Issue #1, Volume #2

How Tariffs, Immigration, And Taxes Affect The Big Picture

Happy 2025… We hope you enjoyed the “12 Days of Christmas” over the holiday, when members of the Porter & Co. team shared a favorite essay, article, speech, or book excerpt and how it inspired them.

We are back today with the Daily Journal, Porter & Co.’s free e-letter. Paid-up members can access their subscriber materials, including our latest recommendations and our “3 Best Buys” for our different portfolios, by going here. On Thursday at 4 pm ET, we will publish The Big Secret on Wall Street, and also on Thursday, we release new issues – including brand-new recommendations – of Biotech Frontiers and Distressed Investing for those who subscribe. (One holding in the Biotech Frontiers portfolio is up 40% today – and is nearly a triple since Erez re-recommended it. To learn more… call Lance James, our Director of Customer Care, at 888-610-8895, or +1 443-815-4447 internationally.)

Three Things You Need To Know Now:

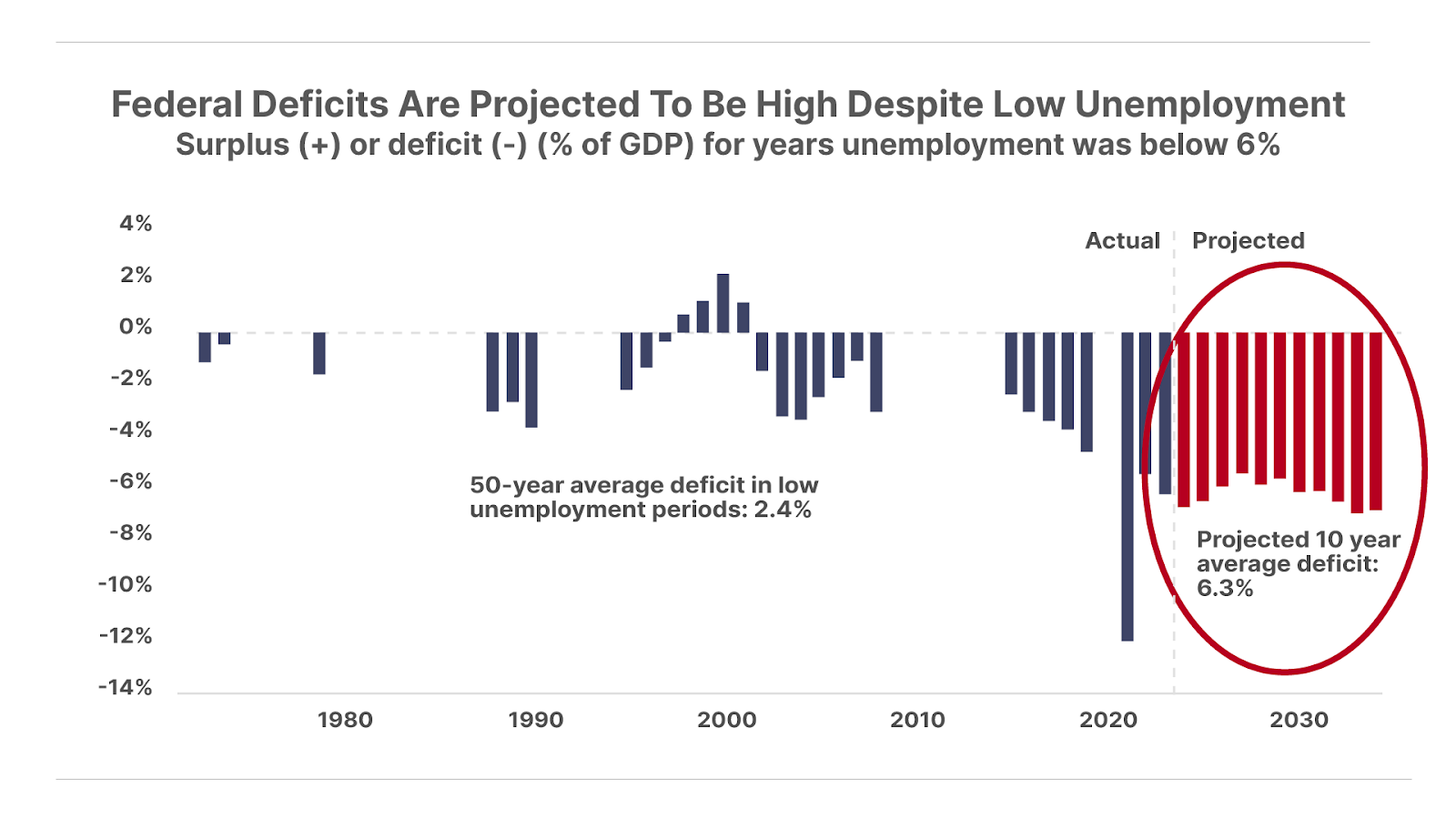

1. America’s deficits spell doom. As a percentage of GDP, the U.S. deficit is projected to average 6.3% over the next 10 years. This is historically unprecedented: This level of indebtedness has never happened outside of periods of shattering economic crises or war… And now, it’s business as usual. (This year the deficit is expected to hit 7.1% of GDP – third only to China and India. Welcome to the developing world, America!) What this means over time is the end of the dollar, as there’s no way that U.S. trading partners will indefinitely finance this kind of irresponsible and unsustainable borrowing. The other losers are civil society and private enterprise… and the stock market. Winners – so to speak – will be Bitcoin and gold.

2. In the meantime, though, the dollar is stronger than ever. The U.S. Dollar Index (DXY) – which measures the value of the dollar versus a basket of six other major currencies – has risen 22% over the past four years, and nearly 9% since September. It’s currently trading at its highest level in over two decades, outside of a brief spike in the fall of 2022. It’s thanks to President-elect Donald Trump’s tariff sabre-rattling… but unless government spending is cut – see above – the dollar’s strength is temporary.

3. Commercial real estate bust accelerates. Default rates on commercial mortgage-backed securities (CMBS) increased to 11.0% in December, surpassing the former high of 10.7% in 2012. The default rate is up by 9.4 percentage points in the last two years, or twice the rate of increase during two years of the 2008-2009 Financial Crisis. That’s a big problem for the holders of the roughly $6 trillion pool of commercial mortgage loans outstanding, including the $1 trillion of loans that will need to be refinanced this year.

