Issue #72, Volume #2

A Very Personal “End Of America” Story

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| People under age 40 can’t afford middle-class life… Student loans, sky-high mortgage payments, credit card debt… This poor fella is going to have to declare bankruptcy… Ahh, but there’s a twist… Is there dissent at the Fed? |

The American dream is dying.

We’ve built an economy and a financial system that’s made a normal, middle-class life impossible for most people under the age of 40.

If you have children or grandchildren in this age group, I bet you already know what I’m talking about. I didn’t understand it – until I got this letter from a struggling 35-year-old father of two.

Please make sure you read to the end. There’s a twist… A big twist. And it definitely matters to you.

Here are the facts:

The man is currently earning $51,000 a year in wages and overtime after taxes. (He works in IT customer service with a good company.) And while that might not seem like a lot of money to some of you with high incomes, his take-home pay is almost 30% higher than U.S. median income. Even so, he can’t come close to affording his annual spending, which over the last 12 months was $71,000.

Why is he spending so much? He has a special needs child who requires specialized care. His wife can’t work because she’s the primary care giver. Obviously, he’s in quite a bind.

But that’s not the real problem…

Like a lot of younger Americans, he and his wife spent way too much money on education at a very expensive, private college. He got a degree in art history and, while in college, spent two years studying art in Europe. They have $200,000 in student loans and $170,000 in credit card debt, which grows every month.

He’s done everything possible to minimize interest payments for the last eight years – shifting the balances from credit card to credit card, etc. So over the last year, he’s only spent about $10,000 on interest. But he knows with Joe Biden gone from the White House, they must start making payments on the student loans again. Plus, with inflation rising, the credit card companies have stopped offering teaser rates. He thinks he’s going to have to spend at least $15,000 on interest this year… or maybe even $20,000. That will eat up at least 25% of his income.

I know what you’re thinking – this poor fella is going to have to declare bankruptcy.

But, he can’t – not if he wants to be able to keep his child out of a state-run institution, which would be a death sentence for his child. Plus, if he defaults on any of these debts, he’ll lose his house.

Right after COVID hit he was desperate to get out of his apartment complex and into some place safe for his wife and their new baby. He didn’t have any money, but, through a charity, he was able to get a “payment in kind” (“PIK”) mortgage.

This PIK mortgage is great for new homebuyers because it doesn’t require any down payment and, for up to five years, you can defer all interest payments, which simply get added onto the loan. The one problem with these mortgages is a cross-default clause, which means, if he defaults on any of his other debts, his mortgage is due in full in 90 days.

He’s been living in the house but hasn’t made a single payment on the mortgage. The balance has grown to over $1 million.

He knows when the PIK grace period ends (in 2028), he’s going to default. There’s no way he can possibly afford the mortgage.

Why not just sell the house? Well, because he needs a place to live and, even worse, he bought in a hot market (Austin, Texas) where prices have now fallen 20% to 30%. After not making payments for years, and with falling housing prices, they owe far more than the house is worth.

So he’s trapped. And he’s about to be obliterated, financially.

What should he do? His strategy has been to buy as much Bitcoin as he can and hope for the best.

Well, not really.

You see, this story isn’t about an individual person. This is the story of all of us.

This is the story of the U.S. government and our national debt.

The man’s income – $51,0000 – represents the $5.1 trillion that our government collects in taxes and tariffs each year. And the $71,0000 in spending represents the $7.1 trillion our government actually spends. Why does our government spend so much? It’s not because of the stuff DOGE promised to cut. It’s because it has to spend $3 trillion to support the country’s “special needs child” – the huge, and growing population of Americans who qualify for Social Security and Medicare.

Why don’t we just raise taxes? Because our “wife” can’t work. The government is already collecting almost 20% of GDP in taxes. It does so in an extremely progressive way, such that the wealthiest 10% of Americans pay for almost half of all income taxes. Nobody votes to raise taxes on themselves. They vote to raise taxes on the other guy. And, in any case, raising tax rates further will most likely result in less revenue, as more taxpayers will simply choose not to work or will find ways to avoid paying. (There’s plenty of evidence that shows, no matter what tax regime is in place, governments can’t collect more than about 20% of GDP in taxes without seriously impacting economic growth.)

