Trillions spent on “renewable” energy sources like wind and solar have failed to make a dent on fossil fuel consumption. And the lack of investment in fossil fuels is creating energy shortages around the world… unleashing a cash flow windfall for one of the world’s most hated commodity producers.

Clean Energy Is A Scam

Coal Rushes Into The “Green Vacuum”

Welcome to Porter & Co.! If you’re new here, thank you for joining us… and we look forward to getting to know you better. You can email your personal concierge, Lance, at this address, with any questions you might have about your subscription… The Big Secret on Wall Street… how to navigate our website… or anything else. You can also email our “Mailbag” address at any time: [email protected].

At the end of this issue, you’ll find our model portfolio, watchlist (which is also here), and Mailbag — as well as a “Best Buys” section, where we’ll briefly cover three portfolio names that we think you should consider buying first.

In addition to hosting The Big Secret on our website, it is also available as a downloadable PDF. Click here to download the full report.

Again… we’re excited that you’re with us…and we’re looking forward to a long and fulfilling relationship.

If you’re not a member and would like to learn more, click here.

The truck driver didn’t know he was being watched.

But as he swerved his large, unmarked vehicle out of the forest and back onto the main road, a hidden camera flashed once, and then again, under the brooding December sky.

Staying a prudent distance behind, the photographer’s smaller vehicle tailed the truck for the next 30 miles. Eventually, the truck driver reached his final destination – a dilapidated plant with rust-marked smokestacks, on the outskirts of Ahoskie, a sleepy railroad town of 5,000 in northeastern North Carolina.

The whistleblower snapped one last photo as the truck, and its cargo, entered the factory gates. The whole journey was officially logged on film.

Enviva had been caught red-handed.

A (supposedly) ESG-friendly “biomass” company, Enviva Inc. (NYSE: EVA) trumpeted on its website, “Displace Coal. Grow More Trees. Fight Climate Change”. Meanwhile – and now documented on camera – it was secretly cutting down huge swaths of native forest to generate “zero-emission” fuel.

That wasn’t the story Enviva was telling the public in late 2021.

The company claimed it picked up scrap wood, loose limbs, and other “wood waste” that would otherwise rot on the forest floor… and that it then recycled those bits and pieces into eco-friendly wood pellet fuel.

According to a former Enviva employee – quoted anonymously on conservation news site Mongabay – “The company says that we use mostly waste like branches, treetops and debris to make pellets. What a joke. We use 100% whole trees in our pellets. We hardly use any waste. Pellet density is critical. You get that from whole trees, not junk.”

Enviva acknowledged on its own website that “if old forests were to be cut down specifically for biomass … biomass powered electricity would have higher … emissions than coal in most cases due to its lower combustion efficiency.”

In other words, the company knew it was doing more harm than good. And – as long as it made money – it didn’t care. It was textbook greenwashing.

The term “greenwashing” – fudging sustainability practices in order to turn an extra profit – was coined in the 1980s by environmentalist Jay Westerveld, after he visited a hotel that instructed guests to reuse towels “for the planet” – while at the same time it was building a suite of new bungalows that disrupted the native ecosystem. Greenwashing, in other words, is environmental hypocrisy.

And activist short seller Blue Orca has a keen eye for hypocrisy.

Blue Orca has a history of taking holier-than-thou companies down a peg or two, including hydrogen fuel-powered vehicle maker Hyzon Motors, whose main customers turned out to be fake shell companies… and luggage manufacturer Samsonite, whose CEO resigned after Blue Orca revealed he’d lied about having a doctorate in business administration.

Enviva was the next company in Blue Orca’s crosshairs.

As part of its due diligence on Enviva, Blue Orca partnered with an environmental watchdog in North Carolina to obtain damning footage: mature trees cut down, tossed into the woodchipper, and transported to the Ahoskie pellet factory in unmarked trucks. But that was just the beginning.

Blue Orca also uncovered a cache of detailed GPS data showing “before and after” forests that Enviva had completely denuded. And it interviewed a former executive who claimed the company was routinely harvesting 70-90% of the trees from various wooded areas. (The razed forests weren’t replanted, either. The land either sat vacant or was sold to housing developers.)

But the biggest lie of all had nothing to do with replanting… or the type of wood Enviva harvested… or even with the company’s shady “non-GAAP” accounting practices.

It was that the whole “biomass” industry was a giant scam.

As Blue Orca explained:

Enviva’s business model is an ESG farce built on a carbon accounting loophole. At a high level, Enviva harvests wood and other biomass from forests in the Southeastern United States for conversion into wood pellets at Enviva’s manufacturing facilities. These pellets are then shipped mainly to Europe, where European power producers burn the wood to produce electricity.

International climate treaties include a grandfathered provision of the Kyoto protocol classifying the burning of forest biomass as a “renewable” energy source under limited circumstances, and this controversial loophole has allowed a burgeoning industry of deforesting biomass to masquerade as a zero-emission energy source. Countries, principally in Europe and Asia, have taken advantage of this loophole, burning wood instead of coal to meet emissions targets.

These countries dole out subsidies in the form of carbon credits for switching to wood burning, even though wood pellets emit more CO2 per unit of heat generated than any other widely used fuel source, including coal.

“Biomass” had nothing to do with clean energy. It was essentially a scheme designed to funnel cash to Europe, while creating what financial commentator Doomberg calls an “orgy of deforestation” in America.

Vox puts it bluntly:

Since Blue Orca published its short report on Enviva in October 2022, the company’s shares have tumbled by over 80% and the UK’s biomass subsidies have come under attack from political leaders, including Tory parliament member Pauline Latham.

In February 2023, Latham criticized her own party for supporting the UK’s biomass subsidies, noting that the UK “pays significant sums in renewable energy subsidies to bioenergy companies making sizeable profits, despite it releasing huge amounts of greenhouse gasses and harming forests’ ability to absorb carbon.”

The UK’s biomass subsidies that put taxpayer money into wide-scale deforestation to produce an energy source more polluting than coal – all under the guise of promoting “clean” and “renewable” energy – is just one of a long list of failures of the climate crusaders.

Despite trillions spent globally on various “renewable” energy investments and tax incentives, alternative energy sources like wind and solar have failed to make a dent on fossil fuel consumption.

According to Goldman Sachs commodities analyst Jeff Currie, over the last decade, a staggering $3.8 trillion has been invested into renewable energy sources….

During that same ten years, guess how much the percent of global energy consumption from fossil fuels fell?

Exactly 1%. From 82%… all the way down to 81%.

Making matters worse, governments around the world – and especially in Europe – are purposely blocking the development of fossil fuel energy sources, despite the failure of alternative energy sources to take up the slack in powering the global economy.

This has set the stage for big distortions in the energy market, including last year’s global gas shortage, which sent prices for natural gas and liquefied natural gas (LNG) to new record highs around the globe.

And it’s creating tremendous opportunities for investors to profit from the repeated failure of modern energy policy… like the one we’re about to explore in today’s issue.

The Horror of the Void

As Aristotle explained, nature abhors a vacuum. Create a void, and some type of matter will inevitably rush in to fill it. The Latin term is “horror vacui,” or “horror of the void.”

Over the past decade, European countries have limited fossil fuel production and exploration in order to curb carbon dioxide emissions. That’s kneecapped the fossil fuel industry in Europe – and left a gaping “energy vacuum” that needs to be filled.

But renewables – once hailed as a shining green savior – aren’t doing the trick.

Europe’s “horror of the void” tale began in 2011, when enlightened France imposed a nationwide fracking ban…

Europe’s woke energy czars especially hate hydraulic fracturing (fracking), a controversial oil extraction technique that forcibly breaks up the earth‘s crust to obtain fossil fuels. (In the U.S., fracking produces 9 million barrels of oil and 80 billion cubic feet of natural gas each day, generating over $300 billion annually.)

