The Most Important New Medical Modality In Decades

Despite A Biotech Winter, This Stock Should Rise

| Below is the most recent issue of Biotech Frontiers, from analyst Erez Kalir. In addition to hosting Porter & Co. Biotech Frontiers on our website, we also make it available as a downloadable PDF. Subscribers can access this issue as a PDF on the “Issues & Updates” page here. If you have any questions, please give Lance, our Director of Customer Care, and his team a call at 888-610-8895 or internationally at 443-815-4447. Again, thanks for being part of Porter & Co. |

In the mid-1970s, as America grappled with post-Vietnam War cynicism and oil shocks, a quieter and positive revolution was unfolding – not in politics or warfare, but in biology labs tucked away in the red-roofed Spanish Colonial buildings of Stanford University. Two Stanford scientists – Dr. Paul Berg, who would go on to win a Nobel Prize for his work, and Dr. Herbert Boyer, who carried forward Dr. Berg’s initial breakthrough – had made an audacious leap: they discovered a way to splice together DNA from different organisms, creating the first recombinant DNA.

What they had built in test tubes was more than a new biological tool. It was, in effect, a programmable system for instructing living cells to produce anything coded in genes – insulin, growth hormone, antibodies, vaccines… Life’s operating system was suddenly editable.

But discovery alone wasn’t destiny. Turning recombinant DNA into a world-changing therapeutic technology would take vision, gumption, and capital. Enter Genentech, co-founded in 1976 by Dr. Boyer and a young venture capitalist named Bob Swanson, who’d literally cold-called university professors looking for the next Big Thing. With less than a thousand dollars of seed capital and a handshake deal, these two bet that genetically engineered bacteria could be coaxed into manufacturing human insulin – a protein-based hormone that, until then, had to be extracted from pigs and cows.

What followed was one of the most consequential biotech races in history. Rival teams around the world scrambled to be the first to clone and express the human insulin gene in microbial cells. Genentech won. In 1978, it announced that its E. coli bacteria were producing real, bioactive human insulin. Just two years later, Genentech went public in a white-hot IPO that sparked Wall Street’s love affair with biotechnology. The stock soared nearly 500% on its first day, and investors who held shares from the early private rounds would go on to reap returns of over 100x.

But Genentech’s impact didn’t stop at shareholder wealth. It pioneered an industry – the industry we know today as “biotech.” The tools, models, and scientific talent Genentech developed would go on to produce blockbuster drugs to fight cancer, rheumatoid arthritis, and growth disorders – and train generations of biotech founders. It turned DNA into a source code not just for medicine, but for a new economy.

This month in Biotech Frontiers, we turn our lens on the next great paradigm of modern biotechnology: RNA interference and small interfering RNA (“siRNA”). If recombinant DNA and Genentech taught us how to treat disease by manufacturing proteins outside the body, siRNA therapies are teaching us how to silence disease from within – by turning off the genes that cause it in the first place. Just as recombinant DNA unlocked a new era of drug-making, siRNA is now unlocking an era where we don’t just supplement biology – we command it.

This month’s recommendation is a company that is as category defining in its leadership of the siRNA era as Genentech was for recombinant DNA. And to advance our discussion, we’ll rely on a variation of our proprietary Biotech Frontiers investment framework:

- The Big Picture

- The Science

- The Opportunity

- The Catalysts

- The Balance Sheet And Cap Table

- The Risk/Reward

The Big Picture

In December 2024, we significantly shrank the Biotech Frontiers portfolio due to the Big Picture risks we foresaw from President Donald Trump’s economic policies. We highlighted his announcements on tariffs, immigration, and taxes as likely causes of major indigestion for the U.S. economy as well as capital markets. Since then, the flagship U.S. large-cap biotech index (XBI) is down 20%, the Russell 2000 index of small cap stocks is down 15%, and the U.S. dollar is down 9% relative to a basket of trade-weighted currencies. None of these declines are surprising. In fact, I’d have expected the S&P 500 index to have fallen by more than about 2% in the same period.

Several Biotech Frontiers readers have written to ask whether I think the economic and market environment will continue to deteriorate. Unfortunately, the answer is yes – for three key reasons.

The Era Of Economic Chaos

The first is the unpredictability the Trump administration has introduced into economic policy. Take tariffs. On April 2, the Trump Administration announced its “Liberation Day” tariffs, a draconian set of levies on more than 100 of America’s trading partners that far exceeded what most analysts and markets had anticipated. Following this announcement, global stocks registered their steepest daily and weekly declines since the COVID-19 pandemic. Seven days later, when the U.S. Treasury bond market – the most important financial market in the world – showed signs of cracking, President Trump flinched. He announced a 90-day “pause” on the Liberation Day tariffs, replacing them instead with a universal 10% tariff on U.S. imports from all countries except China, whose goods would be tariffed at 145%. Since then, nearly every successive week has witnessed some convulsive change to the proposed tariffs regime.

