Issue #8, Volume #2

And Our Portfolio’s Exposure To The California Wildfires

This is Porter & Co.’s free e-letter, the Daily Journal. Paid-up members can access their subscriber materials, including our latest recommendations and our “3 Best Buys” for our different portfolios, by going here.

Three Things You Need To Know Now:

1. Trump gets started… but not on tariffs (yet?). Newly inaugurated President Donald Trump wasted no time in signing a pile of executive orders, including ones to withdraw the U.S. from the Paris climate accord, end DEI programs in the federal government, give TikTok more time to find a way to not be banned in the U.S., end automatic birthright citizenship, and pardon defendants involved in the January 6, 2021, attack on the U.S. Capitol. He also said that he was aiming to impose 25% tariffs on imports from Canada and Mexico and 10% tariffs on imports from China by February 1. See this Daily Journal from last week for Porter’s thoughts on the damage that tariffs can cause.

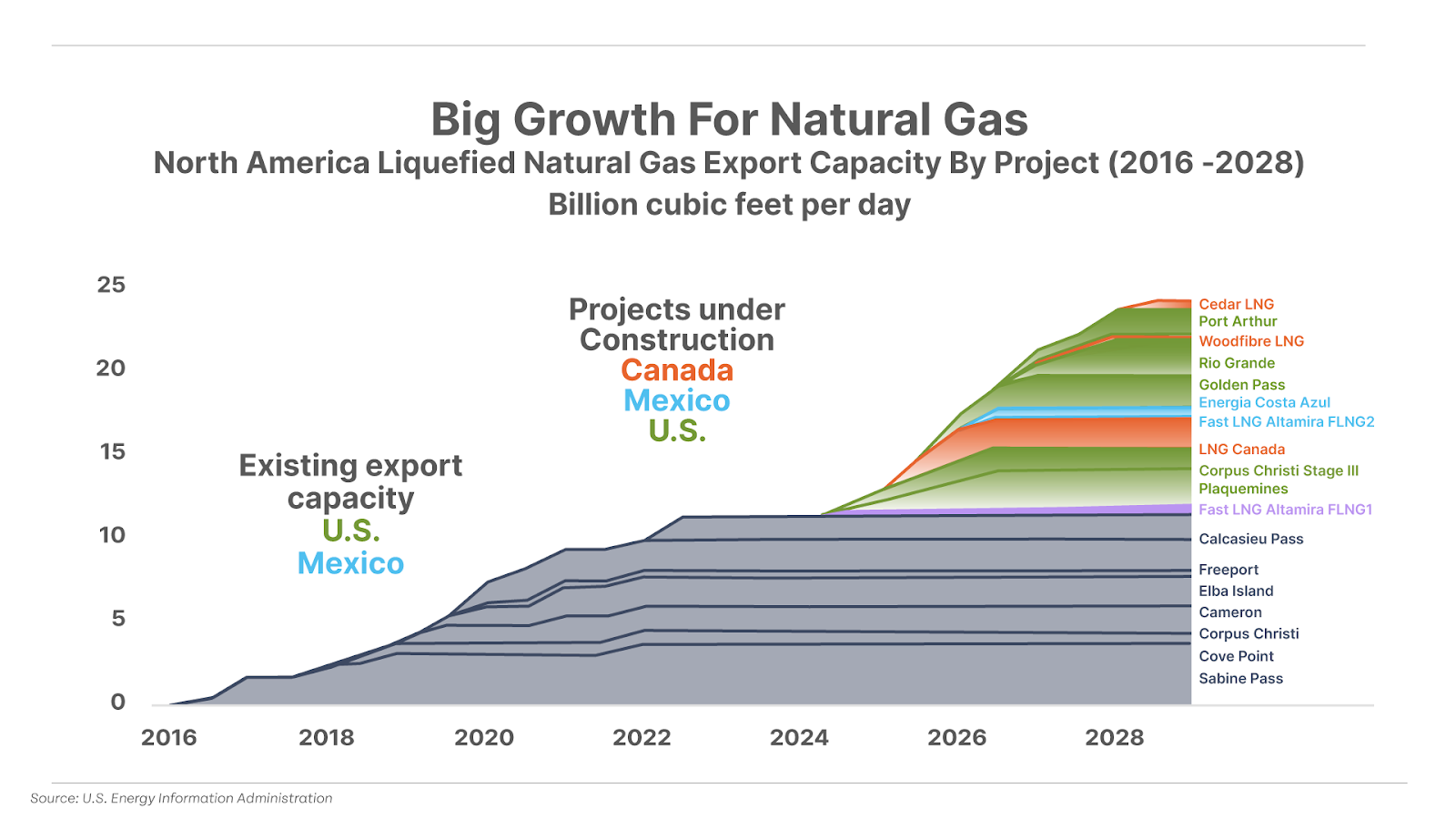

2. Making American energy exports great again. One of Trump’s other first orders of business on Monday was signing an executive order lifting former President Joe Biden’s freeze on permits for new U.S. liquefied natural gas (“LNG”) export terminals. The regulatory green light should accelerate America’s ongoing gas export boom, with U.S. LNG export capacity on track to double by 2028. This should add more upside to America’s leading natural-gas producers and LNG exporters, which have recently broken out to new 52-week highs across the board.

