Issue #38, Volume #2

The Best Approach Is Simply To Ignore All Macroeconomic Risks

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| Purchase, at a rational price, a part interest in an easily-understandable business… Here is a real example of a multi-generational family business at a great price… People have been drinking wine for all of human history, and they will likely continue to do so… The Big Secret’s “Best Buys”… |

In the Journal today, I want to give you the single best piece of advice I ever got about investing. And I want to show you – with a real example – exactly what a great investment looks like.

In 1996, in his annual letter, Warren Buffett spelled out exactly how to become a great investor:

To invest successfully, you need not understand beta, efficient markets, modern portfolio theory, option pricing, or emerging markets. You may, in fact, be better off knowing nothing of these…

Your goal as an investor should simply be to purchase, at a rational price, a part interest in an easily-understandable business whose earnings are virtually certain to be materially higher five, 10, and 20 years from now…

You must also resist the temptation to stray from your guidelines: If you aren’t willing to own a stock for 10 years, don’t even think about owning it for 10 minutes.

When carried out capably, an investment strategy of that type will often result in its practitioner owning a few securities that will come to represent a very large portion of his portfolio. To suggest that this investor should sell off portions of his most successful investments simply because they have come to dominate his portfolio is akin to suggesting that the Bulls trade Michael Jordan because he has become so important to the team.“

And Buffett offered this one important caveat:

Investors making purchases in an overheated market need to recognize that it may often take an extended period for the value of even an outstanding company to catch up with the price they paid.”

Today, there’s more macroeconomic risk to our economy than there has been since the 2008 Global Financial Crisis.

That’s led many risk-averse investors to sell stocks, to raise cash, and, in general, to “batten down the hatches.” And doing so might be important to you. My advice is not to have any capital that you might need within five years invested in stocks – see Buffett’s 10-year rule above.

But, for investors with an appropriate time horizon and who have the emotional fortitude to sit quietly through volatility, my best advice is simply to ignore all macroeconomic risks.

I’ve been investing in stocks since 1992. The first stock I ever bought was Coke (KO). The second was Amazon (AMZN) in 1997. I’ve invested through the: ’94 peso crisis, ’97 Thai baht crisis, ’98 Russian default and Long-Term Capital Management collapse, ’01 tech bust, ’08 Global Financial Crisis, ‘15 oil collapse, and the ’20 COVID collapse.

I knew that none of these macro events were going to permanently impair the value of my best investment ideas: Coke, Amazon, NVR (NVR), Moody’s (MCO), McDonald’s (MCD), Texas Pacific (TPL), Franco-Nevada (FNV), The Hershey Company (HSY), WR Berkley (WRB), etc. Great businesses weather storms. For good investors, there’s no better way to protect the value of your savings.

My dad has been an investor in Coke stock since the late 1970s. Coke has been his largest position – and frequently his only position – for more than 40 years. When the market crashed in 1987, shares of Coke fell almost 20% in one day. My mom was beside herself – worried they would lose their life’s savings. I asked Dad how much money they’d lost. And I’ve never forgotten his reply:

Porter, I own exactly as many shares of Coke today as I owned yesterday. I haven’t lost anything.”

As we approach yet another macroeconomic storm, my advice to you is to make sure you own great businesses. Make sure you understand their business models and keep tabs on whether you believe they are continuing to build their moats. If so, ignore everything else.

What is a great business? Buffett explained:

No sensible observer – not even these companies’ most vigorous competitors, assuming they are assessing the matter honestly – questions that Coke and Gillette will dominate their fields worldwide for an investment lifetime. Indeed, their dominance will probably strengthen. Both companies have significantly expanded their already huge shares of market during the past 10 years, and all signs point to their repeating that performance in the next decade.”

I could give you a bunch of other specific data points. But is that really necessary? How long have you known that Apple (AAPL) is a dominant provider of consumer tech products? Remember when it was featured in the movie Forrest Gump as the secret to the family’s wealth? That was in 1994 – more than 30 years ago!