Other countries soon followed France’s lead, and by 2019, virtually every major economy across Europe had outlawed fracking. These politically-motivated fatwas left the continent’s massive shale gas reserves (an estimated 14 trillion cubic meters of shale gas throughout Europe) completely untapped.

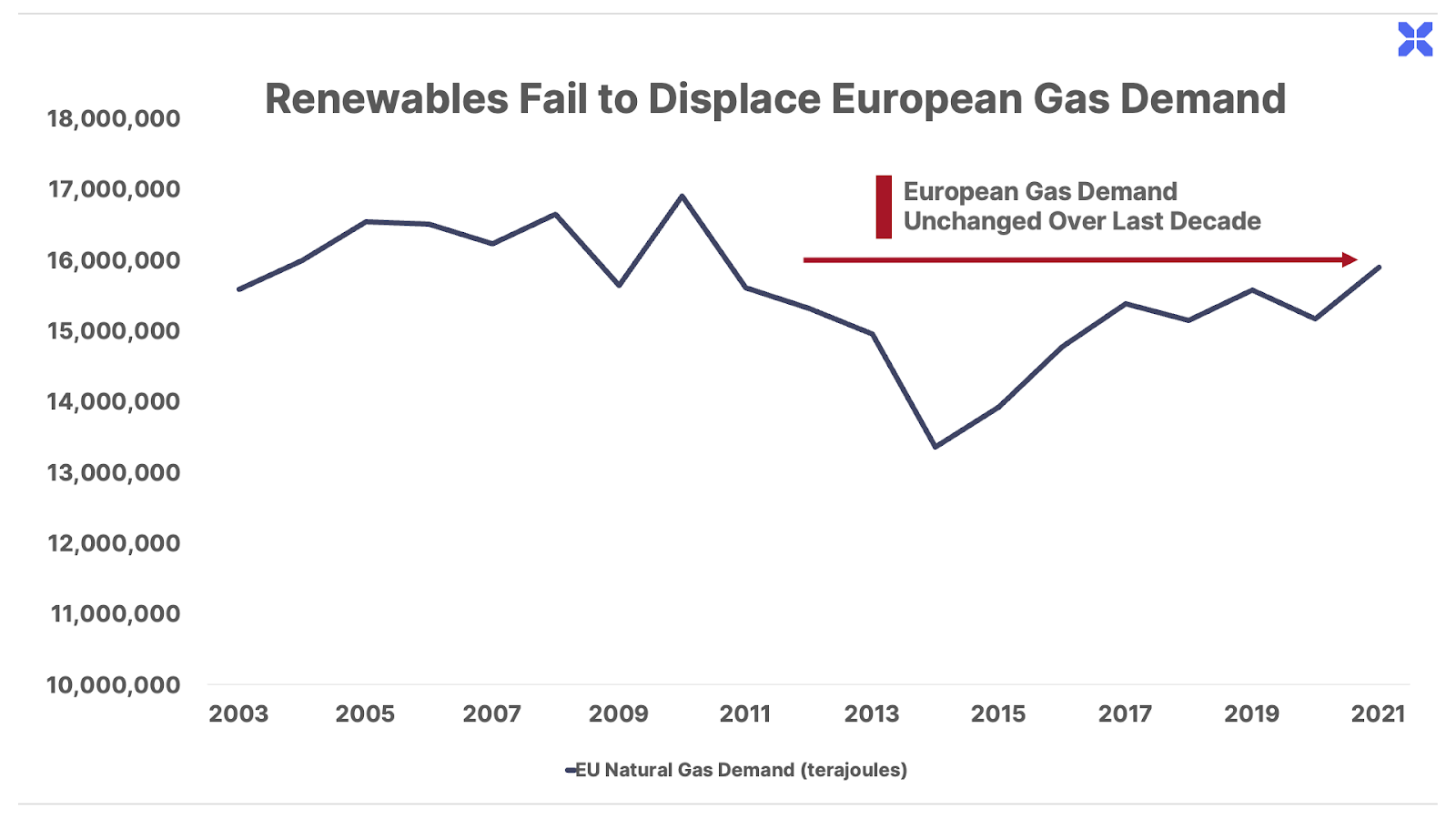

Instead, Europe poured three-quarters of a trillion dollars into renewable energy investments, plus untold billions more in tax breaks and government subsidies over the last decade.

Despite this flood of money aimed at replacing natural gas-powered electricity with alternatives like wind and solar, Europeans obstinately continued to use exactly the same amount of gas:

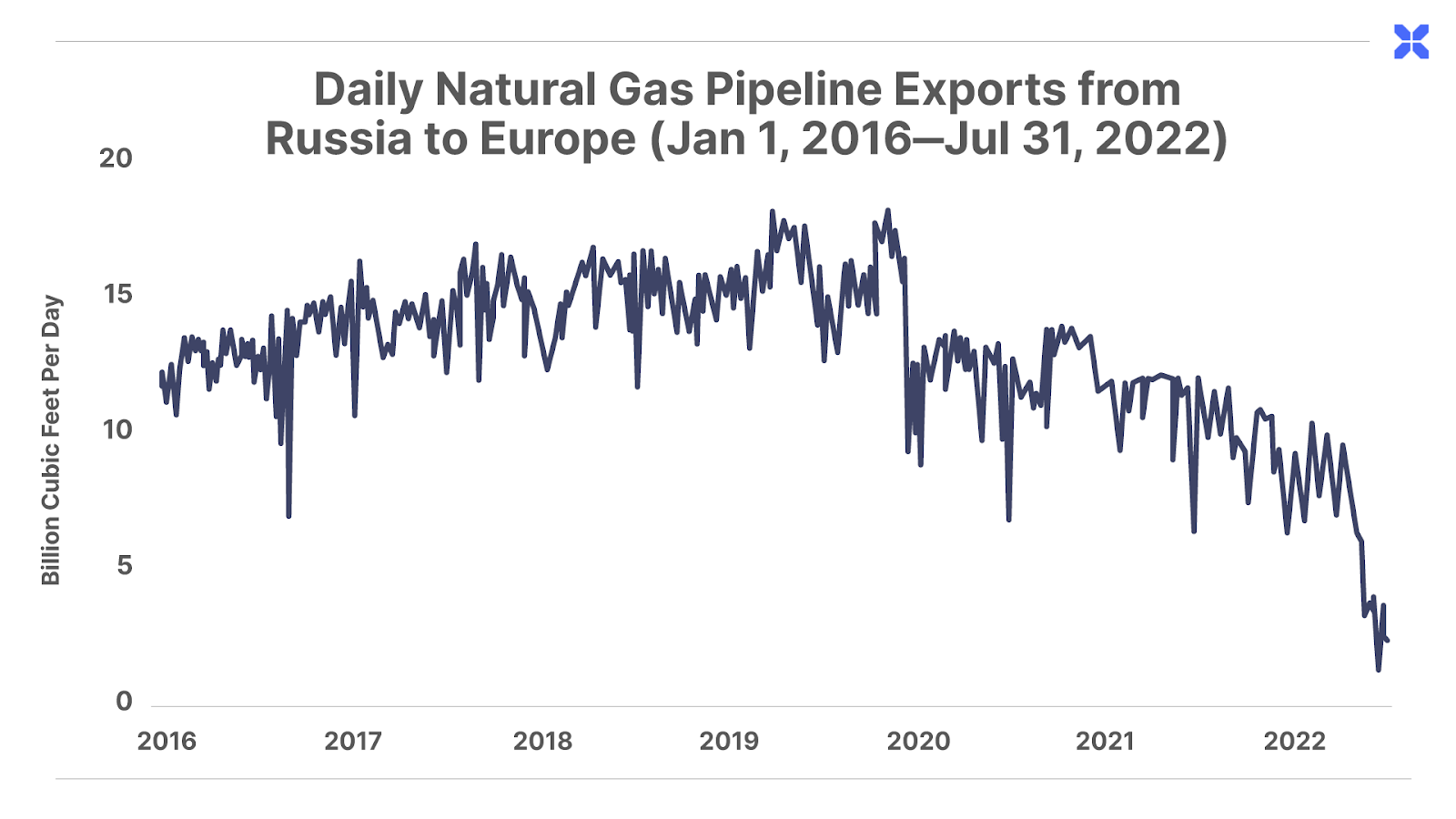

Since Europe had failed to invest in its own gas supply, it turned to foreign imports to keep the lights and heat on. By 2021, 83% of European gas was sourced from foreign suppliers, with Russia accounting for 45% of European gas imports.

