Issue #126, Volume #2

Fraud, Credit Collapse Signal Coming Market Collapse

Critical Market Update: The Rarest And Most Dangerous Economic Anomaly Is Occurring

We’re seeing credit stress in cohorts that still have jobs. That’s new. Usually, you lose the job first.”

– JPMorgan Chase (JPM) 3Q earnings call

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| A “shorting” environment… The credit market is cracking… Defaults before job losses… Big fraud at big firms… Big news for The Big Secret… Hershey announces earnings… Big Tech starts to borrow… |

On Wednesday, I made $82,900 in a single trade, in about three days.

It wasn’t my best trade of the year. But it was the only major short trade I’ve made in the last 10 years.

I put over $1 million short a single stock. That is, I bet more than $1 million that the share price of a business would fall. As you might imagine, I didn’t take the position lightly. I knew the company was about to collapse.

I virtually never short stocks. That’s because, in an inflationary, paper-money economy, the nominal prices of just about everything always goes up. And you can only make money shorting stocks when nominal prices go down.

However, there is one kind of an economic environment that will cause plummeting nominal prices – especially in financial assets. Inflationary environments sometimes lead to sudden, deflationary crashes. They are rare. And they are caused by fraud.

And that’s what’s happening right now.

What happens next will happen very fast. This is something I’ve only seen once before in my career – in the days leading up to the collapse of Fannie Mae and Freddie Mac.

You may remember in May 2008 – about four months before their collapse – I wrote the most definitive and critical warning about the coming mortgage crisis. I explained, in precise detail, that the two largest and most important financial institutions in the entire world were “zeros” – that their share prices were going to zero – because they were hiding losses of more than $250 billion.

In the months that followed, the Secretary of the Treasury of the United States insisted, before Congress, that the firms were “well capitalized.”

He was lying.

Within 90 days, both businesses collapsed, triggering the worst global economic crisis of the last 50 years.

I am urging you to read the following carefully.

The same economic scenario that led to that disaster is occurring today. This is an extremely rare situation. This will have a long-lasting and catastrophic impact on the financial markets.

Let’s start here, with my trade from this week.

I borrowed and then sold in the market (“selling short”) shares of America’s leading subprime retailer of used automobiles, Carvana (Nasdaq: CVNA).

When I borrowed the stock, it was trading for around $350 per share. The stock has been one of the strongest performers of this bull market, rising from under $5 per share in 2022 to almost $400 last month. And it was scheduled to report earnings after the market close on Wednesday.

I’ve been closely following all the credit market news over the last few days. There’s a disaster unfolding:

- Tricolor Holdings, which like Carvana is a subprime auto lender, filed bankruptcy in September. The bankruptcy trustee’s lawyer (from Akin Gump Strauss Hauer & Feld) described Tricolor as a “pervasive fraud” of “extraordinary proportion.” It was double pledging the same cars as collateral to multiple lenders and publishing fake loan-performance data. Tricolor specialized in subprime loans to “overlooked communities,” explicitly marketing to undocumented immigrants. As a result, JPMorgan – the highest-reputated bank in the world – wrote off $170 million in losses and Fifth Third bank wrote off $200 million. This is DEI finance – and it’s corrupted the entire financial system.

- First Brands, an auto parts supplier, filed for bankruptcy next – and once again, a huge fraud was exposed. This company, spun out of Dow Jones component Honeywell International (HON), is one of the country’s most important auto-parts makers. Suspiciously, First Brands’ revenue doubled between 2022 and 2024. And now creditors allege $2.3 billion has “simply vanished.” The U.S. Department of Justice is investigating. This led to major losses at two investment banks, Jefferies Group (JEF) and UBS (UBS). The losses are massive and only a 20% to 30% recovery is expected. The company’s senior bonds are trading at 15 cents on the dollar.