And, much like credit card teaser rates and Biden’s long pause in collecting student loans, our government’s ability to avoid paying meaningful rates of interest on its outstanding $37 trillion in debt (what I represented as $370,000 in student loans and credit card debt) has come to an end. More of our foreign creditors and trading partners and selling our bonds and buying gold instead. In 2024, central banks bought another 1,044.6 tons of gold. That was their third consecutive year of purchases exceeding 1,000 tons.

Our country’s current deficit ($2 trillion) is represented here by the family’s $20,000 in overspending, equal to almost 40% of our government’s income.

We aren’t having a one-time funding gap: we have an entire financial model that’s completely broken.

And that PIK mortgage I described?

That’s exactly the real-life situation with our looming Social Security and Medicare unfunded liabilities. They now total over $100 trillion!

People believe, falsely, that these promises are funded in some way, that the money they’ve paid into the system over the years belongs to them and will be there for them. That’s all nonsense. The money was never invested. And you don’t own the rights to anything. If you doubt that, look up Flemming v. Nestor (1960). The Supreme Court explained it very simply: Social Security payments are taxes. Nothing more.

What the system “owns” are the bonds of our bankrupt government. And those promises will start coming due before 2030. There’s zero chance we can live up to these promises.

What do bankrupt governments do?

They inflate.

And they start wars.

Plan accordingly.

Jim Rickards: “One Executive Order Changes My Entire ‘Birthright’ Thesis…”

In his original “Birthright” presentation, Jim Rickards conservatively projected this $150 trillion mineral boom to transpire over four years… But Trump has just completely accelerated this timeline. What happens next will shock most Americans. Jim just recorded an urgent interview with all the new details.

Watch his full analysis of The American Birthright: Phase II HERE.