Russia filled the energy void until it didn’t.

As has become clear, it’s not a great idea to place the future of your nation in the hands of Vladimir Putin.

On February 24, 2022, Russia invaded Ukraine, and the diplomatic fallout was immediate. Europe, along with its western allies, including the U.S., imposed a series of financial sanctions against Russia, including restricting imports of Russian oil and gas. The end result: Russian natural gas imports into the EU and the United Kingdom dropped by 50% in 2022 versus the prior five-year average:

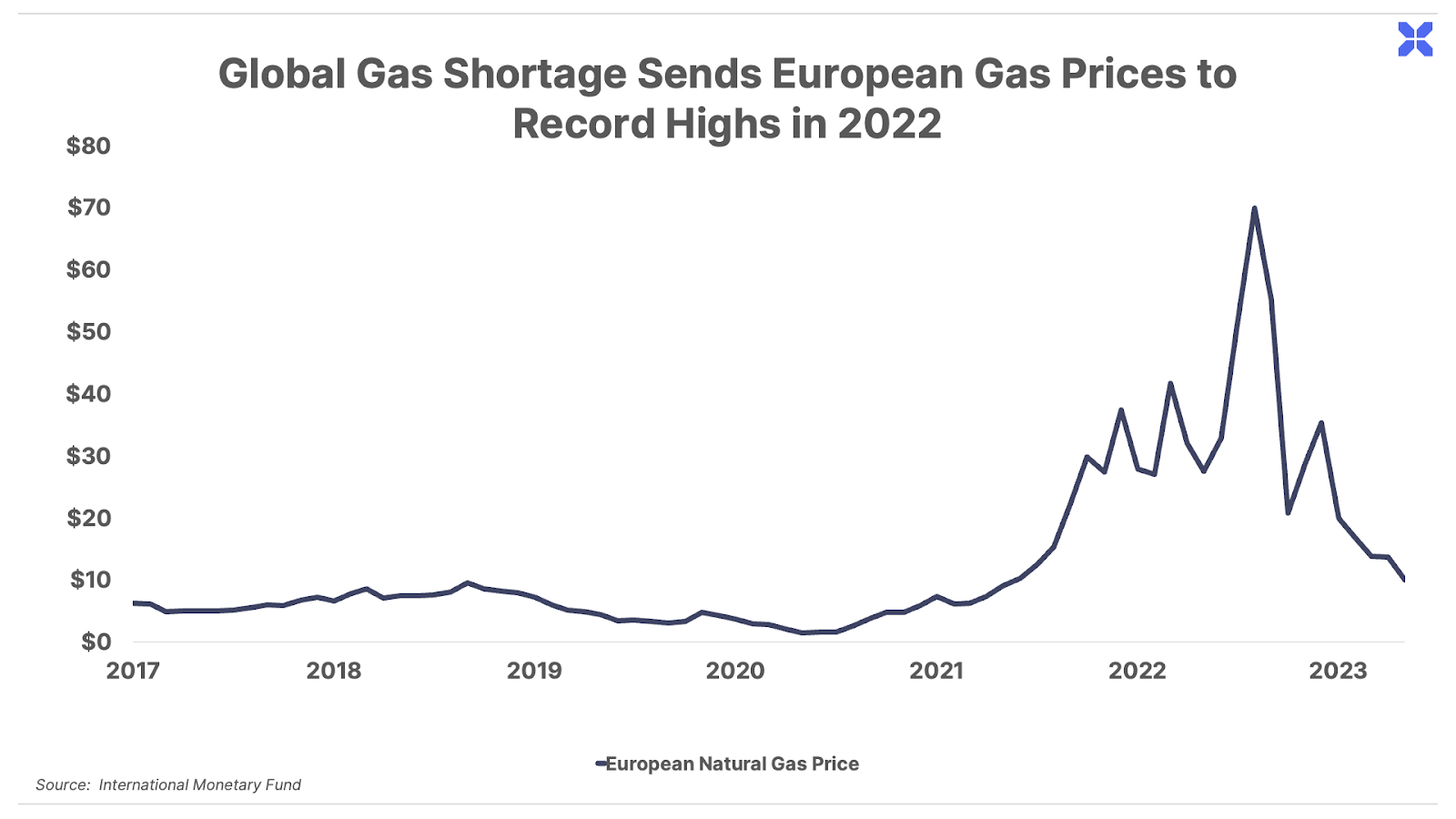

Europe scrambled to replace lost Russian gas supply with imports of liquefied natural gas (LNG), which surged 58% in 2022, including a record volume of LNG imports from the U.S.

Going into 2022, the LNG market was already under strain from booming demand as the global economy emerged from COVID-19 lockdowns. Prices for Asian LNG had already shot up six-fold to new record highs in 2021, with strong global economic activity amplified by a colder-than-expected winter.

So when Russian supplies dried up in 2022, Europe was caught in a bidding war to attract LNG cargoes in the already-tight market… sending European natural gas prices skyrocketing from less than $10 per million British thermal units (MMBtu) in 2021 to a high of $70 per MMBtu by late last year.

Fortunately for Europe, LNG prices plummeted last winter as Mother Nature delivered a “get out of jail free” card, thanks to one of the warmest winters on record. Gas prices fell back to Earth, creating a temporary sense of calm among European policymakers. But the global gas shortage has merely been postponed, not resolved.

Even before the 2022 disruption in Russian gas supplies into Europe, a shortage was emerging in the global gas market and prices had already begun moving to new highs. In early 2021, energy research firm S&P Global Platts forecast that LNG demand would exceed supply through at least 2025, as demand for LNG was growing faster than the rate of construction of LNG export terminals.

Now, Europe has to replace a record amount of missing Russian gas, which will only intensify that demand in the years ahead.

Exxon Mobil CEO Darren Woods recently emphasized at a Wall Street Journal CEO Council Summit that the global LNG market will remain undersupplied through at least 2026:

“You look around the world, and the balance is, the world will be short [of liquefied natural gas] probably through 2026… That’s how we’re seeing that balance play out – it just takes time to bring these very large, capital-intensive projects on stream.”

Europe replacing Russian gas with LNG represents one of the largest re-shuffling of global energy flows in history, and it will have major implications on energy prices for years to come.

We’ve written about some of the biggest winners from this trend, including one of the largest natural gas producers in the world with an unmatched footprint in the heart of America’s most prolific shale gas basin, managed by the Gods of Gas. We’ve also recommended a natural gas royalty company as a capital-efficient way to play the coming supercycle in natural gas prices.

But this same trend has also created an opportunity in a much less appreciated commodity that virtually no one on Wall Street wants to own…

Global Gas Shortage Makes Coal Great Again

Coal and natural gas compete for the cheapest sources of baseload power generation around the globe. But coal is less environmentally friendly: It generates about twice the amount of carbon dioxide emissions as natural gas to release the same amount of energy.