3. An office-space time bomb. The federal government owns 370 million square feet of office space nationwide – nearly as much as is in all of Manhattan. However, according to the General Services Administration, no major government agency occupies more than 50% of its allotted space. As a result, President Trump wants to sell two-thirds of these buildings. Given that office values have already declined by 30% on average over the past several years, these sales could further pressure commercial real estate prices and also hurt small banks – which issued roughly 70% of the loans for these properties.

And One More Thing…

As the economy holds steady, legendary investor Stanley Druckenmiller is observing a notable shift in business sentiment, with C-suite executives turning “giddy,” he told Becky Quick on CNBC’s Squawk Box on Monday.

“The economy is very interesting. We’re at a very low unemployment rate, essentially 4%, with 3% GDP growth. I’ve been doing this for 49 years, and we’re probably going from the most anti-business administration to the opposite. We do a lot of talking to CEOs and companies on the ground. And I’d say CEOs are somewhere between relieved and giddy. So we’re a believer in animal spirits…”

But it’s not all good news. He continued: “In terms of the markets, I would say it’s complicated. Despite what I just said about all the wonderful things about the economy, we have an earnings yield to bond yield ratio that’s the most unattractive level in 20 years” – in short, the reading of that ratio suggests equities are overvalued.

When Druckenmiller speaks, it’s worth paying attention. Don’t be surprised if we see more “animal spirits” like the Trump coin over the first half of 2025. But as we’ve warned recently, and as Druckenmiller was alluding to, equity prices are at multi-decade highs… and it might take a decade or more for many of today’s S&P 500 members to “grow” into their current valuations.

