markets growing from $19T to $220T by 2030…

“And tech insiders betting billions are giving us a roadmap to target stocks with 1,000% profit potential month after month.”

Click here to get the full story.

Three Things To Know Before We Go…

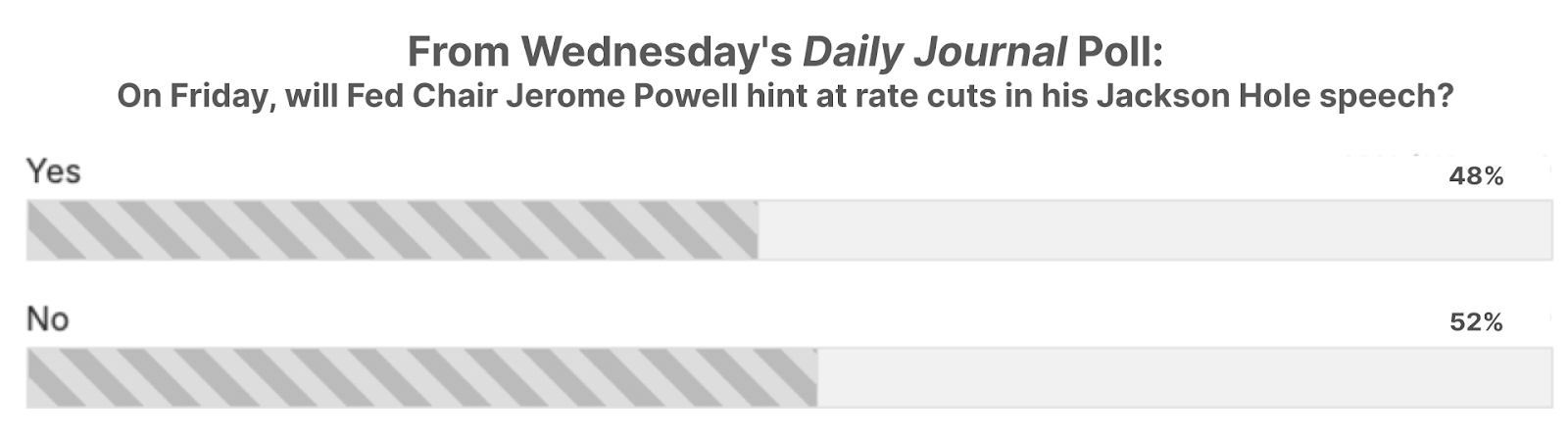

1. Powell speaks, and markets rally. This morning in Jackson Hole, Wyoming, Federal Reserve Chair Jerome Powell downplayed the Fed’s 2% inflation target in favor of boosting the labor market. This led to a sharp stock market rally, and the market-implied odds of a Fed rate cut jumped from 71% to 93%.

