Issue #56, Volume #2

How To Build A Portfolio That Outperforms Berkshire’s

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| A portfolio that outperforms Berkshire Hathaway… BRK has become virtually unmanageable… Pulling winners from the list of Wealth Creating Machines… An all-new portfolio that mostly follows the Berkshire allocation model… The dollar and 10-year yield diverge… |

Editor’s Note: In last Friday’s Daily Journal, I shared some surprising research showing that because of huge potential losses at Berkshire Hathaway Energy and large recognized losses at Kraft Heinz and Precision Castparts, Berkshire Hathaway’s (BRK) private investments have been, on a net basis, money losers over the past 25 years. I’d recommend reading that article before you read today’s Daily Journal, as without that context, what I’m suggesting below won’t make as much sense. – Porter

At first glance, the idea that you could build a portfolio that would reliably outperform Berkshire Hathaway (BRK) seems ridiculous.

For decades, Berkshire was a free and easy way to beat the market consistently. Thanks to Berkshire’s huge insurance company float (now over $170 billion), Berkshire was a leveraged bet on Warren’s “alpha” – his legendary ability to make great investments.

But over the last 25 years, as Berkshire has grown to become virtually unmanageable (it’s a $1 trillion market-cap business!), its relative performance has declined. Likewise, because of the growing portion of Berkshire’s capital that’s locked into regulated and capital-intensive businesses, it’s unlikely that Berkshire will outperform relative to high-quality equity portfolios.

Last week, I offered a list of stocks I feel certain will outperform Berkshire.

These are ultra-high-quality businesses that buy back large portions of their outstanding shares each year. In my mind, this is a virtually fool-proof way to beat the market: these are wealth-creating machines.

One of our analysts, Jared Simons, plugged last week’s list into an equal-weighted portfolio and back-tested it using Bloomberg. The results were better than Buffett: 20% annualized returns with less volatility than the market as a whole (beta: 0.95). The combination of market-beating returns and less volatility led to a Sharpe Ratio of 1.10 for this portfolio (the Sharpe Ratio compares the return of an investment with its risk).

Now, of course, this analysis is rear-looking. A fund like this would be called The Hindsight Fund!

But it’s also true that these companies are very likely to continue producing high returns on equity and to continue buying back their shares. Barring a financial crisis, it’s extremely likely that a portfolio made up of these stocks will generate very adequate returns. I’m also virtually certain they will beat Berkshire Hathaway and the overall market by a wide margin.

And that led to a thought experiment.

Why not build a portfolio (which could become the model for an ETF or a fund) that’s based on Berkshire’s structure and asset allocation, but that’s only made up of world-class businesses that, when measured objectively, are better than their Berkshire analogs?

