Issue #83, Volume #2

Understanding The “Magic” In Porter’s Permanent Portfolio

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| Porter’s Permanent Portfolio has way outperformed the S&P 500… Less than half the beta and an-unworldly 2.02 Sharpe Ratio… Older investors can sleep soundly at night… Add leverage and the performance gets even better… White House turns up the heat on Fed Chair Powell… |

Last fall, when I unveiled Porter’s Permanent Portfolio, I promised that it would deliver stock market-like returns with far less risk.

And I told the attendees of our Porter & Co. Annual Conference that, although I couldn’t promise it, I believed that Porter’s Permanent Portfolio would far outpace the returns of the stock market. As you may remember, this strategy involves allocating capital into four buckets: stocks, bonds, gold, and cash (90-day U.S. Treasury bills).

With 50% of the portfolio invested in fixed income, how could I expect to beat the market and have less risk? First, by owning low-volatility, high-quality stocks. And secondly, by replacing the traditional bond market allocation, with high-quality property and casualty (P&C) insurance stocks.

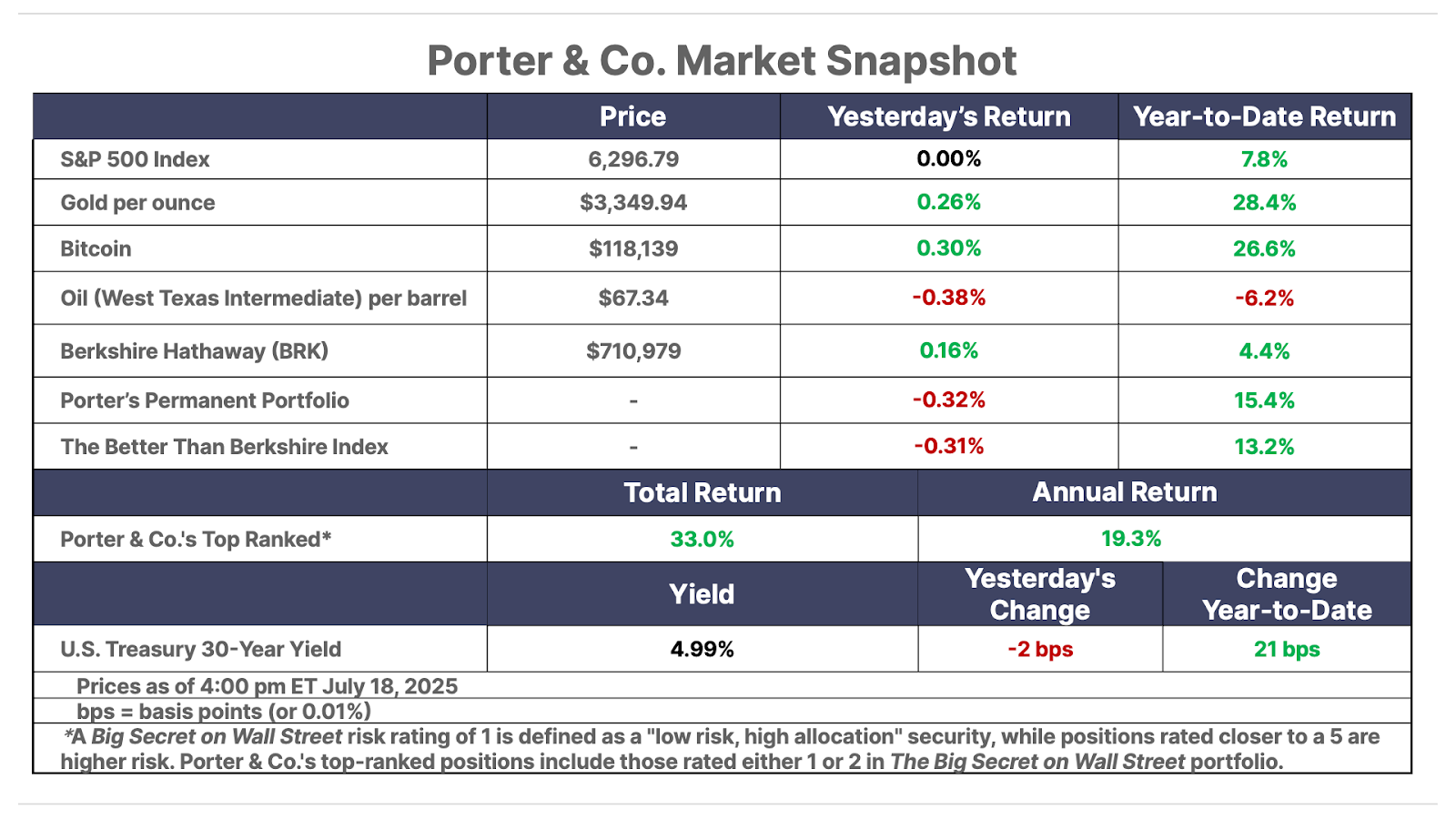

So far, we’ve handily beat the market, with a return since inception of 20.9% and a year-to-date (“YTD”) return of almost 15.4%. That’s twice the stock market’s (S&P 500) return this year. And it dwarfs Berkshire Hathaway’s 4.4% return. That’s notable because Berkshire is a security many investors have used to beat the market for decades, but that I’ve warned will not beat the market going forward. Porter’s Permanent Portfolio is even beating our proprietary “Better Than Berkshire” Index, which is up 13.2% YTD.

Good returns are nice, but it might just be luck. What isn’t luck though is when you beat the market and take on much less risk. In fact, most finance professors would tell you that’s impossible.

But Porter’s Permanent Portfolio has less than half the volatility of the stock market (beta: 0.41, compared to the market benchmark of 1) while earning twice the S&P 500’s returns.

Producing massive excess returns with such little volatility is virtually unheard of in the markets. With higher returns and less risk, Porter’s Permanent Portfolio has Sharpe Ratio investors almost never see: 2.02.

The Sharpe Ratio is a measure of return per unit of risk (volatility): return/volatility.

