Issue #21, Volume #2

Warren Buffett’s Biggest Investment Mistakes

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| Shocking analysis: Why Berkshire Hathaway should be broken up (Hint: Buying windmills is a bad idea)… Porter reviews Buffett’s annual letter live tomorrow @ 3 pm (for Partners only)… The world is selling U.S. Treasuries for gold… |

Editor’s note: I’ve learned a lot about Berkshire Hathaway from Whitney Tilson, who is probably the most famous “Buffett-watcher” on Wall Street. Tilson has been to every Berkshire annual meeting for the last 25 years and, you should know, he doesn’t agree with my analysis below. But we do agree that major changes are needed in New York City, where I am a part-time resident (Hudson Yards) and where Tilson is running for mayor. If you are a resident of New York City, I’d like to invite you to sit down with me and Tilson on March 3. I’ll pay for dinner – but we need you to make a donation to Tilson’s campaign. Please do so here, so that we can enjoy a safe and sane city again.

For the last 60 years, investors have enjoyed a “free ride.”

The only thing you needed to know about investing to beat the market by a wide margin was the name “Warren Buffett.”

Warren’s character and his extraordinary intellect led to the greatest economic engine since Standard Oil: an economic powerhouse virtually without peer in the entire history of capitalism. But, much like father time, there is no way to outrun the inevitable impact of trying to compound enormous amounts of capital.

Buffett has long warned that the growing size of Berkshire Hathaway’s (BRK) portfolio must, inevitably, begin to negatively impact its returns on invested capital. And that’s certainly occurring – though for reasons that are not obvious.

As I first warned in a series of essays in 2018, Berkshire Hathaway is virtually certain to underperform the market going forward. Buffett underperformed in 2019 and in 2020. He underperformed in 2023, and I’m virtually certain he underperformed again last year.

Since 1999, Buffett has underperformed the S&P 500 10 times on an annual basis. And that’s going to occur more and more often – no matter who is running Berkshire.

Before I write anything further, let me please explain that I have more respect for Warren Buffett than any other investor, dead or alive. There is no question that he is the greatest investor of all time and one of the greatest Americans who has ever lived. I have learned virtually everything I know about investing from Buffett. And I’ve read everything he’s ever written – and most of those things, a dozen times or more.

Buffett has made a few mistakes in his thinking over time. Not many. But there are some significant flaws in the way he views resources and humanity. Meanwhile, his belief in his own judgment is absolute, which means these flaws have led him to make some very big mistakes.

What am I talking about?

Buffett has long held Malthusian ideas about population and resource scarcity.

Studying Buffett you’ll discover he’s constantly doing math in his head. He counts everything, all the time. Because he counts everything, constantly, he understands exponential growth in a way very few other people do. He thinks about numbers compounding all the time. He doesn’t think about the price of things. He thinks about the impact of spending that capital instead of allowing it to compound for decades. And he can do that kind of complex math accurately in his head, in real time.

To someone with a mind like that and firm belief in linear, compounding numbers, reading things like The Population Bomb and other books predicting that the exponential growth of humans would soon outstrip our ability to produce commodities would be terrifying. These ideas have resonated with Buffett his entire life, because to him the math was linear, and it was right.

Thus, Buffett has done everything possible to reduce the growth of the human population.

Buffett has donated billions of dollars to support and promote abortion through the Buffett Foundation. Without Buffett’s direct financial support, the “abortion pill” would have never been produced in America. He provided millions in funding for the clinical studies and provided capital to the company, Danco Laboratories, which developed it. The Buffett Foundation even financed lawsuits to overturn the federal ban on late-term abortions, though these bans were upheld by the Supreme Court.

Regardless of where you stand on the issue of a woman’s right to abortion, it is hard to stomach the idea of promoting late-term abortions, in which otherwise viable humans are destroyed using methods that are obviously traumatic.

And then there’s this.

Before Roe v. Wade legalized abortion nationwide, Buffett and the late Charlie Munger, Berkshire’s vice chair, personally founded a “church” – the Ecumenical Fellowship – to finance an underground network that would transport women to states where abortion was legal. The legality of these actions was… cloudy.

It is hard for me to square the idea that a man I admire so much for his mind, for his kindness, and for his character could have done so much to contribute to the tragedy of abortion. But these are facts.