Did you need to see any financial statements to know that Apple is a great business? No. That’s been blindingly obvious for at least two decades. Remember: there are no bonus points for difficulty when it comes to investing. All you have to do is buy great businesses at reasonable prices.

But you do need financial statements to measure price.

To maximize your future returns, it’s important that you buy great businesses when you can acquire them for substantially less than their intrinsic value. Ben Graham taught that intrinsic value is determined by multiplying the earnings per share by (8.5 plus double the earnings growth rate). So a business that’s producing $1 per share in earnings and has been growing those earnings by 10% a year, should be worth $28.5 per share. But, remember, market prices are highly influenced by sentiment and interest rates. Market prices rarely match intrinsic value.

And, one more important warning. Never buy a bad business, no matter how cheap the price.

What should you be looking for? Here’s a real, current example, which, by the way, was passed on to me by a long-time subscriber, who is a leading professional investor in Europe.

Rémy Martin makes the world’s most expensive spirit, Louis XIII cognac. It is packaged in Baccarat crystal and costs $10,000 a bottle – or more. It’s not hard to figure out that this is a great business. And by the numbers (gross margin 70%+, operating margin ~30%), it’s just as obviously a great business.

Rémy Martin was founded in 1724 by Rémy Martin, a winegrower in France’s cognac region. This is the roughly 200,000 acres that surround the town of Cognac, which is about 75 miles north of Bordeaux, near the Atlantic coast.

Rémy Martin has remained family-run for generations. Under Paul-Émile Rémy Martin (1813-1878), the company created its famous Centaur logo and decided to focus exclusively on creating the highest-quality cognac by using only eau-de-vie from the Grande Champagne and Petite Champagne crus, or growing regions.

Paul-Émile’s emphasis on terroir and aging set Rémy Martin apart from competitors that used blends from lesser cognac regions. And then… in the late 19th century when sap-sucking insects called phylloxera destroyed France’s vineyards, Rémy Martin had lots of wine aging in barrels. Rémy Martin continued to produce cognac, while most other producers failed. With a huge decline in wine production, cognac became even more expensive and more sought after globally. With these tailwinds behind him, Paul-Émile’s son, Paul Remy Martin, used the firm’s aged cognac to create two new dominant brands: VSOP (Very Superior Old Pale) and Louis XIII. In doing so, he created one of the world’s first luxury products.

After World War II, in 1948, Anne-Rémy Martin, the daughter of Paul Rémy Martin, married André Hériard Dubreuil. André was a local boy – the son of a cognac grower. But he had ambition. He went to college (École des Hautes Études Commerciales) and was determined to modernize the cognac industry. By 1965, he’d bought out most of the other family shareholders and taken control of the company.

In the 1960s and 1970s, Dubreuil expanded Rémy Martin into the U.S., partnering with alcohol giant Seagram’s. Later, in the 1980s, he targeted Asia – especially Japan and China – where Rémy Martin VSOP and Louis XIII became status symbols. (Among Dubreuil’s innovations was putting Louis XIII into a Baccarat crystal decanter.)

He also organized the supply chain, creating the Alliance Fine Champagne in 1966 and granting growers a stake in the business.

Then, in the 1980s, everything changed in the small, clubby world of cognac makers. In 1987, Bernard Arnault took over luxury fashion house Louis Vuitton and merged it with Moët & Chandon and Hennessy – a cognac brand – creating LVMH. Rémy Martin thought it needed more scale to compete globally with LVMH.

Faced with a well-financed competitor with global marketing and distribution, Rémy Martin responded by launching a similar global acquisition strategy. Dubreuil’s daughter Dominique Hériard Dubreuil led the repurchase of the company’s distribution rights from Seagram’s. And then the company began acquiring other brands, most importantly Mount Gay, the world’s oldest rum.

This acquisition strategy was going to require outside capital. And there was another important reason to list Rémy Martin on the stock exchange.