- And the latest “cockroach” in the credit markets… an Indian-origin CEO Bankim Brahmbhatt fabricated accounts receivable to collateralize $500 million in fraudulent loans for his telecom firms Broadband Telecom and Bridgevoice. These businesses claimed to handle receivables for giants like T-Mobile, Telstra, and Telecom Italia Sparkle – totaling hundreds of millions in “projected revenue.” But it was all a “breathtaking fraud.” Brahmbhatt forged client lists, contracts, and email trails. Some “clients” denied any relationship with his businesses at all, calling it “clear fraud.” Court documents in the case describe “fake contracts, fake emails, fake clients” across multiple countries. And the creditors involved are some of the most sophisticated in the world: BlackRock’s HPS Investment Partners (a $150 billion private-credit lender) provided the capital and major French investment bank BNP Paribas structured the deals.

I believed that Carvana, long one of the fastest-growing and most aggressive subprime auto lenders, would inevitably be caught in the credit-market mess. And, at first, it looked like I was dead wrong and about to take a huge loss.

When the company reported earnings on Wednesday, the results were some of the strongest I’d ever seen in my career: revenue was up 55% year over year – stunning growth for a business of this size, with both prices and unit volume (+44%) growing.

The company far surpassed its guidance, with earnings per share (“EPS”) of $1.03 versus the $0.85 forecast. The stock should have been up – a lot. Maybe by 20%.

But instead, it cratered.

Carvana’s stock tanked 13.8% yesterday, October 30, closing at $305.07 (from $354 the prior day). This erased about $6 billion in market cap in a single trading day, the biggest single day drop since 2022.

And you must understand why.

Carvana’s business, like so many consumer businesses, hinges on financing.

Carvana provides credit to virtually all its customers. And the money for these loans comes ultimately from investors. Carvana is well-known to be the most aggressive provider of subprime auto loans, with almost half of the cars it sells going to customers who have poor credit histories (FICO scores under 600).

All this subprime lending fueled an enormous 2025 expansion, with almost $2.5 billion in new lending in the first half of 2025. Carvana packages these loans into big securities and sells them to investors. Or, at least, it used to. In Q3, Carvana originated $1.98 billion in loans, but instead of securitizing them and selling them to investors, it sold almost all of these loans ($1.5 billion) directly to other banks. And, as you’d imagine, that’s not nearly as profitable as selling directly to investors.

This suggests that a major source of funding – securitization – is closed. Suddenly investors are demanding a huge increase in the “credit enhancements” on these securitizations. That means, Carvana was going to have to pay at least another $100 million a year in funding costs if it wanted to continue to access the credit markets directly. Why? Because Carvana’s 60-day delinquency rate on its loans is already 4x higher than its peers.

And these same kinds of changes – investors withdrawing from the credit markets – are happening across our entire economy right now.

That’s extremely unusual, because we haven’t – yet – seen any major uptick to unemployment. Normally, these kinds of credit problems only occur after a big recession. People lose their jobs, which causes them to default.

But sometimes – very rarely – there’s so much credit being created, and so much of it is fraudulent, that the “weight” of these bad debts leads to cascading defaults ahead of a recession.

In these rare cases, it’s all the bad debt itself that causes the recession, not the other way around.

That’s exactly what we saw in 2008: the enormous amount of fraudulent subprime mortgage loans led to cascading defaults that destroyed the entire world’s financial system.

Obviously, these kinds of credit problems – when defaults occur before recessions – are far more dangerous to the financial markets.

And that’s exactly what’s happening right now. Why? Well, it’s simple. We’re broke.

Americans have seen their real, after-tax wages decline consistently for decades, because of inflation and the soaring costs of taxes and healthcare. Real wages down another 2.5% over the last three years. And our savings rate (3.2%) is the lowest since 2008. Nobody is saving, in part because no one under 50 can afford to buy a house.

Americans are more tapped out than they have ever been in history: Currently the household debt-to-income level in the U.S. is 124% – that’s the highest ever.

And does this sound familiar? Currently one-in-three new auto loans is subprime, with most loans made at 120% loan to value. As subprime mortgage lending reached about 40% of all new home mortgages in 2006, the entire housing market broke. Those enormous losses took the entire financial system down with it.

And that’s exactly what’s happening again right now, but this time the losses are stemming from subprime auto loans.

Today, AAA-rated auto asset-backed securities (“ABS”) – which are rated “as good as gold” by the ratings agencies – are trading at 180 basis points over U.S. Treasuries of similar duration. That is up from a spread of only 40 basis points a year ago.

