Issue #12, Volume #1

If You Print Enough Money And Spend It, Inflation Will Happen

| Editor’s note: Before we get to the financial stuff, a word about something that’s more important. Back in September, I decided that I had to do a better job of taking care of myself. That’s easy for me because my wife Shannon is a yoga instructor, health coach, and a model. Health isn’t just her passion – it’s her job. I asked her to lead me through a 30-day fitness challenge. And I invited all of you to join us. Dozens of people did. It was an incredible experience to see so many people “come back to life” by adding routine, simple movement, and meditation to their daily routines. It’s incredible how much better I feel, and how much more I’m in control of my mind and my emotions when I follow these simple routines. If you’ve ever wanted to feel better, to think better, and to sleep better… not to mention, I lost 15 pounds in a month…. I urge you to take this 30-day challenge. Shannon is launching a new one next week, on Monday, October 7. Please, don’t let better finance and investing insight be the only thing you let us give you this year. Sign up right now and join our next 30-day challenge. |

Three Things You Need To Know Now:

Today there’s only one thing you need to know… but the consequences come in three parts.

1. Jobs report spooks the bond market. Today the Bureau of Labor Statistics released the September payrolls data and, after months of weakening data, suddenly the economy added 254,000 jobs in September, which was way more than the 100,000 jobs that economists expected… Virtually every news source reported this jobs data and concluded, like good minions, that this is a sign that Bidenonomics (and that our economy) is sound. In another reversal of trend, both the last two previous monthly releases (July and August) were revised upwards. As a result, the unemployment rate for September fell to 4.1%. But, as I warned you about yesterday (telling you not to own any long-dated U.S. government bonds), what’s not being reported is the cause behind this strong economic data…

2. Government debt is now up $2.1 trillion in the last 100 days. We have never experienced this kind of Banana Republic-stye economic manipulation in the U.S. The administration is spending on everything, as fast as it possibly can, to make sure there’s not a recession before the election. The Fed cutting short-term rates in the face of this massive deficit spending ensures that inflation isn’t going to subside. As a result, long-term government bonds are crashing, sending the 10-year Treasury yield ripping higher. Yields on the U.S. 10-year bond are now up from 3.6% – prior to the Fed cutting rates – to 3.94% today. That’s a huge move in less than a month. If, as I expect, inflation data follows the employment numbers higher, then I expect we will see 5% rates by the end of this year – rates that we haven’t seen in more than 20 years. That implies enormous losses to the bond market. There are currently $27.6 trillion of outstanding U.S. Treasury bonds and another $11 trillion of outstanding corporate bonds. Higher inflation means very large losses for the holders of long-dated bonds.

3. Bank of America (BAC) is in big trouble. Bank of America, America’s largest depository institution, owns $585 billion of long-dated government bonds and government-backed mortgages, purchased during the summer of 2020 near all-time lows of interest rates. Losses on these bonds previously peaked at $131.6 billion in October 2023. But, if I’m right, and the 10-year yield goes back above 5%, then Bank of America will see its losses grow. The bank’s total equity is $293 billion. Its Tier One capital is around $200 billion. If rates go to 5% or higher, Bank of America will most likely become insolvent. Also, in what I’m “sure” is just a coincidence, Warren Buffett is liquidating Berkshire Hathaway’s (BRK) huge position in the bank, selling more than $10 billion worth of shares (around 250 million shares, or 3% of total outstanding) since July.

And… then… there’s this fact, which nobody in the media has even bothered to mention…

And one more thing…

On September 30, which was the last day of the third quarter, a bank (I wonder which one) pulled $2.6 billion in cash from the Federal Reserve’s repo facility for emergency liquidity. These repo agreements allow the Fed to give banks loans based on the face value of the bonds they exchange – rather than on the current market price. The sums of cash drawn from the repo facility will increase more and more and Bank of America’s losses mount. Sooner or later this hidden bailout will become a huge political football. And I don’t expect the shareholders are going to prosper.

Always Own These Businesses… Always

If there’s only one business to teach your children, it should be insurance – specifically property and casualty insurance.

