Issue #84, Volume #2

An Incredible Risk-To-Reward Opportunity

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| This company has the very best underwriting process in the industry… It earns far more than most firms on its insurance float… It has increased its premiums at a 35% CAGR since 2015… Nearly every time it releases earnings, its share price falls… Buy this stock: it could produce gains of 50% in a month or two… A natural gas producer posts strong Q2 results… |

I want you to buy a stock I’m virtually certain is going to fall 20%+ by the end of the week.

What you’ll read below won’t make any sense to most “normal” investors. But for those of you who understand risk versus reward, this is the best set up you’ll see all year. This is, essentially, a risk-free way to make around a 50% return.

The first part of understanding what we’re doing here is knowing why this particular stock, Kinsale Capital (KNSL), is so safe.

Long-time followers of our work know that we like the insurance industry for one key reason: capital efficiency. In almost every other kind of business, companies have a capital cost. They can either borrow capital or they can issue equity for additional capital, but the capital they need for expansion and growth almost always comes from outside the business.

But not with well-run property and casualty (P&C) insurance companies.

Well-run insurance companies have access to zero-cost capital in the form of their insurance “float” – the money they collect upfront from premiums on their insurance policies. Until there are claims on these policies, the insurance company can use the float – this zero-cost capital – to generate earnings (typically through fixed-income investments) or for expansion.

Kinsale earns far more than most insurance firms on its float because its underwriting process is the very best in the industry. And it maximizes its underwriting edge by only insuring the biggest risks. Kinsale exclusively sells policies in an area of the market called “excess and surplus” (E&S).

These are niche, bespoke policies that cover risks most insurance companies won’t touch. These policies cover extreme events with significant loss potential, like terrorist attacks, natural disasters, and oil spills on deep-sea drilling rigs. E&S policies also cover smaller, but hard-to-predict risks, like damage or theft of a vintage wine or gem collection.

Wait a minute… how does insuring against ultra-risky events create a very safe stock?!?

Covering risks that others can’t underwrite is a great business. The idiosyncratic nature of the risks involved means that there aren’t “standard” policies to compete against or expensive regulatory burdens to follow. In fact, this area of the market is virtually unregulated. Thus, Kinsale enjoys almost complete flexibility in creating policy terms that limit their risk exposure and maximize their revenue.

As I’m sure you can understand, the key to this business is the quality of its underwriting process. There’s no “net” under this business. Kinsale’s underwriters have to anticipate every potential loss scenario, no matter how unexpected. That’s why Kinsale underwrites risk unlike anyone else in the business – in fact,100% of the underwriting is done in-house.

This goes against the traditional industry practice of outsourcing underwriting to third-party insurance brokers.

As Kinsale’s CEO Michael Kehoe explained in an interview last year:

… brokers get paid on premium volume, not profitability. So when you delegate underwriting authority to commissioned salespeople, you do create a misalignment of interests. And that shows up sometimes in the form of a higher loss ratio. So Kinsale is able to maintain absolute control over our underwriting. We never ever delegate that outside of our company.

This strategy – taking on big risks with unregulated policies, while doing all of the underwriting in-house – allows Kinsale to keep its loss ratio among the lowest in the industry (the loss ratio compares claims paid to premiums collected). From 2015 to 2024, Kinsale generated an average loss ratio of 57.7, or 3.4 points lower than its peer average of 61.1 over the same period.

Those savings go straight to the bottom line. And, believe it not, that’s not the company’s defining advantage over its peers.

The company’s far bigger edge is its ability to price new policies faster and more efficiently.

Last year, James River, which is Kinsale’s largest competitor in E&S insurance (and where Kehoe used to be the CEO), processed 321,000 submissions with 649 employees – that’s 495 submissions per employee. But in the same period Kinsale processed 735,000 new submissions with 561 employees – 1,310 submissions per employee. Kinsale is 2.6x more efficient than its top competitor.

How is it possible that Kinsale has both superior underwriting and leading efficiency?

When Michael Kehoe founded the company, he built it specifically to do this – to be the leader in E&S. From its first day, Kinsale was built on data. It created in-house its own fully integrated information management system to keep every bit of relevant data in one place, where it can be accessed in real time by teams of people. It provides easy and immediate access to all of the information each division needs to determine its own risk budget, expense, and loss ratios – making for easy and fast pricing of new policies. And the system’s high level of automation eliminates the errors and labor expense associated with manually transmitting information internally and externally.