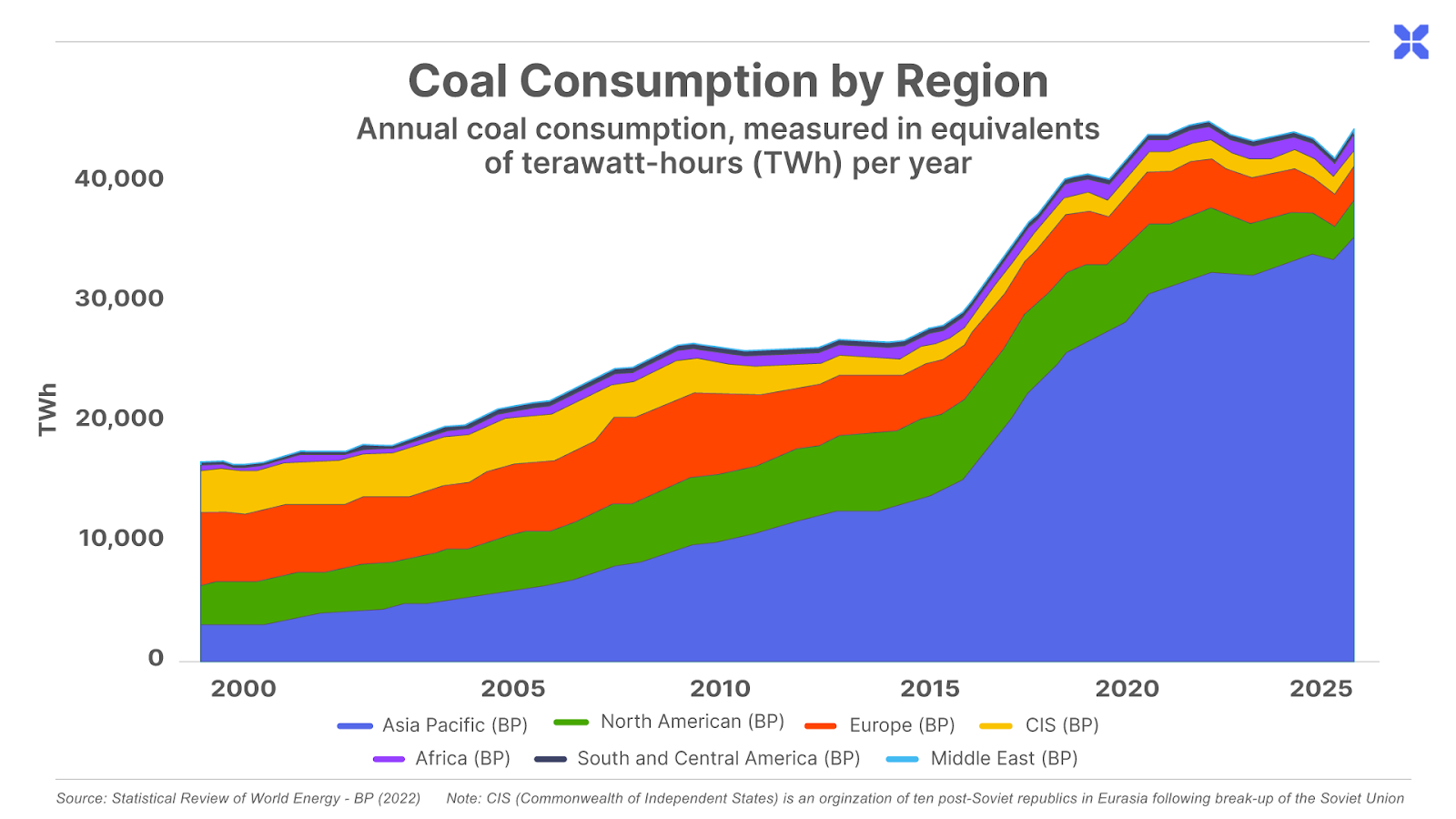

That’s why countries around the world have over the past decade been transitioning their electric grids from coal to gas. After growing by 40% from 2004 – 2013, global coal consumption peaked and flatlined from 2013 – 2019. The global shift from coal to gas was made possible by the rise of the global LNG trade, which, in turn, was fueled by cheap U.S. shale gas unleashing low-cost LNG exports around the world.

But last year, as Europe added massive new buying pressure onto an already-tight LNG market, there simply wasn’t enough LNG to go around – particularly for developing countries like Pakistan and Bangladesh.

Bangladesh relies on gas for two-thirds of its power generation. The country couldn’t outbid Europe for the increasingly scarce LNG cargoes last year, causing its LNG imports to drop by 14% in 2022. This caused widespread power outages, including electricity blackouts in nearly every day of the third quarter of 2022, when the global gas shortage reached its peak leading into the winter.

Bangladesh was forced to shutter 22 of its gas-fired power plants, or about 15% of its gas-fired power capacity, in response to surging LNG prices last year. After years of building out its natural gas-based power capacity, the country is now doing a u-turn back to coal. Bangladesh announced plans to add 4.4 MW of coal-fired power plants last year, which will more than double coal’s share in its power grid from 8% to 17% of electricity generation.

Pakistan also couldn’t compete with Europe’s bids on LNG cargoes, forcing the country to slash its LNG imports by 17% in 2022 to a five-year low.

Left without gas, Pakistan went back to coal. In February, Pakistan announced new investments to boost its coal-fired power generation up to 10 gigawatts (GW), nearly 5-fold increase from 2.3 GW currently. The country’s energy minister said in a Reuters interview that “LNG is no longer part of the long-term plan.”

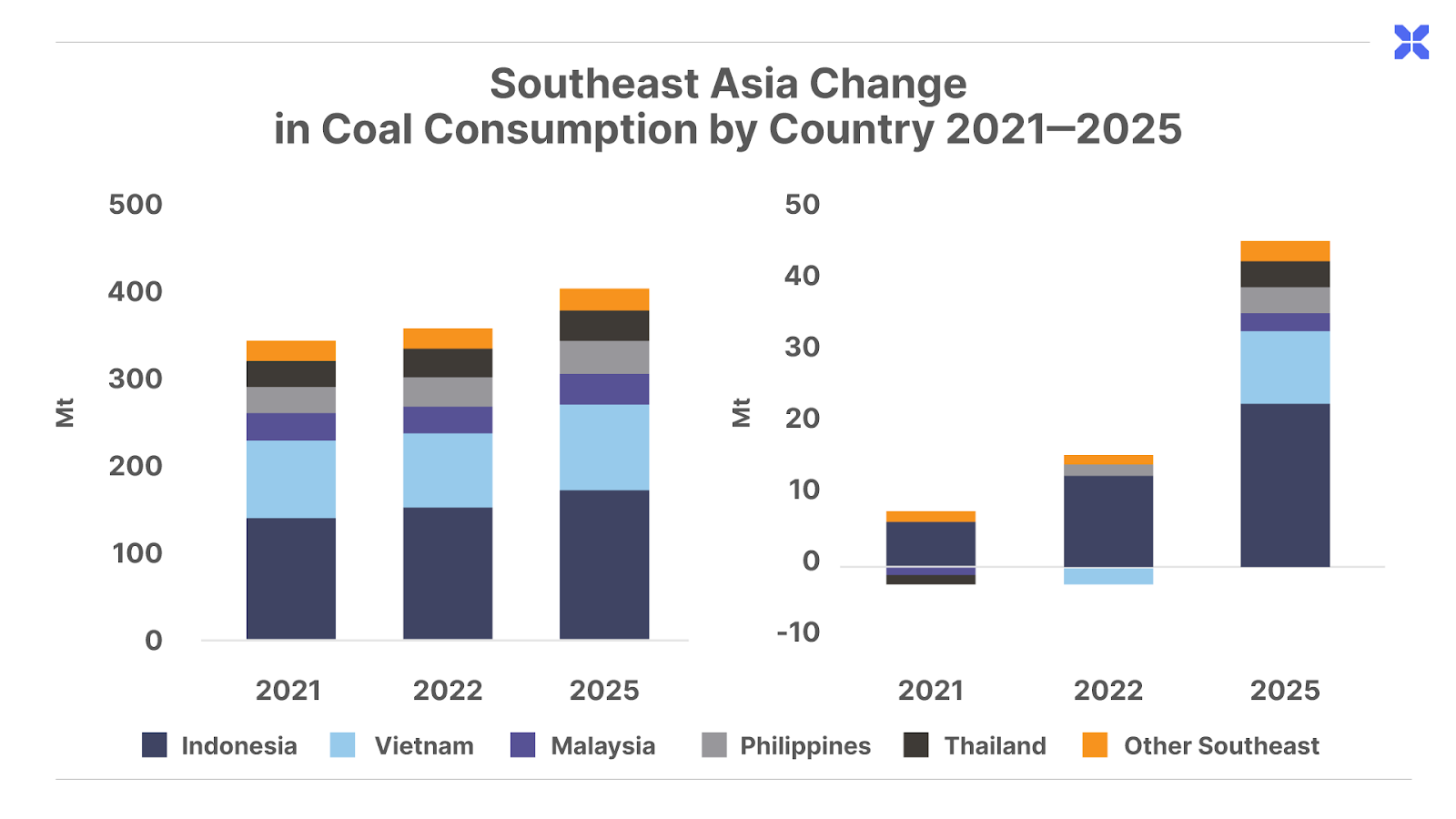

Developing economies across southeast Asia also boosted their coal consumption last year, led by 9% growth in Indonesia’s coal consumption and 6% in the Philippines. Last November, Vietnam updated its long-term energy consumption targets that called for growth in the country’s coal consumption through 2030 – reversing a previous plan to cut coal consumption by 2030.

