Issue #117, Volume #2

You Just Need To Look… And Then Unlock It

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| Supply the U.S. with energy… Out with the old, in with the new… Heading to Asia to find bargains… It burns its coins… A 400-year-old Japanese conglomerate… Setback for Venture Global… Oil is getting really cheap… |

If you could buy something for 20 cents that would eventually be worth $1, you would do that all day long…

Of course, most of you don’t believe that’s possible… these incredible opportunities disappeared in the bull markets of the past. But over the last few weeks, Porter has shown how investors can make enormous, life-changing profits in stocks that are (almost) sure things.

He started with the story of the Philadelphia & Reading Railroad (“P&R”). For much of the 1800s, until the early 1900s, this railroad and coal producer would become the most valuable economic engine in the country – hauling its anthracite coal around the growing United States.

Anthracite – a hard, clean-burning coal – powered the nation’s energy revolution in the 19th century. At one point, the railroad supplied nearly 20% of all U.S. energy.

But debt and success did it in. By the early 1900s, the company had outstanding bonds totaling $135 million – that’d be about $5 billion today – and its dominance attracted anti-trust actions. Meanwhile, coal’s energy dominance faded as cheaper alternatives emerged.

In 1954, it had a $19 million market cap – but it had millions in locked-up capital. Warren Buffett’s mentor Ben Graham bought 5% of the company, became its chairman, and installed a savvy CEO. Buffett made the stock his largest holding, buying in under $10 a share.

They renamed it the Philadelphia & Reading Corporation and liquidated excess inventory, generating $7.3 million in tax losses. These tax-loss carryforwards and the cash these sales generated funded diversification – Union Underwear in 1955 and Acme Boots the next year… clothing firms, toys, and eventually Fruit of the Loom in 1961.

Over 13 years, management extracted almost $400 million in value from P&R. But there was no guessing. The capital was in the business all along. They just had to get it out. And they did for a gain of 2,000%

Buffett has used this model to turn Berkshire Hathaway into the nearly $1 trillion conglomerate it is today. And it is the same blueprint he is following again with his recent massive investments into several Japanese trading firms…

Opportunities to buy $1s for 20 cents are rare. But they do exist. And right now they mostly exist in Asia.

Huge Korean conglomerates are going through this same evolution as Buffett and Graham – divesting non-core units amid massive economic transformation.

Porter read about one of these in Grant’s Interest Rate Observer about a year ago.

SK Square (402340 on the Korea exchange) is part of South Korea’s second-largest conglomerate. After its chairman went to jail for embezzlement, its stock plummeted… shares traded for less than the company’s book value.

One asset on the company’s books is SK hynix, the market leader in the kind of data-storage chips that data centers need to fuel their massive parallel processors.

Since Grant’s published this report, the stock has doubled. The rise was inevitable – the value was already in the business. The discount had to melt away… and it did.

Porter went on to share another example that he and Tech Frontiers editor Erez Kalir have reported on. He wrote:

Launched in 2012 by Ripple Labs, Ripple is a system built to facilitate virtually instant, secure interbank transfers. At the core of the system is the XRP Ledger, which is a decentralized, open source, blockchain. It can handle enormous transaction loads (1,500 transactions per second), offering virtually free settlement in three to five seconds. This is comparable to Visa’s network, which is considered the world’s best proprietary payments network. And compared to the existing SWIFT network, Ripple is a miracle.”

Ripple’s token, XRP, is the future of how payments will be made. JPMorgan, PNC Bank, MoneyGram already use it in the U.S.

But for investors, XRP holds another advantage. Unlike Bitcoin, whose coin count will grow, all of the XRP that will ever be created has already been mined – and there will be fewer of them as things progress. Tokens are “burned” as they get used – the XRP Ledger incurs a teeny tiny base fee, which are automatically destroyed. Thus, over time, the total supply of Ripple’s XRP token will decline, creating more value for the token holders.

As supply shrinks, each remaining XRP captures more value. Porter explained:

Unlike inflationary tokens, XRP aligns incentives: users pay for efficiency, holders gain scarcity.”

And guess who owns the largest stash of Ripple tokens in the world? A forgotten Japanese financial conglomerate called SBI Holdings (TSE: 8473), a $14 billion financial holding company… it’s hiding a crypto war chest worth multiples of its market cap. SBI isn’t a bet on ifs. It’s $1 for 20 cents. (It’s up 80% since Erez recommended it in Tech Frontiers in February.)