That reveals a huge rise in funding costs for auto loans.

And that’s never happened before a rise in unemployment. Not ever.

That means, if you’re trying to sell cars and provide the financing, you’re going to have to pay a lot more for the money. Obviously, that means the customers are going to have to pay a lot more too – and they can’t afford it.

That starts the default cycle. And you know what comes next: rising delinquencies and falling collateral values. Bigger and bigger losses. Higher funding costs… etc.

While the problems are centered in auto lending, the pain is across the entire consumer landscape.

- Subprime auto delinquency (60+ days) is now at 6.43% of all outstanding loans (up 52% this year). That’s a record high, greater than the 2008 previous peak.

- Auto repos: 15-year high, on the way toward an all-time high. Hasn’t happened yet only because there’s a huge amount of fraud in the system. Called “loan modifications,” lenders do everything possible to avoid a technical default, even when it means taking a loss on the loan.

- The 90-day-plus credit card delinquency rate is 12.27% (up 22% this year), highest rate since tracking began.

- Private credit defaults: 2.4% and rising, with notable flagrant frauds emerging week after week.

Again, it is highly unusual – and a deadly serious red-flag leading indicator – for consumer credit to “roll over” (delinquencies/defaults rising sharply) before any meaningful rise in unemployment.

Historically, labor-market weakness drives credit deterioration, not the other way around.

When the reverse happens, it often signals very serious problems with the underlying economy and causes severe recessions.

It’s only happened twice before. It happened during the late 1980s savings-and-loan (S&L) crisis, which was triggered by early tax reforms that made commercial real estate lending much more expensive – a kind of fluke occurrence. And it happened most notably in the 2007-2008 Global Financial Crisis.

I think we’re seeing it again because so much of our economy since 2015 has been built on massive credit expansion. Federal debt has doubled, from $18 trillion to $36 trillion. Corporate debt has grown 65% – from $13.3 trillion to $21.9 trillion. And consumer debt is up 50%, from $13.9 trillion to $20.5 trillion.

Credit growth has also fueled inflation and the soaring price of gold and crypto.

Most people believe that the soaring gold price is a harbinger of inflation, but that’s false. A soaring gold price is a harbinger of soaring credit defaults. The last time gold went up like we’ve seen this year (up 54%) was during the big run-up between 2004 and 2008. What happened next?

We’re entering a very dangerous period in the markets.

I want to do everything I can to help protect you – and even grow your wealth. That’s exactly what I’m doing with my own money. My family office is having its best year ever. We’re up about 80% on the year. We follow the same kind of strategy we use for Porter’s Permanent Portfolio, plus we add “alpha” – extra performance – through using leverage and by selling options.

And now, for the first time in more than a decade, as I mentioned above, I am adding “short” positions: bets that individual securities will decline in price.

Since I launched Porter & Co. in the fall of 2022, my singular goal has been to provide the highest-quality financial information in the world, bar none. I won’t bother going over all of the details with you, but I can tell you there’s no finer source of investment research available anywhere for investors who are interested in safe investments. Just look at the score board at the bottom of the page.

Porter’s Permanent Portfolio is beating the market (up 25% this year) with half the market’s volatility. Our Better Than Berkshire Index is trouncing Berkshire Hathaway (BRK). Our ultra-safe property and casualty insurance companies are having a down year (because interest rates are falling), but they’ve produced about 3x the market’s return, on average, since 2022. I’m certain there’s no finer research available anywhere, at any price, for investors who want to remain in the market but who do not want to take big risks.

And guess what? I’ve added all of those extra features to our existing newsletter, for free.

Today, I’m adding a critical new feature to The Big Secret On Wall Street, my paid-subscription newsletter.

It’s a new “short” portfolio: made up of companies whose share prices we expect to collapse in the ongoing credit-market implosion. While shorting stocks is usually a very tough way to make money, I have a legendary career in that style of investing. I’ve predicted many major bankruptcies and accounting scandals (Fannie, Freddie, GM, GE, several airlines, etc). And whether you decide to actually trade my short recommendations or not, knowing about these problems, so you can avoid all of the businesses in these industries, is worth more than the total cost of the newsletter.