In total, growth in coal consumption across southeast Asia is expected to grow by 4% per year through 2025:

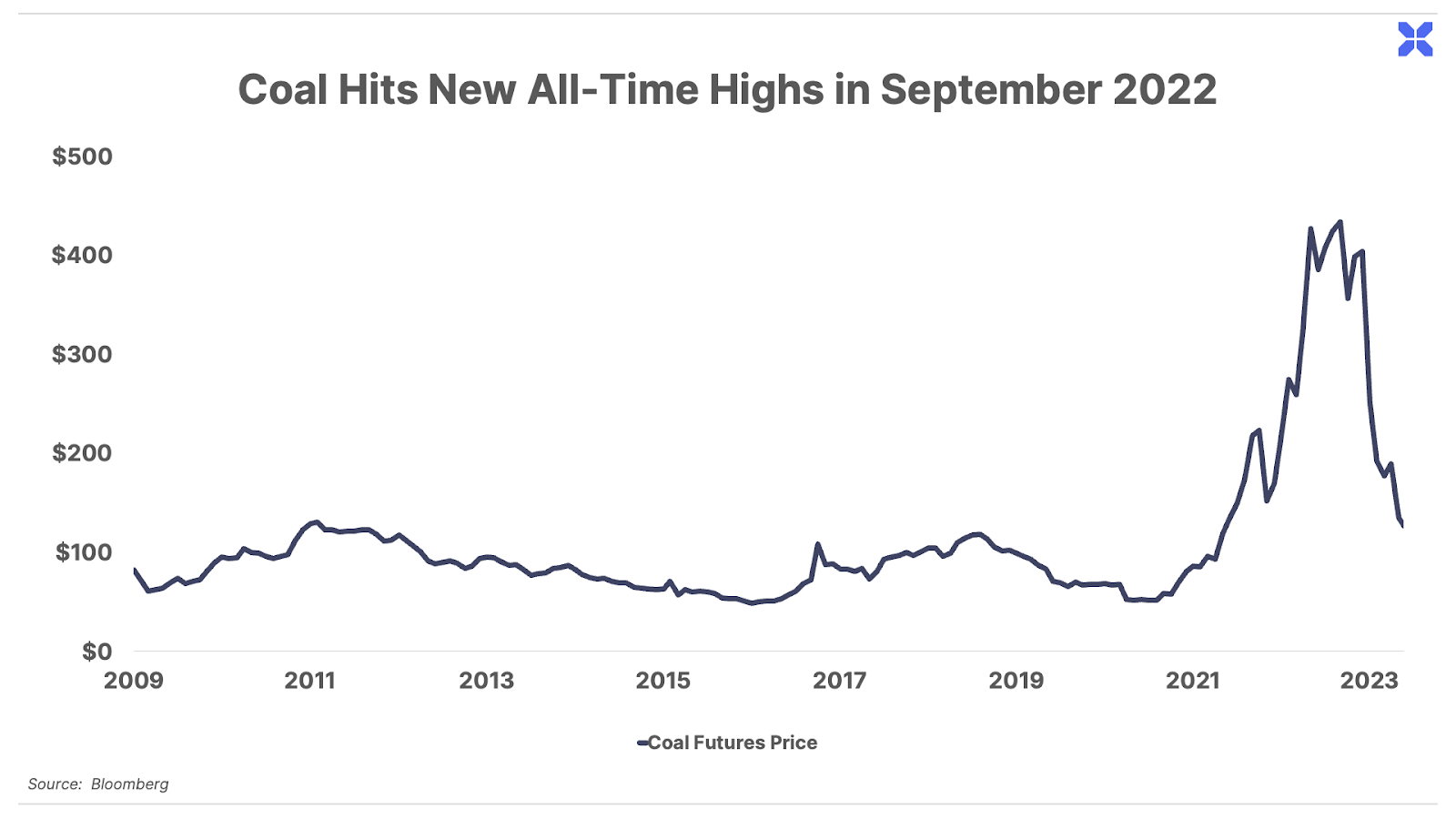

This demand resurgence sent coal prices to new all-time highs above $400 per metric ton last fall. Prices have reversed lower as record-setting warm winter weather provided temporary relief to both gas and coal prices:

Ironically, “enlightened” Europe was one of the biggest contributors to coal’s resurgence in 2022. Policymakers were forced to defer their climate-saving ambitions and scramble to prevent millions of households from literally freezing in the 2022 winter.

That’s how coal consumption in Europe – the leading global climate warrior – grew by 9% in 2022 to 377 metric tons (Mt). In total, seven EU countries restarted coal-fired power plants that had been closed, and lifted caps on existing coal-powered electricity in 2022.