And one more thing…

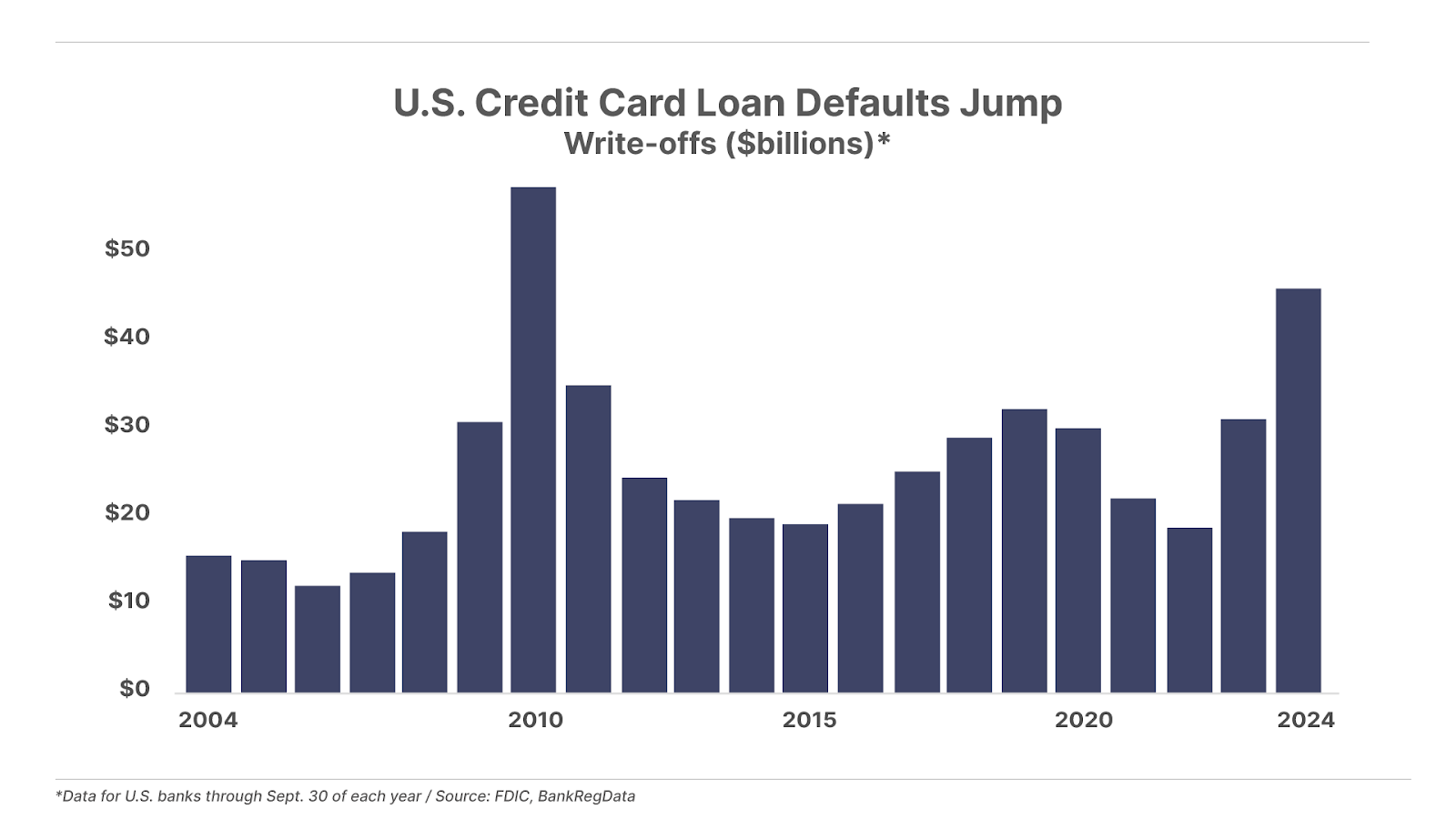

Over the first nine months of 2024, U.S. credit card lenders wrote off $46 billion in seriously delinquent loan balances – up 50% from the same period in 2023… and the highest level in 14 years. When the spending power of lower-income Americans is tapped out – what’s happening now – the American economy will be in trouble. Don’t say we didn’t warn you…

Coming up this week: This week will likely see additional evidence of the ongoing economic slowdown. On Tuesday, the results of November’s Job Openings and Labor Turnover Survey (JOLTS) will be released, which are expected to decrease 3.1% compared to October. On Wednesday, the ADP Nonfarm Employment report is projected to show 139,000 jobs created in the private sector in December, down from 146,000 in November. On Friday, the December Jobs Report should show that U.S. employers added around 153,000 new jobs over the past month, on pace with the six-month average.

Trump’s Inflation Triggers

How Tariffs, Immigration, And Taxes Affect The Big Picture

The following is extracted from Erez Kalir’s most recent issue of Biotech Frontiers. While Erez usually writes about biotech stocks, he has a well-grounded perspective on how the macro-level economic environment plays out in the overall market. In his prior experience he worked directly for Julian H. Robertson at Tiger Management during the Global Financial Crisis.

We are sharing portions of his most recent issue that provide readers a clear-eyed perspective on what he sees ahead. On Thursday, we will publish a new issue of Biotech Frontiers in which Erez will provide updates on this topic.

In his election-night speech following his resounding victory on November 5, President-elect Donald Trump conveyed a simple message to the nation. To those wondering what would come next after he took office, he said: “Promises made, promises kept.”

So what has Trump promised to do, economically? Let’s focus on three key pillars of his policy agenda: tariffs, immigration, and taxes.

Tariffs

Tariffs were a centerpiece of Trump’s economic policy throughout his campaign – and in his first term as president. And on November 25, he announced his intention to impose 25% tariffs on Mexico and Canada – America’s two largest trading partners after China – until they significantly clamped down on fentanyl trafficking and undocumented migration. As for China, Trump stated he would consider levying an additional 10% tariff on all imports from China, over and above the 60% tariffs on Chinese goods that he had previously promised.

While some commentators have suggested Trump is threatening these tariffs as a negotiating tactic and won’t actually implement them, his track record as president suggests otherwise. During his first term, Trump imposed 30% to 50% tariffs on imported solar panels and washing machines, 25% tariffs on steel, and 10% tariffs on aluminum. Collectively, first-term Trump tariffs covered about 4.1% of U.S. imports. This time, the tariffs he has promised cover a much broader swath of America’s imports from its three largest trading partners.