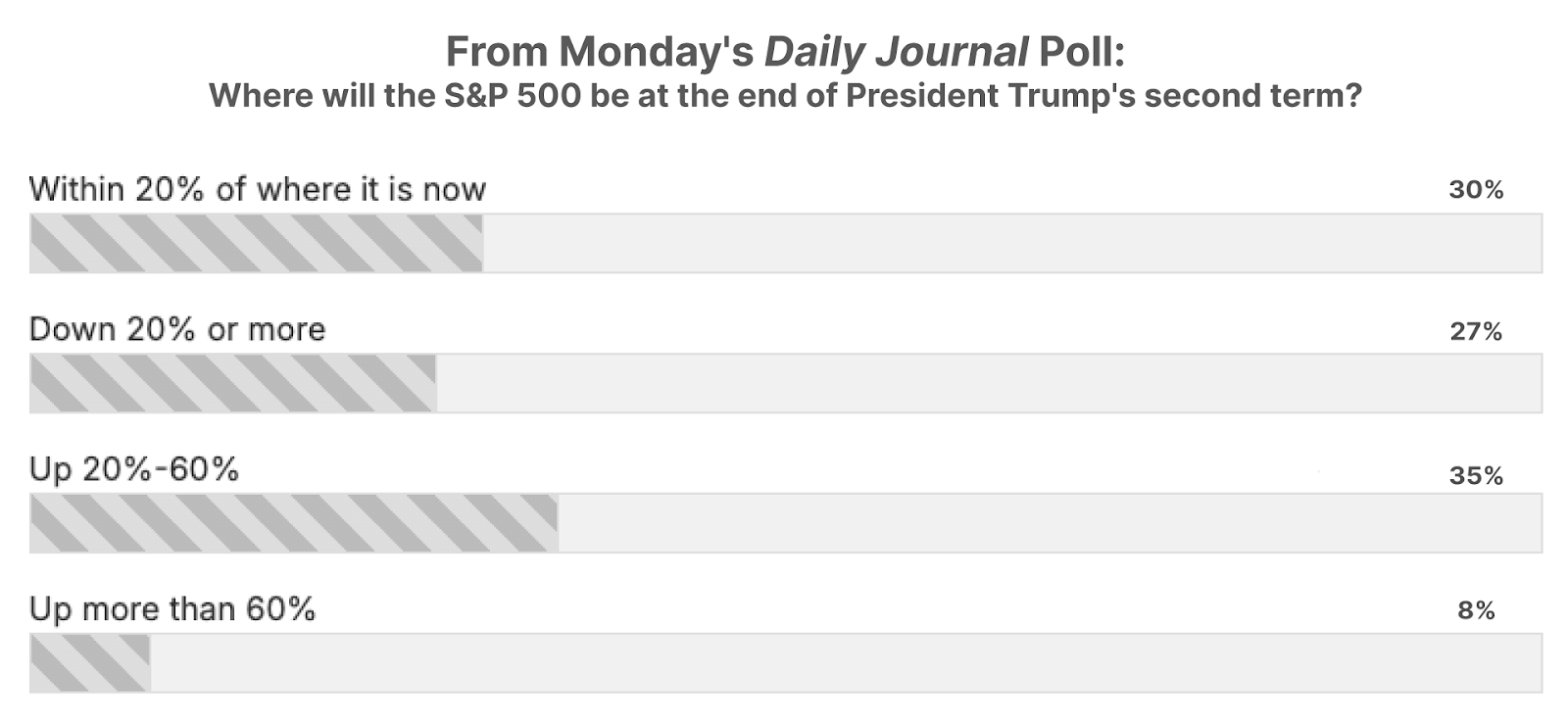

Poll Results… The S&P 500 At The End Of Trump’s Term

In the Daily Journal on Monday, President Donald Trump’s inauguration day, we asked readers: “Where will the S&P 500 be at the end of Trump’s second term?” And we got a mixed bag of results. Of those readers who took the survey, 35% selected “Up 20%-60%,” 30% checked “Within 20% of where it is now,” and 27% picked “Down 20% or more.” Just 8% of survey takers took the most bullish option of “Up more than 60%.”

An Update On Property & Casualty Insurance

And Our Portfolio’s Exposure To The California Wildfires

As many of you know, property-and-casualty (P&C) stocks are the foundation of my investment strategy.

There are three reasons:

- Well-run businesses in the property and casualty insurance sector do not have to pay for capital. Instead, much like a private equity fund or a hedge fund, they get paid to hold and invest capital. This so-called “float” is the money that customers have paid in premiums but that has not yet been paid out in claims. Investing this capital enables them to produce relatively high returns on equity for very long periods of time, as long as (and this is a very important “but”) they maintain their underwriting discipline.

- From time to time, for various reasons, these firms will trade at a wide discount from intrinsic value. That’s mostly because the market doesn’t understand how to value “float” – that’s the capital these firms control, but do not own.

- Assurance – that is, managing risk – is a core function of the economy and it is very unlikely to change in a material way during my lifetime.

Not many investors understand that the “magic” of Berkshire Hathaway isn’t Warren Buffett’s extremely good investing decisions. The magic is the incredible leverage Berkshire produces for his investing through its insurance float. Cliff Asness of the legendary quant firm AQR Capital Management estimates that Berkshire’s insurance float gives it the same investment advantage as using six times its equity capital.

If you want to understand P&C insurance, I strongly recommend reading Buffett’s 1999 shareholder letter. On page six, he explains the entire strategy under the subhead “The Economics of Property/Casualty Insurance.”

Our main business – though we have others of great importance – is insurance. To understand Berkshire, therefore, it is necessary that you understand how to evaluate an insurance company. The key determinants are: (1) the amount of float that the business generates; (2) its cost; and (3) most critical of all, the long-term outlook for both of these factors.

