Issue #99, Volume #2

Socialism In The Boardroom

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| Shareholders are not company owners… George Floyd/BLM inspired “inclusive” boardrooms… Cracker Barrel got a refreshed board of directors… And a new logo… Socialism doesn’t work… Car loans get longer and longer… Shakeup at the Fed… The “Mailbag” looks at Better Than Berkshire… |

As soon as I saw the Cracker Barrel “rebrand,” I knew immediately what had happened.

In 2020, during the George Floyd/Black Lives Matter (“BLM”) madness, the Nasdaq floated an idea to force companies to name more minorities and homosexuals to their boards of directors. These discussions eventually became a formal proposal. They were adopted by the Securities And Exchange Commission (“SEC”) in 2021.

While this was positioned in the media as a good-faith effort to make corporate boardrooms more “inclusive,” the real point of this measure was to further separate the control of public companies from their rightful owners, the shareholders.

You might remember this new regulation and others like it were called “stakeholder” capitalism.

And that sounds wonderful, doesn’t it?

Americans certainly believe in treating stakeholders well – people who own a stake in something, who have “skin” in the game.

But wait… that’s not what it means at all!

“Stakeholders” aren’t a company’s owners. In our brave new world of Orwellian language, stakeholders are the people who receive benefits from a corporation. Like employees. And suppliers. And government institutions. Isn’t that just socialism with a new name?

I’m sure you’ve noticed that there’s a clear link between the “solutions” for “climate change,” “structural racism,” and whatever it is the homesexuals want.

What’s the link? In each case, activists are demanding things for their special interest group that the rest of us will be forced to provide. After all, some pigs are more equal than others. And these sacrifices are for a noble cause!

Again, this is merely socialism dressed up as “social justice.”

Socialism is the proper term when people who don’t own something get to demand rewards from people who do own things, no matter what the justification.

And socialism creates extremely bad outcomes, no matter what people claim.

Letting a weirdo compete against women to justify his sexual delusion doesn’t make our society better. It’s patently unfair and it creates a society that’s based on political power instead of merit.

Awarding elite degrees to people who, judged on merit, would have never qualified to attend an Ivy League school doesn’t make our society better. It’s patently unfair, and it creates a society that’s based on political power instead of merit.

If building windmills or solar panels or electric cars makes the world a better place, then why the need for government mandates and subsidies? You know why: because forcing people to buy your product via the government is a lot easier than building a great product that is good enough to earn a sale on its own. These policies create a power grid that’s based on political power instead of efficiency. And that’s a catastrophically bad idea.

In fact, the higher up you go in society with this nonsense, the worse the impact becomes on the country. Soon our entire way of life will be threatened. And you see that happening in many places, like Chicago, where criminals are now considered a protected class.

But there’s no more dangerous front in this battle for property rights and genuine equality under the law than the battle taking place in the corporate boardroom.

Public companies make up an enormous part of our economy, with the Russell 3000 market cap now equal to almost $70 trillion.

Activists can gain control of all of that capital – without having to save, invest, or create any benefit for our economy – if they use “social justice” to control the boardrooms.

That, of course, was the real purpose behind the SEC’s 2020-era Nasdaq diversity rule and all the media associated with Black Lives Matter. It was all a socialist putsch to take over the United States.

And we’re seeing how those terrible policies are playing out in America’s corporations today.

How many of Cracker Barrel’s directors were appointed to the board after the 2020 Nasdaq diversity rule was proposed? Nine out of 10. The diversity rule sparked a complete “refresh” of the board. After all, “Uncle Herschel” was a cracker – a white man. He had no future in the new, BLM-ruled America.

Who was the first director Cracker Barrel appointed after the diversity rule was floated?

Gilbert Dávila. What was his experience in the restaurant business? He had none. But he’s hispanic – part of a favored racial group. He’s also the CEO of DMI Consulting: “a leading multicultural marketing, diversity & inclusion and strategy firm.” His previous experience? Head of diversity and inclusion for The Walt Disney Company (DIS). Dávila is a professional race grifter. And they made him right at home in the boardroom.