To state plainly what most readers already know, a tariff is simply a tax on imported goods. When these taxes are imposed, they aren’t usually absorbed by the foreign manufacturer, but instead passed on in whole or in part to U.S. consumers through higher prices. For example: If a toy manufactured in China used to cost, say, $15 at Walmart, and that toy (along with all other Chinese-made goods) is now subject to a 60% tariff, the $9 tax on the toy isn’t going to get eaten by the manufacturer. It’s going to be reflected in a new, higher price at Walmart – probably something close to $24.

This inflationary result isn’t just common sense. It’s also borne out by historical economic data.

In 2019, economist David Furceri and his colleagues at the International Monetary Fund published the most comprehensive analysis ever on the impact of tariffs. Their study encompassed 151 countries and nearly 60 years of data, from 1962 forward. What did they find? Tariffs cause a substantial increase in inflation… and the higher the tariffs, the bigger that increase.

I am not generally a big fan of academic economists. Too often, the pretty mathematical models they build end up having no helpful relationship to the real world. But there are a few exceptions.

No major academic economist has been more “right” about important things in recent years than Harvard’s Larry Summers. After all, Summers – a Democrat who served as Treasury Secretary under President Bill Clinton – loudly warned the Biden administration early in its term that its post-COVID economic policies would unleash massive inflation. At the time, these warnings made Summers a pariah within the Democratic Party. But he was proven right.

Summers some weeks ago gave a long interview to one of my favorite journalists, News Items (on Substack) author John Ellis (a conservative who is a cousin of former President George W. Bush). The interview is well worth listening to in full. Here is the relevant excerpt on Trump’s proposed tariffs:

The more important part is he’s talked about a big tariff on every good that we import, which means higher import prices, also means higher prices for everything that competes with imports… that’s substantially inflationary.

Summers has shown that his economic predictions are accurate and not politically biased. He was witheringly critical of Biden’s economic policy. I’m confident his call about the inflationary impact of Trump’s tariffs will be on the money as well.

Immigration

Another centerpiece of Trump’s agenda is his promise to deport the estimated 13 million undocumented immigrants who reside in the United States. When pressed on how many of these immigrants a Trump administration could realistically deport, Vice President-elect J.D. Vance said at least 1 million per year. Trump has already signaled his intention to follow through on this promise by appointing Stephen Miller – the architect of his first-term immigration policies – as deputy White House chief of staff.

Immigration is a hot-button political issue that elicits strong emotions on all sides. But at Biotech Frontiers, I’m not interested in politics or emotions. My job is to help you understand the economic and investment consequences.

Undocumented immigrants make up approximately 50% of the U.S. farm workforce today. Most of these laborers are unauthorized workers who get paid below the minimum wage with none of the benefits that are provided to U.S. citizens or legal residents. They work 10 to 12 hour shifts in all weather, with longer hours during harvest seasons.

Yet despite this reliance on undocumented workers, U.S. farmers still face an acute labor shortage. A study produced by Michigan State University earlier this year found that the average U.S. farmer reports a 21% labor shortfall. Even relying heavily on undocumented immigrant workers, the typical U.S. farmer is able to fill only about four out the five jobs they need to run their farm effectively.

This should not be surprising. How many Americans do you know who would want to spend 10 to 12 hours a day in the punishing heat of the agricultural basins in California, Texas, or Nebraska picking crops for the minimum wage or less?

But agriculture isn’t the only critical part of the U.S. economy that depends on undocumented immigrants. Around 23% of the construction workforce in the U.S. consists of immigrants who entered the country illegally and have no residency or labor authorization. And in construction, too, a heavy reliance on undocumented immigrants hasn’t saved the sector from a labor shortage – the U.S. construction industry today faces a shortfall of between 500,000 and 1 million workers. As a result, the U.S. has a massive shortage of affordable homes. Arguably the largest factors driving this housing shortage are rising construction costs, driven in part by higher labor costs, and long lead times to complete construction.

Now ask yourself: What will happen when the agriculture and construction sectors – already dealing with labor shortages – suddenly have a big piece of their workforces deported, mired in deportation proceedings, or afraid to show up to work for fear of being rounded up?

