Issue #81, Volume #2

Beat The Crowd: Get Your Money Out Of The Banks, Now

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| Bitcoin is going to replace gold… Stablecoins will replace the U.S. dollar… This is good news for people around the world… Every regional bank in the U.S. will fail over the next five years… Beat the crowd… Today’s poll: Will Trump fire Powell? |

It’s happening.

Whether you understand it or not, the nature of money is changing forever.

We are at the beginning of the most important change to the world’s economy since Western Union’s first international money wire in 1872. The internet and stablecoin encryption offer unlimited transfers of money, instantly, to anyone, anywhere in the world, for free.

Likewise, you do not need a bank to keep your stablecoins safe. The biometric devices on your phone and passwords work just fine.

If you think about this for a minute, you’ll realize something: the reason banks exist is because they safeguard our money and facilitate payments. They’ve done so for decades, using everything from American Express strongboxes (in the 1850s) to the Visa network (1958).

But much like what happened to the telephone companies in the 1990s, the internet has eliminated the need for these banking services through the evolution of digital communication.

If you don’t have time to read all of this, just understand this: Bitcoin is going to replace gold as the ultimate reserve currency, and stablecoins will replace the dollar as the money most used in daily exchanges.

These changes are incredibly good news for people all around the world. But they will be incredibly challenging for institutions (governments and banks) that run, mainly, on cheating people through monetary schemes.

Money has always evolved.

People have used all kinds of things as money to facilitate trade. But for the last 4,000 years or so, people have preferred to use gold. Why gold? Because gold is nature’s perfect money. It is scarce and it represents a “proof of work” (it requires capital and labor to produce). Gold is timeless (it doesn’t tarnish). Gold is relatively stable in supply (only increases 1% to 2% a year, on average). And, even as the industrial revolution made gold easier to mine, its growing scarcity made it harder to find, limiting the annual increases to supply. In this way, its value has been stable for thousands of years. (Its price changes – but its value does not.) Gold is also easily divisible. And it’s universally recognized, but hard to counterfeit.

Finally, and most importantly, gold isn’t consumed by industry. There are better, cheaper metals for virtually every industrial application.

That last part is difficult for a lot of people to grasp – even Warren Buffett. Buffett has famously argued that because gold is virtually useless for industry, it has no intrinsic value.

That’s nonsense: money has the greatest utility of all, because it enables trade. It’s ironic that Buffett – of all people – wouldn’t understand the enormous importance that sound money plays in facilitating trade and investment. Trade is what creates the miracle of comparative advantage. Unlike what President Donald Trump says, no one loses through trade: both sides win. But without a sound form of money, there’s no way to facilitate these win-win exchanges.

And without sound money, saving for investment becomes almost impossible, as a lot of middle-class people who have depended on the U.S. dollar for decades are finding out.

That’s why, for thousands of years, the global economy has run on a gold-backed system.

Even today, although there is no formal link between the U.S. dollar and gold (the value of our currency “floats”), most central banks continue to use dollars to facilitate the purchase of gold for their reserves.

I’m not going to get into the details of why the world is fleeing the dollar, but this number will shed light on their reasons. I asked Grok 4 – the world’s current leading artificial intelligence platform – to calculate how much money the government would need to print right now to meet its existing Social Security and Medicare obligations for the next 25 years.

Grok’s answer:

“To maintain the promised benefits for Social Security and Medicare over the next 25 years (through 2049), the government would need to contribute additional funds equivalent to the present value of the projected shortfalls between program costs and dedicated revenue (such as payroll taxes and premiums). Based on the latest trustees’ projections adjusted for these economic assumptions, this amounts to approximately $30 trillion in present value terms.”

Everyone assumes I’m exaggerating when I try to patiently explain that our government is bankrupt. I don’t think we can honestly (that is, without printing) finance our existing $37 trillion in debt. But there’s absolutely no way we can afford the promises we’ve made.

Things that can’t happen, don’t. And that’s why you have seen, and will continue to see, much higher prices for Bitcoin and gold. And as the world flees the dollar, people are going to turn to new forms of digital money.

Why? Because Bitcoin is better than gold. Bitcoin is not merely difficult to counterfeit. It’s impossible to counterfeit. Likewise, Bitcoin is much easier to use, to store, and to safeguard. And the very best reason? Stablecoins virtually eliminate transaction costs.

