Issue #142, Volume #2

The $40 Billion Per Month T-Bill Plan To Solve The “Liquidity” Crisis

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

|

The spending will never stop… Liquidity issues in the T-bill market… It’s what happened to GE in 2008… $40 billion per month… The End Of America… A small-cap breakout… Time’s Person of the Year… A sign of the top… |

We are approaching the “end game” with the U.S. government’s management of its debt load.

Federal debt is now more than $37 trillion. The interest to service that debt this year will exceed $1.2 trillion. That’s more than the U.S. defense budget. A generation ago, in 2000, the debt-to-GDP ratio was only 33%. Today it’s more than 120%. And that ignores the massive obligations of Social Security and Medicare (~$75 billion) that remain “off balance sheet,” but continue to come due, more and more, every year.

While most investors will ignore these problems, they are going to have a profound impact on our whole society, not just on your investments. It’s the government’s incessant expansion of the money supply that creates inflation, causes America’s affordability crisis, and creates the wealth inequality that’s fueling the rise of socialism.

I’ve written about these problems many times, but what happened this week is the first concrete action I’ve seen by the Fed that validates my hypothesis that we are two to three years away from a collapse in the U.S. Treasury market.

To minimize its interest expenses, the U.S. federal government has shifted the bulk of its debt into short-duration Treasury bills. A bill is an obligation that comes due in less than a year. Moving most of the outstanding debt “shorter on the curve,” lowers the government’s interest expense, because debts due in less than a year have a lower interest rate than notes or bonds with much longer durations.

But putting so much debt into short-term paper is also very dangerous. It sets up a funding tempo – vast debts must be refunded almost constantly – that frequently leads to a crisis.

This is more or less what GE did in the 2000s as it amassed an enormous $700 billion debt load. And as I warned about GE back then, when institutions have so much debt coming due every day, every week, every month, it’s only a matter of time until something goes wrong and there’s not enough time to work out a viable solution. Without the government’s bailout in 2008, GE would have gone bankrupt in less than a week.

Total government debt has doubled in the last decade and most of these additional obligations have been financed at the extremely “short” end of the Treasury market. Ten years ago, the amount of T-bills outstanding was only $1.7 trillion… or less than 10% of GDP. Today, there are $5 trillion worth of T-bills outstanding – a 194% increase and an amount of debt that’s equal to nearly 20% of GDP!

Needing to borrow vast sums constantly puts the government at risk of a funding crisis. That is, unless they turn on the printing press. And look what just happened.

The Fed announced last week that due to “liquidity” issues in the T-bill market, it would resume buying Treasury bills – roughly $40 billion per month. That means it’s going to print money to buy government debt, again. The liquidity issue the Fed is describing is far too much Treasury bill issuance and not enough buyers of the paper.

As the Fed returns to printing money to finance the government’s debt, it’s doing so at the extremely short end of the curve, which, in some ways, isn’t as inflationary as buying long-dated bonds because it won’t impact long-term interest rates. But in another way, it’s a very bad sign: banks are growing reluctant to buy government paper, even for very short durations, at the existing interest rate.

Why? Two reasons…

-

For the first time in more than 50 years, gold is now a viable alternative for global financial institutions to use as a reserve asset

-

It’s a sign that the financial markets doubt the government’s ability to successfully manage its enormous debt load

This sets the stage for the final collapse, where the Fed must continually print to refinance the debt. That starts the inflationary doom loop, where the resulting inflationary pressures cause more investors to flee the dollar, causing funding costs to rise still more… leading to more and more printing.

In this scenario, the social problems we’ve seen emerging for the last decade become vastly worse, as the affordability crisis moves from the young, who can’t afford to start a life in America, to the old, who are completely dependent on government payments, which have less and less purchasing power.

The “End of America” is not a prediction anymore.

It’s here.

Three Things To Know Before We Go…

1. A shift in market leadership. After years of underperformance, smaller and mid-sized stocks have taken the lead from their mega-cap counterparts. The small-cap Russell 2000 index (IWM) and the equal-weight S&P 500 (RSP) each broke out to new highs this week, while the top-heavy S&P 500 and Nasdaq 100 have lagged behind and struggled to make new highs. This comes at a time when earnings estimates for small and mid-size stocks are moving higher, while the earnings for the large-cap artificial-intelligence (“AI”) winners are set to decline next year. If this trend continues, 2026 could become a “stock pickers market,” where finding the hidden gems among smaller, lesser-followed stocks could be the key to outperforming the broader market.