In the short run, these policies will put a gaping hole in the labor force. That in turn will lead to a sudden supply shock, as both farms and construction companies are simply unable to deliver the same amount of supply as they did before the policies went into effect. As we all know, a sudden drop in supply when demand remains constant results in higher prices.

In the medium and long term, farms and construction companies will have to replace these undocumented immigrant workers with Americans or legal immigrants. But to attract such replacements, employers will undoubtedly have to offer higher wages, which get passed onto consumers in the form of higher prices.

As Trump’s immigration policies take effect, get ready to pay more for your groceries, for a new house or a remodeling job, and for anything else that depends on undocumented immigrant labor – for instance, your hotel room, which is often cleaned by an undocumented immigrant maid. Like Trump’s tariffs, his immigration policy is significantly inflationary.

Taxes

The 2017 Tax Cuts and Jobs Act was the signature economic policy of President Trump’s first term. The act cut the corporate tax rate from 35% to 21% and reduced individual taxes in several ways as well – for instance, cutting the rate at the top bracket for individuals from 39.6% to 37%. These Trump tax cuts are set to expire this year. With President Trump’s election victory and Republican control of Congress, these tax cuts will now be extended. President Trump has also promised deeper tax cuts.

At a personal level, I couldn’t be happier about a reduction in my tax bill. I hate taxes. Who doesn’t?

But I suspect that these tax cuts will also be inflationary, albeit less pointedly than Trump’s tariffs and immigration policies.

The results of cutting taxes will be to put more money in the pockets of corporations and households. They will very likely spend that money – just as they did when the Biden administration put money in their pockets after COVID by literally mailing stimulus checks as part of the American Rescue Plan. But as that prior episode showed, putting stimulus money into pockets at the same time the Fed is cutting interest rates and the economy is growing tends to be inflationary. That is exactly what Larry Summers warned of back in 2021.

One of the things I respect about President Trump is that he does what he says he’s going to do. In that sense, his mantra – “Promises made, promises kept” – is exactly right.

But keeping his promises on tariffs, immigration, and taxes will unleash inflation at least as severe as what we saw under President Joe Biden… and, depending on how the Fed reacts, possibly even more so.

At the moment, investors seem exceptionally bullish about Trump’s presidency. Despite the S&P 500’s back-to-back advances of over 20% in 2023 and again in 2024, Wall Street prognosticators at the big investment banks are projecting another year of double-digit gains in 2025 – a streak that has happened only once before… inauspiciously, during the dot-com bubble. In the meantime, major players on Wall Street and in Silicon Valley are celebrating Trump’s victory as fantastic news.

In my view, expectations for the stock market today are much too high. I would be using this moment of extreme bullishness to take profit in your stock portfolio and to raise cash… building yourself a reserve of “dry powder” that you can tap if – as I expect – Trump’s policies lead to significant economic and investment turbulence over the coming 18 months.

At Porter & Co. we have been writing about the over-valuation of the overall market, most recently in The Big Secret on Wall Street with “The Naughty List.” While Erez also suggests it’s the right time to lighten up on your overall exposure to stocks, there’s one sector of the market (that’s not biotech!) that he feels you should be looking to add to your portfolio – as a hedge. It’s a part of the market that intrigues Erez for three reasons: it is a hedge against inflation, it’s undervalued in relative and real terms, and it’s likely to benefit from some Trump administration policies this year.

To read more about that recommendation and to get access to the full Biotech Frontiers portfolio… please call Lance James, our Director of Customer Care, at 888-610-8895, or +1 443-815-4447 internationally.

I’d love to hear what you think: [email protected]

Good investing,

Porter Stansberry

Stevenson, MD

P.S. Since the November 5 election of Donald Trump, the S&P 500 is up 3.3%. The talking heads have been – and continue to be – blathering about the “Trump trade.” However: They’re missing the best opportunities… which we uncovered thanks to Porter’s work with a long-time Trump advisor. If you’re a subscriber to The Big Secret on Wall Street, we recently sent you a report about six exceptionally promising investment opportunities that we think will explode as Trump re-assumes the presidency. If you’re not… this presentation that Porter put together will open your eyes to what may be the best way to compound your wealth over the next four years.