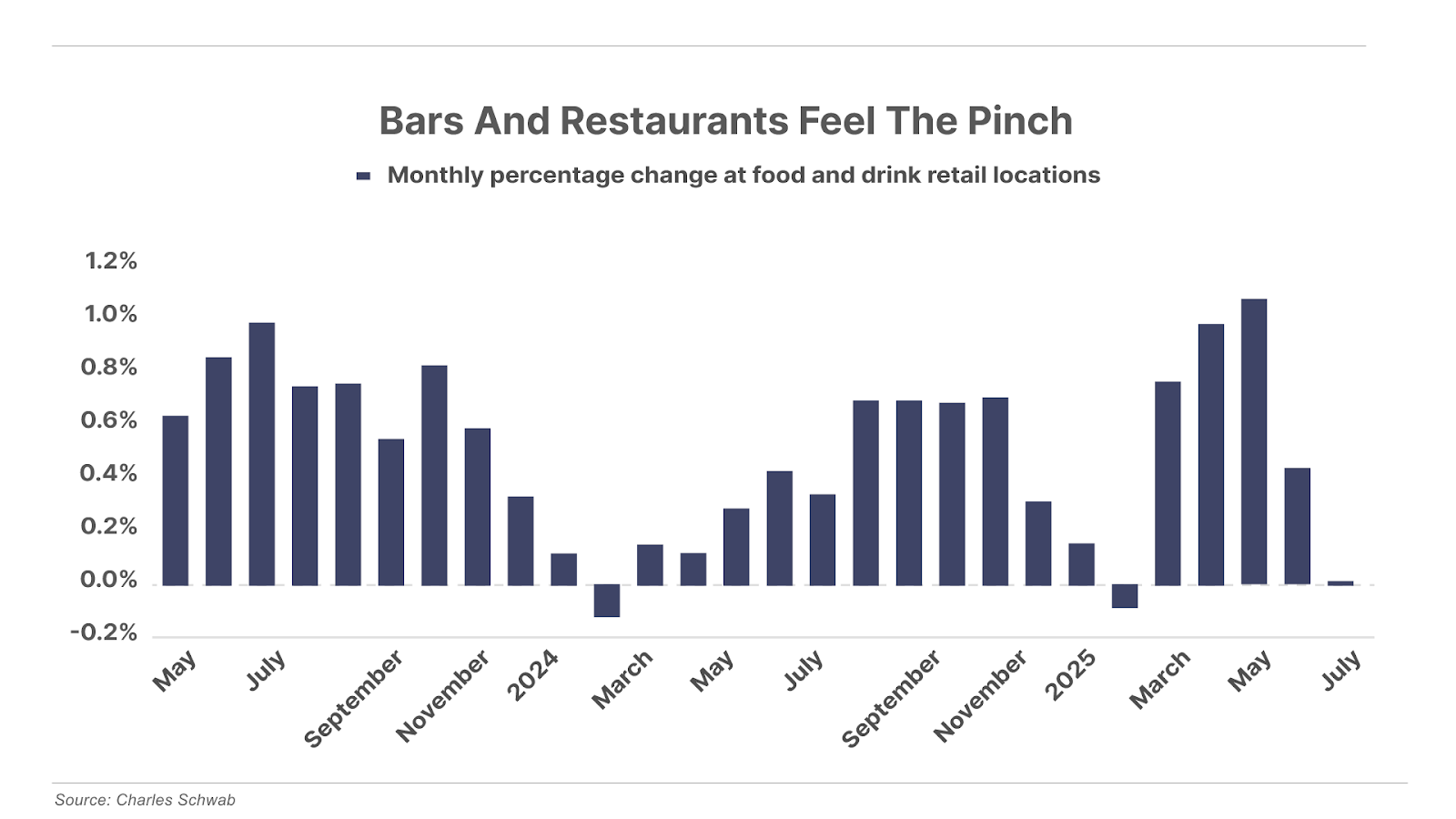

2. Consumer spending is drying up. Bar and restaurant sales have been flat for the past three months, marking one of the lowest readings in the last two years – particularly concerning since summer is typically a peak period for travel and dining out. This data signals that discretionary spending is drying up, as consumers pull back on non-essentials.