2. The return of quantitative easing. On Wednesday, Fed Chair Jerome Powell acknowledged that payrolls have likely been overstated by roughly 60,000 jobs per month – about 35% of a typical normal jobs gain – implying that real job growth has been flat or negative for much of 2025. At the same time, the Fed cut rates and effectively ended its tightening policies, launching a $40 billion per month strategy of “Reserve Management Purchases” (which we referenced above). Liquidity has no doubt been drying up – bank reserves are at four-year lows, the repo market is flashing warning signs, and lenders are hoarding cash. But with easing now underway and the likelihood of a cut-friendly Fed chair taking over in the spring, the “permanent liquidity drain” narrative is starting to unravel. And that means one thing: dollar debasement is real, and owning hard assets like gold and silver is as critical as ever.

3. A classic “sign of the top” in AI. This week, Time magazine named “The Architects Of AI” – including Meta Platforms (META) CEO Mark Zuckerberg, Tesla (TSLA) CEO Elon Musk, Nvidia (NVDA) CEO Jensen Huang, and OpenAI CEO Sam Altman – as its 2025 Person of the Year. The Financial Times joined in by naming Huang alone as its Person of the Year. While this kind of popular consensus doesn’t necessarily mean the AI bubble has peaked, similar events – such as Amazon (AMZN) CEO Jeff Bezos winning Time’s Person of the Year in 1999 – have marked the later stages of a bull market in the past.