Imagine being a CEO in this environment. Many important American industries rely on imports to function, either because raw materials aren’t available domestically or because foreign production is cheaper. For businesses in these industries, their input costs have suddenly become totally unpredictable. How can they make investment decisions or even simple profit-and-loss forecasts when they’re flying in the dark about their costs? And what effect does this uncertainty have on their appetite to take risks? Little surprise that many metrics of business confidence have collapsed since the beginning of the year.

The Rule Of Law

The second reason I’m bearish centers on the Trump administration’s attack on the rule of law. Founding Father John Adams wrote that the U.S. is “a government of laws, not of men.” His point is simple: The U.S. president is not a king. Because he’s not a king, he doesn’t dictate the law nor have the final word on its meaning. The federal courts do, interpreting laws passed by Congress and the U.S. Constitution. The president and the Executive Branch implement the laws exercising reasonable discretion – they don’t invent them, nor can they willfully ignore them based on a president’s whims. This separation of powers protects the American economy, and American citizens, from the kinds of arbitrary abuses of power that we see from despots like Russian President Vladimir Putin, China’s head Xi Jinping, and Venezuelan leader Nicolás Maduro in countries where the rule of law doesn’t exist.

These ideals may seem like they’re about civics or politics, but they are crucially important to a flourishing economy. Entrepreneurship, private investment, and innovation all depend on the rule of law – it’s what gives people confidence that contracts will be enforced, property rights will be protected, and disputes will be resolved impartially by independent courts. A stable rule of law fosters trust and enables risk taking. When it’s absent, corruption, expropriation, and violence become everyday parts of economic life. Just ask anyone trying to do business in a banana republic. The biggest difference between the U.S. economy and corrupt, mafia-state economies like China, Russia, and other emerging markets is that we have a strong rule of law – and they don’t.

Unfortunately, the Trump administration has attacked the rule of law head on. Many of the administration’s most controversial executive orders have, perfectly understandably, been challenged in the courts. But when federal judges – including in several key instances, conservative, Republican-appointed judges – have ruled against the administration, Trump has viciously attacked them by name, calling them “lunatics” and “USA haters.” He has incited his supporters to intimidate them and, in some cases, has brazenly refused to comply with court orders. Federal judges around the country who’ve lived most of their professional lives in quiet anonymity have started to receive unordered Domino’s pizzas delivered to their homes. The message is clear: “We know where you live.”

Last week, a three-judge panel of the U.S. Court of International Trade, a branch of the federal judiciary, unanimously ruled that President Trump’s sweeping tariffs exceeded his authority under the International Emergency Economic Powers Act (“IEEPA”). The court found that President Trump’s stated reasons for imposing the tariffs didn’t meet the law’s definition of “unusual and extraordinary threats.” In effect, the Court said: Congress passed a law that gave a president special economic powers during wartime. But the United States isn’t at war today. Two of the three judges on the panel were Republican appointees, including one placed there by President Trump himself. While the Court’s order was stayed pending an appeal, President Trump once again caustically attacked the judges who issued the ruling.

The Trump administration’s attack on the federal judiciary and the rule of law won’t serve our economy well. It amplifies the unpredictability the administration has introduced through its policies. And it compels entrepreneurs, investors, and business leaders to reckon with gnarly questions they haven’t had to before, for instance:

- Will American law continue to provide a stable bedrock for commerce that U.S. businesses are accustomed to?

- Will the administration comply with legal rulings if it loses in court?

As these questions snowball in the months ahead, they will only drive capital flight out of the U.S. economy and increase the cost of capital for American businesses.

The Status Of The U.S. Dollar

The final reason I’m deeply concerned about the market environment ahead is a looming crisis of confidence in the U.S. dollar.