Achieving portfolio Sharpe Ratios in excess of 1.0 is very, very rare because, most of the time, return is tightly correlated to risk. There are, occasionally, assets whose exceptional returns can lead to higher Sharpe Ratios in the short term. Bitcoin, for example, has a 1.12 Sharpe Ratio over the last five years. But virtually all stocks have a Sharpe Ratio that’s less than 1.0. The S&P 500, for example, has a Sharpe Ratio of 0.89.

That we were able to achieve such high returns with low-risk assets was foremost because of our stock selection. Many of our low-volatility recommendations have turned in outstanding performances:

- Philip Morris International (PM), up 52%

- EQT (EQT), up 55%

- Deere & Co. (DE), up 25%

- Alibaba (BABA), up 30%

- Tencent (TCEHY), up 28%

We’ve also gained a lot of “alpha” – that’s performance above our benchmark – by not owning bonds directly, but indirectly through insurance companies, two of which have been outstanding performers:

- Markel Group (MKL), up 30%

- W.R. Berkley (WRB), up 25%

And finally, our relatively large 12.5% allocation to Bitcoin in lieu of holding only gold has been an outstanding decision:

- Bitcoin is up 88% since inception

Having a low-volatility and high-return portfolio is very attractive for retired investors who cannot easily suffer the volatility of the stock market. Porter’s Permanent Portfolio is designed to produce equity portfolio returns, with about the same low volatility as a bond portfolio.

This strategy allows older investors to put their money in the stock market and still sleep soundly at night.

But that’s not the reason people in finance seek Sharpe Ratios in excess of 1.0. People in finance seek out Sharpe Ratios in excess of 1.0 because they are like magic: they create more return per unit of risk.

Thus, these strategies can be leveraged efficiently to produce very high, consistent returns.

In most investments, adding leverage will create too much volatility, resulting in big drawdowns and margin calls. But with Sharpe Ratios above 1 – and even better, above 2 – investors who can tolerate market-levels of risk can produce astonishing results.

As I detailed for our Partner Pass subscribers a few days ago, I’ve been running a leveraged version of Porter’s Permanent Portfolio in my family office. My YTD returns are 70.5%, with less volatility than the market (beta: 0.74) and a Sharpe Ratio of almost 3!

How’s that possible?