Right now you can deposit your paycheck into Coinbase and immediately transfer your dollars into a digital form of the dollar, something called USDC, issued by Circle Internet (CRCL). This is a stablecoin (a digital receipt) that’s 100% backed by short-term U.S. Treasuries. Why would you do this? Because instead of earning virtually nothing, like at your bank, it will pay you 4.10% annually, beginning instantly. And you can use this digital dollar to buy things at retailers all over the world, using emerging payment platforms like Bitpay and Shopify. These transactions are free and they happen instantly.

Soon – within five years – most payments will be made using digital stablecoins like USDC.

That’s going to be really bad news for all of the institutions that have been stealing from us for years by withholding our funds, delaying settlement, and earning billions from the resulting “float.” Likewise, it’s going to bankrupt every financial institution that refuses to pay market rates of interest on our money.

I recommend you take all of your cash out of your bank and begin using Coinbase and stablecoins to pay for things. Doing so will help safeguard you from inflation and will vastly reduce the “friction” you face using the banking system.

Plus, you’ll want to beat the crowd. Regulators and banks are going to make it harder and harder for you to withdraw your funds. In the first half of 2025, $38 billion came out of the banks into stablecoin.

That trickle is going to turn into a flood.

A few years ago, I had a major Texas land deal in hand (my partners and I were buying 68,000 acres in the Permian Basin for $48 million). We would have made $300 million to $500 million on this deal within 18 months. But it didn’t happen because, at the last minute, our scumbag banker who’d promised to finance the deal reneged. (His bank suddenly realized that lending $48 million at 2% for 15 years was going to end badly.) The day after our financing fell through, the Chinese bought this land for cash.

Our banker’s behavior was so egregious that we sued – and won. Nothing in my life has felt better than suing a bank – and winning.

Soon, there won’t be any banks. I won’t shed a tear. The end of these rapacious institutions is great for our economy and for individuals. Let me say this clearly, so everyone will understand:

I believe every regional bank in the U.S. will fail over the next five years.

The same thing that happened to telephone companies in 1999 when the internet came along is about to happen to banks. The internet is about to take over money. And that means we don’t need banks anymore – at all.