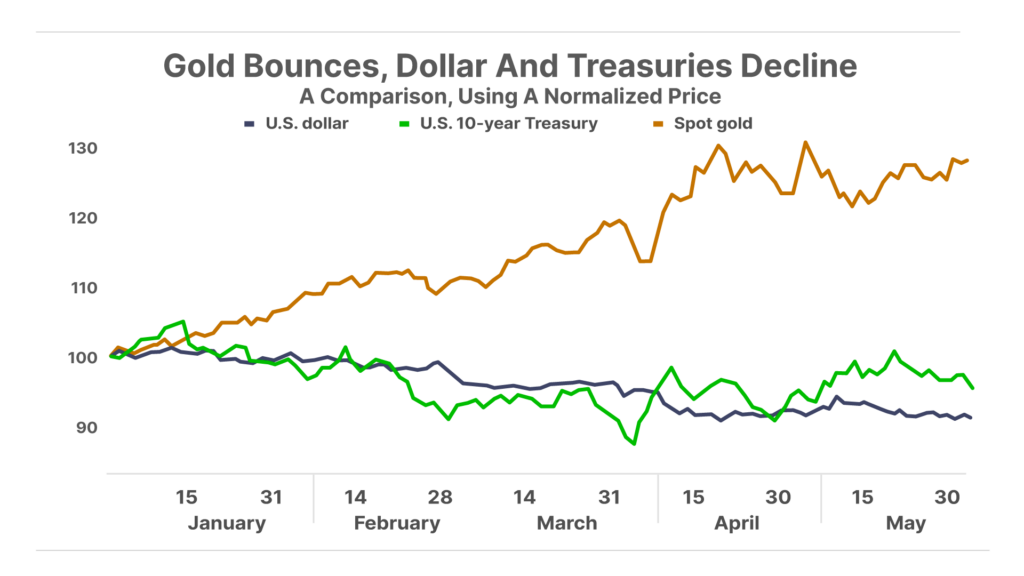

In April, I wrote a guest piece for Porter’s Daily Journal, in which I argued that the Trump administration’s attack on the global trading system and the institutions, agreements, and norms that have supported it over 80 years – the “Pax Americana” – was driving capital out of U.S. assets. The main casualties of the Pax Americana’s end are U.S. Treasury bonds and the U.S. dollar, both of which are experiencing a collapse in demand as America’s trading partners stay away from these assets to avoid the damage Trump has inflicted. The dollar’s 9% decline since December against a basket of other global currencies is a strikingly large move in the foreign exchange market. Even more striking is the move in gold, which has appreciated nearly 25% over the same time. Capital is leaving the dollar into other paper currencies and into “hard money.”

Now the Trump administration appears set to make this self-created problem even worse with its “Big Beautiful Bill.” The bill, which has already passed the U.S. House, will make the 2017 tax cuts permanent while eliminating taxes on tips, overtime pay, and car-loan interest payments. The Congressional Budget Office estimates that the bill will add $3.8 trillion to the U.S. national debt over the coming decade – or about $11,000 per American.

Now don’t get me wrong: I’m all in favor of lower taxes and believe that thoughtful tax cuts can help spur growth. But cutting taxes while embracing profligate federal spending – as the “Big Beautiful Bill” does – isn’t a smart idea. Instead, it sends a message to the world that the U.S. isn’t remotely serious about reigning in its debt… And that we’re looking to “print” our way to prosperity.

If the Trump administration’s attack on America’s trading partners was the first major shock to the dollar, the “Big Beautiful Bill” could be the second. The bill’s passage will prompt large foreign holders of U.S. Treasuries to think seriously about getting out before the U.S. fiscal situation, and the dollar’s value, deteriorates even further. And it will prompt large discretionary buyers of U.S. Treasuries to search with determination for alternatives.

I don’t necessarily believe that the endgame will be a Lehman Brothers moment, in which the dollar collapses overnight. In fact, it’s more likely that the dollar experiences a slow bleed – a multi-year decline relative to other currencies (and gold) that unfolds over a decade or longer. But such a slow bleed will still be exceptionally painful for Americans, as we see our purchasing power decline annually and inflation inflict the kind of economic damage it last did during the 1970s.

Bringing It Back To Biotech

As a longstanding reader of Porter’s newsletter, I’ve always appreciated his guiding principle of giving readers “the same advice I’d want to receive if our shoes were reversed.” I’ve taken pains to share my thoughts on The Big Picture here with you in detail – because these aren’t ordinary times, and because The Big Picture is relevant not only to biotech but also to every other investment you hold in your portfolio. I’ve approached this discussion the same way I would a conversation with my family around a dinner table, when they ask for my thoughts about the financial world.

As bearish as these Big Picture reflections may seem, I actually think they’re fantastic news for readers of Biotech Frontiers. Let me explain…

As our regular readers know, we don’t make broad bets on the biotech sector in this newsletter. Instead, we take carefully chosen “sniper shots”: We aim to identify the distinctive, single stocks within biotech that offer us the most favorably asymmetric ratios of reward to risk. We have a detailed methodology for finding these opportunities, and our emphasis on strong catalysts helps steer us toward stocks with concrete events on the horizon to unlock value.

Our approach means that the wipeout in biotech – and the bearish market environment more broadly – works to our advantage. Because biotech stocks that benefit from positive catalysts often propel upward explosively, with gains of 50%, 100%, or more, we don’t need a positive trend in the sector or the market to help our winners “work.” The proof is in our results: We’ve identified six recommendations over the past 18 months that have appreciated more than 100%, with few losers. This track record helps illuminate how the bear market enables us to underwrite many of our investments at extreme, bargain-basement prices. We can also use the bear market to build a “shopping list” of the world’s most promising biotech franchises, with a realistic anticipation that the prices of these franchises will fall to levels at which they are compelling values.

This content is only available for paid members.

If you are interested in joining Porter & Co. either click the button below now or call our Customer Care team at 888-610-8895.