| Below, you’ll find the latest market update and portfolio review from Porter & Co.’s Director of Distressed Investing, Martin Fridson. We release a full report with a new recommendation on the second Thursday of each month, and an update like this one two weeks later. Marty also provides a sell recommendation and the “Top 3 Best Buys” – a regular feature that highlights what he views as the three most attractive positions to focus on in the portfolio, to help those who are new to distressed investing get started. As always, please call Lance James, our Director of Customer Care, with any questions. You can reach him and his team at 888-610-8895, or internationally at +1 443-815-4447. |

Since the Federal Open Market Committee began lowering short-term interest rates on September 18, with a second cut announced November 7, long-term interest rates have responded by going higher. Between September 17 and November 22, when short-term rates decreased 75 basis points, the 10-year Treasury yield jumped 78 basis points, from 3.62% to 4.42%.

There was nothing extraordinary about that. Measured on a month-over-month basis since 1989, 40% of the time the 10-year Treasury rate has historically moved in the opposite direction of changes in the Fed funds rate.

The only question was whether the recent rise in the Treasury yield reflected expectations of economic growth, as Federal Reserve Chairman Jerome Powell maintains… or heightened inflation fears, as many pundits argue.

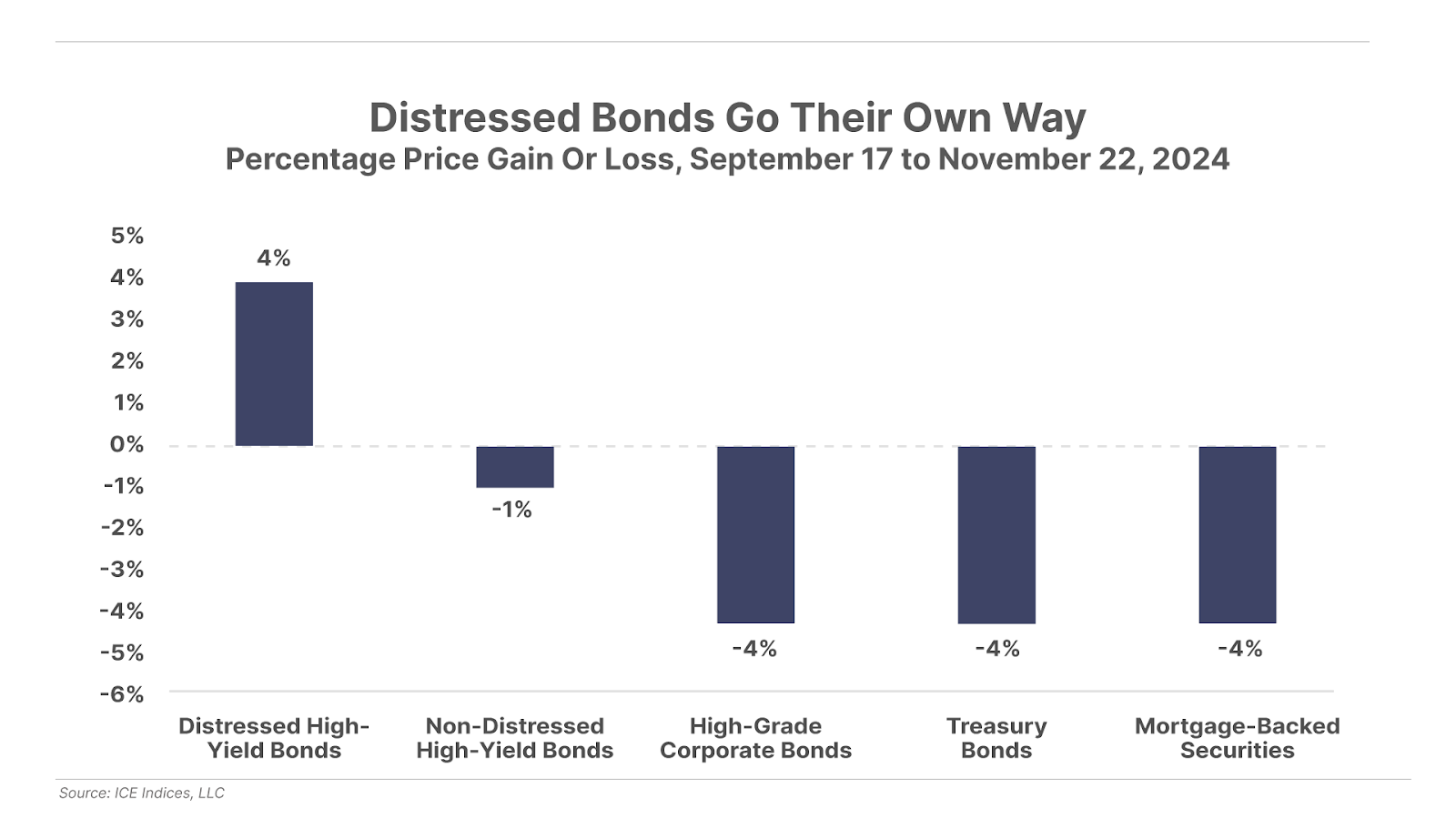

That debate overshadowed an interesting detail of the bond market’s reaction to the Fed’s action. As the Wall Street Journal frequently reminds its readers, when interest rates go up, bond prices go down. The chart below shows the performance of various segments of the bond market. Distressed bonds are those whose yields are 10 percentage points or more above the yields on default-risk-free U.S. Treasury bonds. Non-distressed bonds are those with a credit rating that is not investment grade, but that is not experiencing financial difficulties or bankruptcy. We see that most segments obeyed that rule as the benchmark 10-year Treasury yield rose. But not distressed bonds. They recorded a gain, of 4.15%.