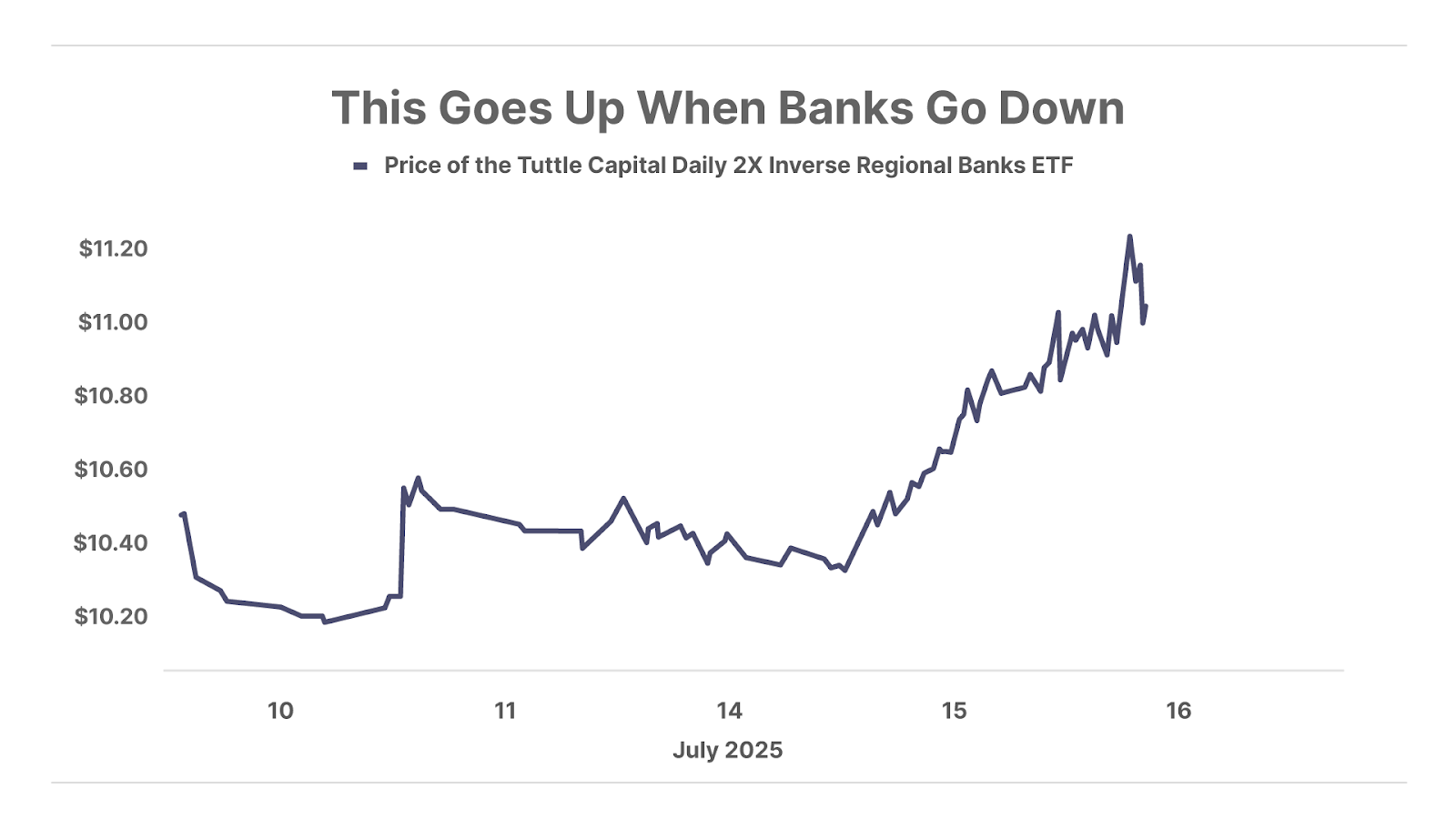

Don’t believe me? Just watch. The Tuttle Capital Daily 2X Inverse Regional Banks ETF (SKRE) is an exchange-traded fund (“ETF”) that offers investors about 200% of the inverse of the daily performance of the SPDR S&P Regional Banking ETF (KRE). In simpler terms, this ETF is designed to go up – a lot – when the regional banking sector, as tracked by KRE, goes down. And since it’s going to zero, this ETF is going to go up… a lot.

Migrating into digital dollars is only the beginning.

As soon as people get used to using digital money, they’re going to ask themselves a simple question: why bother using the dollar at all? Coinbase will pay you 4.1% to use digital dollars (the money comes from the yields on the underlying U.S. Treasury bills). But you can earn between 7% and 15% a year (depending on the platform) lending your bitcoin.

And, of course, Bitcoin isn’t going to decrease in value every year. In fact, it’s extremely likely to continue to appreciate, massively, against the dollar and against gold.

How do I know?

Bitcoin, in total, is now worth 9.3% of all of the gold in the world, and it’s worth only 3.4% of U.S. stocks. But it should be worth just as much as gold. And should probably be worth 20% to 25% of U.S. stocks. In the first half of this year, the number of companies holding Bitcoin in their treasuries almost doubled, from 70 to 134 (including 41 U.S. companies, 29 Canadian companies, eight Japanese companies, and seven UK companies).

If you don’t have exposure to Bitcoin yet, I believe you should begin to buy it. Bitcoin makes up 12.5% of Porter’s Permanent Portfolio.

These changes are coming for a very good reason: Bitcoin is better than gold.

Classified Military Lab In New Mexico And Next 40% Market Crash

Inside, scientists aren’t studying weapons or viruses – they’re exploring a far more alien technology that could change how wars are fought.

This new technology could be unleashed as soon as July 15.

Once you see it for yourself, you’ll understand the urgency.