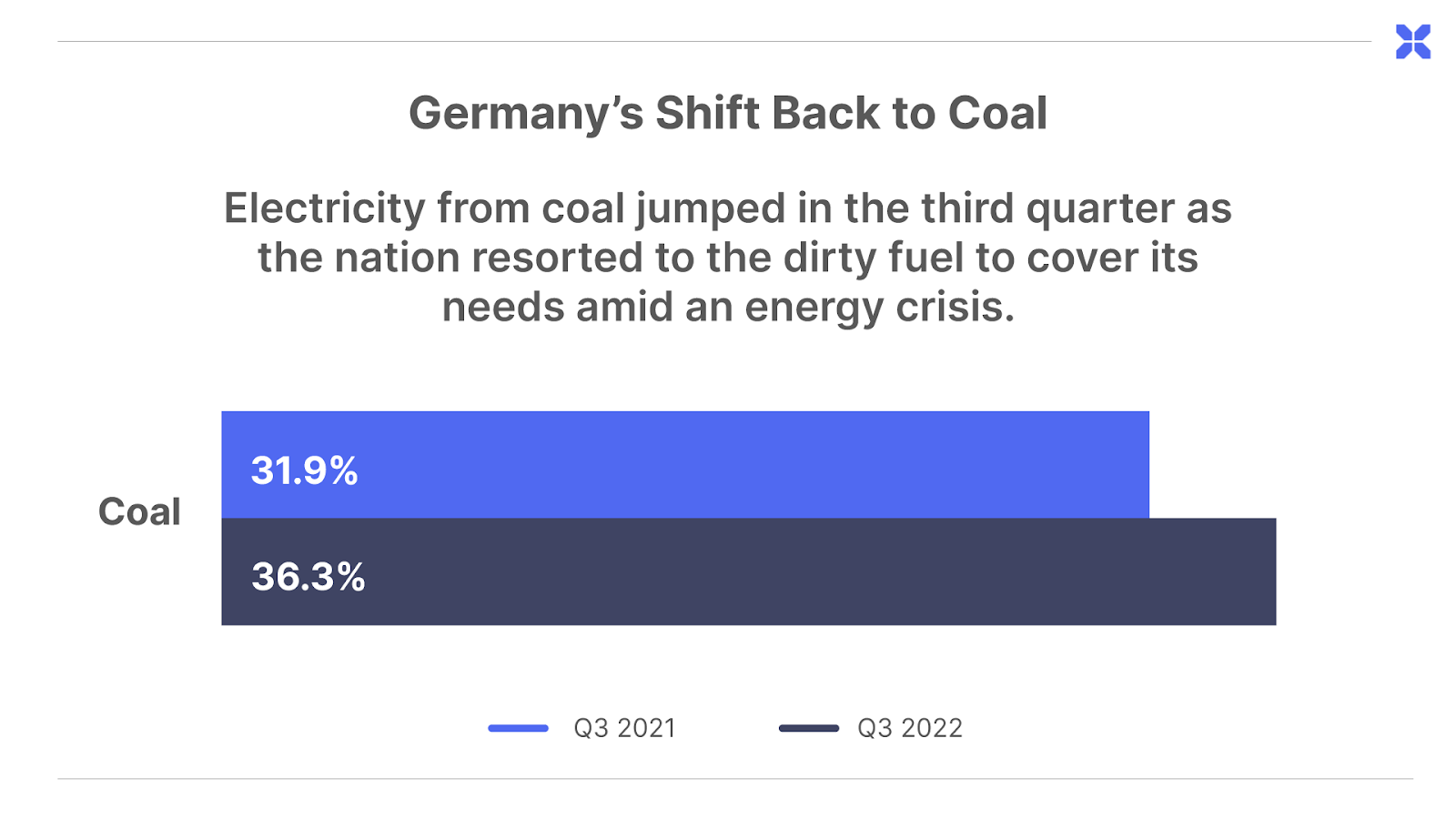

Germany was the largest contributor to Europe’s coal burning bonanza, as it scrambled to replace Russian gas (55% of its total gas consumption). Germany restarted 11.6 gigawatt hours (GW) of previously shuttered coal-fired power plants, and postponed the previously planned shutdown of an additional 3.8 GW of coal-fired power generation.

This increased the share of coal-fired electricity powering Germany’s electric grid from 31.9% in Q3 2021 to 36.3% in Q3 2022:

Europe still plans to cut coal out of its power mix, but the Russian “energy vacuum” means coal will be a necessary stopgap until at least 2025. The latest coal market outlook from the International Energy Agency (IEA) explains:

“The current forward markets indicate that the marginal costs of coal-fired power plants will be far below those of gas-fired power plants in the next few years… This would only change in 2025 when forward gas prices are low enough to place efficient gas-fired power plants ahead of inefficient coal-fired ones. However, (coal-fired) power plants are expected to remain very competitive until 2025.”

Japan and South Korea have also had to burn more coal. Both countries had made progress cutting back on coal consumption to reduce CO2 emissions over the last decade, but turned the coal furnace back up in response to higher LNG prices last year.

In South Korea, the government suspended limits on coal-fired power generation, resulting in a 6.3% increase in coal consumption last year. Japan likewise boosted its coal demand by 1.8% last year to reduce its consumption of high-priced LNG imports.

Given the relative pricing between coal and natural gas, the IEA expects Europe, Japan and South Korea to hold coal consumption flat at today’s elevated levels through 2025.

World’s Largest Countries Double Down on Coal

And then, there’s China and India – home of the two largest populations on the planet, and the two largest coal consumers globally. These countries are both all-in on the cheapest, most reliable source of baseload power generation.

China, the world’s largest coal consumer, accounts for 53% of global demand. Despite China’s pledge to supply 25% of its energy grid with alternative energy sources like wind and solar, the country remains committed to coal as a critical source of reliable base power generation.

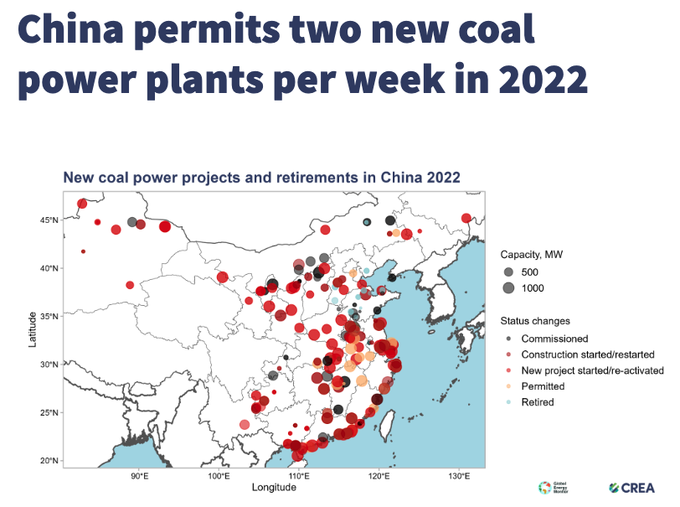

Coal makes up 60% of China’s total energy consumption, and even before the global gas shortage of 2022, the country was doubling down on coal. In 2021, China increased its coal-fired power capacity by roughly 3% with the addition of 26 giga-watts (GW) of coal-fired power generation – adding more coal power plants that year than the rest of the world combined. Last year, China tripled down on its coal fleet with 106 GW of additional capacity, representing an average of two new coal power plants each week. This pushed its total coal consumption up by 4.6% in 2022 to a new all-time high.

India, home of the second-largest population in the world at 1.4 billion people, is also one of the fastest-growing economies on the planet, with expected GDP growth of 7.3% in 2023. Much of that growth is powered by coal, which fuels 73% of the country’s electricity generation. India currently has 25 GW of coal-fired power plants under construction, and the IEA estimates coal demand for India will grow through at least 2025.