I attribute these mistakes to Buffett’s flawed understanding of resources. Thanks to humans (which are the ultimate resource) and human innovation, there’s no such thing as an economically scarce resource. Or as this concept was first explained to me, the stone age didn’t end because we ran out of stones. In every epoch of human history, new and better critical resources have been discovered, which enabled human populations to grow.

And today, thankfully, it is obvious to almost everyone that as societies become wealthier, birth rates fall. Native population has begun to decline in virtually every developed country. Soon, the major threat to the world’s economy will be too few people.

In addition to Buffett’s promotion of abortion, we can also see the impact of his Malthusian philosophy in his massive investments into “renewable” energy.

Buffett has long embraced the idea of “peak oil,” saying many times in public that we should be conserving our supplies of oil as carefully as possible because we could run out of it in only a few years.

These predictions have always proven to be laughably wrong, unlike in Buffett’s head where the numbers always compound on a linear scale, innovation compounds geometrically, but not in a way that can be predicted. A recent example is how parallel-processing computer systems have dramatically expanded computer efficiency at far faster rates than was predicted by Moore’s Law, which had a Buffett-like perfectly linear growth rate that could be computed easily.

These kinds of “breakthrough” innovations can’t be forecast or modeled precisely, and thus, Buffett doesn’t know how to handicap these kinds of changes. He’s been famously skeptical that these kinds of “miracles” would continue to occur in the oil industry.

And yet… since the very beginning of the oil industry there’s been one breakthrough after another that has allowed proven oil reserves to increase at the same rate as increases to production. That continues today. Back in 2009, the Energy Information Administration reported there was a total of 20.6 billion barrels of proven oil left in the U.S. Since then, U.S. production has grown from around 6 million barrels a day to just over 13 million barrels a day, transforming the U.S. into a major crude oil exporter. But… are we going to run out? Of course not: proven reserves have expanded at the same rate, to over 50 billion barrels.

The more oil we produce, the more we discover. How? This is the law of human abundance: people are the ultimate resource.

Buffett has never understood any of this, and, a result, Buffett has frequently made huge and disastrous investments in energy.

I’d bet there’s not another equity analyst in America who understands how much money Buffett has lost investing in energy over the last 25 years.

These investments have been disasters!

But they are largely hidden from view because they’ve (mostly) taken place inside his wholly owned businesses.