Next, in September 2020, they picked Gisel Ruiz. Can you figure out why? She checks two boxes: she’s hispanic and a woman. But did she have any restaurant experience? Nope. She had a long career at Walmart (WMT).

Who was next? Well, look who’s coming to dinner!

They picked Chip Wade – a black man, but I’m sure that’s not why they picked him. After all, he has real restaurant industry experience. He was before joining Cracker Barrel’s board the head of operations for Red Lobster… which most recently filed for bankruptcy.

Porter is such a bigot, they’ll say. How could he single out Chip Wade! Obviously, his race was irrelevant.

Maybe.

And then… they picked Jody Bilney. Did she have any industry experience? Almost none. She was recently head of communications for Humana (HUM), the healthcare provider.

I could go on, but you get the point.

All of this could, of course, merely be just a coincidence. Maybe these candidates weren’t chosen because our entire society went cuckoo for “diversity.” Maybe the new Nasdaq rules requiring DEI board members had nothing to do with the fact that immediately after they were proposed and adopted that Cracker Barrel appointed four new directors with little to no industry experience, but plenty of diversity cred.

And how’s that working out for the shareholders?

Since the diversity board shakeup began, the Cracker Barrel (CBRL) stock is off 65%, from $170 to $60.

If you believe that diversity, by itself, is a virtue for running a business or serving on a corporate board, then I encourage you to start a business and prove it.

I’ve started lots of businesses. I serve on a corporate board. And even before I’d done both things, I knew the color of someone’s skin (or whether they take a piss standing up or sitting down) is completely irrelevant to a business. What matters – and the only thing that matters – is business judgment gained through decades of relevant experience.

If someone is a bonafide expert in a business, they’ll also usually be investors in that business. Aside from Chairman Carl Berquist, not a single Cracker Barrel board member has ever bought a share of stock.

Not one single director, not a single share.

Think about that for a minute: a group of people who have never invested any of their capital at all – not a single penny – get to control an asset that’s worth $1.4 billion of other people’s money. What have they done with that power? They’ve pursued a political goal instead of a business goal.

That’s socialism. And socialism doesn’t work.

My advice: don’t invest in companies with boards like Cracker Barrel’s.

A Historic Gold Announcement Is About To Rock Wall Street

For months, sharp-eyed analysts have watched the quiet buildup behind the scenes. Now, the floodgates are set to open. The greatest investor of all time is about to validate what Garrett Goggin has been saying for months: Gold is entering a once-in-a-generation mania. Front-running Warren Buffett has never been more urgent and four tiny miners could be your ticket to 100X gains.

Be ready before the historic gold move. Click here to get Garrett’s Top Four picks now.