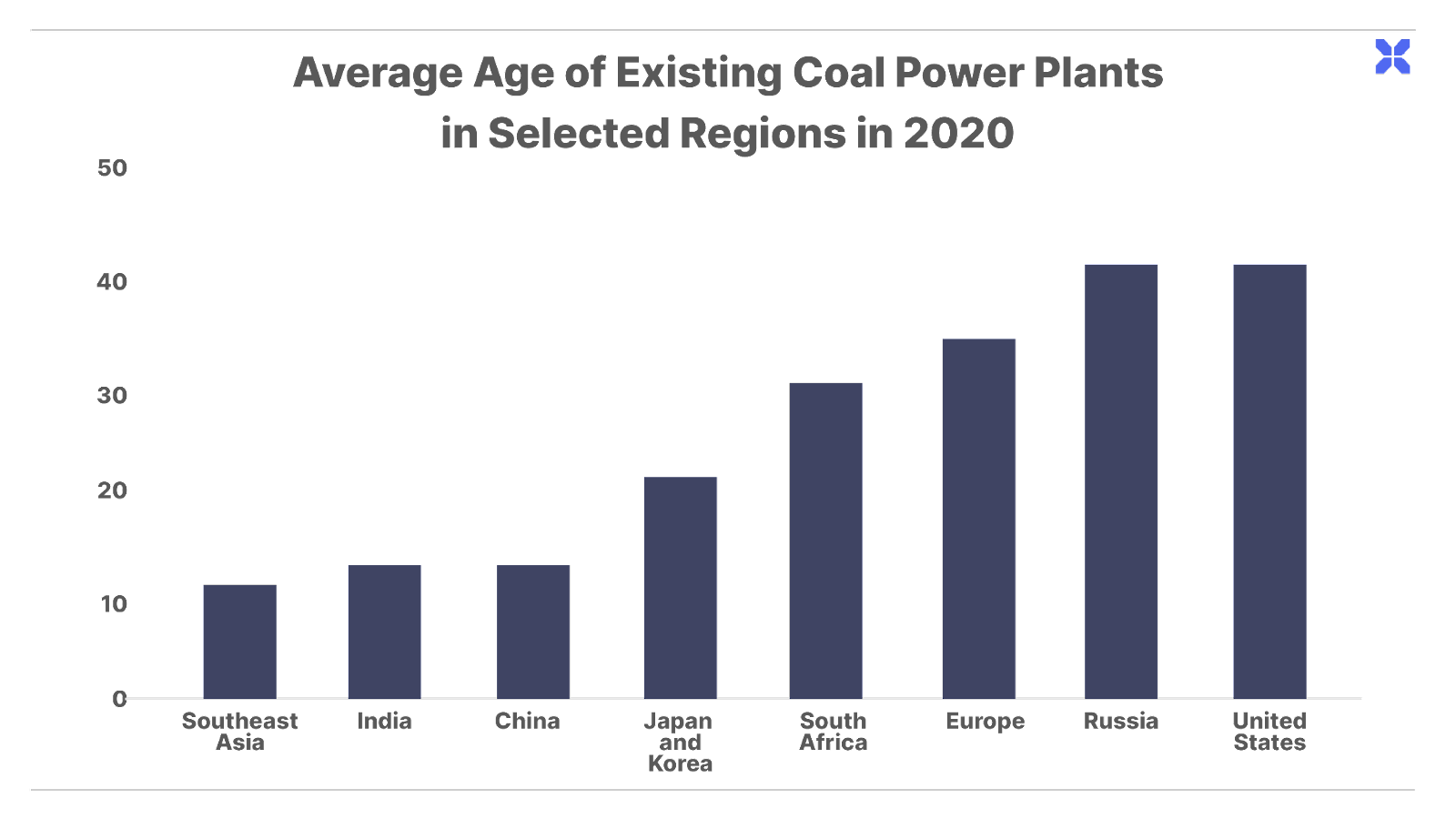

In the U.S. and Europe, policymakers are prohibiting investment in new coal-fired power plants, and pushing the industry to begin phasing out these plants as they reach the end of their useful lifespans. In contrast, India, China and a large cohort of developing economies in southeast Asia, like Indonesia and Vietnam, will be running their relatively young fleet of coal-fired power plants for decades to come:

With the global gas shortage pushing both rich and poor countries around the world towards burning coal, the hated commodity will experience a multi-year demand boost that will hold global consumption flat through at least 2025, according to the latest estimates from the IEA.

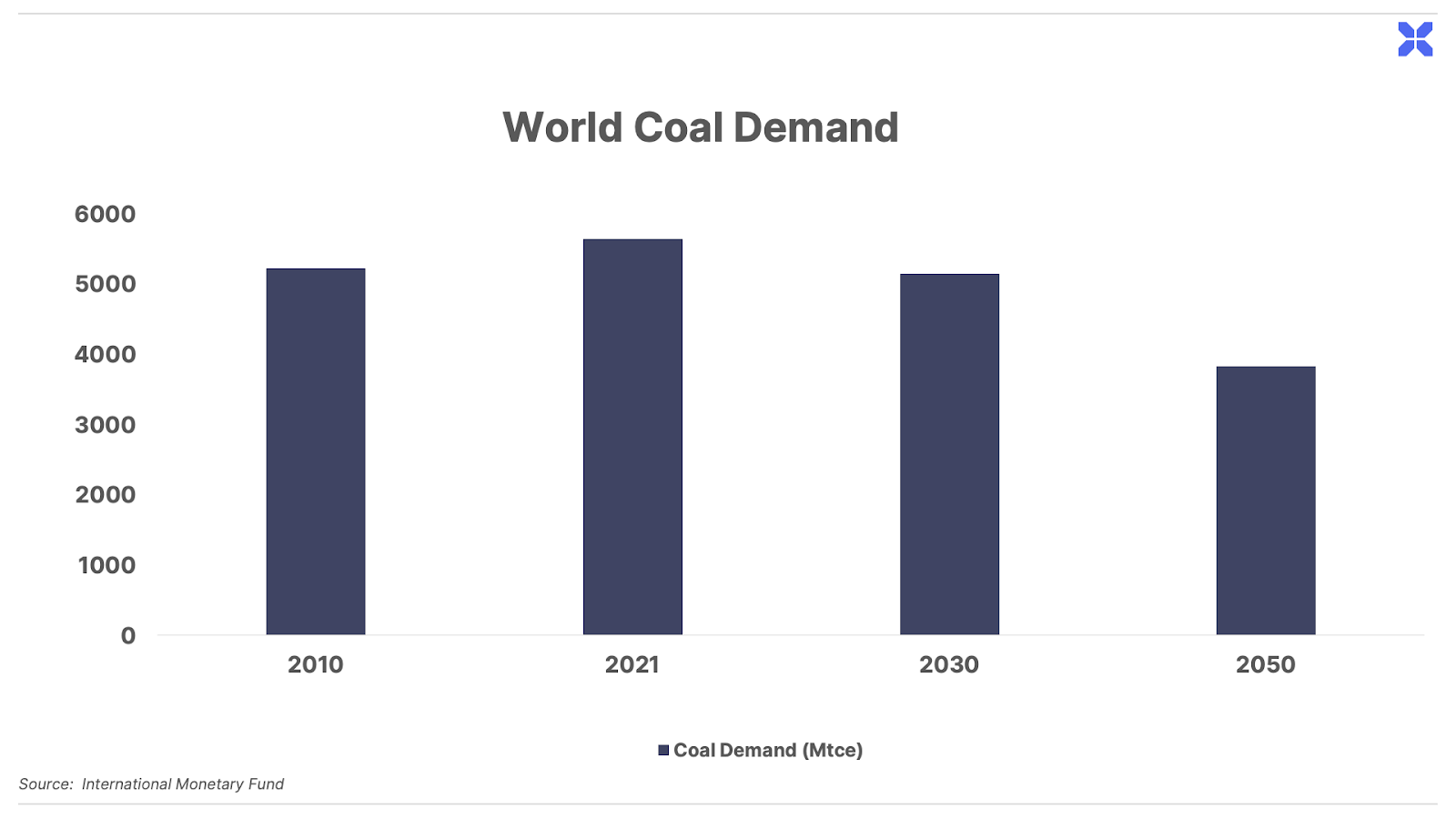

Looking ahead, the IEA notes that if policymakers around the globe eventually follow through on their long-term plans to close coal plants, consumption will fall by around 10% from 2022 levels by 2030.

From there, the IEA’s projections assume that further progress in closing down coal plants will bring global consumption down another 25% through 2050:

For the next several years, though, it’s clear that coal demand is headed straight up.