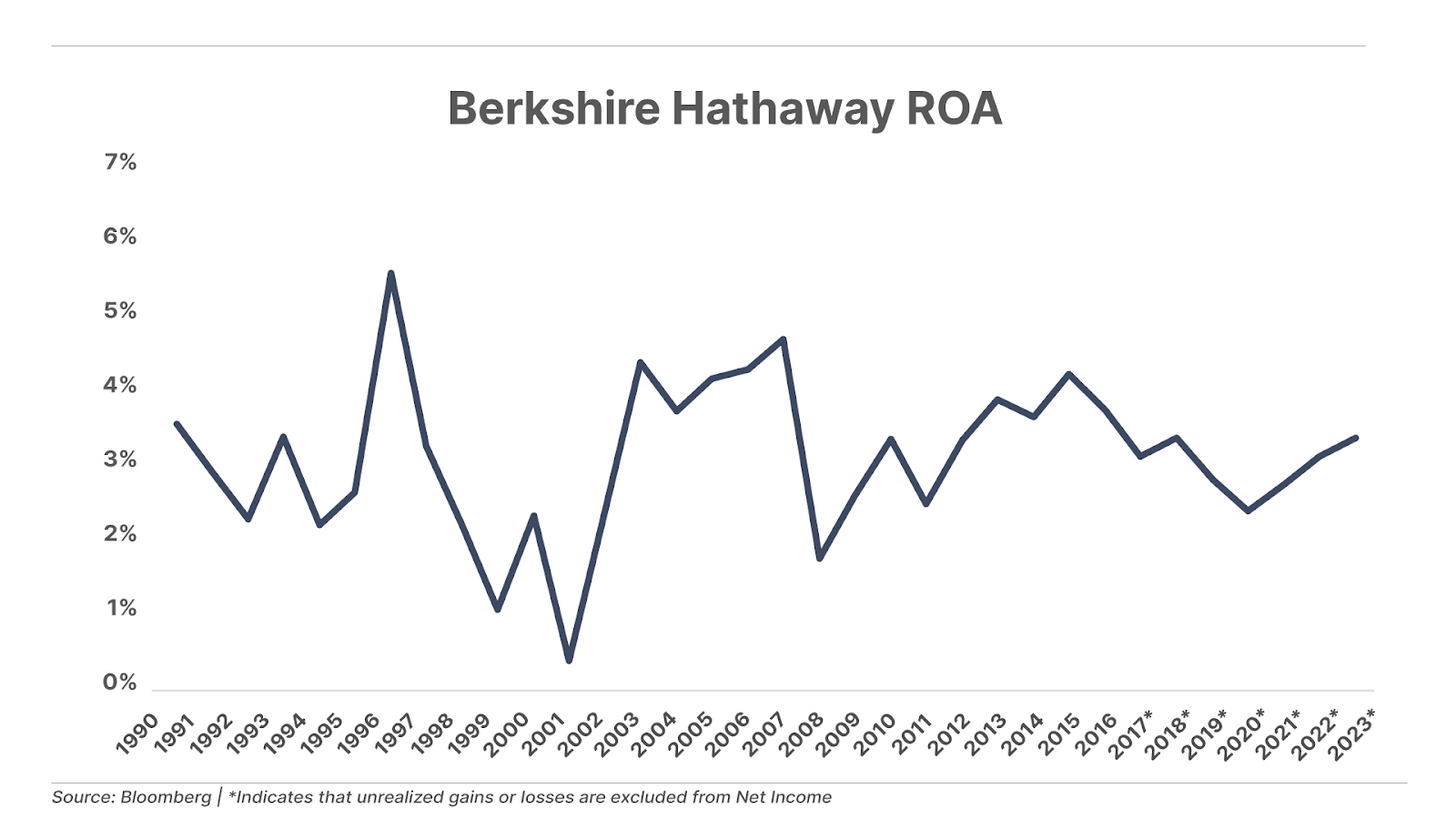

Here’s an interesting fact: Buffett’s massive losses on energy have made Berkshire’s return on assets (“ROA”) decline over the last 25 years. And, unless Berkshire is broken up, these declines are going to accelerate going forward.

If you believe we are running out of oil and you want to save the country, you’d be willing to invest billions to expand the electric grid (because soon cars and everything else will have to run on electricity) and you’d willing invest billions in wind and solar energy, no matter how inefficient.

And, if you were right, then these investments would become immensely more valuable. But if you were wrong, you’d be facing huge losses.

Let’s look and see what happened…

In 2000, Buffett closed on the $4.3 billion acquisition of MidAmerican Energy. Today that subsidiary (which you’ll see has grown) is called Berkshire Hathaway Energy (“BHE”).

It owns a host of enormous assets, including: Northern Natural Gas (a $1 billion pipeline that used to belong to Enron), PacifiCorp ($5 billion electric utility serving notoriously liberal Oregon), Kern River Gas Transmission ($1 billion gas pipeline), NV Energy ($5 billion electric utility in Nevada), and Dominion Energy ($10 billion gas pipeline).

Altogether these assets cost $22 billion, in cash. I’m not including the assumed debt in these deals. But that’s just the beginning of the investment that’s required to own and operate these assets: these assets require massive amounts of capital spending every year for maintenance.

These businesses (or their customers) are regulated utilities, where prices are set by government authorities. Meanwhile, the input costs of these businesses are driven by market forces, like interest rates and commodity prices. When you look under the hood, the returns on these investments are all driven by factors (politics, commodity prices, interest rates) that are very difficult (aka, impossible) to manage.

This entire area of the market is like a blind canyon: once you fly into it, there’s no way out.

And Buffett has spent almost $100 billion on these businesses over the last 25 years.

That’s far more capital than Buffett allocated into his three all-time largest equity investments. It’s 3x what he invested in Apple (AAPL); 5x what he invested in Bank of America (BAC); and almost 10x what he invested in Verizon (VZ).

The 2023 Berkshire annual report revealed that Berkshire Hathaway Energy invested $39 billion in capex from 2014-2023. Almost all of that was spent on building windmills and solar panels ($34 billion). In the years before these major investments, company reports and investor presentations show capex between $1 billion and $2 billion per year, mostly for wind projects in Iowa. More recently, the company has been spending heavily (almost $10 billion a year) on wildfire mitigation and related transmission line improvements.