Then yesterday, Porter reported on another Japanese holding company for paid-up subscribers of The Big Secret On Wall Street. But it isn’t a normal holding company. The 400-year-old business is part of Japan’s strategic plan to acquire and retain critical energy, metals, and food. And because of its place in Japanese society, it is granted capital at remarkably low rates. As a result, it is the world’s most formidable, long-term investor.

It invests like Buffett, except instead of insurance-company float, it uses cheap government and bank money. That’s its secret sauce. Often backed by Japan’s government financial institutions, the company captures high returns on invested capital (“ROIC”) with minimal overhead. Its ROIC averages 12% to 15%, far above global conglomerates like General Electric, who generate ROIC around 8% to 10%, because they avoid heavy operational burdens by holding minority equity positions.

As global investors flee fiat currencies – seeking refuge in gold, Bitcoin, or real estate – the value of this Japanese conglomerate is poised to soar. As Porter explained:

This is not mere speculation. It is the timeless mechanism by which the intellectual elite of business preserve and multiply wealth, a strategy Buffett has championed throughout his career.”

And if you are not a paid-up subscriber and you want access to the amazing story that Porter told about this Japanese company in yesterday’s Big Secret, click here now to join.

Trump to Open ‘Phase II’ Of The American Birthright?

President Trump has made a move to permanently open the floodgates of America’s mineral dominance, unleashing Phase II of the American Birthright.

Historically, Phase II has been the most lucrative investing window across resource booms. The last time this happened, investors could’ve seen rare peak returns of 7,500%… 20,183%…even 140,000% in the span of 3 years.

Trump is just days away from opening a new Phase II window. To know exactly what to do, get the complete Phase II strategy immediately HERE.

Three Things To Know Before We Go…

1. Venture Global suffers legal setback. Shares of liquefied natural gas (“LNG”) exporter Venture Global (NYSE: VG) fell 20% today on the news of an adverse ruling in its arbitration case against BP. The oil giant accused Venture of failing to supply it with contracted LNG cargoes in 2022 in order to sell its LNG into the higher-priced spot market, when global prices rose following Russia’s invasion of Ukraine. The final damages have not yet been awarded, but analysts estimate they could exceed $1 billion, causing a selloff of Venture shares. Despite this setback, Venture’s business, which Porter wrote about in an early-summer Daily Journal, and long-term prospects remain bright. And notably, Venture’s current supply agreements with BP remain unchanged, with Venture continuing to supply BP with LNG.