Three Things To Know Before We Go…

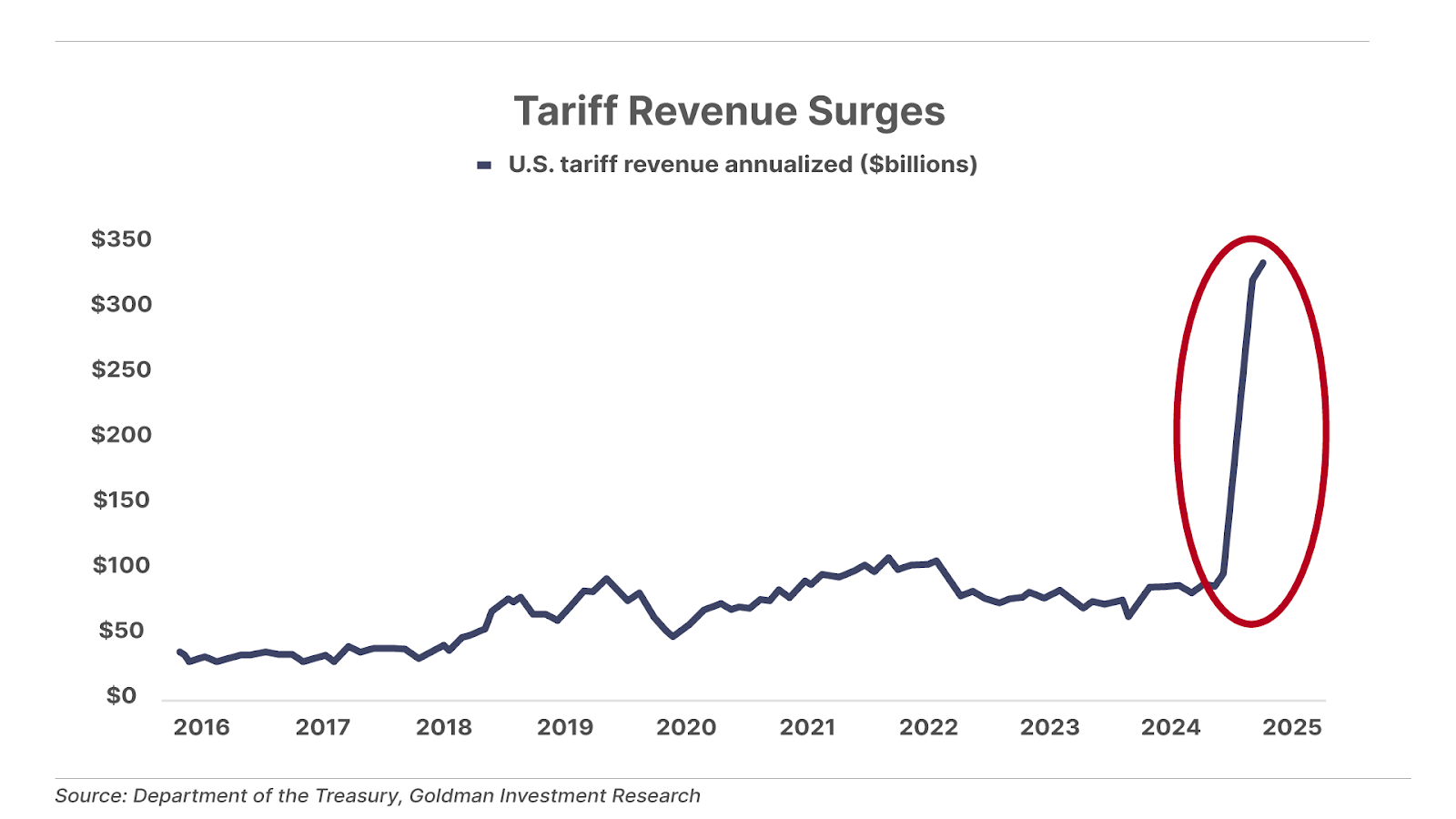

1. Tariff revenue surges. The annualized rate of tariffs collected by the U.S. government has jumped to $335 billion, up from under $100 billion at the start of the year. While this extra revenue will bolster Uncle Sam’s finances, it also represents one of the largest tax hikes imposed on the U.S. economy. It remains to be seen what the ripple effects will be as higher import taxes begin impacting U.S. consumer prices and corporate profits.