Three Things To Know Before We Go…

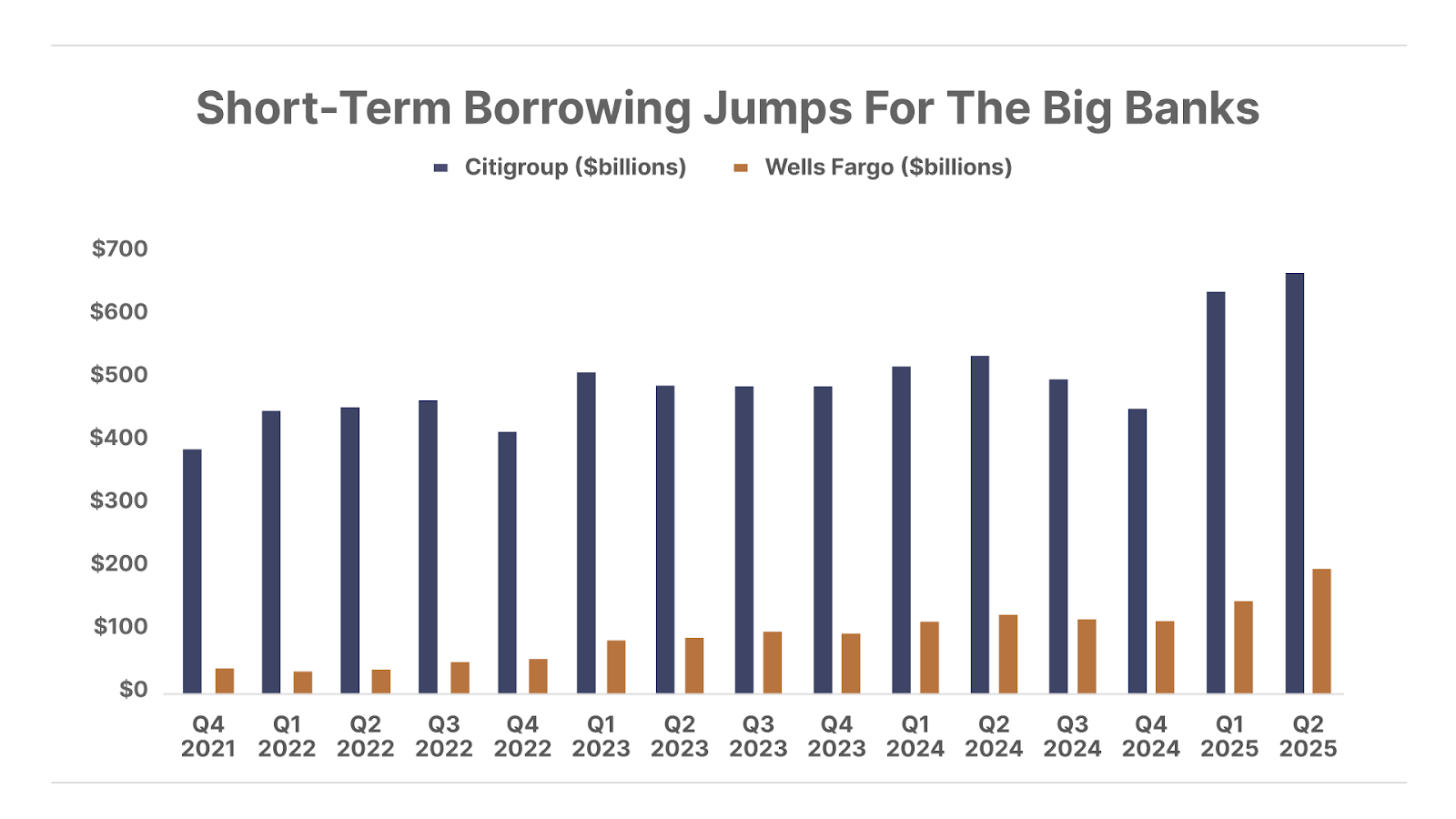

1. Banks slide as short-term borrowing surges. Yesterday, Citigroup (C) reported that its short-term borrowing surged 44% year-over-year (“YOY”), signaling a growing dependence on external funding rather than core deposits to run its business. And Wells Fargo (WFC) reported that its short-term borrowings jumped 58% YOY, to a staggering $188 billion. Without this short-term funding, these institutions could have faced serious liquidity shortages – potentially triggering bank runs and fire-sale liquidations. The message is clear: liquidity stress is building, and a broader crisis may be on the horizon.