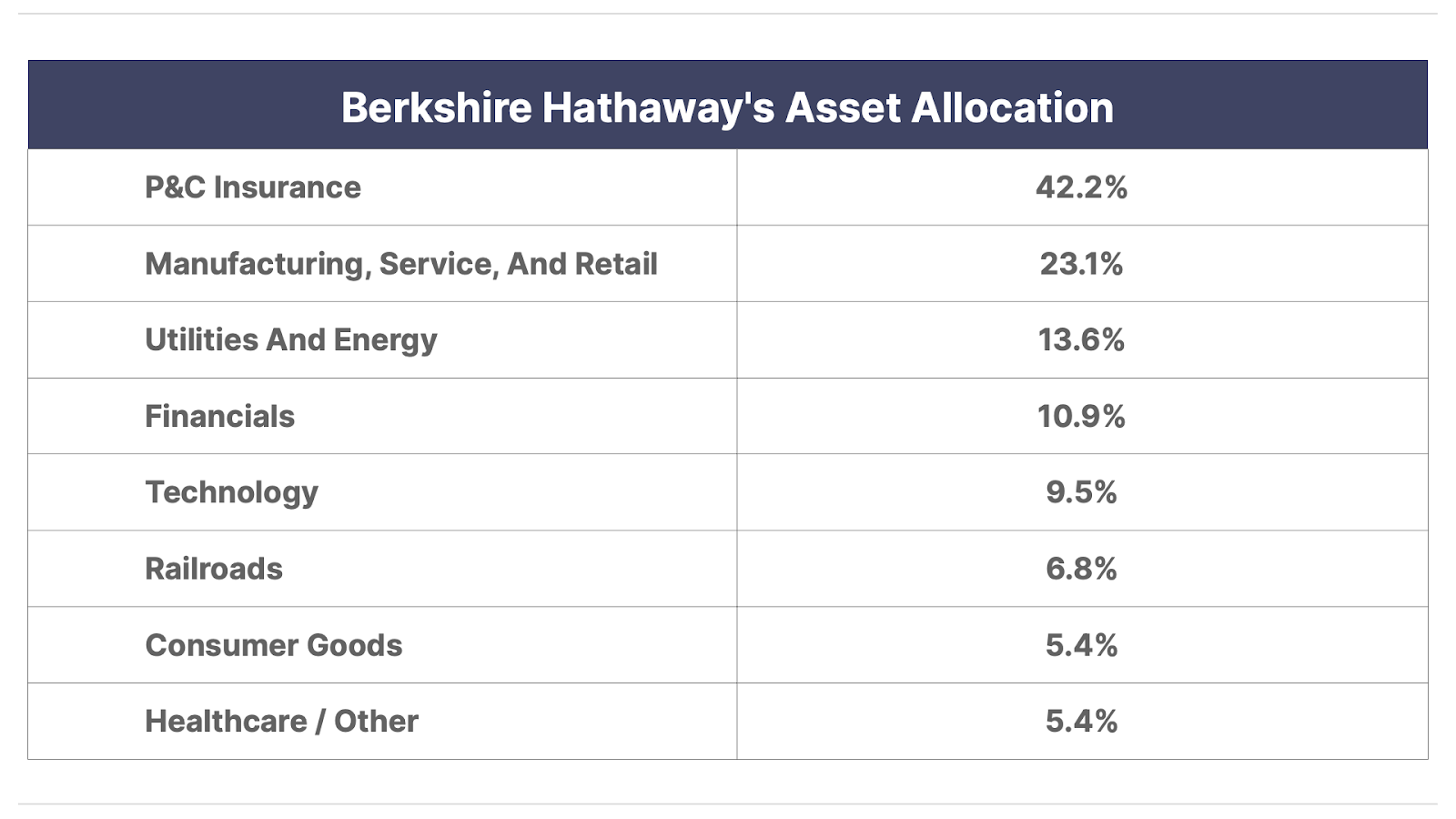

If you back out Berkshire’s cash, you’ll find that its assets are allocated across these industries in these percentage:

If you want to build your own Berkshire, you can use this asset allocation, but you can load up your version with the very best businesses in the world. The result would be a portfolio that’s like Berkshire… only better.

Is that possible?

Let’s try it.

When it comes to P&C insurance, Berkshire owns some of the best businesses that have ever been created in the industry. But Progressive (PGR), one of my long-time recommendations, has clearly been outperforming Berkshire’s GEICO and, I believe, will continue to do so for a long time.

Likewise, I feel confident that both Kinsale Capital (KNSL) and AXIS Capital (AXS), which was a long-time recommendation of mine at Stansberry Research, will outperform Berkshire’s other property-and-casualty insurance businesses because of its focus on the unregulated excess-and-surplus insurance lines, their industry-leading underwriting and combined ratios, and their faster growth rates (thanks to their relatively small size). I’d also include W.R. Berkley (WRB), which is the gold standard in the industry.

When it comes to Manufacturing, Service, and Retail (“MSR”), outperforming Berkshire isn’t a challenge.

Berkshire’s $37 billion Precision Castparts acquisition has been a disaster. If you want to own the best aerospace business, buy shares of HEICO (HEI). It is a serial acquirer in aerospace, defense, and electronics. It’s made over 100 acquisitions since 1990. It is one of the best businesses in the world – it’s up ~800% over the last decade with virtually no volatility.

But you don’t need to leave the list of Wealth Creation Machines we shared last week for the MSR allocation: Lockheed Martin (LMT) is a better business than Precision Castparts, too. Homebuilder NVR (NVR) is a vastly better business than Clayton Homes. The Home Depot (HD) is one of the best retailers in America – far better than Mrs. B.’s Nebraska Furniture Mart – and AutoZone (AZO) is a very safe bet too. Deere & Co. (DE) is one of America’s greatest manufacturers and one of the best businesses in the history of capitalism, and Winmark (WINA) has been one of the best retailers in the world since adopting its franchise model, with a better-than-3,500% return since the Global Financial Crisis – both are in The Big Secret On Wall Street portfolio.