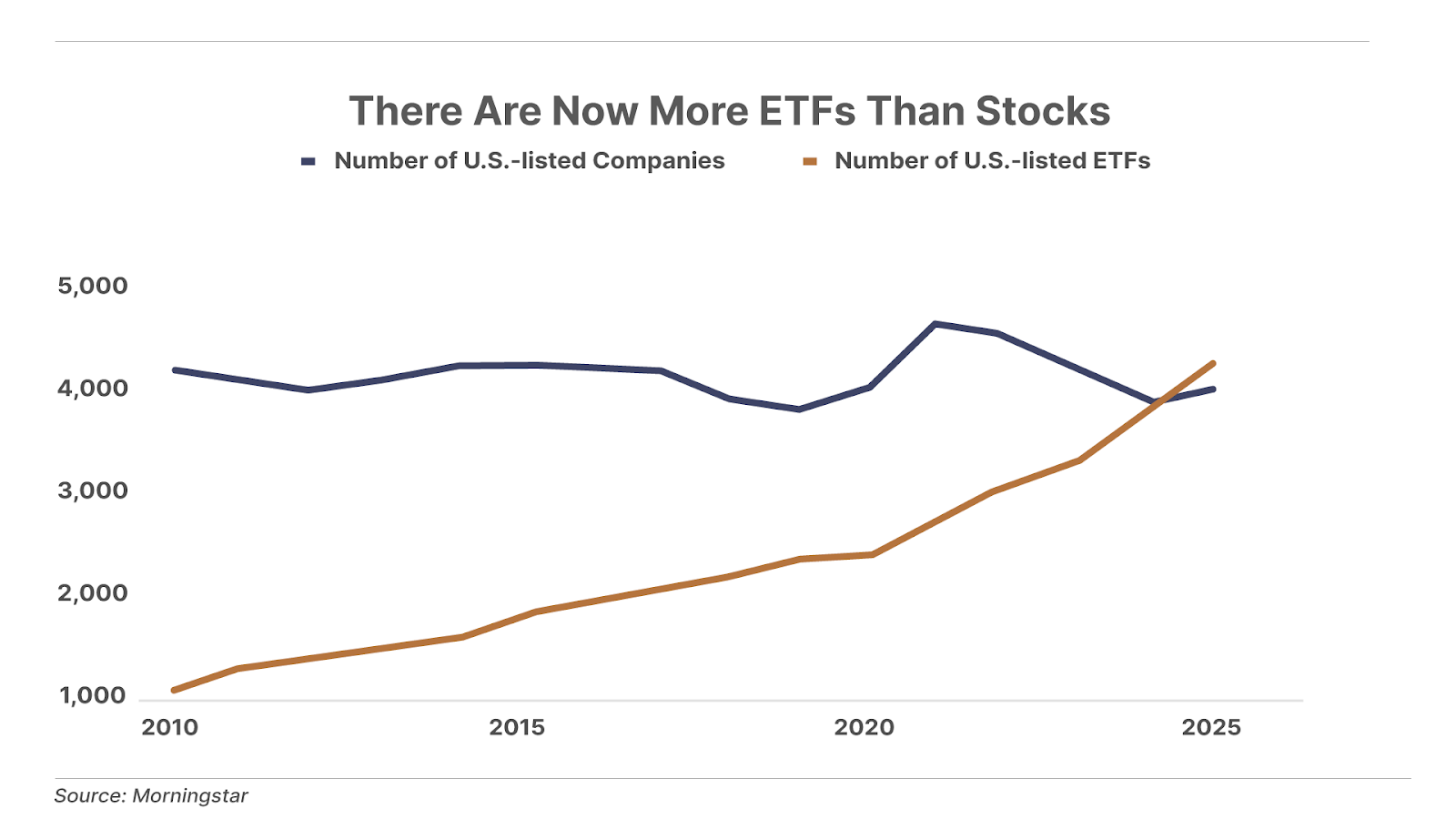

2. There are now more ETFs than stocks in the U.S. Following a surge in recent launches, there are now more than 4,300 exchange-traded funds (“ETFs”), officially exceeding (for the first time in history) the roughly 4,200 individual stocks trading on U.S. exchanges. ETFs now account for 25% of the total universe of investment vehicles versus just 9% a decade ago, according to data from the Investment Company Institute.