Three Things To Know Before We Go…

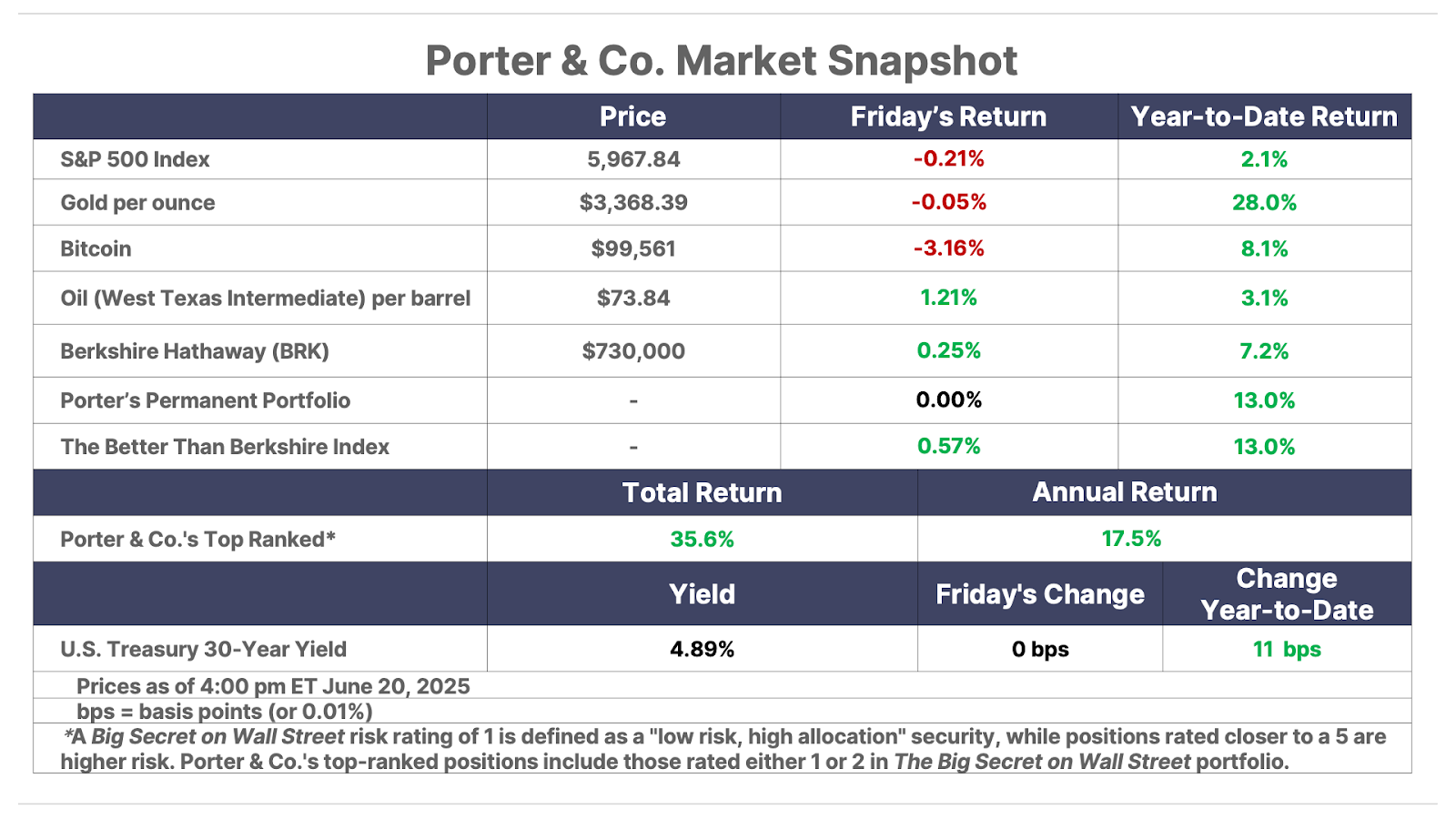

1. Markets shrug off Iran strike. The U.S. joined Israel in its bombing campaign on Iran over the weekend, including dropping seven B-2 bombers that released 14 30,000-pound GBU-57 “bunker buster” bombs on three Iranian nuclear sites. President Trump called for “peace” and encouraged the Iranians to come back to the negotiating table following the strikes. Markets breathed a sigh of relief that the situation appears contained, even after news broke that Iran launched missiles at U.S. military bases in Qatar this afternoon. After jumping as high as 5% on Sunday night, oil prices retreated and were trading in the red by this morning. Meanwhile, stock indexes in the U.S. and Israel moved higher.