I’ve written volumes about this industry in the past. You can learn everything (if you’re a paid-up subscriber) that you need to know in our report The World’s Greatest Investment: Guide to Property & Casualty Insurance Investing. (And if you’re not a subscriber to The Big Secret (or a Partner Pass member), I urge you to learn more about the sector that I believe is the most powerful wealth-creation machine on earth.)

There’s a simple reason why this industry always outperforms the stock market and always will: with disciplined underwriting, these companies get all of their capital for free. If you’re looking for a machine that prints money, it’s a heck of a lot easier if the input costs are all free.

As I’ve spent a lot of time over the last month building a new model portfolio, which we’re calling Porter’s Permanent Portfolio, for subscribers to The Big Secret On Wall Street and our Partner Pass members, I’ve been studying what kinds of portfolios are resilient. Building a portfolio is a completely different challenge than simply determining what stock is attractive today, relative to others.

What you want is a business that will grow, consistently, for decades. Trading – which triggers taxes – is the enemy of portfolio performance. To build real and lasting wealth with your investing, you need a portfolio that’s completely bulletproof and that contains high-quality businesses that can grow your wealth for decades. And, ideally, you’d most want to own a collection of businesses that have both higher returns on invested capital (than other businesses), and lower volatility than other shares. That would set a situation where you could, if you wanted, safely leverage your investments to produce results that vastly outpace the stock market.

Doing the research on what kinds of businesses can do that, I found two industries that stood out: branded consumer products – think Philip Morris International (PM), Coca-Cola (KO), McDonald’s (MCD), Procter & Gamble (PG), Walt Disney (DIS) and, not surprisingly, property and casualty (“P&C”) insurance.

And, even though I’ve been writing about the sector for more than a decade, I still don’t believe most people understand how resilient or how profitable good insurance companies can be… for decades.

But here’s what I can tell you: if you haven’t been able to make 20% a year with your portfolio over the last 30 years, you shouldn’t buy anything else besides great consumer brand companies, like Domino’s Pizza (DPZ) to cite a recent recommendation, and P&C insurance companies. Some investors can do better than 20% a year – look at Marty Fridson’s results in Distressed Investing. Look at Erez Kalir’s results with Biotech Frontiers. But, for us mortals, there’s simply no way to make more money consistently than with P&C insurance and great consumer brand companies.

Caveat – price matters. But assuming you’re relatively disciplined about your entry prices, it’s awfully hard to screw up if you stick to P&C insurance and great consumer brands.

I began recommending P&C insurance stocks in 2012 when I hired two great accountants with deep experience in the sector, Bryan Beach and Mike DiBiase, to help me generate alpha (which is excess returns) in the sector.

Since then, Stansberry Research has recommended 16 different P&C insurance companies. All but one was a profitable investment. And the combined returns, from both open and closed positions, is currently 25% annually. That beats both the S&P 500 and the U.S. Insurance ETF (IAK). And, underappreciated, is that the beta – the volatility of these stocks compared to the S&P 500 – was 0.80 (the S&P is the benchmark at 1.0, and lower than 1.0 means less volatile). What that means is that this portfolio of insurance stocks was able to produce market-beating results, with substantially less risk than the market as a whole.

Was it just luck? No. There’s a simple and fundamental reason why these businesses outperform: they get their capital for free. You pay for insurance upfront. And, most of the time, you never file a claim. Even when you do file a claim, those demands typically come over time – giving the insurance company a free window of time on using your capital.

As paid-up subscribers know, the results from our P&C insurance recommendations in The Big Secret on Wall Street have been even better (albeit over a much shorter time period) than the long-term results we achieved at Stansberry Research. In just over a year, we’ve seen gains of: 58%, 93%, 53% and 70%, for an average of 68%. And our latest P&C insurance recommendation, which entered our buy list only in May, is up 24%, so far.

As paid-up subscribers also know, we also have several world-class consumer brand companies in the portfolio, most of which are trading at very attractive prices, including: PayPal (PYPL), Deere & Co. (DE), Diageo (DEO), Nike (NKE), The Hershey Company (HSY), Celsius (CELH), and Philip Morris International (PM).