I mentioned that in 1948 Anne-Rémy married André Dubreuil, who eventually gained control of Rémy Martin and managed the company for almost 40 years. Well, the other 49% of the company was passed down through Anne-Rémy’s sister, Genevieve. And she married Max Cointreau, whose family made the eponymous Cointreau liquor.

Sibling rivalry: In 1980, the Cointreaus sued the Dubreuils in a dispute about Rémy Martin. To settle the dispute and to raise additional capital, in 1990, the two companies merged and, in 1991, listed their stock, which allowed disgruntled family members a way out of the deal. It also allowed Rémy Martin to raise capital (~300 million euros) to pay down debt from the Mount Gay acquisition.

Here’s the interesting part: Despite listing the shares for the public market, the Dubreuils continued to build their stake in the company.

In France, receiving dividends in shares can defer tax liabilities compared to cash, as no immediate taxable income is realized until the shares are sold. For a wealthy family, this preserves capital for reinvestment, compounding its equity stake’s value as Rémy Cointreau’s stock appreciates. The Dubreuils, through their family holding company Orpar, continue to choose shares.

This system has steadily grown the Hériard Dubreuil family’s interests since the 1991 listing. Their capital stake rose from 40% in the early 1990s to 55% to 56% by 2021. The current key family figure is Marc Hériard Dubreuil, who succeeded his sister Dominique as chairman in 2017.

Since a peak of around $24 per share in 2021, the stock (OTC: REMYY) has fallen by more than 80%. Many spirits makers have seen their shares fall because there’s a belief that more and more people are going to abstain from alcohol. And, of course, there are big fears around the impact of a global trade war on this legendary French export.

People have been enjoying fine cognac and other fine wines from France for all of recorded human history. I’ll take the “over” on people continuing to do that. I suspect that, in another decade, tariffs will have come and gone. And more people around the world will value Rémy Cointreau’s ultra-premium cognac. Meanwhile, today, Rémy Cointreau is the cheapest high-quality business I’ve ever seen in my career.

The stock is cheap, by just about any metric. It’s trading at 1.16x its book value, meaning, you’re buying the company for the value of its underlying assets. Rémy holds roughly 2 billion euro worth of inventory, against a market cap of 2.4 billion euro. That means you’re getting its earnings, its brands, its global distribution, and all its intellectual property more or less for free.

And there’s far more to these assets than most investors understand.

Under IFRS (International Financial Reporting Standards) accounting rules, Rémy values its inventory at the lower of cost or net realizable value, using the weighted-average cost method. As a result, the aging of that inventory does not revalue it upward.

A cask distilled in 1985 (possibly destined for Louis XIII) still sits on the books at its original production and storage cost. The longer it ages, the more it’s worth economically, but not accounting-wise.

Rémy doesn’t disclose the precise breakdown of its inventory by product type, so we have no way of knowing its precise composition. But the structure of the reporting offers major clues. Each year, Rémy categorizes inventory as:

- Raw materials and supplies (grapes, neutral alcohol, packaging)

- Finished goods (ready-to-ship cognac)

- And, most importantly, work-in-progress (aging eau-de-vie in barrels)

And here’s the key: work-in-progress consistently makes up more than 80% of total inventory.

To give you the most recent examples:

- FY 2024: ~82%

- FY 2023: ~81%

- FY 2022: ~82%

- FY 2021: ~83%

Rémy’s entire business model relies on slowly building an asset base of aged, ultra-premium cognac that can later be sold via its legendary brands at huge profit margins.

Since this vast stockpile is carried at cost, the gap between book value and economic value continues to widen over time. And while we can’t know exactly how much these reserves will ultimately fetch in the market, we do know that the company has exited the lower-tier (VS) portions of the market to focus only on its ultra-premium brands. So “higher” is a reasonable expectation.

I believe the current value of Rémy’s inventory is likely 5x to 10x its accounting value. That means the inventory isn’t worth 2 billion euro. It’s worth more than 10 billion euro. And could be worth as much as 20 billion euro. Meanwhile, the company’s market cap is now less than 2.5 billion euro.