With this major expansion of our coverage, I’m going to increase the annual price of my newsletter from $1,425 to $1,999. This is our first price increase ever.

And… I’m also changing the name of my newsletter. With all of the new indexes and portfolios, and especially now that I’m building a short portfolio, my newsletter is the single most complete advisory that’s available, anywhere, at any price.

I’m going to call it Porter Stansberry’s Complete Investor.

If you haven’t ever subscribed before, or if you want to lock in the previous lower price forever, I’d urge you to subscribe now, renew now, or, best of all, sign up via our membership offer to lock in the previous low price, forever.

Until Thanksgiving, we are willing to honor our first-time subscriber, introductory price of $1,000 for a full year’s subscription.

We will also allow anyone who wants to renew early access to that discounted price – only $1,000.

But after Thanksgiving we will no longer offer discounted renewal subscriptions. So please… consider acting now.

All subscribers will receive my new short portfolio over Thanksgiving weekend.

I’ve got a lot of work to do over the next three weeks to make sure it’s exactly what you need to protect your wealth from this debt debacle.

And, listen. It doesn’t please me to have to do this work. The coming consumer credit crisis isn’t going to be good for people or our country. It isn’t going to make our politics any less volatile or radical. It’s going to make a lot of things much worse. We continue along the path toward civil war.

I can’t stop what I call “the end of America.” But I can help protect you and your family. I hope you’ll let me.

Whatever you do, please do not ignore this warning.

I am not wrong.

Take advantage of this offer now.

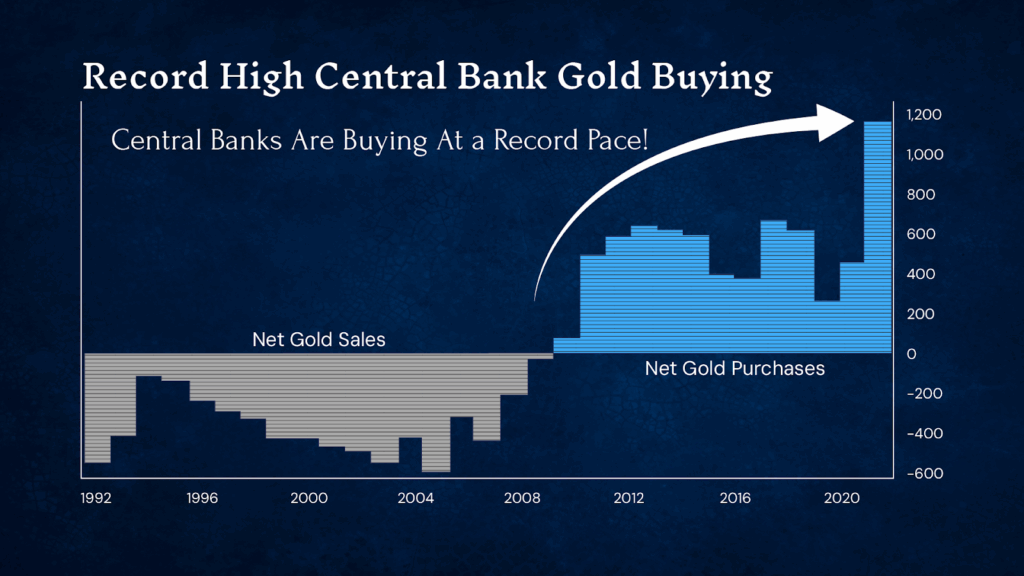

Gold Dethrones the Euro… Is the dollar next?

Gold recently surpassed the Euro to become the world’s #2 reserve asset. Central banks are buying record amounts — and yet, gold miners are still dirt cheap.

This is your chance to ride gold’s return to the monetary system – and make a potential generational fortune.

Go here for details on Garrett’s top 30 miners, already handing investors gains of 441%, 446%, 618%, 784% and more since January 2024.