When you add up all the numbers, after buying these firms, Berkshire has invested another $70 billion in these businesses. That means Buffett has invested a total of almost $100 billion in these energy-related assets. But guess how much money Berkshire Hathaway has made from this, its largest-ever investment.

Almost nothing.

Incredibly, unlike every other subsidiary in Berkshire’s holding company, Buffett never required BHE to send cash back to headquarters. Buffett never took a single dividend from BHE until the legal risks of the wildfires started to become a threat to the business’ solvency. BHE has only paid one dividend, ever, to Berkshire: $1 billion in 2023.

Not taking out cash along the way has been a huge mistake.

Currently third-party estimates (S&P Global) place a fair value for all of BHE (net of all debt) at around $80 billion.

Thus, Buffett has invested almost $100 billion into assets that, after 25 years, are worth considerably less than what he paid for them. Do you remember Buffett’s #1 rule for investors? It’s don’t lose money. Rule #2 is never forget rule #1.

What happened here…? I believe the explanation is that Buffett badly misjudged the basic economics of the energy business. He believed that energy prices would climb enormously. And, of course, they haven’t. Adjusted (for inflation) into current dollars, a barrel of oil was $168 in 1979. The average inflation adjusted price for oil since 1946 is around $60 a barrel, or just a little less than today’s $70. In other words, despite massive growth in demand, the price of energy (a basic commodity) hasn’t gone up much.

But the costs of everything else in those businesses sure has: especially the cost of transmission lines and liability.

BHE now faces $10 billion to $40 billion (!) in wildfire liabilities. Take a mid-point of these risk estimates – say $25 billion – and you get a fair value for BHE of only $55 billion, implying that Buffett may have lost around half of his investment in these assets over the last 25 years.

You’d think that’s something The Wall Street Journal or CNBC would ask Buffett about – but that won’t happen. Nobody wants to challenge him because he’s an enormous draw for the audience.

And energy isn’t the only big mistake, either.

Buffett’s railroad investment hasn’t gone much better. I’ll spare you all of the details, but the math is pretty clear. Not including any of the debt he assumed, Buffett spent $34 billion (and that included $18 billion in Berkshire shares!) in 2009 to buy BNSF Railway, which, at the time, was America’s best railroad. Since then, he’s taken $57 billion in dividends – which sounds pretty good. A lot better than BHE!

But… BNSF has also spent $56 billion in capex, which means Buffett has had to continue to invest almost as much capital into the railroad as it has been able to pay him. That’s the trouble with capital-heavy businesses. And the returns on these continuous investments aren’t great.

Fair market value for BNSF today is around $90 billion. Adding together realized gains ($57 billion in dividends) and unrealized capital gains ($56 billion) gives you total returns of $113 billion. Divide that by Buffett’s $34 billion acquisition cost and you see a 333% return. Sounds good. But it’s only 10.3% annualized – which has underperformed the S&P 500 by about 2% a year.

What’s fascinating to me about both these investments is how different they are from Buffett’s traditional investment style. Buffett practically invented the high-quality, capital-lite investment approach of buying consumer branded businesses with incredible returns on equity. Think about it: Buffett was selling McDonald’s (MCD) in 1999 to fund his purchase of MidAmerican Energy! Just imagine Berkshire’s returns if, instead of spending $100 billion on energy over the last 25 years, he’d simply kept buying shares of McDonald’s. Or American Express (AXP). Or Coca-Cola (KO).

Sure, it’s easy to be a Monday-morning quarterback, but both the power company and the railroad were bought during periods of dramatic market turmoil (2000 and 2009) when Buffett had virtually unlimited opportunities to buy ultra-high-quality businesses.

Instead, he bought things that were designed to survive (or service) the end of the world: windmills, the railroad, the largest bank (Bank of America).

(The returns on Bank of America have been lousy too. Despite getting the preferred shares and the warrants at the beginning of the deal, Buffett’s total annualized return on these investments comes to “only” $20.7 billion, or 238% over 13.5 years, or 9.4% annualized. That’s a very significant underperformance of the market, by more than 3% a year.)