And, while we wait for this value to be realized, we will be well-paid. The company is a dividend-paying machine. Over the past 20 years, the company has paid out dividends and special dividends of 1.6 billion euros. The current yield is almost 5%, but, with additional special dividends, I expect to see annual yields over the next five years of at least 10%.

Find a great business. Buy it at an attractive price. Ignore everything else.

That’s investing.

Presented by Crowdability

“Those who act now will be talking about this for years…”

Elon Musk’s next company could be his biggest success, and you can be part of it before it goes public…

It all starts by grabbing your free 4-letter ticker symbol, where you’ll learn how to gain exposure to this private company.

Click here to get your ticker symbol while this presentation is still available.

Three Things To Know Before We Go…

1. Trump’s tariff “liberation day” arrives. After months of speculation, U.S. President Donald Trump is set to officially announce the full scope of his administration’s tariffs at 4 pm ET today. Trump has said the tariffs are meant to be reciprocal, meaning they will be imposed on imports from countries that already impose tariffs and trade barriers on U.S. exports. While details are still unclear, this also suggests that tariffs could be lowered or removed if those countries were to reduce trade barriers against the U.S. Given this possibility, it’s worth noting that two countries – Israel and Vietnam – have already proactively agreed to eliminate tariffs on U.S. goods ahead of today’s announcement. In the meantime, the uncertainty over Trump’s tariff policies has sent U.S. stock markets falling – and there will likely be continued uncertainty over how tariffs, once enacted, will play out.

