Issue #135, Volume #2

Here’s What No One Else Will Tell You

Plus, How To Fix It

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| Why Social Security will run out of money by 2030 … A private market alternative… Nvidia delivers another quarter of blowout earnings … More credit cockroaches … New highs in continuing jobless claims… |

I have to tell you three things most people don’t know about Social Security.

Don’t shoot the messenger. Everything in this Daily Journal is true. And I had nothing to do with it. So if these things make you angry, then let’s fix these problems before it’s too late. What can you do? Post this analysis on social media. Send a copy to your Congressmen and your Senators. Demand accountability and action.

Here’s the bad news:

#1. Your contributions don’t belong to you. There is no actual account with your name on it. All of your “contributions” were merely taxes and you have no legal right to them, at all. A 1960 Supreme Court case (Flemming v. Nestor 1960) definitely ruled, as a matter of law, that Social Security “contributions” are merely taxes.

#2. Your “contributions” were never invested. The Social Security Administration (“SSA”) never invested any of the funds. Instead, all of the money went into the government’s general fund – and was spent. The SS Trust account at the Treasury was credited for these deposits with non-marketable Treasury securities. These are government IOUs, which pay the SS Trust account an interest rate based on the average yield and duration of all outstanding Treasury debt. What’s the problem? Well, our government is bankrupt – it owes $38 trillion and can’t possibly balance its budget or even afford a real rate of interest. As a result, the real return on these IOUs is negative. That’s been the case since 2010.

#3. Social Security will collapse by 2029 or 2030. The entire system is financed as a “pay-as-you-go” redistribution scheme, aka a Ponzi scheme. And like all Ponzi financial schemes, Social Security isn’t sustainable.

In 1950, there were 16 workers supporting one beneficiary. Today, that ratio is down to 2.8 to 1.0 – if you include the 23 million government workers in America as “productive.” When you look closely at the real numbers, you discover the real ratio is about 1:1. There are only 57.6 million households in the United States that paid more than $10k in federal income taxes in 2022 (the most recent data available). Currently, 73.9 million people receive benefits from Social Security. In other words, for every American household that’s engaged in real, productive work… there’s at least 1.28 people who are mostly or fully dependent.

If that productive household is yours, nobody is going to “thank you for your service.” In fact, they are going to blame you when the system collapses. If you’ve seen people threatening to riot and steal because their SNAP benefits (food stamps) aren’t being paid because of the government shutdown, you’re getting a tiny taste of what’s going to happen when Social Security checks aren’t mailed out.

When will that happen? SSA’s Trustees predict by 2033. But I think a far more accurate forecast is by 2029 or 2030, because annual COLA adjustments will continue to increase faster than expected, thanks to rising inflation.

Social Security benefits, by law, can only be paid from the Social Security Administration Trust Fund (Section 201 of the Social Security Act (42 U.S.C. § 401). “The Commissioner of Social Security shall pay from time to time from the Trust Funds… benefits and administrative expenses… but only to the extent that such payments are made from moneys appropriated to the Trust Funds.”

When the Trust runs out of money, payments automatically drop to match incoming revenue, which means payments will be automatically cut. That won’t be a good day for our country.

Social Security is, without question, the worst thing that’s ever happened to our country.

Since 1935, people (and their employers) have been forced to pay 13% of their wages into a system that’s systematically destroyed these capital investments. Why? In 1971, Nixon defaulted on government bonds (and on Social Security) by removing the link between our dollar and gold. That’s when the real returns on Social Security’s government IOUs began to decline and, eventually, became negative in 2010.

Let me show you what that’s cost us…

If, instead of holding worthless government IOUs, SSA put Social Security’s reserve ($40B in 1971) and all additional net contributions into the S&P 500, and nothing else about SS changed (payout ratios remained the same) the Social Security Trust Funds would have $50 trillion in them today, not $2.4 trillion (18x more). Meanwhile, today, because of the abysmal real returns from holding government IOUs, the average annual SS payout is only $24,100, with an estimated total payout (over 20 years) of $482,000. If the SSA had invested in stocks (S&P 500) instead of government bonds and if payout ratios were maintained as they are now, the average payout would be $442,300 per year, with an estimated lifetime value of $8.84 million. Social Security would, all by itself, provide retirees with a luxury retirement.