Many subscribers have asked about the impact of the California wildfires to our recommended P&C insurance stocks.

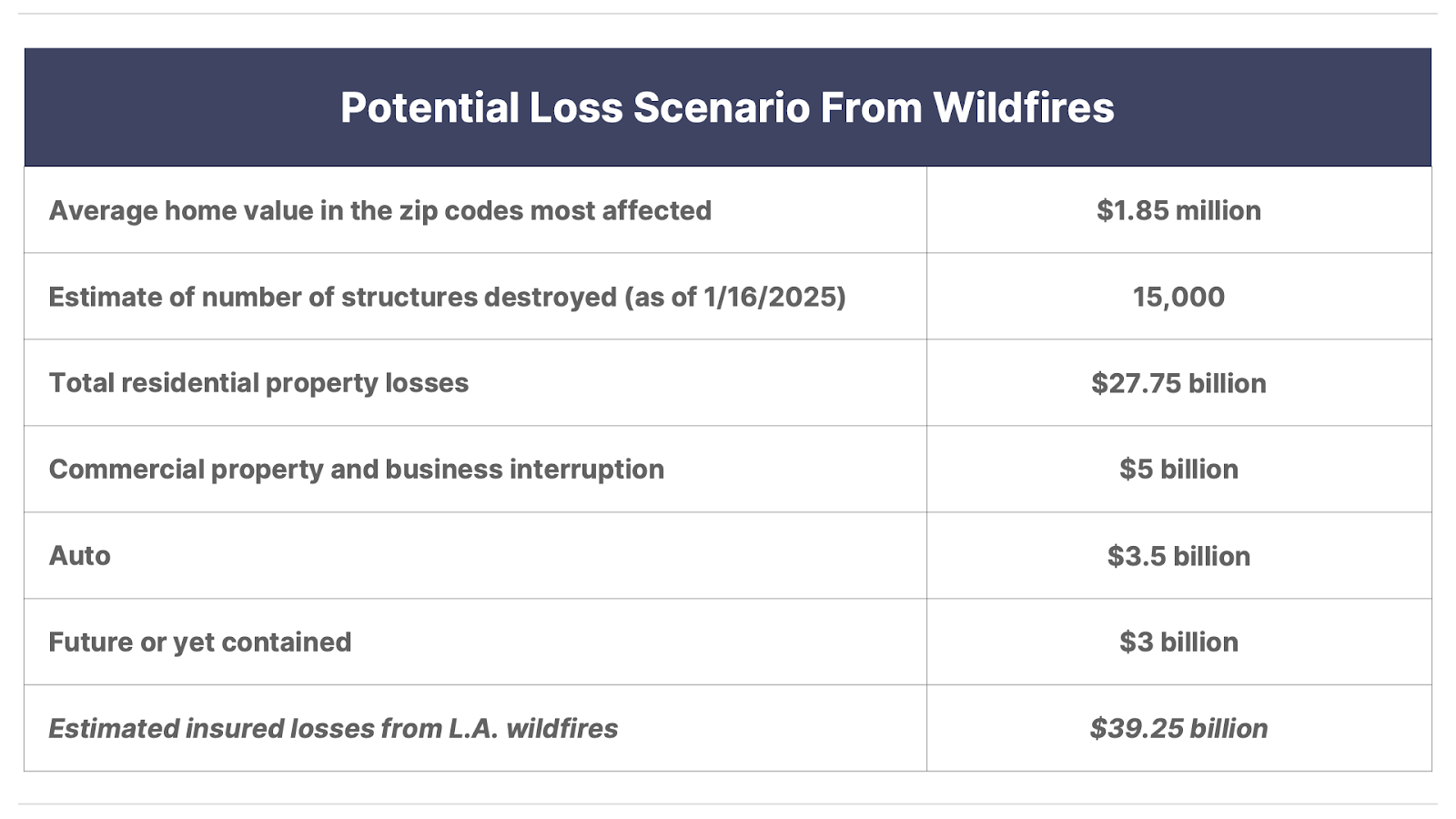

Their concerns are valid: one of the largest and wealthiest communities in the United States has been largely destroyed, with over 15,000 structures burned across 63 square miles, an area roughly the size of Washington, D.C.