A Capital Vacuum

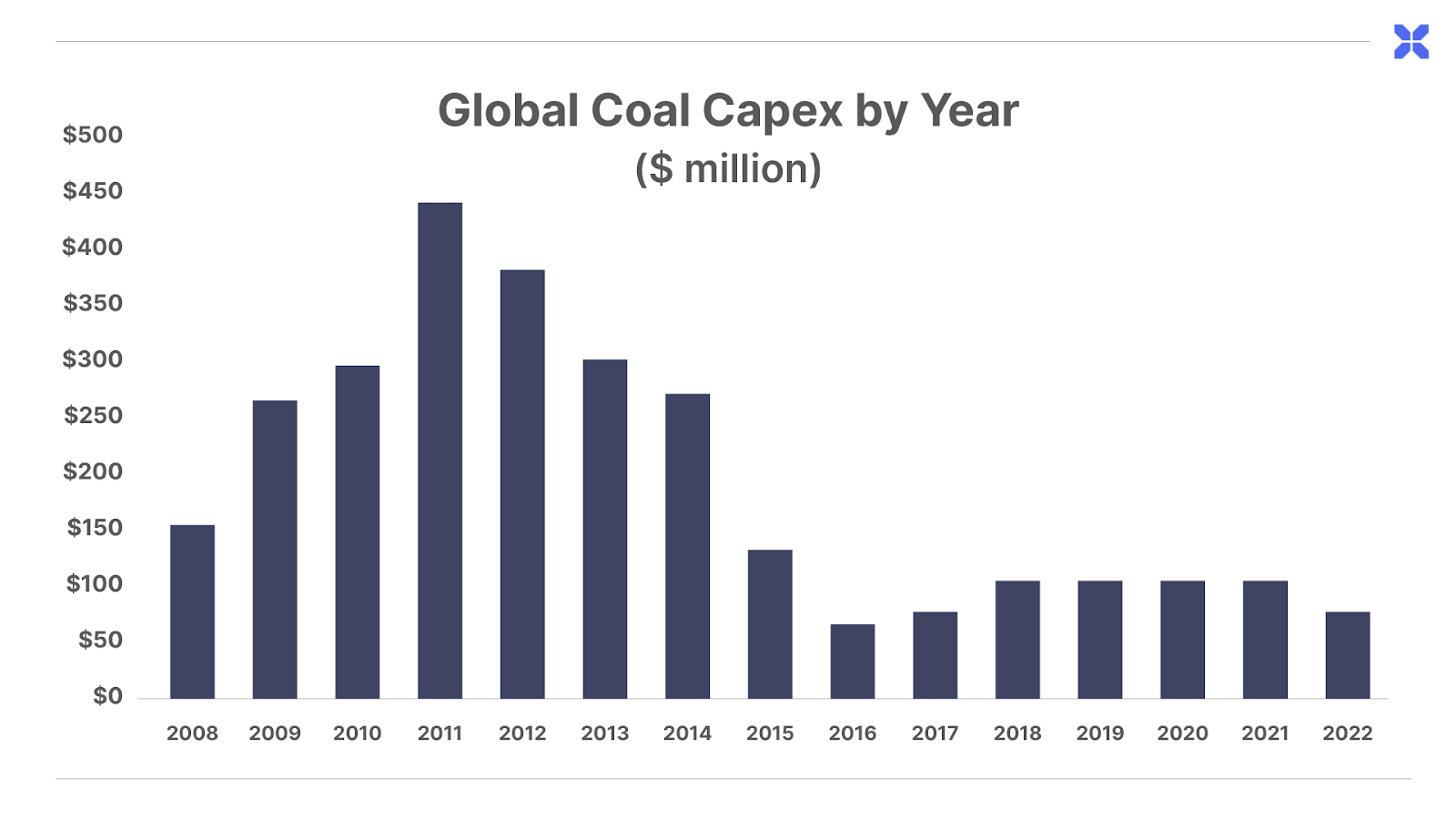

The problem for global energy markets, and the opportunity for us, is that institutional investors don’t want coal dust on their fingers.

Even after 2022’s cash flow windfall resulting from record high coal prices, capital expenditures for growing coal output (i.e., growth capex) fell to new lows last year, as shown below:

So even though coal demand may fall by 25% through 2050, ongoing, significantly lower levels of investment into coal production means supply could fall even faster – regardless of how high prices go.

In other words, even assuming that policymakers follow through with their stated intentions to shut down coal plants (i.e., the global energy shortage is solved), there’s still a multi-decade runway for low-cost coal producers to rake in the cash.

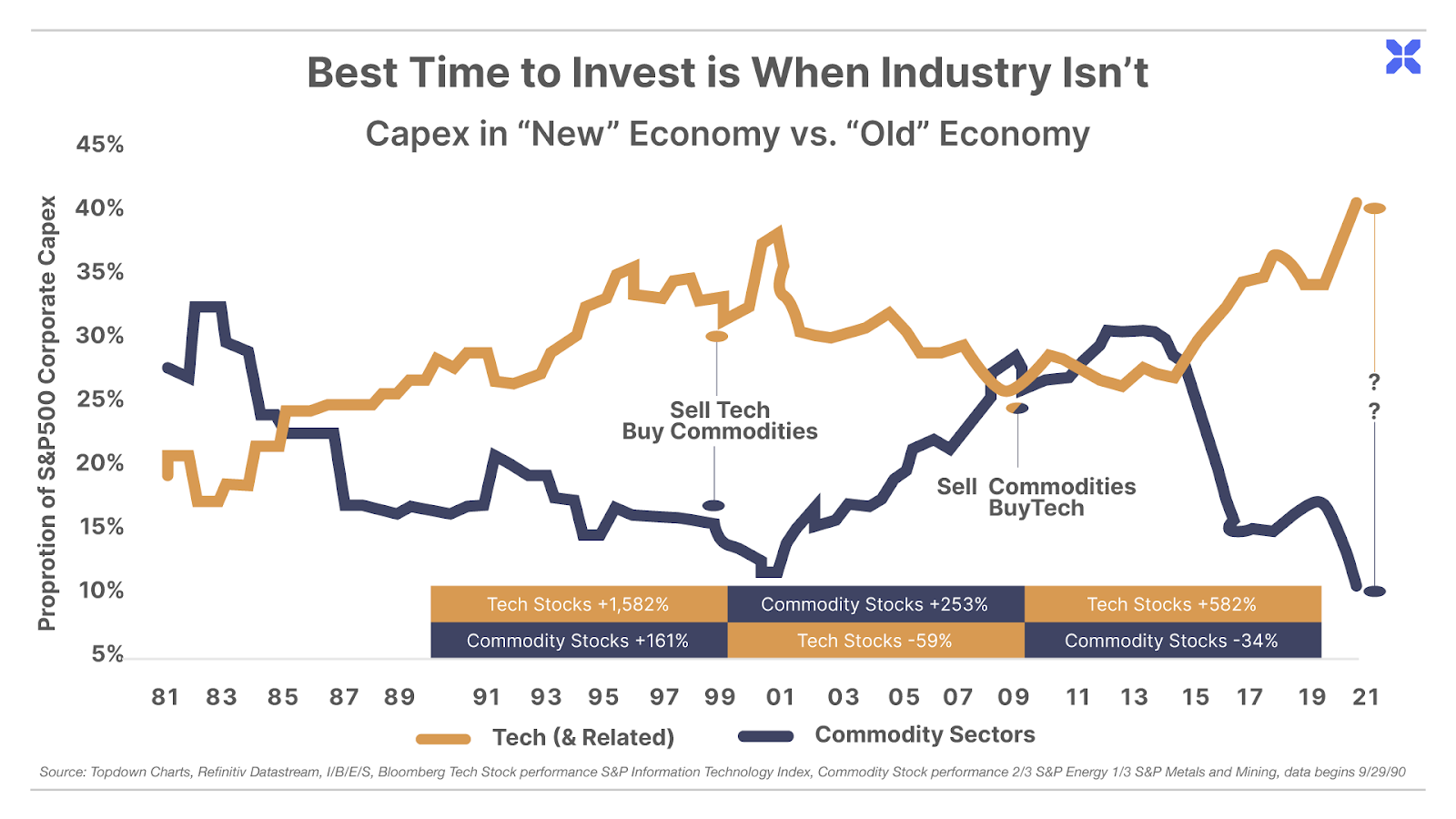

History shows that the best time to invest in any sector is precisely when capital is fleeing:

Right now, the big money is out chasing AI (as we discussed here). Institutional investors have left the boring “old economy” sectors like energy in the dust in favor of new darlings like Nvidia. Today, energy is by far the cheapest sector in the S&P 500… and the coal sector is the cheapest, and most hated, among the energy cohort.

Now, these are not the kind of world-class, capital efficient businesses that Porter & Co. typically focuses on. (We’ll delve into the financials of the sector in a moment.) But top-tier coal producers today are priced as if they’re facing imminent bankruptcy, despite all of the factors lining up to unleash a cash flow windfall for years to come.

In short, coal stocks have simply become too cheap to ignore.

How cheap? Below, we’ll introduce a business that generated $1.6 billion in free cash flow over the last 12 months. And after netting out the $500 million in net cash on its balance sheet, the company trades at just 1.5x free cash flow.

It’s committed to returning the majority of its cash flows back to shareholders, including a recently announced $1 billion buyback, representing 40% of the company’s current trading value, net of cash.

This content is only available for paid members.

If you are interested in joining Porter & Co. either click the button below now or call our Customer Care Concierge, Lance James, at 888-610-8895.