But that didn’t happen. And it still isn’t happening. As a result, the real-world value of SS payments are in terminal decline. If you measure the value of the average payout in U.S. Gold Eagle coins, this devastating reality becomes crystal clear.

In 2001, the value of the average SS payout ($10,493) was worth 38 gold eagles.

In 2011, just after the financial crisis, the average payout increased substantially, in nominal terms, by about 40%, to $14,743. That sounds pretty good… except by then, SS’s average payout had fallen dramatically in real money. That year’s payout would only buy 10 gold eagles, a decline in real terms of nearly 75%.

And, after the COVID bailouts, the situation got even worse. By 2025, the average payout was $24k, up 63% in dollar terms. But that only bought six gold eagles, a further decline in real terms of 40%.

Every dollar you’re paying into the current system is, like all taxes, being destroyed and wasted by the government. That might be necessary or worth it when it comes to national security, highways, and other critical shared resources. But it’s not necessary when it comes to our retirement accounts.

First of all, like all government programs, the Social Security Administration is vastly too expensive ($14.2 billion a year in overhead) to administer. That’s as much as Goldman Sachs, Morgan Stanley, and Bank of America each spend on their investment banking staffs. I hope it’s obvious to you that the SSA staff are not the same caliber of people Goldman hires. And they don’t need to be because SSA is only allowed to invest in worthless government IOUs.

If we don’t fix Social Security in the next five years, it is going to wipe out an entire generation of Americans – Gen X. And there will be nothing left for millennials or Gen Z either.

The solution is utterly simple: take the SSA out of the government’s hands. Pay a private sector institution, with legal fiduciary obligations, $2 million to $3 billion to administer a federally mandated retirement system that is privately owned (your actual property) and governed by a familiar set of rules. You and your employer would both be required to contribute (tax free) at a minimum rate of 6.5% a year. And you’d have to invest, for the long term, into one of a few high quality, broadly diversified index funds (S&P 500, Nasdaq 100, etc.) As you get older (i.e., above 50) you could also own short-dated corporate investment grade bonds, so that you’re not gambling your retirement on the stock market without enough time to mitigate the risk.

Folks with less than 20 years remaining until retirement age would have the option of keeping the current system (bad idea) or opting into the new system. And, to ease the risk of the transition, the government could guarantee 80% of the value of the current system, so you wouldn’t have to bear the full burden of the risks. Nothing about current recipients would change.

The government’s solution will, undoubtedly, be to raise the amount of Social Security’s payroll taxes. In other words, throwing even more capital into the inferno. Don’t let them. Require any increase in funding to be predicated on privatizing the system and making sure that your contributions are your private property.

We must stop pretending that the government is the answer. It’s not. It’s the problem.

P.S. Whether or not the government gets out of the retirement business, a great solution to protect yourself from the coming great inflation is to consider Rick Rule’s new product. Rick is an old friend of mine, one of my best mentors. He’s also the “axe” in resource investing, which can offer wonderful leverage against the impact of inflation. That’s extremely important when you’re retired and most fixed-income coupons won’t keep pace with inflation. Click here to access Rick’s new product.

Rick Rule’s NEXT 1,000X Trade?

Presented by Digest Publishing

While helping build a $50 BILLION empire, market wizard Rick Rule made not one but TWO famous 1,000X trades. Now, he just went live with a special mystery guest to reveal how an exciting “about-face” from Washington could potentially hand you the biggest stock wins of your lifetime.

Click here for the full story (and a free stock recommendation).