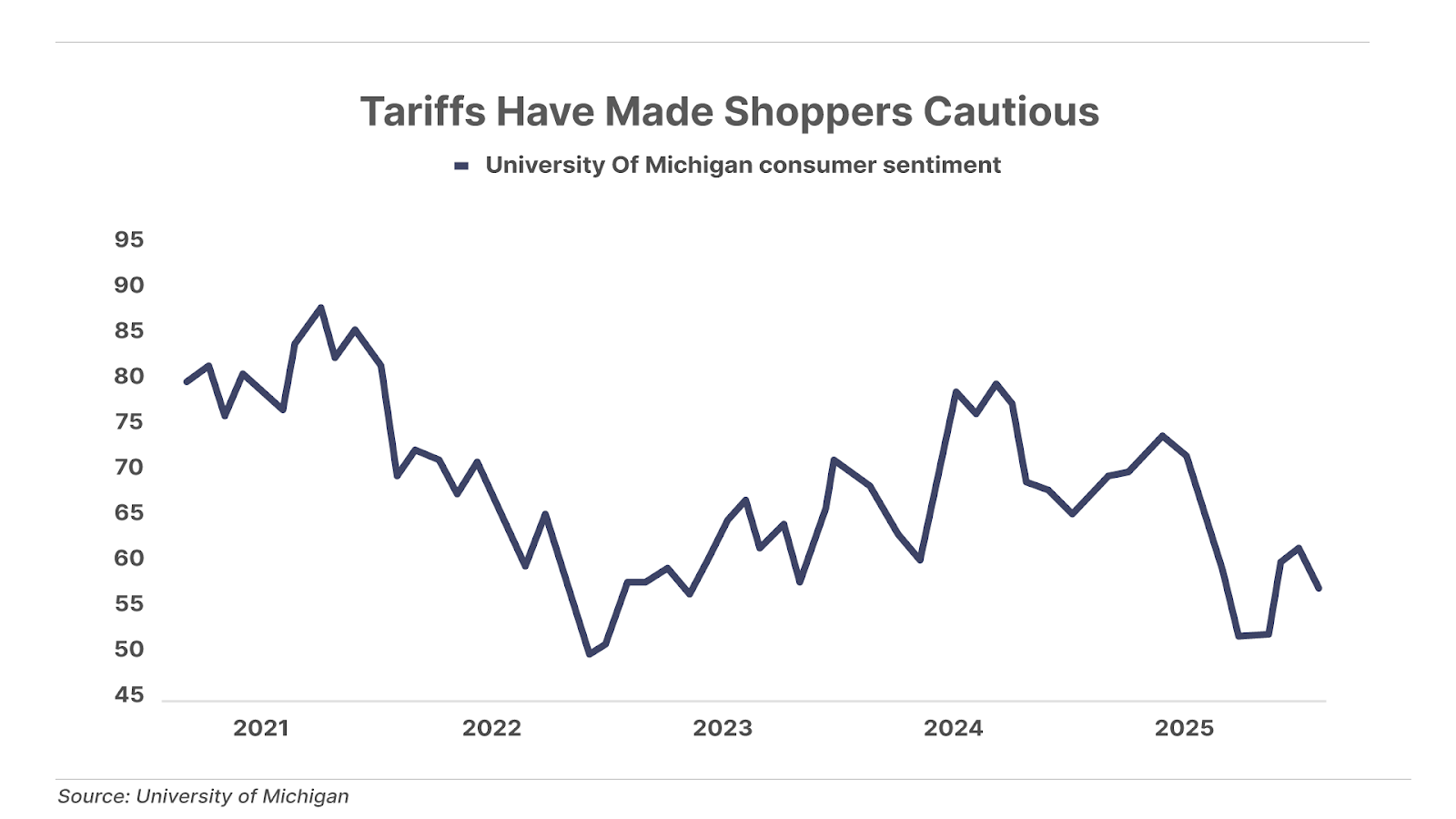

3. Big retailers cater to worried shoppers. Walmart (WMT), Amazon (AMZN), and T.J. Maxx (TJX) are grabbing market share from smaller rivals by eating tariffs and keeping prices low. Worries about tariff-related price increases have made shoppers pull back on all spending and pull way back on non-essentials. But good times won’t last forever… executives at all three of those major retailers acknowledge that eventually they’ll have to pass along the tariff burden in the form of higher prices.

And One More Thing… Poll Results

On Wednesday, we reported that Federal Reserve Chair Jerome Powell has been using his speech at the Jackson Hole Economic Policy Symposium as a platform for signaling Fed policy changes. We then asked readers if they thought he would “hint at rate cuts in his next speech,” which he did this morning. Survey takers were more or less evenly split… with 48% saying “yes” and 52% saying “no.”