By setting up an automated system that eliminates the friction of manual data processing, Kinsale allows brokers to get a rapid response (as fast as just one hour) to new business submissions, which is an enormous “moat.” No one else can do this this fast.

As Kehoe explained in an interview with industry data provider AM Best:

The E&S market is renowned for atrocious levels of service. And we think that’s a great opportunity for us to distinguish Kinsale. We’ve put enormous focus on turnaround times. And we’re at the point now where 30% of submissions, we’re able to respond to our broker within one hour of the submission being cleared. And for 70% of those submissions, we respond within one day. So those high levels of service allow us to distinguish the company.

All of these factors give Kinsale a best-in-class expense ratio (the expense incurred per dollar of premiums collected), which has averaged just 20.8 over the last 10 years, or an incredible 12.7 percentage points below its peer average.

And this edge in efficiency explains the incredible growth of the business: Kinsale has increased its premiums at a 35% compound annual growth rate (“CAGR”) since 2015. That’s roughly 3x the growth rate of the overall E&S market, indicating the company is taking significant market share from its competitors. It’s more than twice the rate of the next fastest-growing competitor, Arch Capital Group (ACGL), which increased premiums at a 14% CAGR over the same period.

With $1.35 billion in premiums collected last year, Kinsale currently holds less than a 3% share of the $100 billion annual market for E&S policies.

There’s a very long runway for more growth and larger profits. You measure insurance company’s operating profits by combining their loss ratios with their expense ratios to derive their combined ratio. Kinsale is the most profitable underwriter among its E&S peers, with its best-in-class average combined ratio of 78.5 for the years from 2015 to 2024. That’s an incredible 16.2 points below its peer average of 94.7 over the same period.