When it comes to utilities and energy, I’d absolutely avoid any regulated utilities. Instead, I’d focus on businesses that seem best able to produce, fuel, and distribute electricity – which is sure to be in increasing demand thanks to the insatiable appetite that artificial intelligence (“AI”) has for it. From our list of Wealth Creation Machines, Caterpillar (CAT) has a large and growing back-up power business. But in this industry, I’d look to our Big Secret On Wall Street portfolio for high-quality businesses like leading natural-gas supplier EQT (EQT), liquefied natural gas exporter Venture Global (VG), energy royalty business Texas Pacific Land (TPL), Permian basin royalty business Viper Energy (VNOM), and the leading provider of small modular nuclear reactors BWX Technologies (BWXT).

In Financials, Buffett has a huge position in Bank of America (BAC)… which in 2020 made a huge bet on bonds at the worst time in a century: when yields were less than 2%! I’d avoid banks, which are both highly leveraged and highly regulated, and instead focus on far more capital-efficient payment processors. From our list of Wealth Creators, you could pick Visa (V). But I’d strongly recommend American Express (AXP) instead. That’s one stock that Buffett has that is impossible to beat. (Somehow we missed including it in our analysis last week: Amex has bought back 30% of shares over the last decade, or about 4.6% a year.) From The Big Secret, I’d include PayPal (PYPL) and… a potentially controversial choice: Credit Acceptance (CACC). Subprime auto lending is not a business that I think Buffett would have ever been involved with, but this company does this necessary (but unsavory) job in a first-class way. It’s been a terrible business for the last three years as auto-loan delinquencies have set new record highs. But this is a cyclical business. These lean years will drive out the weaker players and over the next decade, Credit Acceptance could easily become our best-performing stock.

When it comes to technology, it’s awfully hard to guess which firms will end up dominating. But I think Alphabet (GOOG) and Booking (BKNG) from our Wealth Creators list have become de-facto “Lindy” stocks in the sector and have proven to be steadfast buyers of their own shares (our Lindy’s List of businesses are those that have excellent economics and long, at least 20-year, track records). Also from The Big Secret portfolio, it’s hard to imagine a world that doesn’t include Uber Technologies (UBER). And I’d add Coupang (CPNG), which is a fast-growing e-commerce leader in Asia.

Railroads? There’s only one on our Wealth Creators list, CSX (CSX).

And then there’s consumer goods – one part of Berkshire’s asset allocation that I’d suggest changing substantially, making it 15% of the total instead of 5.4%. And we have lots of great businesses to choose from: Philip Morris International (PM), British American Tobacco (BTI), Coca-Cola (KO), which also should have been on our Wealth Creators list, The Hershey Company (HSY), Nike (NKE), and Domino’s Pizza (DPZ). I’d also add McDonald’s (MCD), which also should have been on our Wealth Creators list. It has repurchased 26% of its shares over the last decade.

When it comes to healthcare, we’ve got to go with our Wealth Creation list’s healthcare leader, HCA Healthcare (HCA). And I’d also include Alnylam Pharma (ALNY), one of Biotech Frontiers editor Erez Kalir’s core long-term recommendations, and Danaher (DHR) from The Big Secret. What might be considered controversial, rather than going with our existing recommendation of Novo Nordisk (NVO), I’d allocate into Eli Lilly (LLY) for the coming generation of weight-management drugs. Why Eli over Novo? I don’t trust the legacy of Novo’s not-for-profit ownership structure. I think capitalism will win.

So putting it all together… I’d build a portfolio that looks like this:

- 40% P&C Insurance: Progressive, Kinsale, AXIS, W.R. Berkley

- 20% Manufacturing, Service, and Retail: HEICO, Lockheed Martin, NVR, The Home Depot, AutoZone, Deere & Co., Winmark

- 15% Consumer Products: Philip Morris, British American Tobacco, Coke, Hershey, Nike, Domino’s Pizza, McDonald’s

- 5% Energy: EQT, Venture Global, Texas Pacific Land, Viper Energy, BWX Technologies

- 5% Financials: American Express, PayPal, Credit Acceptance

- 5% Technology: Google, Booking, Uber, Coupang

- 5% Healthcare: HCA Healthcare, Alnylam Pharma, Danaher

- 5% Railroads: CSX

We’ll start tracking this portfolio as an index in our Daily Journals to see if, in fact, we can produce something that’s “Better Than Berkshire,” which is what we will name it. For the purposes of our index, we’ll use a “plain Jane” equal-position-sizing strategy inside each allocation. And, going forward, we’ll rebalance and reassess the portfolio at the end of each year.