Three Things To Know Before We Go…

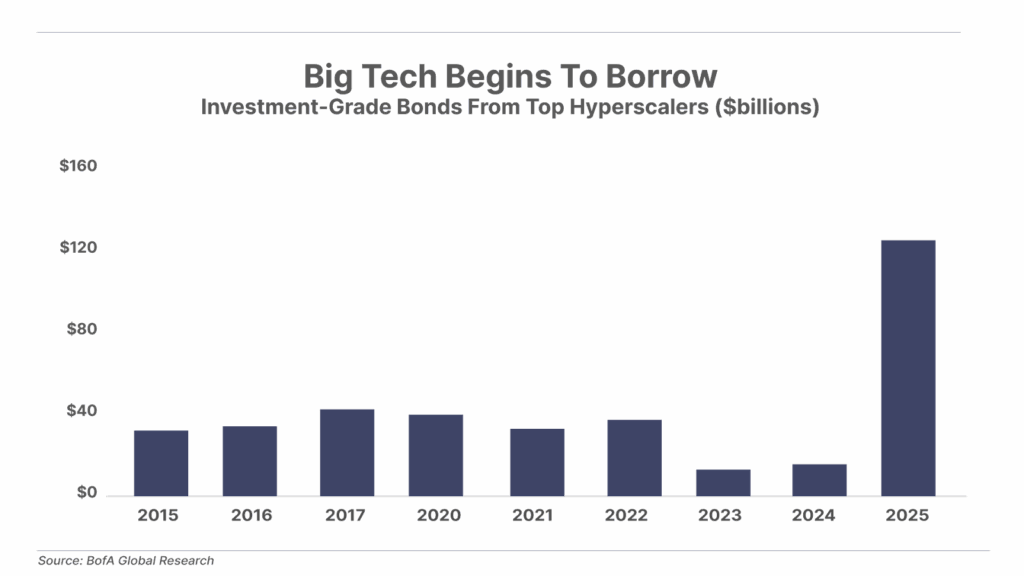

1. Firms are now borrowing to fund artificial intelligence (“AI”) data-center spending. Most of the AI data-center buildout to date has been funded by Big Tech hyperscaler cash flows. However, that is now changing… As the chart below highlights, there has been a sharp increase in borrowing from a handful of these firms over the past couple of months.

2. More job cuts are piling up. Amazon just announced plans to eliminate 30,000 jobs, Accenture is laying off 11,000, and Target is cutting another 1,000. Add to that EV car maker Rivian, Meta, semiconductor supplier Applied Materials, NBC News, and countless others. Whether driven by AI adoption or softening demand, the tide has clearly turned. With tens of thousands of jobs disappearing, the impact will inevitably surface in the broader economy as consumer spending slows.

3. Hershey’s profit margins and pricing power in recovery. The Hershey Company (NYSE: HSY) beat expectations in its Q3 earnings report yesterday, with EPS of $1.30 ($0.24 ahead of expectations) and revenue of $3.18 billion ($60 million better than analyst estimates). The key takeaway: Hershey has regained its pricing power, with a 6% increase in prices while volumes remained steady. This bodes well for 2026, when the company will benefit from higher selling prices and lower cocoa prices, which have fallen by over 50% so far this year. Returning to profit margins of 15% to 20% would put Hershey’s net income in a range of $1.8 billion – $2.4 billion. At a current market capitalization of $35 billion, this implies Hershey trades at a forward P/E ratio of between 15x and 19x – a compelling bargain for one of the most iconic brands of all time.

And One More Thing… Poll Results

In Wednesday’s Daily Journal, we reported that the hyperscalers – the Big Tech companies investing heavily in artificial-intelligence (“AI”) infrastructure – had dramatically increased their capex spending over the last year… So we asked: Will these data-center investments ultimately deliver sufficient returns on investment, or will the AI buildout turn into a great big misallocation of capital?

The answer from readers is a mixed bag, with 63% of survey takers selecting “some winners, many losers,” while 21% say it’s “overbuilt and overhyped,” and the rest split between the options of “transformative profits ahead” and “too soon to tell.”

Tell me what you think of today’s Daily Journal or anything else that is on your mind: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call our Customer Care team at 888-610-8895 or internationally at +1 443-815-4447.