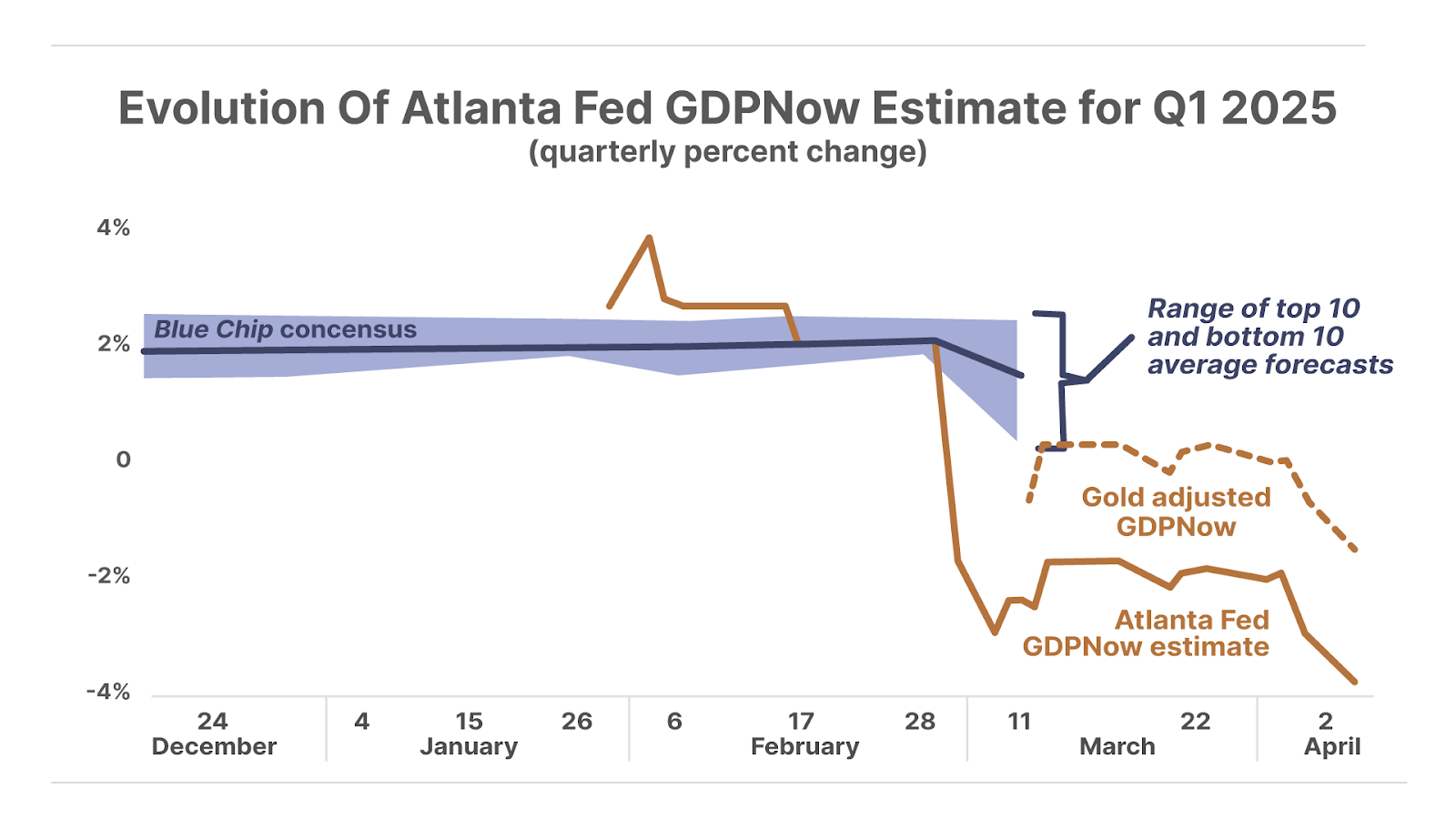

2. A huge drop in GDP expectations. The latest Q1 GDP estimate from the Federal Reserve Bank of Atlanta indicates the U.S. economy will shrink by nearly 4% in Q1, a dramatic reversal from expectations in late January of 4% growth for the quarter. Even setting aside the one-time impact from a surge in gold exports (which has pushed net exports lower, thereby lowering GDP), the Atlanta Fed sees a 1.4% decline. If these estimates play out, the U.S. economy may already be in a recession.