I hope this has taught you something about how to think about building a whole portfolio. And, I hope you’ve discovered a few great businesses that weren’t on your radar before.

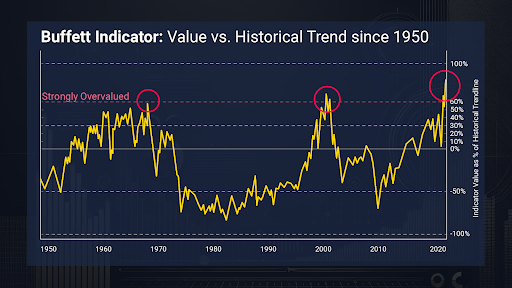

History Says Gold Wins When This Signal Flashes — and It’s Flashing Now

Every time the Buffett Indicator has hit extreme levels, stocks have crashed – and gold has dominated the decade that followed. Today, the Buffett Indicator is at its highest reading in history… and Buffett himself is sitting on an unprecedented $325 billion cash pile. Sources say he’s preparing to deploy it – not into stocks, but into gold. Garrett Goggin has uncovered which gold company could be his next big move.

Three Things To Know Before We Go…

1. Another “cool” inflation report. On Thursday, the Bureau of Labor Statistics reported that the producer price index (“PPI”) – a measure of wholesale price inflation – unexpectedly declined 0.5% in April. This was the first month-over-month drop in the PPI in over a year, and the largest in five years. Following Tuesday’s lower-than-expected report on consumer inflation, this should be welcome news for the Federal Reserve. However, with significant tariff uncertainty, this trend in lower inflation may still not be enough to convince the Fed to reconsider its “wait and see” approach to rate cuts.