Distressed bonds’ defiance of the downward move in bonds was no anomaly. In fact, in 55.4% of the months in which Treasury bond prices fell between January 1997 (when ICE Index Platform began tracking the data) and December 2023, distressed bond prices rose. That kind of disparity occurs in other bond categories, too, but not as frequently. For example, the comparable historical percentage for high-grade corporate bonds is just 24.1%.

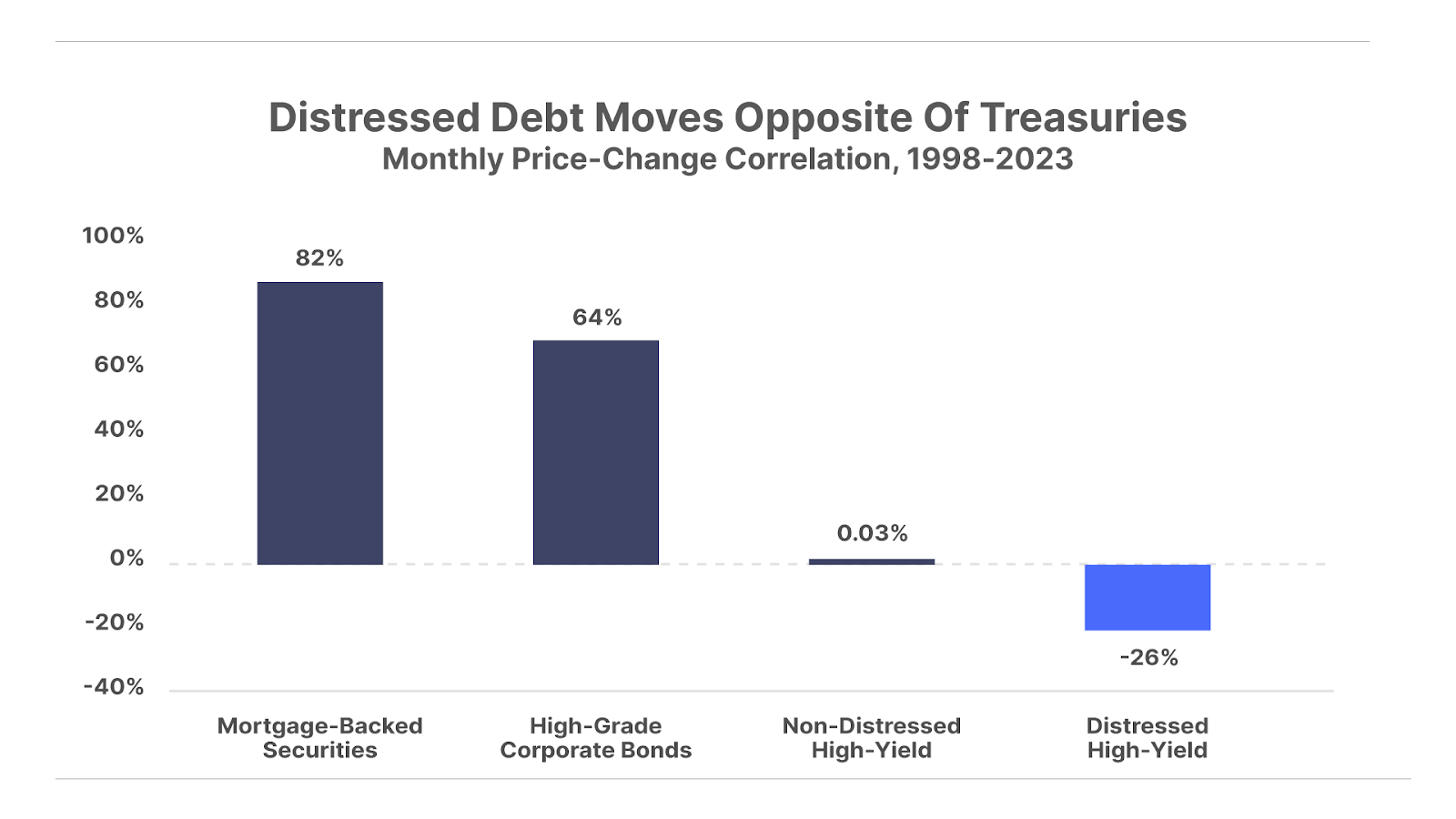

Distressed bonds’ greater independence from U.S. Treasuries, compared with other types of bonds, shows up conspicuously in the chart below. Don’t expect much of a diversification benefit from adding mortgage-backed securities or high-grade corporate bonds to a Treasury portfolio, because they typically move in the same direction. In contrast, non-distressed high-yield bonds’ correlation with Treasuries is essentially zero. And distressed high-yield bonds actually have a materially negative correlation with Treasuries. Clearly, their prices are driven by more than just fluctuations in the yields of government bonds.

The most important driver of distressed-bond price action is the performance of the economy. When gross domestic product and other key economic indicators are on the rise, the risk that these bonds will default declines. That makes investors want to own them, to capture their juicy yields. Of course, the increased demand for them pushes their prices higher.

The two-month rally in distressed bonds supports Chairman Powell’s contention that the surge in Treasury yields was a function of rising expectations for U.S. economic performance. For investors, the increase in distressed debt’s price highlights the value of diversifying your fixed-income holdings.

During economic slumps, Treasuries, high-grade corporates, and mortgage-backed securities provide downside support for portfolios that also contain stocks. But those types of bonds suffer when long-term interest rates rise. In some periods, though, the key problem that investors face is rising long-term interest rates. At such times, carefully selected positions in distressed bonds offer the possibility of achieving gains on the fixed-income side. The experience of the past two months underscores that point.

This content is only available for paid members.

If you are interested in joining Porter & Co. either click the button below now or call our Customer Care team at 888-610-8895.