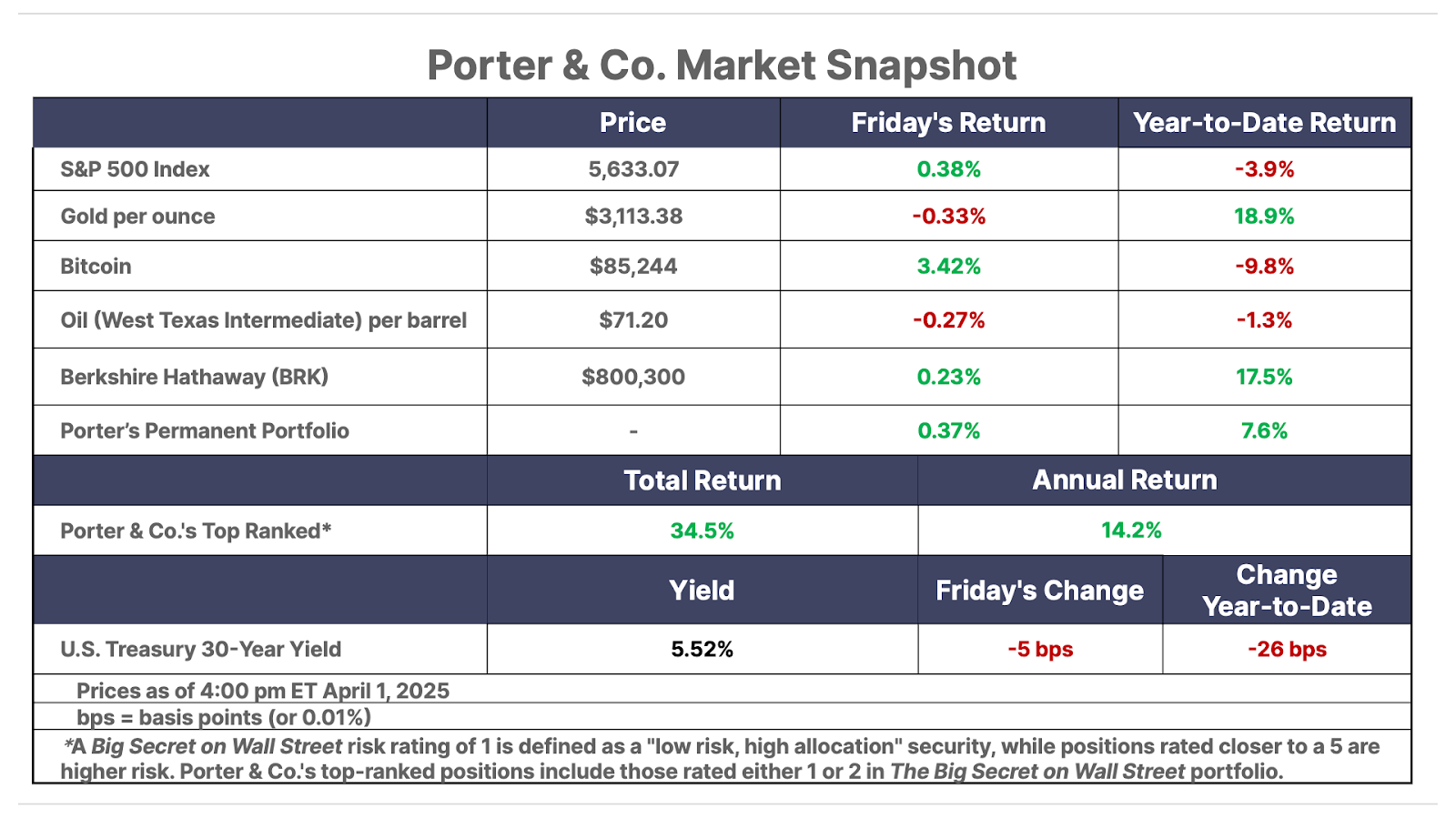

3. The Big Secret “3 Best Buys” are crushing the market. Every issue of The Big Secret On Wall Street includes our “Best Buys” – three recommendations that are currently at an attractive buy point. If you had invested in our “Best Buys” when they were released over the last two-plus years, that portion of your portfolio would be up 28% – double the 14% return if you had instead bought into the S&P 500. It’s been a steady stream of double-digit winners, with Viper Energy (VNOM) leading the pack, up 73%. The current “Best Buys” are well under their buy-up-to prices, and, our analysts believe, are poised to soar. … If you’re not already a subscriber to The Big Secret On Wall Street, click here to unlock our market-beating recommendations… or call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447, for more information on becoming a subscriber.