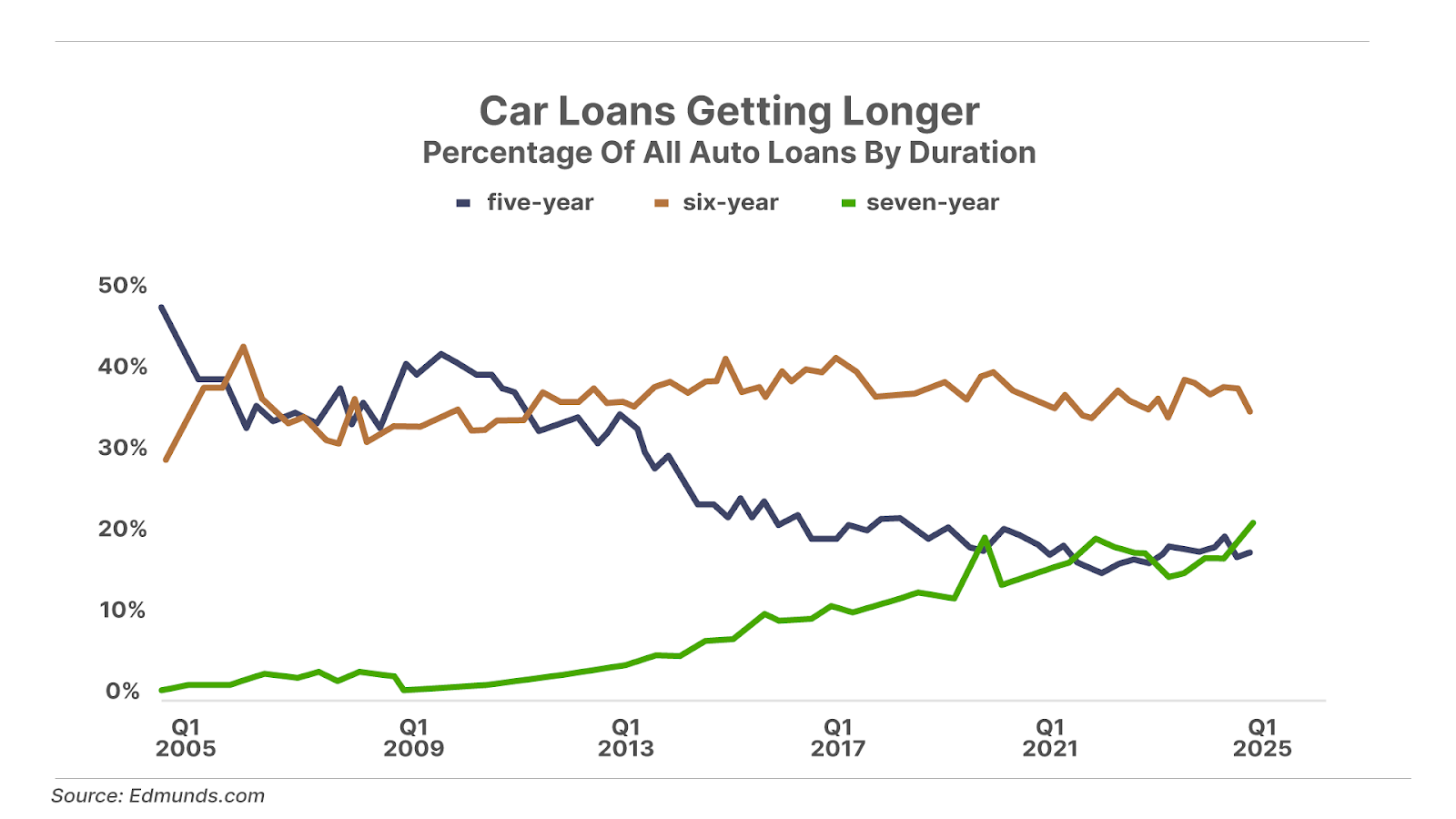

3. Car loans stretch from five to seven years. Since 2020, the average price of a new vehicle has surged 28%, reaching nearly $50,000. To manage affordability, many consumers are turning to longer-term financing. In Q2, 21.6% of new-vehicle loans spanned seven years – almost triple the 7.4% share a decade ago – while six-year loans account for 36%. A seven-year loan on an average-priced vehicle adds $5,000 more in interest compared to the five-year loans that were once the standard. For many households already under strain, that trade-off is unsustainable and a sign that affordability is slipping further out of reach as inflation persists.

And One More Thing… Turmoil At The Fed

U.S. President Donald Trump announced that he has fired Federal Reserve governor Lisa Cook – who along with the majority of the Fed board did not vote to cut interest rates at the most recent Fed meetings, to the dismay of the president. President Trump cites evidence from Federal Finance Housing Agency head William Pulte that Cook lied on various of her personal mortgage applications as the reason for the dismissal. Cook has sued to keep her position on the Fed – and as of today remains a Fed governor. Meanwhile, it looks increasingly likely that Cook, Chair Jerome Powell, and other Fed members will vote to cut interest rates at the Fed’s September meeting – and people might wonder if presidential pressure played a role or whether economic conditions called for such a move.