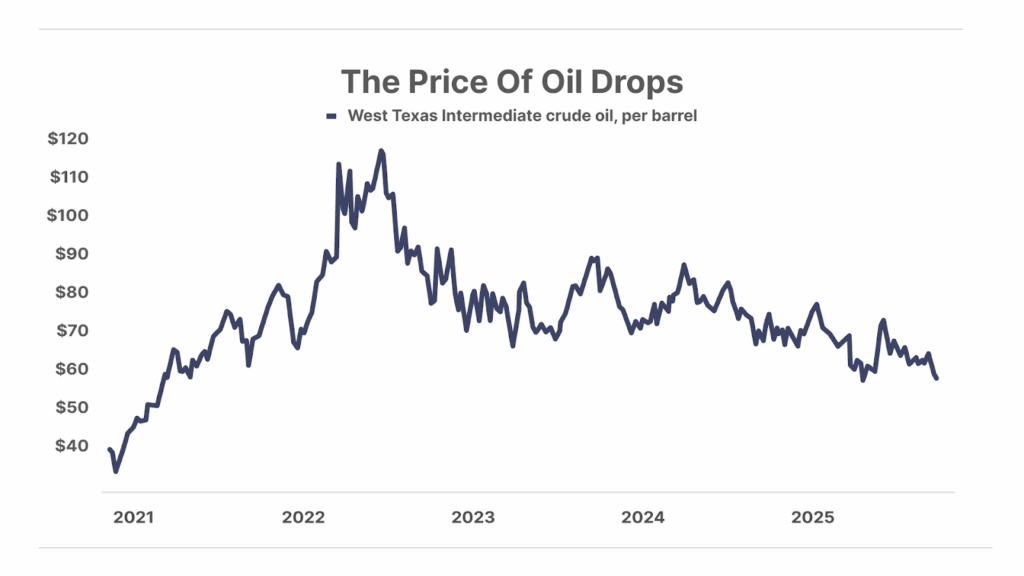

2. Trump is getting his wish on oil prices… for now. West Texas Intermediate (“WTI”) crude oil – the U.S. pricing benchmark – fell below $60 per barrel today, its lowest level in over four years (outside of a brief period following President Trump’s April 2 tariff announcement). This week’s decline follows news of yet another OPEC+ production hike, a tentative peace deal between Israel and Hamas, and Trump threatening another “massive” tariff hike on Chinese imports this morning. Pushing energy prices lower was a key focus of the president’s campaign. Yet despite promises that America would “drill, baby, drill” to reduce prices, oil has been falling without the help of U.S. producers. According to the Federal Reserve Bank of Dallas, U.S. oil and gas production has fallen over the past two quarters as lower prices have made things uneconomical for many producers. While falling energy prices is great news for consumers, low prices are likely to cause a significant decline in U.S. output as weaker producers are shuttered… which would set the stage for significantly higher prices when OPEC+ eventually reverses course.

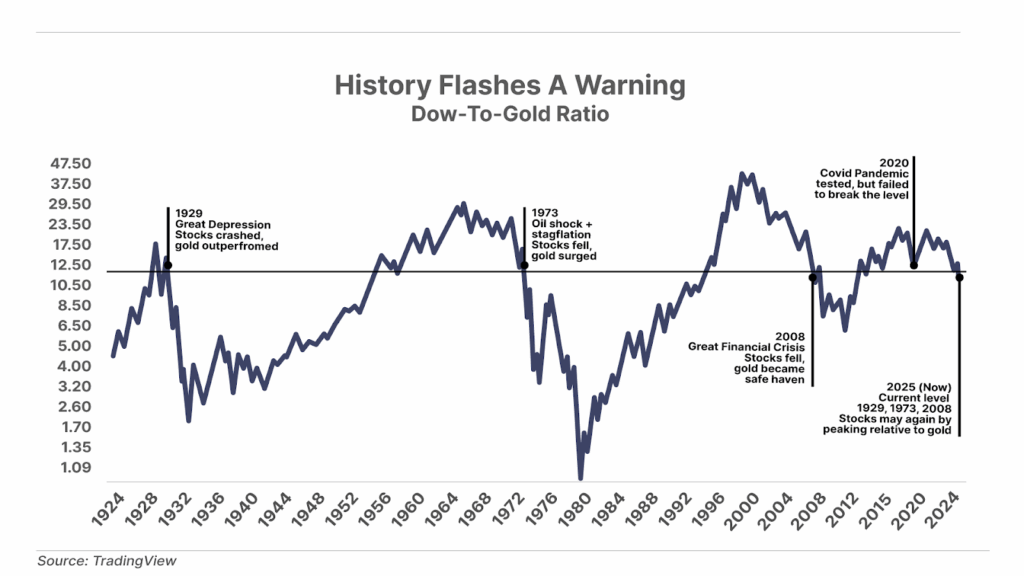

3. The Dow-to-gold ratio has fallen below a historic threshold. This ratio, which tracks how many ounces of gold it takes to buy the Dow Jones, has historically marked major turning points when stocks peaked and gold moved higher. During the Great Depression, the 1970s stagflation, and the 2008 financial crisis, gold climbed as equities faltered. The ratio’s latest decline may signal another shift from paper assets to hard assets, suggesting equities are overvalued and investors are seeking safety. History could be flashing a familiar warning – when the Dow-to-gold ratio breaks down, gold leads and stocks bleed.

And One More Thing… Poll Results: How High Will Gold Go?

With the price of gold rising above $4,000 per ounce on Wednesday, up more than 50% for the year, and still climbing, we asked readers in Wednesday’s Journal if they thought the price of gold still has room to run this year… 62% said yes, but not higher than $4,500 per ounce, while 32% said yes, and chose the option “it will reach $5,000 per ounce by the end of 2025.” Just 8% were bearish and felt the price of gold would fall below its current level of $4,000

Tell me what you think of today’s Daily Journal or anything else: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call our Customer Care team at 888-610-8895 or internationally at +1 443-815-4447.