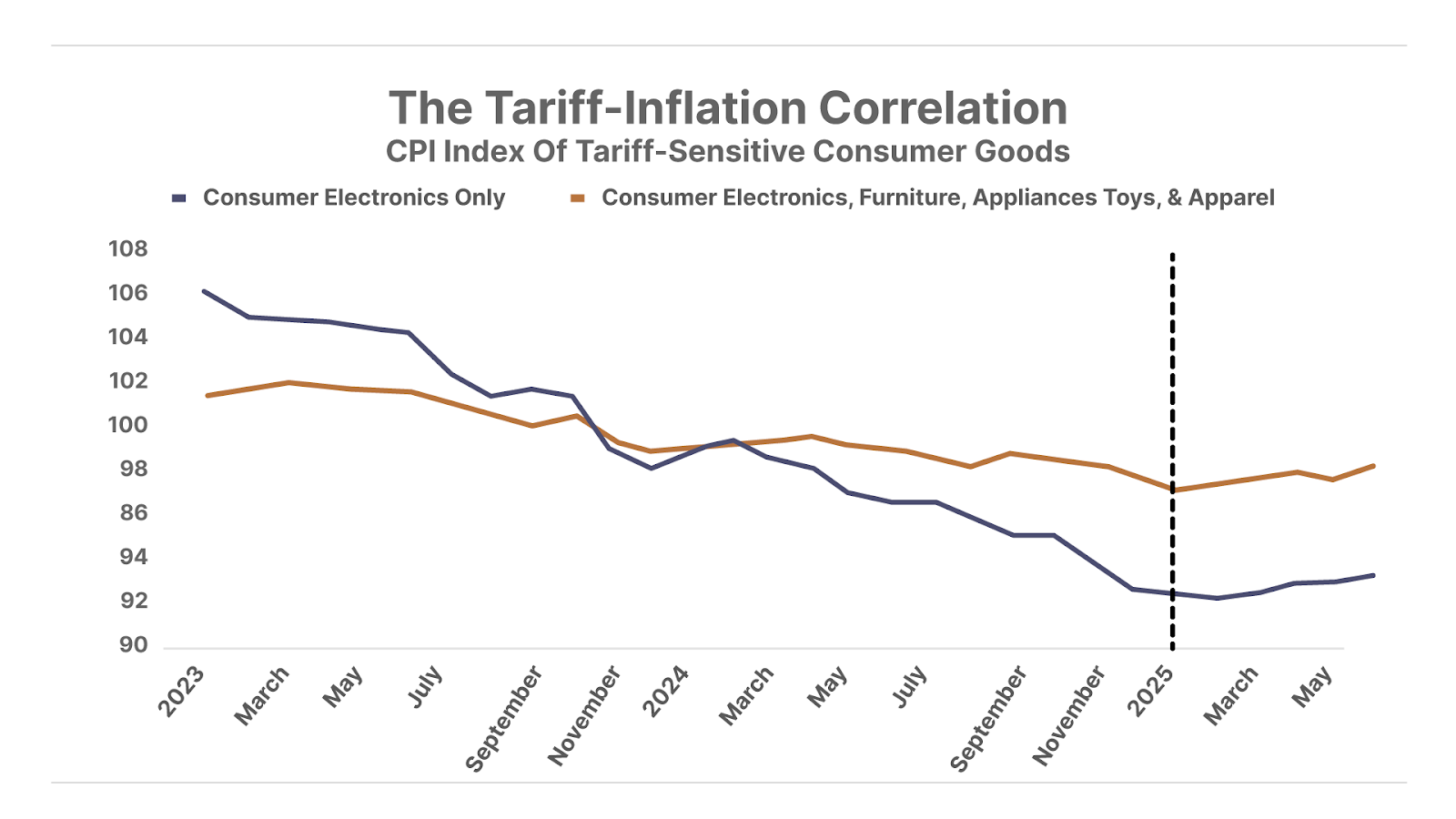

2. Tariffs boost revenue… and inflation. Tariff collections have brought in over $113 billion in revenue to the U.S. government in 2025 – an 86% year-over-year increase – enabling Uncle Sam to post its first monthly surplus in June since 2005. Still, this fiscal win comes at a cost to consumers – inflation rose 2.7% in June, slightly above the 2.6% forecast and up from 2.4% in May, driven by sharp increases in household furnishings (up 1%) and recreation commodities (up 0.8%) – the steepest gains in those categories since 2022. These two data points don’t give Fed Chair Jerome Powell any reason to cut interest rates.