Well, I left out the 25% allocation to cash. And I added 2x leverage. I’ve also been adding substantial amounts of income by consistently selling puts. The result is a portfolio that’s not correlated to the stock market (correlation is only 0.30) but that earns consistent returns, week after week.

You can’t run a portfolio with this much leverage and not suffer large drawdowns from time to time. I’ve experienced a 30% drawdown once this year. Thus, I don’t advocate this approach for retired or risk-adverse investors. But for people with years of income left, this approach is clearly superior to simply being a buy-and-hold investor.

To confirm this approach can work, consistently, I’ve been studying the two most clearly non-correlated portfolio assets: stocks versus gold.

I’ve been looking for a “no brainer” way of using our strategy to produce market-beating results. I want to prove that anyone can do this, to validate not just my own investment performance, but the approach in general.

So to filter out my prescient stock picking, I’ve used a high-quality/low-volatility exchange-traded fund (“ETF”), FlexShares U.S. Quality Low Volatility Index Fund (QLV), whose portfolio dynamics will be like Porter’s Permanent Portfolio.

Since the inception of QLV in 2019, if you’d simply run a buy-and-hold portfolio of 55% QLV and 45% gold (GLD) – and only rebalanced when those allocations got out of range by more than 20 percentage points – you produced a portfolio with 13.4% annual returns (market-beating), but with only 11.2% annualized volatility.

That means a maximum drawdown of just 15%. That’s good for a 1.2 Sharpe Ratio, meaning you could easily leverage this portfolio by 1.5x or 2.0x and still remain within margin limits.

At 1.5x leverage, the annual return grows to 17.6%, with 16.8% annualized volatility and a maximum drawdown of 22.5%. At 2x leverage, the annualized return is almost 22%, with 22% annualized volatility and a 30% maximum drawdown.

For context, over the same period, the S&P 500 saw slightly lower annualized volatility of 14.5% with a slightly higher maximum drawdown of 34%.

It’s clear that using high-quality, low-volatility stocks, hedged with gold, and leveraged, can produce a set-it-and-forget approach to beating the market consistently (by a huge margin) without taking greater than stock market risk.

But I wondered… what if you could find ways to mitigate excess risk through active management? Could you then use even higher-performing stocks that are more volatile? And could you still use gold to reduce volatility enough to make using margin safe?

To answer this question, I downloaded the daily closes for the QQQ ETF (Nasdaq’s largest 100 stocks, weighted by market cap) and the daily London gold spot price (the 3 pm fix), since QQQ began trading in March 1999.

I know that despite its good long-term results, QQQ is far too volatile to be an efficient investment for beating the market… It has a Sharpe Ratio of 0.71. But I also know that like gold, it is an asset class that trends strongly. So to reduce volatility, I applied a simple active management strategy: trend following, using a moving average.

For this strategy, we want to own QQQ when it is above its 50-day moving average. And we want to own gold when it is above its 50-day moving average. We also want to favor the stronger returns available in tech stocks. So if both QQQ and gold are in “bull” mode, then our allocation will be 80% QQQ and 20% gold. If only one is in bull mode, then our allocation shifts 100% into that asset (either QQQ or gold). And if neither is in bull mode, then we revert to 100% cash.

This simple strategy results in an unlevered annual return of 18.2%, with 15.8% volatility and… get this… only a 14% maximum drawdown.

The active management (no-brainer trend following) vastly reduces the severity of the drawdowns, which, in theory, allows for far more leverage to be employed.

At 3x leverage, the annualized return is 45% (!), with 45% volatility and a maximum drawdown of 42%. Yes, that’s far too aggressive for most investors, but it still produces an excellent Sharpe Ratio (1.0). For most investors, using this strategy with 2x leverage will produce “good enough” results: 32% annual return, 30.4% volatility, and a maximum drawdown of 28%.

Looking at these examples, will you migrate some (or all) of your portfolio into Porter’s Permanent Portfolio this fall, when we adjust our allocations and pick our new equity portfolio?

Let me know why or why not: [email protected]

Jeff Brown’s Big Discovery in Washington, D.C.:

“Beginning Immediately, Trillions Could Flood These Tiny Cryptos”

Presented By Brownstone Research

Thanks to a bill President Trump signed on Friday, a trillion-dollar tsunami could hit a corner of the crypto market… beginning immediately.