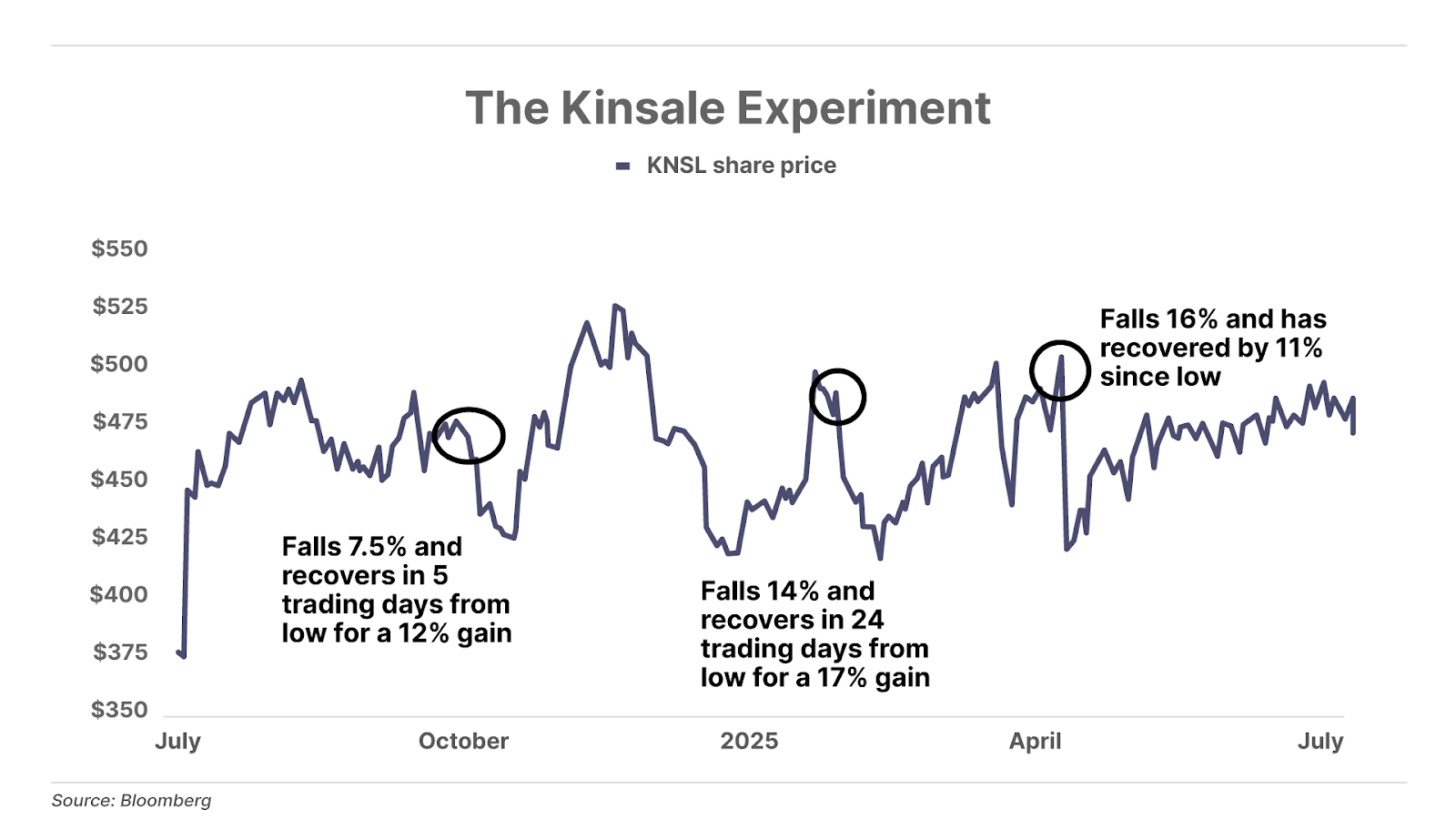

Kinsale is the Michael Jordan of E&S insurance: no one can beat it. That’s led lots of investors into its stock. The results are so impressive that the expectations on this business are immense. And we’ve noticed that quite often when it reports earnings – no matter how good those earnings are – investors are disappointed, and the stock sells off.

For example, when Kinsale reported Q1 2025 earnings on April 24, 2025, it produced $3.71 in earnings per share (“EPS”), beating the consensus forecast of $3.15 in EPS by a wide margin (+17.8%). But were investors impressed? Nope: the stock fell immediately, by about 13% after hours and then by another 16% on the next day. The stock went from $501 to $419, even though it reported great results!

We’ve seen this pattern again and again with this particular stock.

I suspect this pattern is going to occur again this week.

Kinsale reports earnings tomorrow (July 24).

I wouldn’t be surprised to see the stock suddenly fall 15% to 20% even if the company beats earnings, which I am sure it will.

This quarter’s earnings dump might be particularly severe because investors are anticipating lower interest rates. Insurance company’s income is correlated to the 5-year Treasury bond yield, as most of their assets are invested in medium-duration fixed income.

In Kinsale’s case, I think these fears are vastly overblown. It’s going to continue to grow and will simply raise prices on policies if the yield on its portfolio declines.

If you believe, like we do, that Kinsale is among the best long-term opportunities in the entire stock market, these earnings-related dips are a wonderful opportunity to add to your position.

Or if you are simply looking for a very low-risk way to make 20% or so in a month or two, then wait and see if the stock sells off like it probably will and establish a position. Consider selling when the stock rebounds to a new high.

As always, let me know what you think about Kinsale. Will you be adding to your position or just trading the opportunity if it emerges? [email protected]

Full disclosure: I am long Kinsale Capital and anticipate being a holder of my shares for at least a decade.

The Dark Consequences Of Trump’s New Investment

The Trump administration plans to funnel billions of dollars into one specific AI company. On the surface, this investment looks like the next step in Trump’s goal to make the U.S. the AI capital of the world. But dig a little deeper, and the consequences of this investment could be much, much greater than that. This company has the power to send the current AI king on a swift and ruthless 50% crash starting as soon as August 1 – bankrupting Americans who don’t see it coming. But those who do could stand to realize historic gains over the next 12 months. Click here for the full story.