Tell me what you think: [email protected]

Porter Stansberry

Stevenson, Maryland

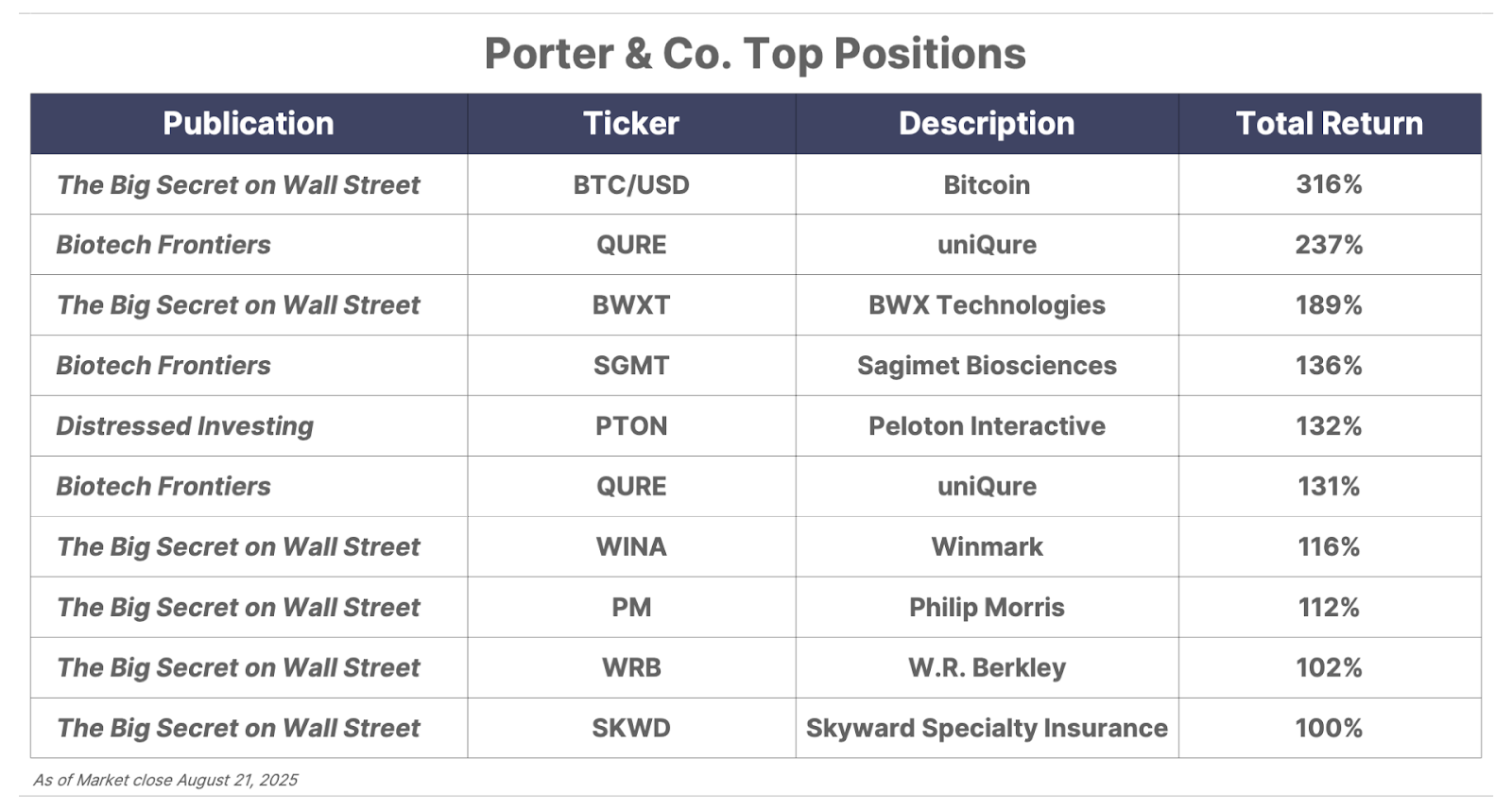

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.