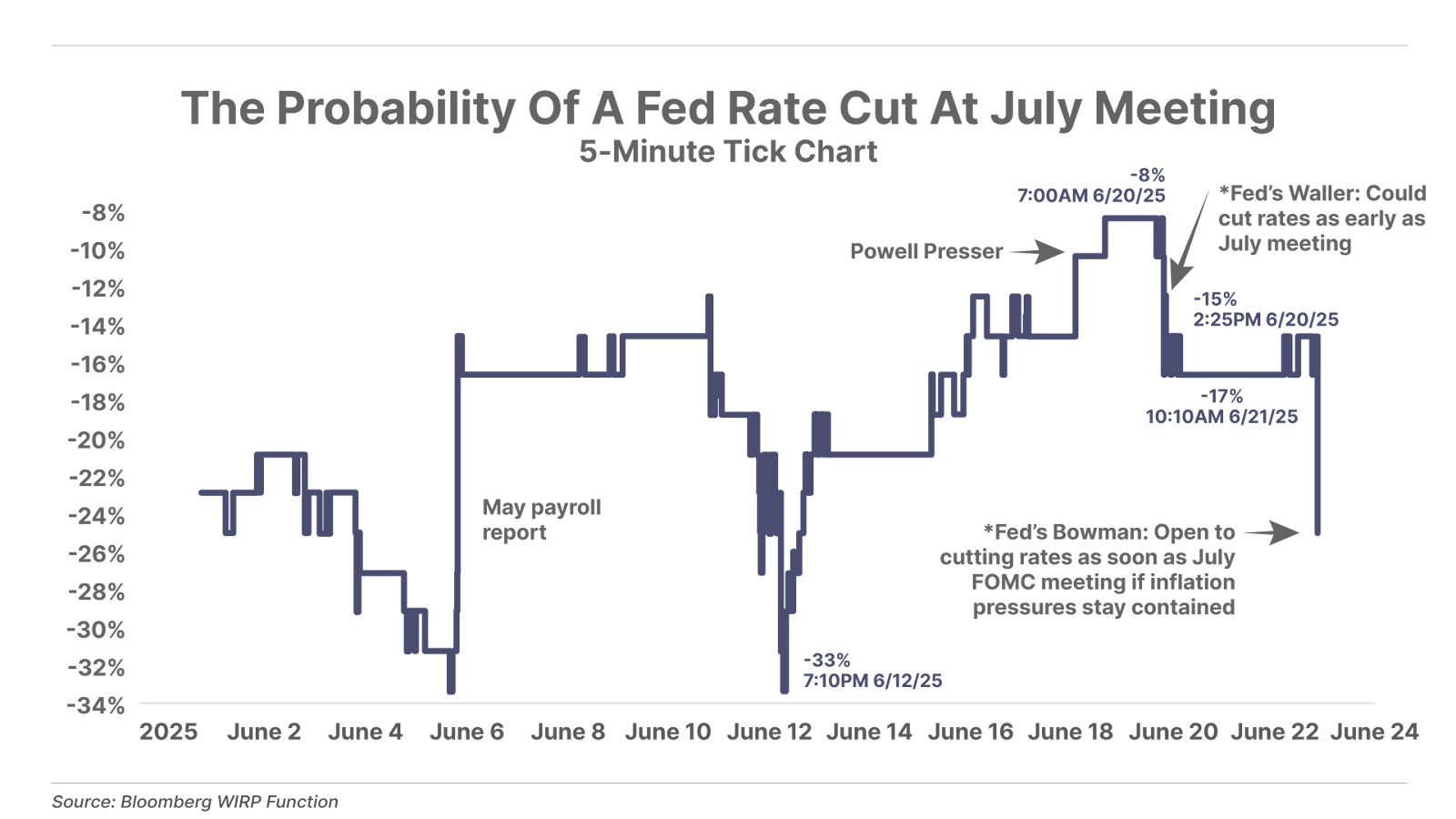

2. Is there dissent at the Fed? During his post-meeting press conference last week, Federal Reserve Chair Jerome Powell reiterated that the central bank is in no hurry to cut interest rates despite growing pressure from President Donald Trump. However, over the past couple days, two Fed governors – both appointed by Trump during his first term – have spoken out in favor of cuts as soon as next month. On Friday, Governor Christopher Waller said he believes the Fed should “look through” one-time tariff-related price increases and cut rates in July. This morning, Governor Michelle Bowman agreed, saying she believes the Fed should cut rates when it meets next month so long as incoming data continue to show inflation remains “contained.” Following these comments, the market-implied probability of a July rate cut has moved from just 8% to 25%.

3. Stablecoins reach Main Street banks. Fiserv announced it will now support stablecoins – digital assets designed as a means of payment. Fiserv is partnering with payment tech companies Paxos and Circle Internet (CRCL) to launch its own stablecoin, FIUSD, enabling banks and developers to build stablecoin-based applications. One of the largest payment processors, handling $90 billion in annual transactions across 10,000 financial institutions, Fiverv’s move could mark a major shift – accelerating the mainstream adoption of digital dollars.