On October 16, 2008, Buffett famously wrote in The New York Times that he was “buying America.” But was he? Kinda. He was buying relatively low-quality assets that would require massive amounts of additional capital.

And nobody even mentions this, but Buffett bought a huge position in Verizon (VZ) in the fourth quarter of 2020, long after the market bottom of March 2020. Once again, every high-quality business in the world was on sale… and he bought Verizon? He invested a total of $9.1 billion (!) in a very capital intensive, intensely competitive, low-margin, highly regulated business. He started selling – at a loss – a little over a year later.

Total loss? About $250 million, including the dividends.

This was the strangest investment I’d ever seen Buffett make. It was an enormous position in a business that couldn’t possibly beat the market. Made no sense.

For the last decade, Berkshire has been able to cover up its massive losses in BHE and its poor returns on the railroad, because of the incredible performance of Apple.

Buffet bought $11.4 billion worth of Apple at different points between 2016 and 2022 – he bought the dips. And he made an absolute killing – the best investment in the history of the capital markets. Buffett has made at least $92 billion (from realized sales) and $4.5 billion in dividends. Assuming $65 billion in unrealized gains, his total returns are well over $150 billion – about 32% a year!

But Berkshire has now sold 67% of its Apple shares. And Apple hasn’t been growing. (We wrote about the challenges that Apple faces in The Big Secret On Wall Street yesterday.) It will get a lot harder to cover up the huge amount of assets on Berkshire’s balance sheet that are not performing well.

The solution? To me, it’s obvious.

The energy assets and the railroad need to be spun off – as quickly as possible. These businesses can be funded, completely, with debt. They will be slow growing. They will trade at a cheap multiple. And they will pay reasonable dividends to “widows and orphans” – investors who need income and security.

The investment portfolio and the insurance companies (which must be funded with equity) should retain the Berkshire Hathaway name. They should resume Buffett’s former investment strategy: funding a world-class investment portfolio with “float” generated from high-quality property & casualty stocks. Profits and dividends from these capital efficient businesses should be sent back to headquarters to be reinvested in other ultra-high quality companies. No more regulated utilities. No more commodity businesses. No more poorly run banks. And definitely no more windmills and solar panels.

If you’re interested in these ideas, I’ll be going over Buffett’s new shareholder letter tomorrow afternoon. The letter comes out at 8 am ET. I’ll read it carefully. I’ll be sharing my findings with Partner Pass members, on a live webcast at 3 pm. We recently closed our Partner Pass promotion… but if you’re still interested in becoming a Partner, get in touch with Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447. We’ll re-open the offer if you mention this Daily Journal, and you’ll get access to the recording of Porter’s presentation next week.