President Trump calls the plan “incredible.” And once you see how to get in front of it, you will too.

Already, small plays are jumping as much as 300%, 318%, 520%, and even 600%.

For a limited time, Jeff Brown is sharing everything.

Three Things To Know Before We Go…

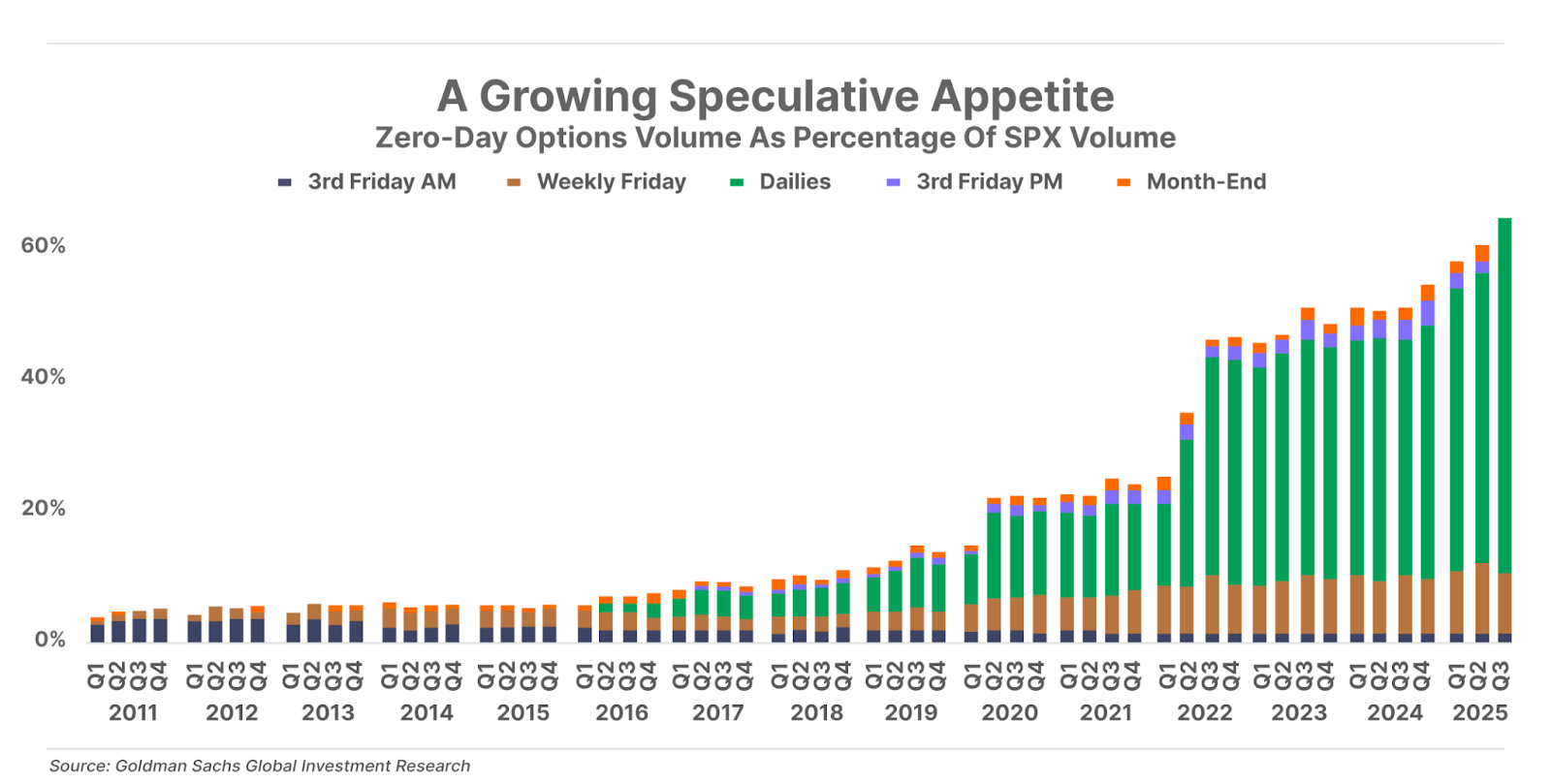

1. Options mania. Options contracts that expire in one day (known as “zero-day options”) now make up a record 60% of all S&P 500 options volume. These high-risk derivative contracts are used to speculate on daily stock-price changes – the latest sign of the growing risk appetite in today’s market.