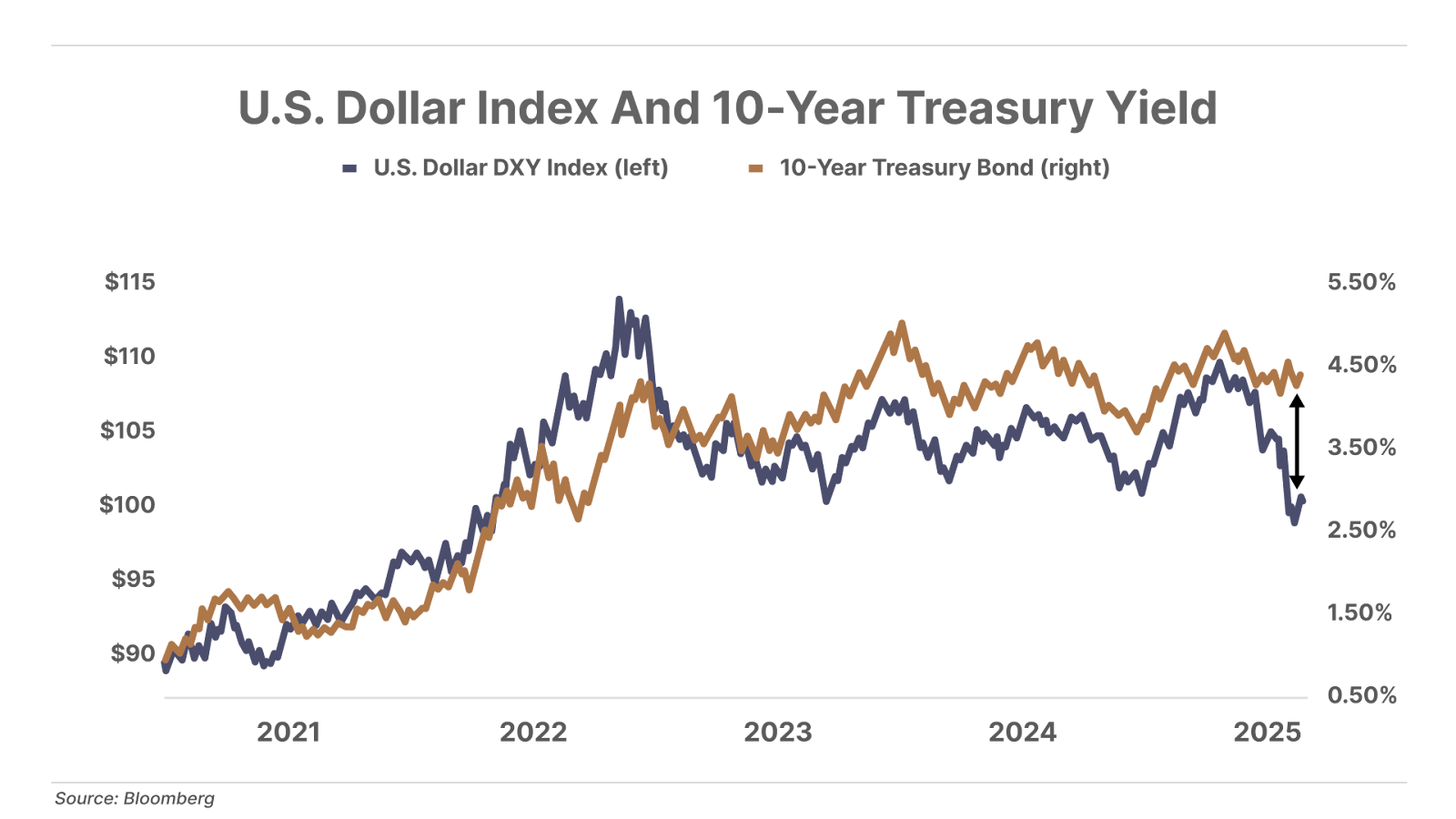

2. The world is losing confidence in the dollar. U.S. Treasuries are selling off – with yields rising to 4.54% on Wednesday, before falling back to 4.41% today, yet still up from 4.16% at the end of April. Typically, rising bond yields attract capital and support a stronger dollar. But since President Donald Trump announced tariffs on many U.S. trading partners, yields have risen while the dollar has fallen. This is a sign that investors are demanding higher returns to hold U.S. debt while simultaneously losing faith in greenbacks. The traditional relationship where higher yields strengthen the dollar is breaking down. Treasury yields are flat for the year, yet the dollar index has dropped 9%. Either yields are going much higher, or the dollar has much further to fall.