Three Things To Know Before We Go…

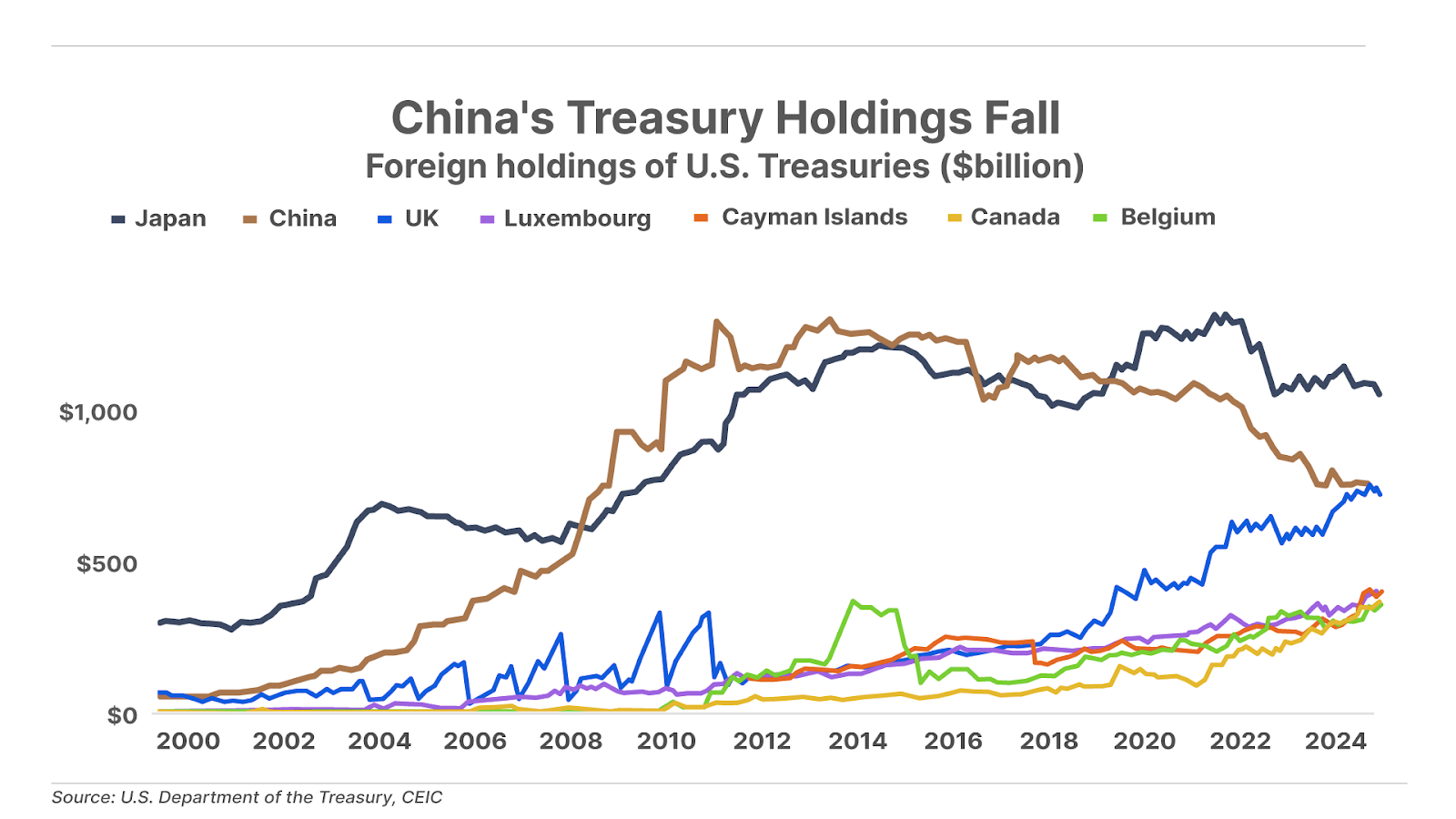

1. Global investors dump U.S. Treasuries for gold. Foreign holdings of U.S. Treasuries fell by $49.7 billion in December, the largest drop since March 2021. Overseas investors are increasingly shifting to gold as an alternative to Treasuries, including central banks, which bought a record 333 tons of gold in Q4. This shift is being led by China, which sold $77 billion in Treasuries to end the year with just $759 billion, its lowest level since 2009, while boosting its gold reserves to new highs. Other countries are joining the global scramble for gold, including India, where the central bank boosted its gold holdings by five-fold last year.

2. Walmart’s earnings reveal a bleak picture for the low-income consumer. While Q4 sales were strong, Walmart (WMT) is increasingly reliant on higher-income shoppers, signaling a financial strain among the lower-income customers. Walmart CFO John David Rainey noted that “wallets are still stretched,” with U.S. shoppers continuing to spend but remaining cautious. Walmart’s 2025 sales growth forecast of 3% to 4% falls short of expectations and barely keeps pace with inflation hovering at around 3% – indicating little to no real growth. The shift in spending patterns and sluggish growth signals broader weakness in retail and the overall economy.