Tell me what you think: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland

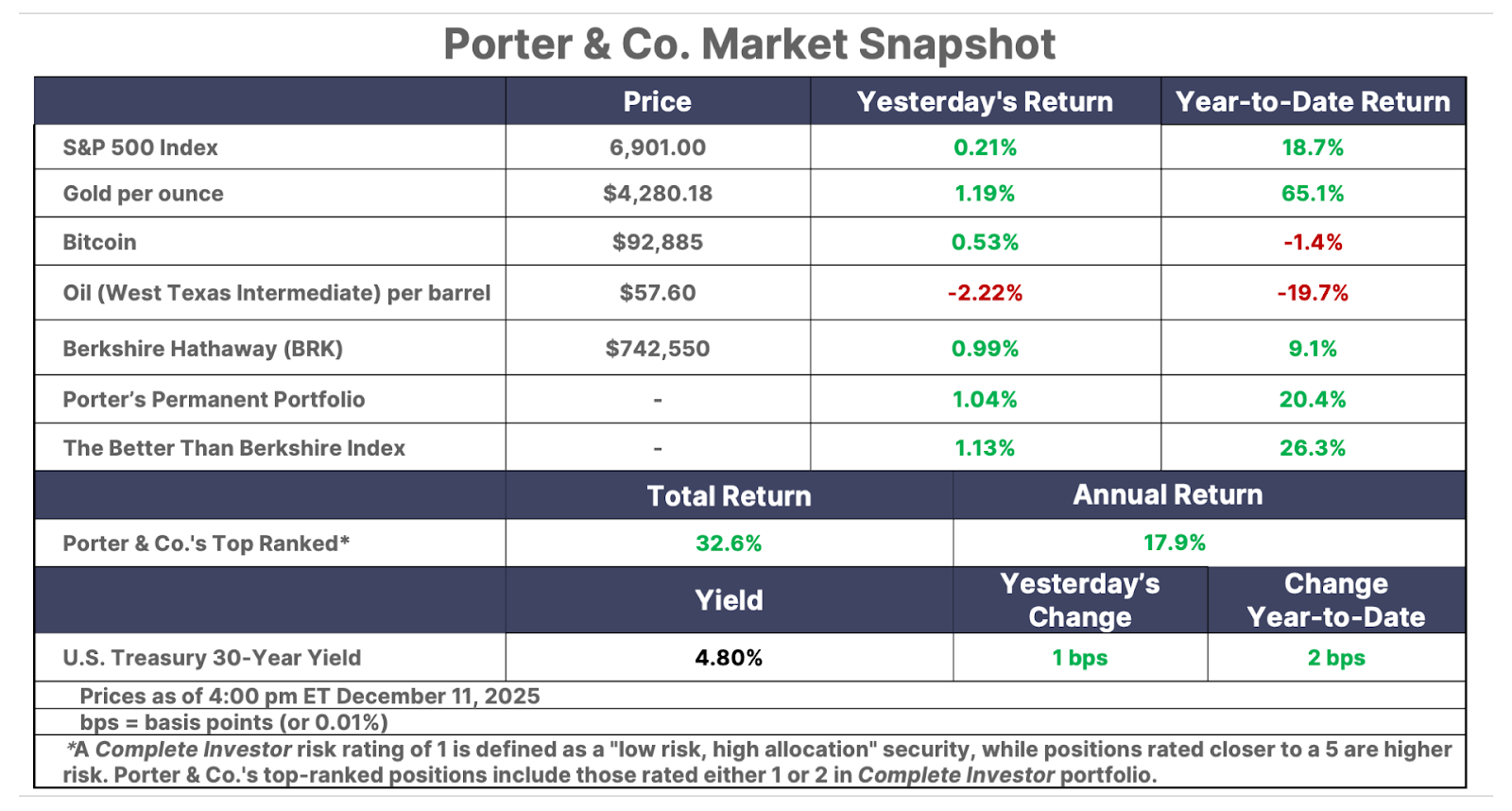

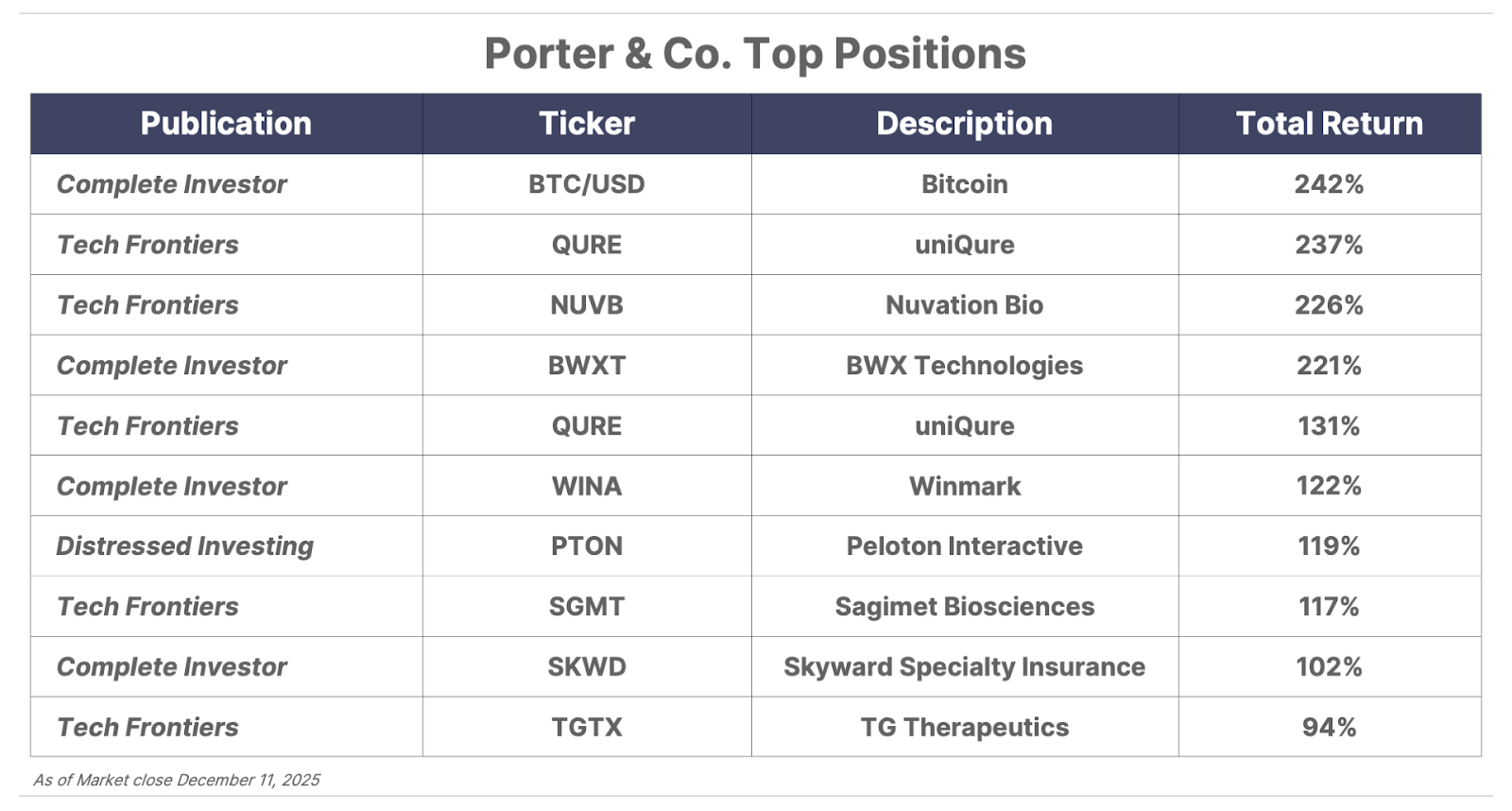

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call our Customer Care team at 888-610-8895 or internationally at +1 443-815-4447.