If you want to build an economic fortress, this is the formula:

Savings + P&C insurance + great consumer brands + time = wealth

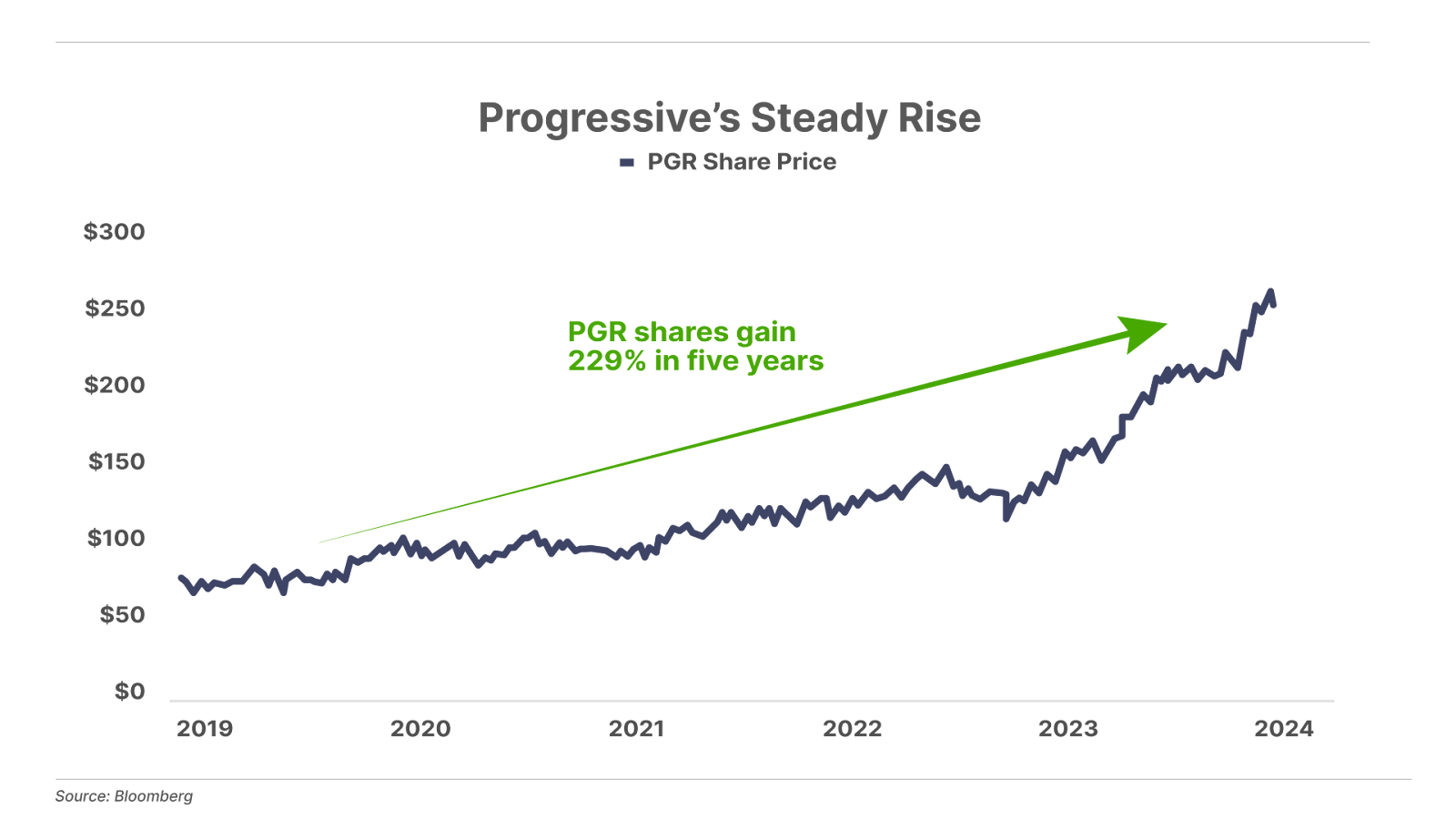

Chart of the Day: It’s Not Sexy, But It Works

Why do I teach my children how to invest in what I call “God’s Investment” – property and casualty insurance? Well, if my parents (God bless ’em) had invested just $1,000 for me in Progressive (PGR) back when I was born in 1972… those shares would be worth $8.7 million today. (And if you’ve seen the share price of MarketWise (MKTW) lately, you’d know: I could use the money.)