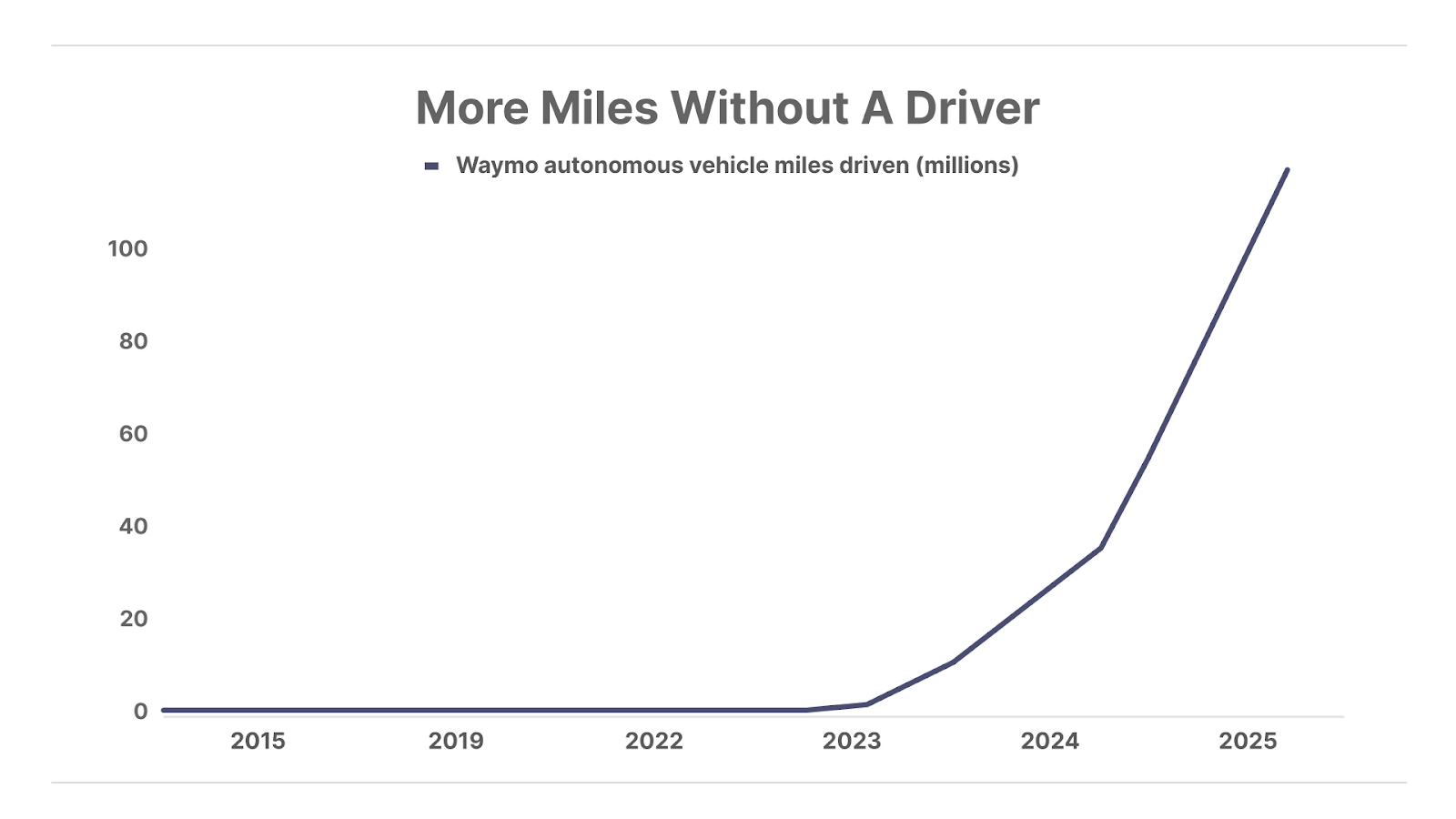

3. The robotaxi revolution has arrived. Autonomous vehicle (“AV”) ride-hailing company Waymo – owned by Alphabet (GOOG) – is rapidly scaling up its network of robotaxis. The number of fully autonomous, paid Waymo trips now exceeds 250,000 per month, up five-fold from a year ago. And the total number of rides on its network recently surpassed 100 million since Waymo became the first company in the world to offer fully autonomous trips in 2020. At this rate, robotaxis could become a meaningful portion of all ride-hailing trips over the next decade.

And One More Thing… The Trump-Powell Showdown Continues

In recent weeks, we’ve heard members of the Trump administration repeatedly berate Federal Reserve Chair Jerome Powell for both his refusal to cut interest rates and his “gross mismanagement” of the ongoing renovation of the Fed’s Washington, D.C. headquarters. This morning, the administration went even further, with an unnamed White House official saying the president is “likely to fire Powell soon.” The New York Times added fuel to the fire, reporting that Trump has already drafted a letter to fire Powell. The president has since half-heartedly denied that report, noting that it was “highly unlikely” he would fire Powell but also saying that he hadn’t ruled anything out. However, it appears increasingly clear that Trump is intent to remove Powell, one way or another. The only question is whether Powell will go quietly.

Today’s Poll – Trump Versus Powell

Tell me what you think… good, bad, or indifferent: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.