And one more thing… Poll Results

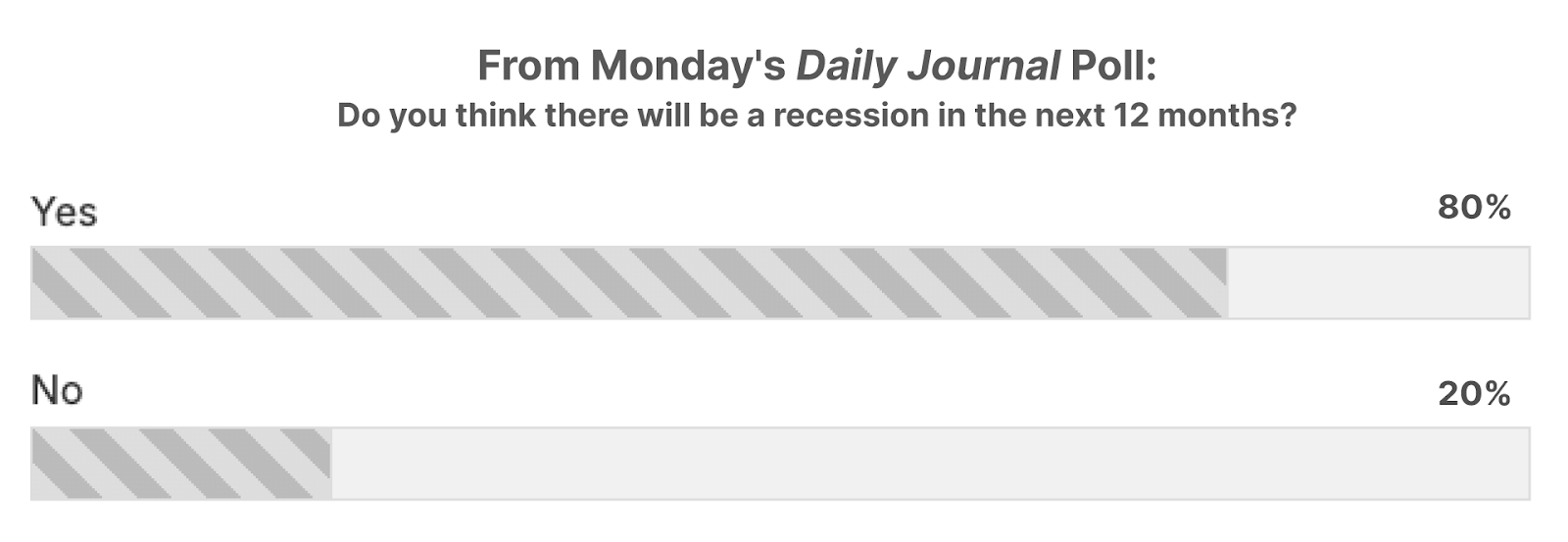

On Monday we reported that economists at Goldman Sachs raised their 12-month recession probability from 20% to 35% on higher tariff expectations and weakening consumer confidence. So we asked readers: Do you think there will be a recession in the next 12 months?… A whopping 80% of survey takers said “yes.”

As always, let me know what you think: [email protected]

Mailbag

Dear Porter,

I became one of your patients a few years ago, and so far I like my doctor.

You said that you don’t have much time for Christianity, which, to be honest, surprised me. Our Creator gave us gold and so far it has proven to be the only real money, even corrupt career politicians have not been able to corrupt it.

Satan has tried everything to duplicate and replace God. I see cryptocurrencies as fools gold and a product he invented.

Keep up the good work!

Rene B.”

Porter’s comment: Rene —

You could easily be right that Bitcoin does not end up replacing gold.

I’ve been a regular buyer of gold since 2003. And I’ve never sold a single coin.

I’ve also been a buyer of Bitcoin for about a decade.

Since I began buying Bitcoin, it has gone from around $2,000 to $60,000, a move of 30x.

Why?

Because Bitcoin is vastly better than gold.

- Bitcoin represents a well-understood proof of work and thus represents intrinsic value.

- Like gold, Bitcoin holds its value because it becomes harder to mine as computer technology improves, just as gold became harder to find after the benefits of the industrial revolution.

- It’s universally accepted. You can use Bitcoin in every major city in the world at a universal exchange value.

- It’s highly divisible – up to eight decimal places. A “Satoshi” is one hundred-millionth of a bitcoin.

- It’s highly portable. Even more than gold, a virtually unlimited amount of value can be stored on a single zip drive.

And there are two qualities that I believe make Bitcoin a far better form of money than gold.

First, unlike gold, Bitcoin cannot be seized. You can hide $100 million worth of Bitcoin in your mind by merely memorizing 20 seed words and then storing your Bitcoin anonymously in the cloud. This has profound implications for human civilizations because it will make it vastly harder for governments to plunder “enemies” or their own citizens.

And second, Bitcoin allows you to send virtually unlimited amounts of money to any individual in a peer-to-peer way that cannot be effectively policed and that is irreversible. This is a revolutionary technology that vastly increases freedom, trade, and privacy.