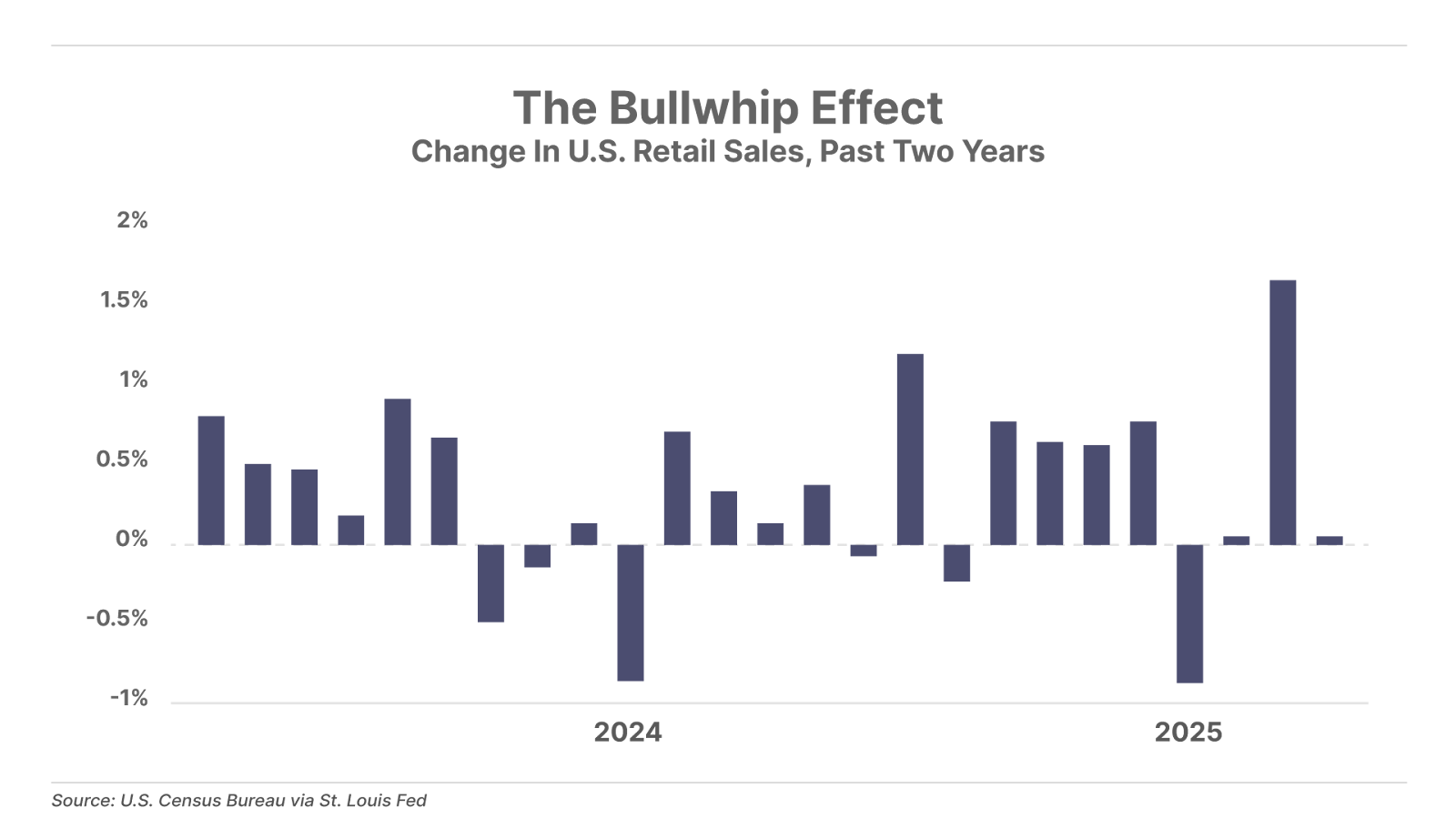

3. Tariff “Bullwhip Effect” drags on consumer spending. U.S. retail sales increased just 0.1% last month, the weakest April in two years. This followed a 1.7% surge in March, as consumers rushed to stock up before new tariffs pushed prices up. Economists expect retail sales to be weak in May and June, as the bullwhip effect of March’s spending spree reverses, amplified by higher costs due to tariffs.

Tell me what you think, I’d love to hear from you: [email protected]

Mailbag

Hi Porter,

I’ve been with Stansberry Research for a long time and am now also a Partner Pass member. I appreciate all you do.

I have a Fidelity account that I’ve had longer than I’ve known you and your work. But I am frustrated right now.

First, I’ve been trying to buy a recent Biotech Frontiers recommendation. However, I put in offers to buy at the current ask price, but they keep not getting filled. I almost never place a market order as it leads to (sometimes) unpredictable results. But I have never seen a situation where I am placing orders either within the spread or at ask and not get filled, and for multiple days. Especially with this kind of stock, market orders can be dangerous.

Second, I find that I can’t trade many of the distressed bonds being recommended in Distressed Investing on Fidelity. I’ve reviewed the recommendations and it looks like Schwab is about the only brokerage that will go out to a third party. Fidelity needs to have “inventory” for me to purchase. They will consider filling an order with a minimum trade of $50,000.

I am looking forward to growing the allocation I’ve made to Porter & Co. recommendations. Many of them are amazingly compelling.

Bill K.”

Porter’s comment: Thanks for your support of me and my companies. And I’m happy to take your questions.

1. Honestly, it beats me. You’re talking about a thinly traded penny stock. I wouldn’t expect getting filled at good prices is likely.

2. Sounds like you might have to get a better broker for your corporate bond investments. Obviously, I don’t make those decisions for Fidelity, but their attitude about that market isn’t surprising. It’s mostly a market for institutional investors and they aren’t eager to share it. We have had good feedback about Schwab and Interactive Brokers. It’s not hard to open an account with either.

Hope that helps –

Porter

Good investing,

Porter Stansberry

Stevenson, Maryland

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.