Lower interest rates have various repercussions on the economy – one of which is boosting investments into biotech and tech companies, ultimately leading to higher share prices in those companies. Porter and Biotech Frontiers editor Erez Kalir just announced that Erez will expand his frontier to the tech world, in what will now be called Tech Frontiers.

Erez told Porter in a conversation shared with readers: “It’s unlike anything the world has seen before. We’re at a tipping point in all these technologies and we’re seeing changes that were unimaginable just a few years ago.”

To learn more about what they say and about becoming a subscriber to Tech Frontiers, click here.

Tell me what you think: [email protected]

Mailbag

On Friday, Porter wrote something in the Daily Journal that seemed to worry many of our long-time readers: Porter’s Permanent Portfolio isn’t designed to beat the market.

Porter’s Permanent Portfolio is designed to weather any financial storm. Thus, it offers extremely low volatility, much less volatility than investing in the market directly. This strategy should deliver equity-like returns, but not market-beating returns, over time. And, yes, Porter has made several improvements to Harry Browne’s original Permanent Portfolio strategy, but any portfolio that’s holding 25% of its assets in cash is unlikely to beat the market in most years. That came as a rude surprise to some of our paid-up subscribers. So what portfolio should you build if you want to beat the market? How can you put our advice to the best possible use for your own investing? That’s the question at hand in today’s “Mailbag.”

Hello Porter,

I am a Partner Pass member. I have to say, I thoroughly enjoy your candor on all subjects, investing or otherwise. Too many people are afraid of being politically incorrect or hurting the feelings of their audience. I’m glad you addressed the differences between the Better Than Berkshire Index versus Porter’s Permanent Portfolio allocations at the end of your article.

I am getting very close to retirement from an airline and military flying career. I now have my fingers in every one of your portfolio pies. As a result, it makes it a challenge to decide what to do. All the portfolios sound so good. I know for a fact that I have way too many stock positions. Additionally, I get investing advice from Stansberry Research as well as a few other sources outside the Stansberry realm. This constant barrage of advice, ideas, and “the next best thing” has added to my investing overload and excessive number of positions.

If you were about to retire (I get the impression you never will), which portfolio would you choose to simplify your investing life? I am not risk averse, but maybe I should be.

Thanks, and keep calling it like you see it.

Ted B.”

Porter’s comment: Thanks Ted —

I think the number-one mistake many readers make is that they don’t identify what they’re trying to achieve before they go looking for advice.

If I was looking not to work ever again, to give up all my income, I would definitely adopt a non-leveraged permanent portfolio allocation… 25% stocks, 25% bonds – insurance companies count, mortgages, etc. – 25% gold and Bitcoin and 25% cash. I might use a blend of Lindy stocks and Better Than Berkshire stocks for a 12-to-15-stock portfolio. Enough to be diversified. But few enough that I can keep track.

I would wait until there’s some kind of serious problem in the corporate bond market, and then I would push my cash into corporate bonds that are close to investment grade but yielding 15% or more. Marty Fridson’s Distressed Investing will tell you which ones to buy.

The corporate debt default cycle is about seven to nine years in duration and, usually, you can find a lot of very cheap (and high-yielding paper) when the default cycle comes. Aim for paper that’s four years-plus in duration.

If, at some point, you end up with 12 “forever stocks,” some great insurance companies, gold and Bitcoin, and 25% of your assets in fixed income yielding 15% in coupons plus another 15% in capital appreciation a year through maturity… you’ll to be the envy of the retirement world.

That’s the goal.

Hope that helps —

Porter

P.S. No one else will tell you this, but I think it makes a lot of sense never to sell your equities. If you’re down for a year and you’re not generating enough income, it’s usually far better to borrow from your portfolio (margin debt) than to sell and pay taxes and then re-buy. Of course, at the top of the market, this strategy will get you in a lot of trouble. I’m talking about when the market is down 30% or more.