The most recent estimate for economic losses stemming from the wildfires has been pegged at $275 billion by AccuWeather. And that was an increase of almost 100% from its original estimate of $150 billion. It will be several months, or maybe even a year, before we have any firm idea about the size of the total loss.

But there are two things to keep in mind, in terms of the liability of insurers, when you hear about these huge numbers.

First, starting in 2021, many large insurance companies began to exit the California market because of state regulations that forbade insurance companies from raising premiums to account for their own reinsurance costs.

And, second, many homes in these very wealthy areas will simply not be insured. For example, for many years I owned homes on Flamingo Drive in Miami Beach. This street is only a few hundred feet from the ocean and runs alongside the Intracoastal Waterway. It is obviously prone to flooding and hurricane damage. In fact, one of the homes I bought had been knocked about six inches off its foundation from a tidal surge in the Great Miami Hurricane of 1926, which ended the first Florida land boom. As a result, getting insurance on these houses was incredibly expensive – equal to roughly 10% of the estimated value, every year. I chose to self-insure, as many wealthy people in the Pacific Palisades will have done, too (which means putting money aside to cover the cost of repair).

Not including this factor, in general, insured losses tend to be around 13% of total economic losses. Using that assumption, then, we estimate that insured losses would be around $40 billion. Here’s our math:

That sounds bad.

And the risks to the industry from this catastrophe will scare many investors. That has, and could easily continue to, lead to selling pressure, in the short term, in some of our longest held and best recommendations. But I would urge you to remember Buffett’s words.

What matters most is the long-term outlook for the growth and the cost of the insurance company’s float.

This catastrophe will, almost surely, lead to the sale of more insurance in the future and at much higher rates.

Meanwhile, while this situation is a terrible tragedy, it doesn’t seem (at least to us) to be anything out of the ordinary for insured risks.