And One More Thing… Today’s Poll

With stablecoins becoming increasingly mainstream, possibly being offered by banks across the country, we asked in today’s poll:

Tell me what you think, good, bad, or somewhere in between:

[email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland

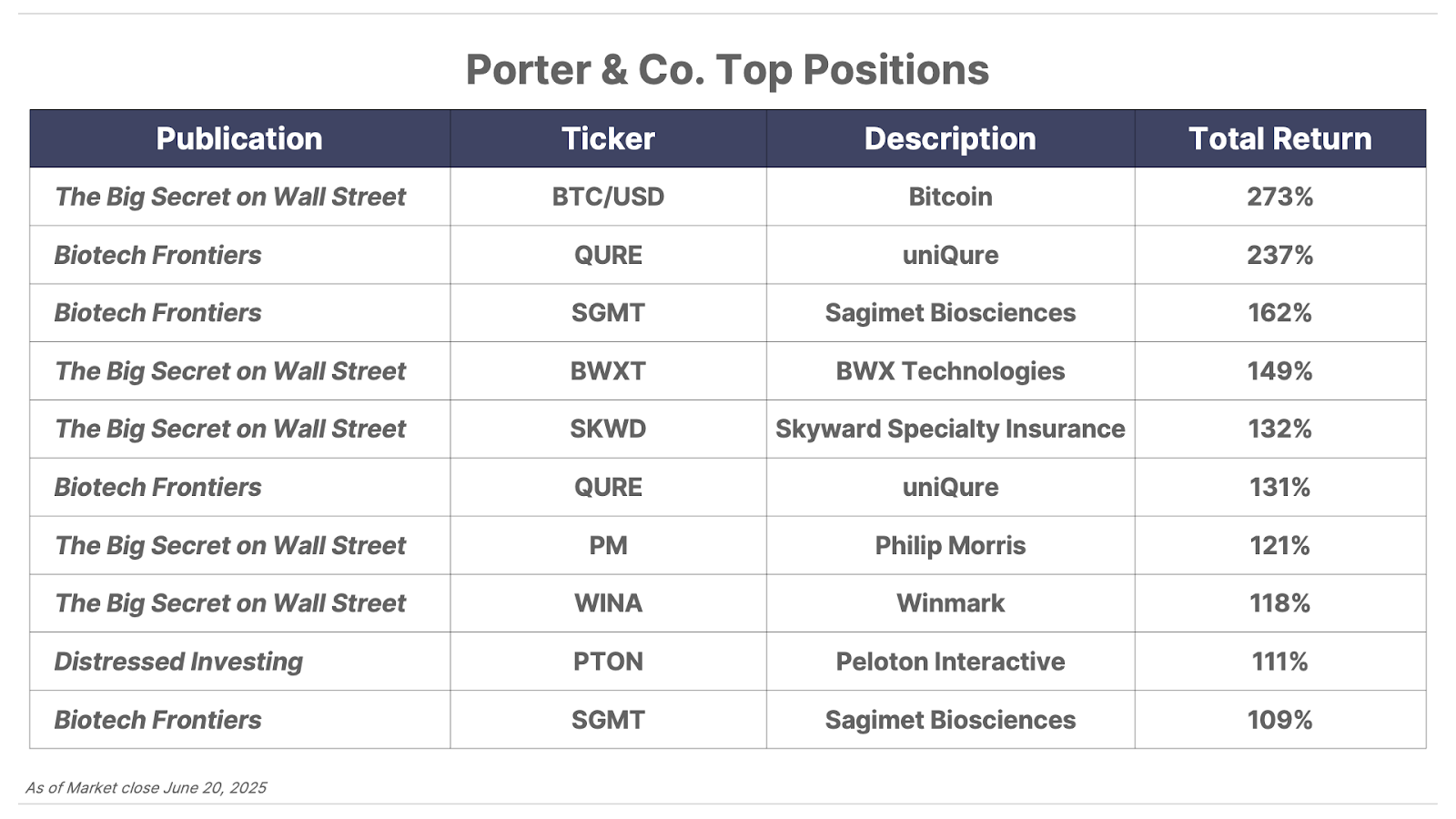

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.