Good investing,

Porter Stansberry

Stevenson, Maryland

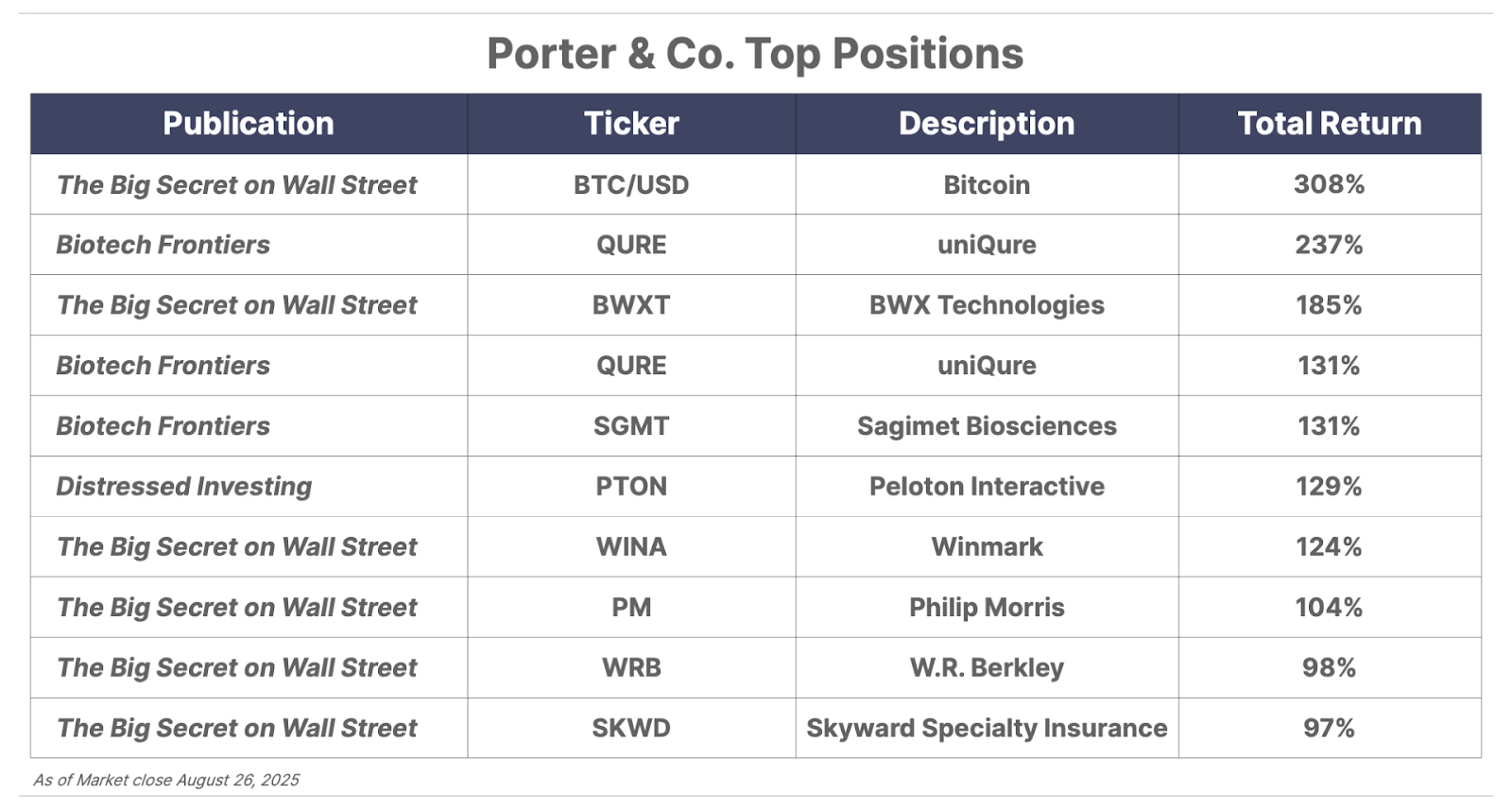

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.