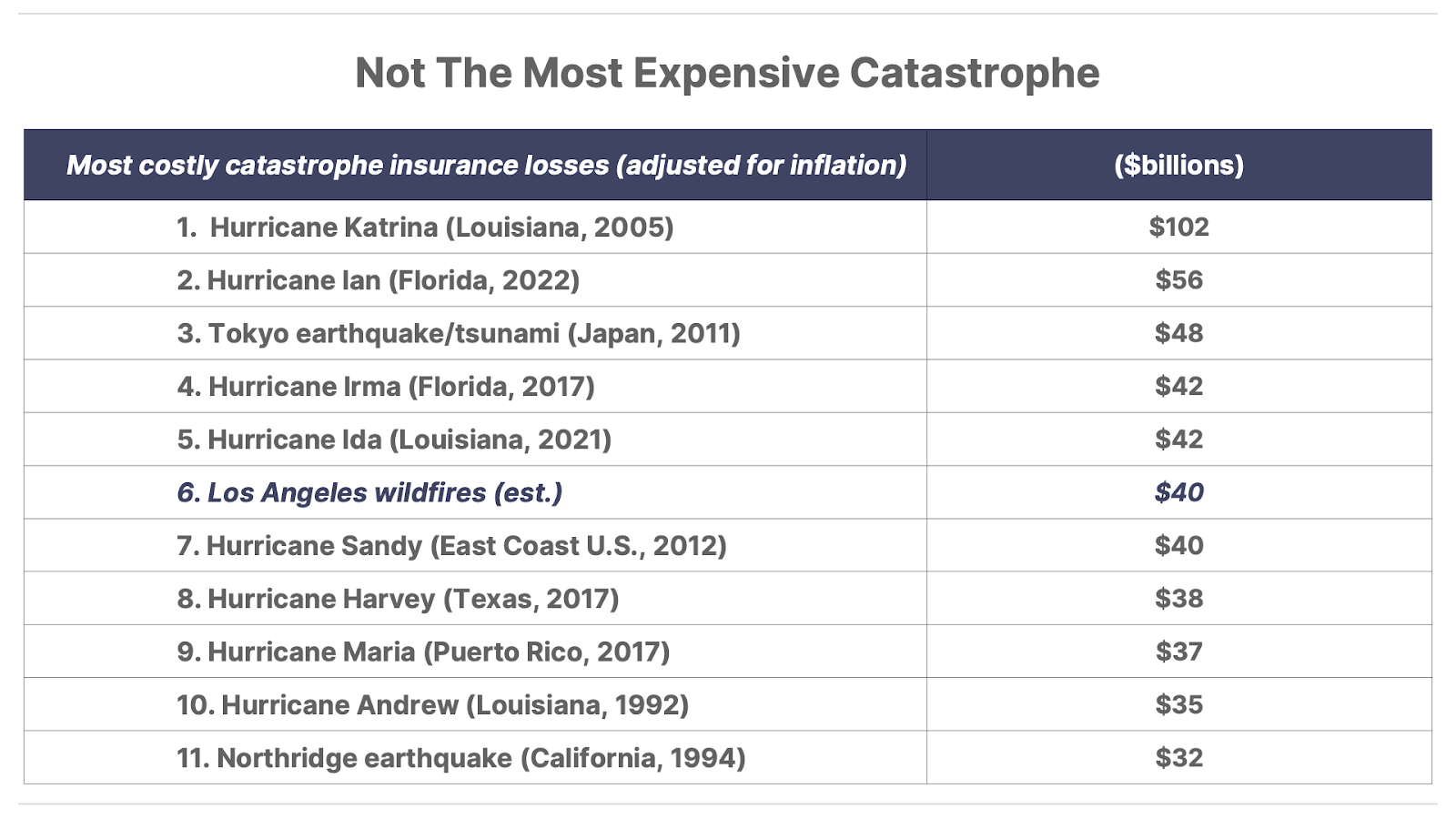

Our loss estimate would establish these wildfires as the sixth costliest insured loss in history.

So… yes… this is a bad situation, but we don’t think it will make any lasting or material impact on our recommended P&C companies – and, ironically, it could lead to substantially higher premiums being paid in the future in California.

Where we do expect to see losses announced are in the excess and surplus insurance firms (E&S). These are the insurance companies that specialize in insuring high-risk properties where normal regulations do not apply.

As it has become increasingly more difficult to get insurance in California, the E&S carriers stepped in to write insurance on commercial properties. E&S insurers, like American Financial Group (AFG), Skyward Specialty Insurance (SKWD), Kinsale Capital (KNSL), and RLI (RLI) are not regulated entities and, thus, could charge whatever price they wanted. As a result, these companies will likely post a loss estimate when they report Q4 2024 numbers in the coming weeks. In particular, we believe Kinsale will have the most loss exposure as it has been growing faster than the other E&S firms.

Again, while we wouldn’t be surprised to see investors sell on this news, we’re certain that selling is a mistake. These companies are the best firms in the entire world at pricing risk, and, while they may take a small loss in this quarter on their California exposure, they’ll make those losses up, and more, in their other markets. And this event will allow them to charge more in the future.

In regard to regulated policies (like home and auto), the publicly traded names that could have high loss exposures are Allstate (ALL), Travelers (TRV), Chubb (CB), The Hartford Financial Services (HIG), AIG (AIG), and to a lesser extent Progressive (PGR).

Progressive – which has been one of our best recommendations – has very limited homeowners’ exposure, but has about 6.5% of the market share in personal auto in the state of California. Personal auto losses are expected to be only a fraction of the total loss costs. Again, we do not expect these losses to be large enough to create an underwriting loss for the year.

On the other hand, Chubb could have both exposure on the commercial side and on the homeowners’ policies. It has a 9% market share in commercial multiple peril in California, which means it will have some exposure on the commercial side. And while its 2% market share in homeowners in the state may seem small, its exposure will be greater because it specializes in high-net-worth homeowners.

But, even if the news sounds really bad at first, you have to remember that Chubb, like all of these firms, carries re-insurance that limits its exposure to these risks. In Chubb’s case, it retains the first $1.75 billion of losses, then reinsurance coverage kicks in (4.4% of total estimated losses). Chubb is a $100 billion market cap business, with $151 billion worth of investments on its balance sheet. It earned $10 billion last year.

My point is, while there may be noise in the headlines, nothing about this situation endangers Chubb. And these losses, while potentially large, do not change the intrinsic value of the business one iota.

And there’s one big wildcard: the utilities.