Three Things To Know Before We Go…

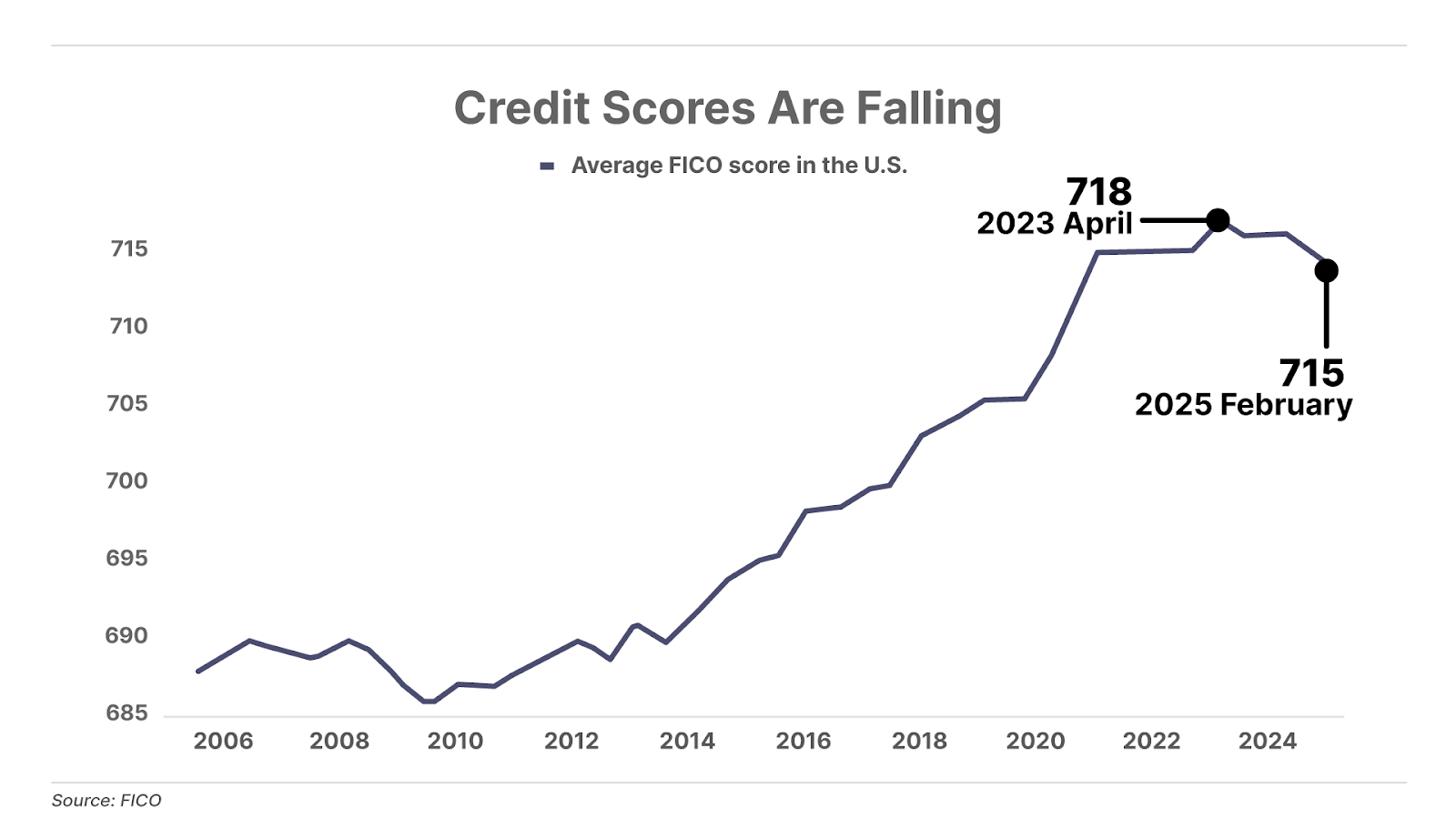

1. Credit scores drop. The average FICO credit score for Americans, which ranges from 350 (poor) to 850 (excellent), recently dropped for only the second time in a decade. Meanwhile, the total number of severe credit delinquencies – loans more than 90 days late on payment – have surpassed pre-COVID levels. Deteriorating credit scores and rising delinquencies suggest that the U.S. consumer is running out of money.

2. Japan trade deal helps global car makers. The U.S. and Japan have settled on a wide-ranging trade deal… Tariffs on Japanese imports were reduced from 25% to 15%, Japan has agreed to invest $550 billion in the U.S., and it will open its market to U.S. trade, including cars, trucks, and agricultural products. U.S. President Donald Trump reported that the two countries will also enter a joint venture on a liquefied natural gas (“LNG”) project in Alaska. The Nikkei and S&P 500 rose on the news, and shares of Japan’s largest automaker Toyota Motor (TM) jumped 15%, while Volkswagen (VWAGY) and Korea’s Hyundai (HYMTF) also saw significant bumps to their share price.