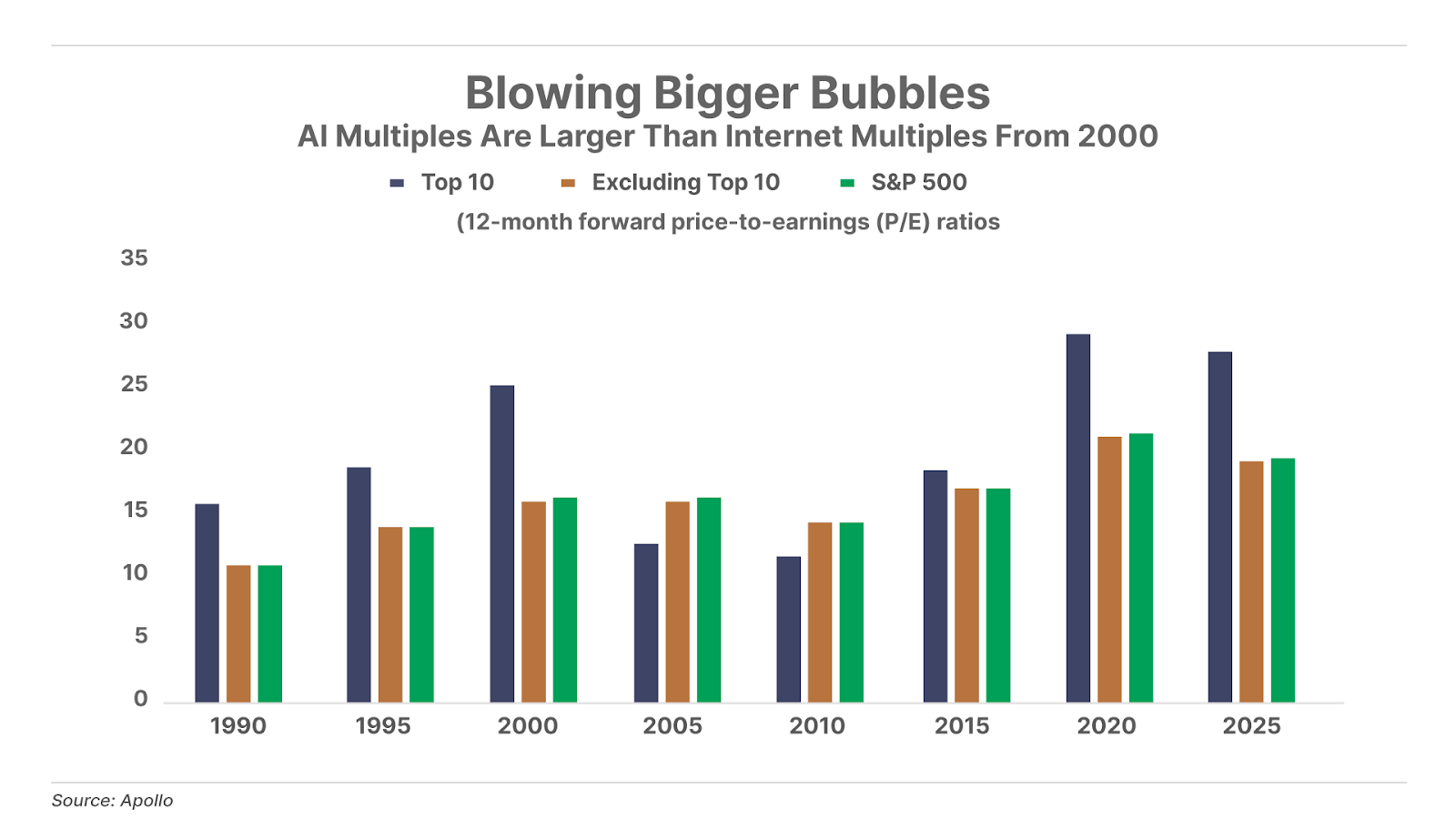

2. The AI infrastructure spending surge: boom or bubble? Capital expenditures on artificial intelligence (“AI”) are projected to reach 1.2% of U.S. GDP this year – a 10-fold increase in just three years. Yet the top 10 companies in the S&P 500 now have higher P/E multiples than the top 10 companies had during the height of the dot-com bubble. At the same time, the staggering costs of AI data centers are fueling concerns over the long-term economic rationale of these investments.