If it is found that any of the California utilities were at fault for part of the fires, the insurance industry can sue for recovery of those losses. California law holds utilities responsible for fires caused by their equipment. Southern California Edison – a unit of Edison International (EIX) – has already been sued, with the lawsuit stating that its high-voltage transmission tower caused the 14,000-acre Eaton fire that decimated the Altadena neighborhoods. Of course this could be tied up in courts for years, but it could easily result in these losses being recouped and these expenses being put back on California’s rate payers for years.

One specialty insurer that we don’t cover (and haven’t recommended) is Mercury General (MCY). It is focused primarily in California, which, in our view, made it too risky.

And, as you would expect, MCY shares have plunged in the last several weeks due to fears of its heavy exposure to losses from the Palisades fire. And, along with the major national insurers that we have covered and recommended, we also believe investors’ fears about Mercury’s exposure are overdone.

Yes, it’s true that Mercury has most of its exposure in California, which makes up roughly 80% of its premiums. However, the majority of Mercury’s California exposure is in the auto market, with only 23% of California premiums written to homeowners. Thus as a percentage of its total business, California homeowners make up just 18% of Mercury’s total written premiums. While this is still a significant exposure, the key thing to note is that Mercury doesn’t focus on the high-end homes in the Palisades and elsewhere that made headlines this month. The majority of its homeowner policies are limited to under $1 million in total insured value.

Raymond James wealth-management analyst C. Gregory Peters recently reiterated his bullish view on the stock, with a $70-per-share price target (it currently trades around $50 per share). Peters noted that Mercury’s reinsurance policy should limit its losses to $150 million. That’s less than 10% of its current shareholder equity of $1.8 billion, and about one-third of its operating profit of $400 million last year.

Further, because Mercury primarily writes short-tail policies (which are usually settled within a year), the impact will mostly be limited to 2025 earnings. Peters estimates the California fires will likely cause 2025 earnings to fall by a third, with the impact dropping off to just a 7% hit on 2026 earnings, which he estimates at $6.50 per share. That leaves Mercury trading at less than 7x next year’s earnings.

For the traders out there, that might be a great opportunity over the next year.

Let me know what you think by sending comments to [email protected]

Good investing,

Porter Stansberry

Stevenson, MD

Mailbag

Today’s letter is from Rodger G. who is commenting on the item in Monday’s Daily Journal that chronicled President Trump’s release of two memecoins, which both skyrocketed in value, potentially providing him billions of dollars in profits over a period of 36 hours.

He writes…

Over the weekend I caught a documentary on crypto. In it, this exact same story of how the crypto market has allowed so many “alt coins” to be used to only benefit the creators was a key topic. It was a great example of why many people are still concerned and skeptical about investing in the crypto space. I would have far more respect for the insiders if the memecoin proceeds were being used to pay down the federal debt, but I’m not holding my breath for that to happen. The greed of this select group – which I’m confident all know each other – is what is so wrong with this country. It’s a perfect example of the very corruption that the new Prez tells the public that he and his conspirators are going to fix.

It’s another example of the “End of America” that Porter has been so concerned about for good reasons. It’s a sad time for the country – while so many are struggling or homeless from the recent wildfires our new leadership is literally laughing at the citizens who voted them into office.

Just my humble opinion!

Rodger G.

P.S. Investing in crypto and technology is all about getting in front of the next big trend.

There’s no one better at that than Jeff Brown.

Jeff is a bona-fide prophet when it comes to understanding what’s next in tech and crypto.

For example… he got his subscribers into Bitcoin in 2015… Nvidia in 2016… and AMD in 2017.

The results… Bitcoin is up 26,613%… Nvidia, 10,422%… AMD, 1,229%.

And now… Jeff is all-in on the world of cryptos.

Jeff has been saying for a while that newly inaugurated President Donald Trump could trigger the biggest crypto boom ever.

And on Friday, with the release of the Trump coin (followed not long thereafter by the Melania coin), the new American president showed just how extraordinary cryptos could perform… when $TRUMP mushroomed from nothing to a short-term peak of $75 billion… in less than 36 hours.

And what’s next? Jeff has long been at the bleeding edge of technology – and cryptos in particular. And he has opinions – potentially extremely profitable ones – about the cryptos that are best positioned to benefit from a pro-crypto White House.

To learn more about what Jeff thinks is coming next for cryptos, see here.