3. The Big Secret’s first recommendation proves why it’s a cornerstone holding. Under the bold leadership of “The God of Gas” – as we dubbed the company’s Toby and Derek Rice – natural-gas producer EQT (NYSE: EQT) just delivered stellar Q2 results: generating $3.3 billion in operating cash flow this year, up 123%. But it’s only the beginning – in 2026, EQT will eliminate its hedging program, giving investors full upside to rising natural gas prices. With demand in the Appalachian Basin projected to surge to nearly 7 billion cubic feet per day by 2030, the Gods of Gas are well positioned to capitalize on rising natural gas demand from utilities, AI-driven data centers, and expanding liquefied natural gas (“LNG”) exports. The first recommendation in our flagship publication The Big Secret On Wall Street, EQT is also a cornerstone of Porter’s Permanent Portfolio.

If you’re not already a subscriber to The Big Secret On Wall Street, click here to learn more… or call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447, for more information on becoming a subscriber.

And One More Thing… The Trading Club Welcomes New Members

We just closed our first three (all winning) trades in The Trading Club. The biggest winner in the current portfolio is an options play that’s up over 150% and that we believe could ultimately deliver a 10x return… This Friday, we’re releasing our next series of trades for Trading Club members, with two income-generating options trades, plus a stock currently yielding around 14%.

If you’re interested in learning about strategies designed for producing consistent income, asymmetric upside, and a risk management strategy for hedging downside, we’d love for you to join The Trading Club… Click here to join.

Tell me what you think… good, bad, or indifferent: [email protected]

Mailbag

In Monday’s Daily Journal, Porter reviewed the performance of Porter’s Permanent Portfolio, which he unveiled at the 2024 Porter & Co. Annual Conference in September. He wrote:

“So far, we’ve handily beat the market, with a return since inception of 20.9% and a year-to-date (“YTD”) return of almost 15.4%. That’s twice the stock market’s (S&P 500) return this year…

Good returns are nice, but it might just be luck. What isn’t luck though is when you beat the market and take on much less risk. In fact, most finance professors would tell you that’s impossible.

But Porter’s Permanent Portfolio has less than half the volatility of the stock market (beta: 0.41, compared to the market benchmark of 1) while earning twice the S&P 500’s returns.”

In response, Mike O. wrote the following:

Porter, I’ve been following you for 15 years or more, and now am with you at Porter & Co. You have taught me so much more than the books I have read over the years. Your knowledge, insights, and instincts have always led me in the right direction and for that I am extremely grateful.

I followed Porter’s Permanent Portfolio as soon as you presented it, and it’s awesome. The changes and tweaks you made to Harry Browne’s original Permanent Portfolio have worked just as you described. Most people would love to beat the S&P, and for most that would be great. You have found a way to beat the S&P, consistently, and with far less risk – amazing.

Most portfolio managers would love to do what you have done. Since the beginning you have always searched for better ways to help your subscribers. Now, even at 75 years old, I am with you in The Trading Club and excited about the active management of the Porter’s Permanent Portfolio.

Once again, you have built a better mousetrap than the originators. As a result of your efforts my family is financially secure. Thank you for providing the knowledge, resources, and tools to make that possible. You’re the best!

Mike O.”

Porter’s comment: What an incredible letter! Made my year.

Thank you so much for appreciating our work over many years.

In Porter’s Daily Journal on Monday, July 21, you talk about a strategy trading only the QQQ [Nasdaq’s largest 100 stocks, weighted by market cap] and gold. I would like to implement that strategy with a portion of my portfolio, and I have some specific questions about implementation.

- For gold, are you talking about trading GLD?

- You talk about trading the 50-day moving average line. Do I need to watch this continually, or is this an end of day or beginning of day trade? I’m looking specifically at how this is modelled so I can implement his strategy.

Great article by the way!

Alvin N.”

Porter’s comment: For my study I used the 3 pm spot price of the London gold fix. I had to use the futures market for gold’s price because my backtest, which starts March 1999, pre-dates the launch of GLD, so I wanted to be consistent.

And yes, the model made portfolio adjustments on the day following a break below (or above) the 50-day simple moving average.

Hope that helps –

I unveiled Porter’s Permanent Portfolio at last year’s Annual Conference for Partner Pass members and plan to rebalance this one at our upcoming conference on September 24 and September 25 at my farm outside Baltimore. There are a handful of conference tickets left for Partner Pass members to purchase.