Three Things To Know Before We Go…

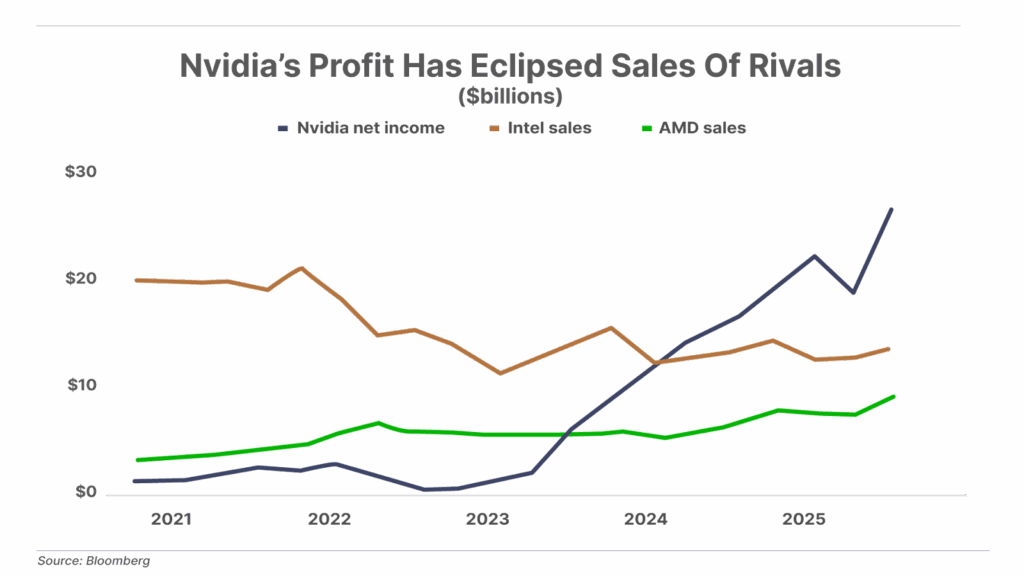

1. Nvidia reports blowout Q3 earnings. Nvidia (NVDA) delivered another massive quarter, with Q3 revenue surging 62% year-over-year to $57 billion, beating expectations, and guiding Q4 revenue to $65 billion versus the $62 billion consensus. CEO Jensen Huang dismissed AI bubble concerns, saying the company sees “something very different,” indicating that hyperscaler spending will continue to ramp up through 2026. Nvidia also previewed its upcoming DGX Spark “personal supercomputer,” part of a broader push to bring data-center-class AI performance directly to developers and consumers – potentially opening an entirely new leg of growth beyond enterprise infrastructure. Nvidia remains the clear winner – and choke point – of the parallel-processing revolution, and is on pace to generate more annual net income than Intel and AMD’s combined revenue.

2. More “cockroaches” are crawling out of private credit. One of BlackRock’s private credit portfolios performed so poorly that the firm was forced to waive management fees just to keep the deal afloat. In October, the portfolio’s collateralized loan obligation (“CLO”) holdings fell so sharply that the value of the underlying loans dropped below the amount owed to the highest-rated tranches of the bonds – a big red flag in structured credit. Even more alarming was that one of the underlying loans was marked at 100% last month, only to go bankrupt this month – prompting BlackRock to mark it down to zero. To fix the imbalance and bring the deal back into compliance, BlackRock waived fees linked to the riskiest tranches, effectively absorbing part of the pain itself. That move helped restore the structure to good standing – but when there’s one cockroach, it usually isn’t the last.

3. Jobless claims hit a new four-year high. Labor market data is back with the federal government reopened for business. The latest jobless numbers revealed that continuing claims for unemployment insurance jumped to 1.97 million in mid-November. That marks the highest rate since November 2021. While new jobless claims remain subdued for now, the rise in continuing claims show that those who lose their jobs are having trouble getting rehired again. The weak pace of hiring also contributed to an uptick in the unemployment rate for September, which reached 4.4% – also the highest level since November 2021. The U.S. labor market remains stuck in a “slow to fire, slow to hire” dynamic.

Tell us what you think of today’s Daily Journal or anything else that is on your mind: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call our Customer Care team at 888-610-8895 or internationally at +1 443-815-4447.