3. The Trump administration’s all-out assault on the Fed. This morning, Treasury Secretary Scott Bessent became the latest member of the Trump administration to publicly criticize the Federal Reserve and its Chair Jerome Powell. In an interview with CNBC’s Squawk Box, Bessent argued that the Fed has done a poor job of achieving its mandate and should be subject to an extensive review. “If this were the [Federal Aviation Administration] and we were having this many mistakes, we would go back and look at why this has happened,” Bessent said. “All these PhDs over there, I don’t know what they do… This is like universal basic income for academic economists.”

And One More Thing… Trading Club Mailbag – Testimonials

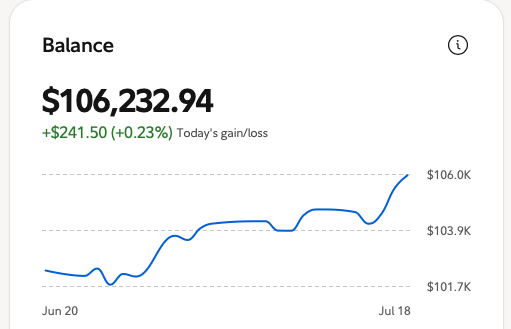

The Trading Club is off to a smashing start. The live $100,000 account we launched on May 30 is now up over 6% to $106,232.

We’ve received rave reviews from members like Larry B., who writes:

This is one of the best products I have ever seen, and I’m a lifetime member at Stansberry Research and at Porter & Co. This is far better than Retirement Trader, for example. Here’s my screenshot from Vanguard on the British American Tobacco (BTI) call I ended up with. I had never before bought a call, and you inspired me to do it! It is up exactly 100% in 18 days.”

Another Trading Club member, Brady G., writes:

I want to commend you on The Trading Club success so far. The training materials, support, trade explanations, follow up, and overall success have been outstanding!

I was looking for a better return on my emergency fund, and a better option for $50,000 of cash in a high-yield savings earning 4+%. I am up $3,850 as of today, July 18.

I executed both the Celsius (CELH) and Dream Finders Homes (DFH) winning trades that expire today and I am happy to say I also executed BTI calls that are up 138%. Wow. All told, I was able to execute 12 of the 15 trades and I am thrilled with the results.

Thank you for the terrific work you and the team are doing… keep them coming.

Very Satisfied Trading Club Member.”

And finally, this note came from Jack P., who writes:

My odometer will tick over 75 years shortly. In that time I have reviewed, purchased, joined, and/or subscribed to scores upon scores of investment newsletters, trading services, courses, software, etc.

Most fall into two broad categories.

One offers more hype than substance bedazzling with astronomical winning trades and/or bells-and-whistle technology… without divulging that losers torpedo net returns in real life.

Second, the generally more conservative genre offers generic portfolios with buy-and-sell recommendations. Mostly, these involve relatively long-term stock purchases, although a few focus on option trading… usually relatively risky long calls and puts or uncovered short options. Strategies range from technical to fundamental. In most cases, little or no guidance is given on risk management.

I was lucky to become aware of the Porter & Co. Trading Club and joined at its opening May 30. This investment service combines in depth fundamental analysis of stocks with integrated risk management and income enhancement using low-risk covered option strategies. Your weekly updates keep us informed and provide training to those unfamiliar with the techniques. The training alone is worth the annual fee (I’m not asking for an increase!).

The official gain of 5% since inception seven weeks ago (44% annualized) is excellent. I personally did considerably better than this as I risked 5% of equity on all positions, including the long call on BTI, which rose sharply.

Thank you very much for The Trading Club.”

The Trading Club is officially open for new subscribers, for a limited time only.