Partners… To get yourself into the conference… to meet and talk with the analysts… to get the latest on Porter’s Permanent Portfolio… to have a cocktail with me and my team… call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447, for more information on how to attend.

Good investing,

Porter Stansberry

Stevenson, Maryland

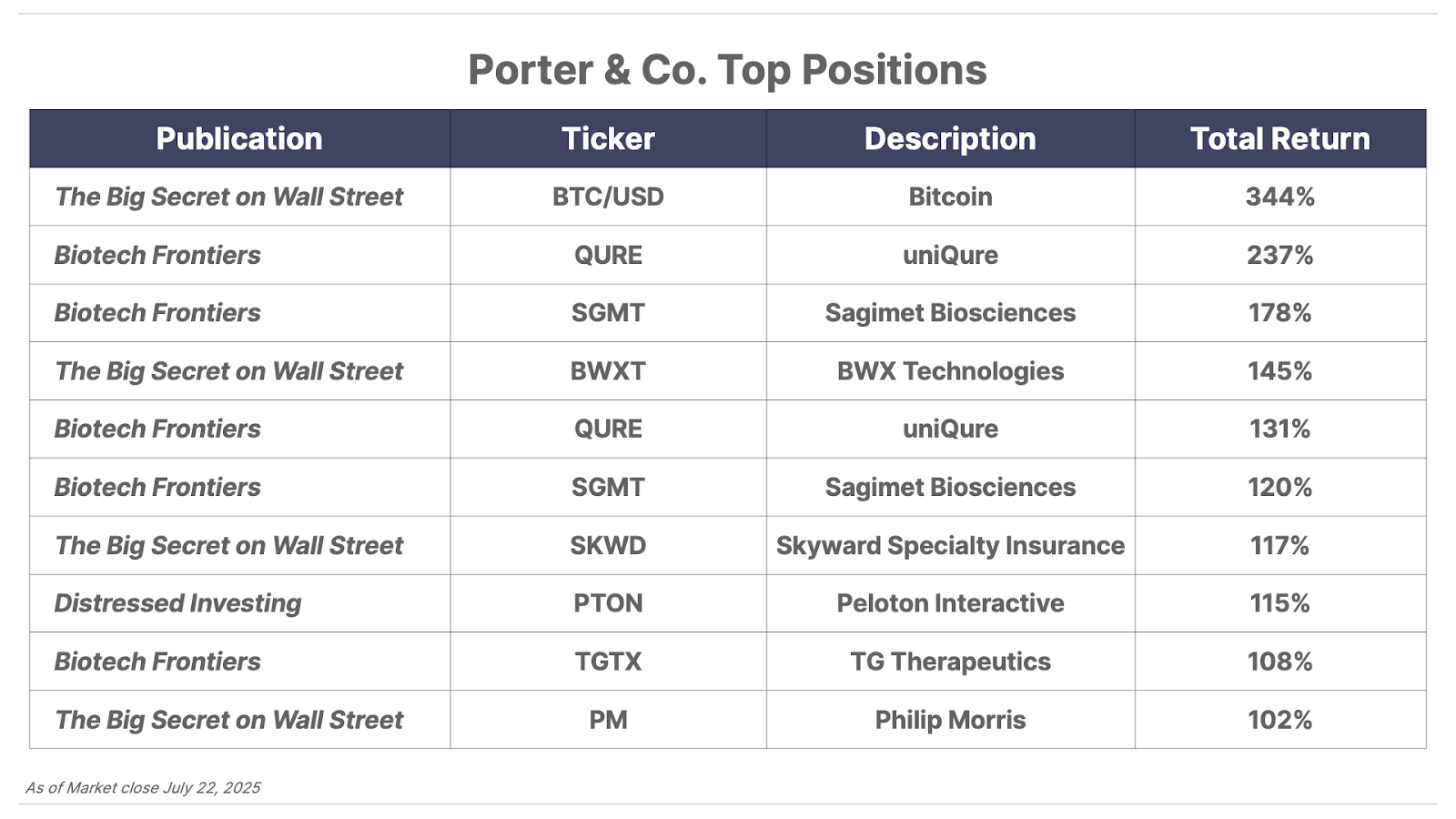

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.