Progressive has been a leading pioneer of using technology to better understand and price risk. The result? They refer the customers they believe are higher risk to their competitors, while offering vastly lower rates to the people they believe will never file a claim. That strategy has led to both incredible underwriting results and huge growth in market share. Since recommending Progressive less than a year and a half ago, it’s almost doubled.

The Mailbag

I’d love to hear your insurance stories. Have you bought P&C yet? Why not? Please let us hear from you this weekend. How do you like the new Daily Journal? Why will you or will you not invest in biotech? We want to know: [email protected]

Ron Burgundy perfectly sums up my brief experience with biotech stocks after returning from your conference. After listening to Erez’s logical, methodical framework for evaluating biotech stocks, coupled with his in-depth experience, knowledge and contacts I had the confidence to put together an initial basket of his recommended stocks. Within 48 hours, [one of his latest recommendations] received a Breakthrough Therapy Designation that more than pays for my VIP ticket to next year’s conference. You and your team put on a top-shelf conference with excellent speakers, great facilities, and wonderful food and refreshments. I look forward to coming up next fall.

– W. Wilson

Porter’s comment: Erez’s performance isn’t human. The stock you mention is up 56% since Erez pitched it to our conference a week ago. Keep in mind, Erez originally recommended this stock back in January as a part of our initial 10-stock basket of negative-EV (enterprise value) biotech stocks. It tripled, moving from $6 to $20, where we sold to bank those profits.

Meanwhile, a slew of world-class biotech investors (including the Baker Brothers, BlackRock, etc.) piled into the stock at $12.50 in March. But, shortly after that financing, its share price went into a deep decline, moving even lower than Erez’s original buy price. So, last month, Erez did another deep dive on the company and recommended it again, at prices below $3. Today the stock is up 67% since his second recommendation.

And, what most people can’t really grasp is that these results are nothing compared to what’s going to happen in this portfolio over time. I’m not suggesting that anyone put 50% of their portfolio into biotech – it’s volatile and risky. But I am telling you, if you follow Erez, you’ll see a 200% to 400% pre-tax return on your investments over the next 12 to 36 months. And, possibly much more. (Be sure to check out Erez’s latest recommendation – released yesterday – here.)

Good investing,

Porter Stansberry

Stevenson, MD

P.S. I gave the Porter & Co. conference planning team a heart attack last month, when just days before Porter & Co. annual conference I insisted that they make space for the analyst responsible for a publication called Compounding Quality to speak.

Pieter Slegels, the young Belgian man behind Compounding Quality, has views on investing that are eerily similar to mine. He’s like my investing brother from another mother. And I wanted our conference attendees to hear what Pieter had to say.

And he didn’t disappoint. Pieter impressed the audience with his focus on exceptionally high-caliber companies that have big moats and trade at a reasonable price.

The fact is: Pieter is one of a kind. While he’s still a young man, he’s got the insight (and performance) of an investor with decades of experience, and following his ideas could make you a lot of money. You can read an example of his work – this is normally available only to subscribers – about “The 10 Stocks to Own Forever” here.

To find out more about Compounding Quality, and get the full portfolio and all of Pieter’s ongoing analysis and recommendations, check out the special offer Pieter has put together exclusively for Porter & Co. It’s a fantastic deal: You’ll receive the Founding Partner package for the price of an annual membership (on the web page link, just select the “Annual” choice, and Pieter will manually upgrade you.)Pieter also joined me and Aaron on the latest Black Label Podcast, which you can watch right here.