If you’re looking for active trading strategies designed for consistent income, asymmetric upside, and a comprehensive risk-management strategy – all tracked with a live, real-world portfolio that shows you every step of the way – click here to join.

Tell me what you think… good, bad, or indifferent: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland

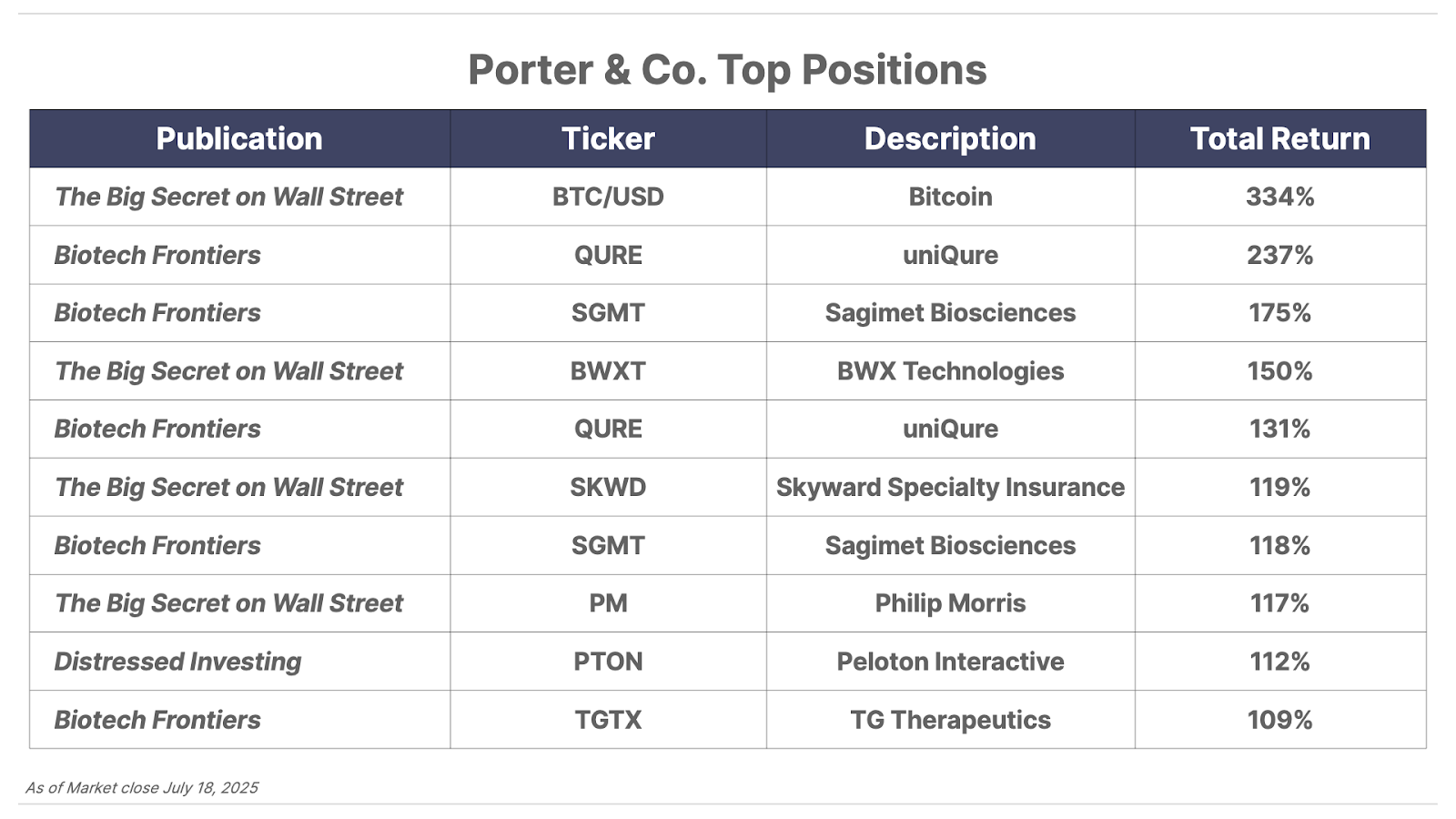

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.