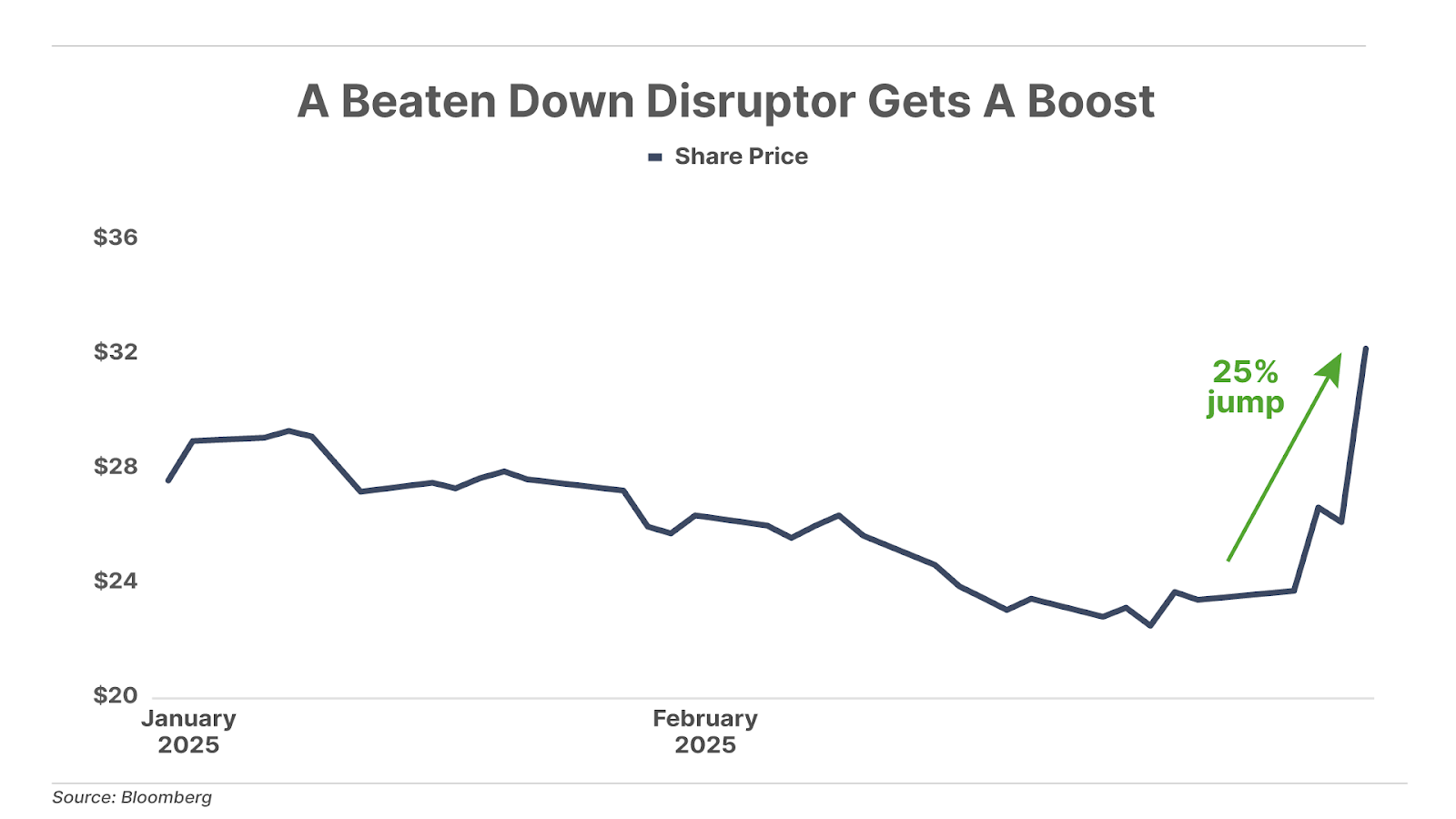

3. A beaten-down disruptor gets a 25% boost. Shares of a disruptive consumer brand in The Big Secret portfolio received a 25% boost today after announcing better-than-expected earnings, plus an acquisition that should turbocharge its growth. We originally recommended this stock last March, and though shares have tumbled since then, the latest earnings results indicate the company’s operational obstacles have now passed. And with this latest acquisition, we believe the stage is set for a breakout year in 2025. (Partner Pass members read about this today on Direct Line.) If you’re a Big Secret subscriber (or Partner Pass member), you can read our latest update here… if you’re not and want to learn more, go here.

Why Trump Might Be Done In 60 Days

Against all odds, Donald Trump is back in the White House and already putting his bold plans in action to reverse the damage crooked Joe did to America. But there’s something brewing under the surface that no one’s talking about except for one man. He is one of the world’s top forecasters, known for predicting the crash of ’87, the second biggest bank failure in history, and even the deadly floods and fires we’ve recently seen in America. Now, this master market timer says that President Trump’s second term could enter a death spiral – in less than 60 days. Click here to learn why.

Good investing,

Porter Stansberry

Stevenson, MD