Thanks for you long support of my business —

Good investing,

Porter Stansberry

Stevenson, MD

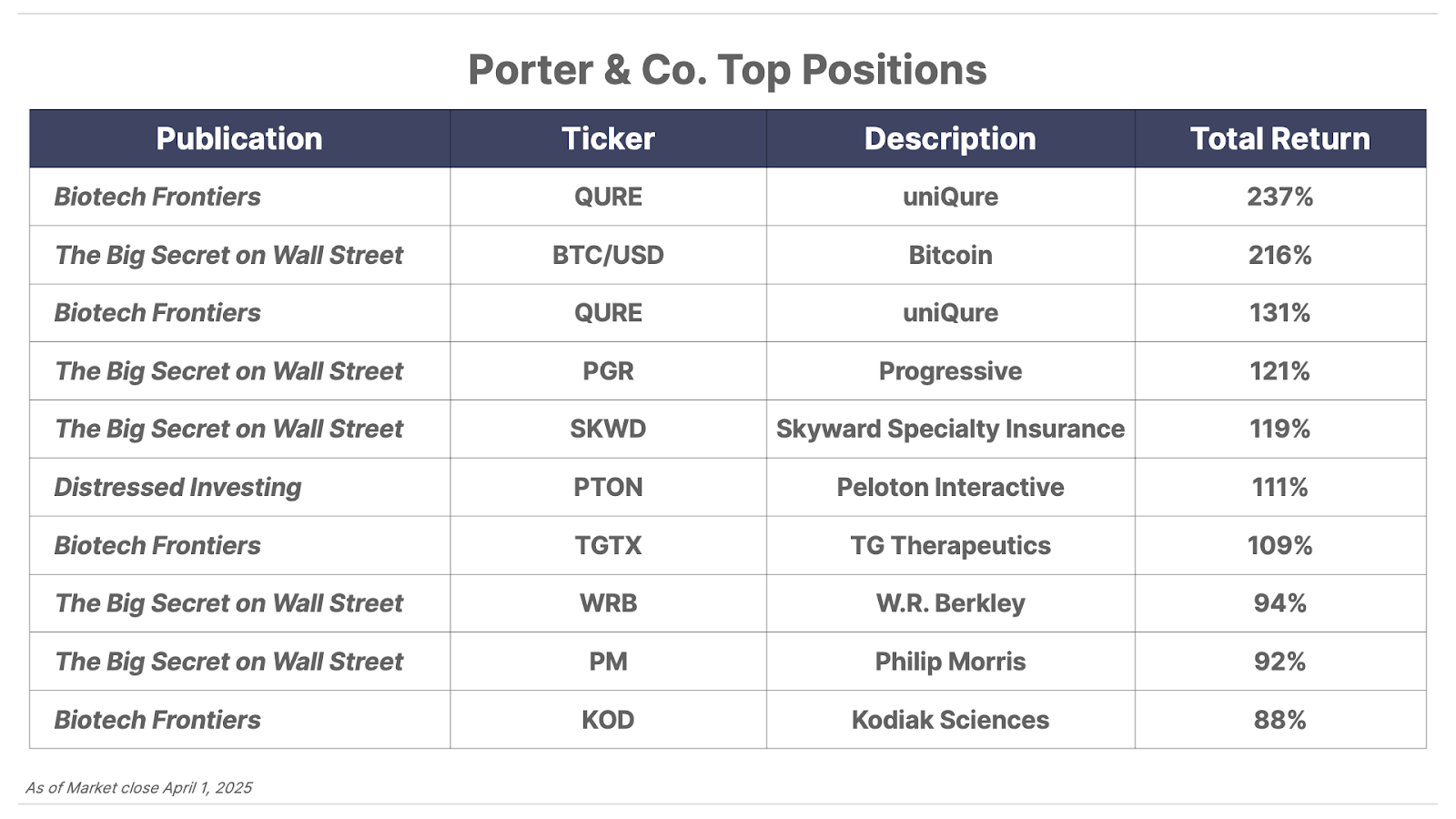

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.