Issue #17, Volume #1

Inflation, War, and the Coming Slaughter of Millions

Three Things You Need To Know Now:

1. The “Two Americas” problem is getting worse. Most working-class Americans are suffering because of the country’s disastrous, runaway government spending that’s inflating away real wages. Car repos are soaring. Credit-card delinquency too. And, as a result, U.S. consumers have almost never been this pessimistic. (Hat tip @Kobeissilletter)

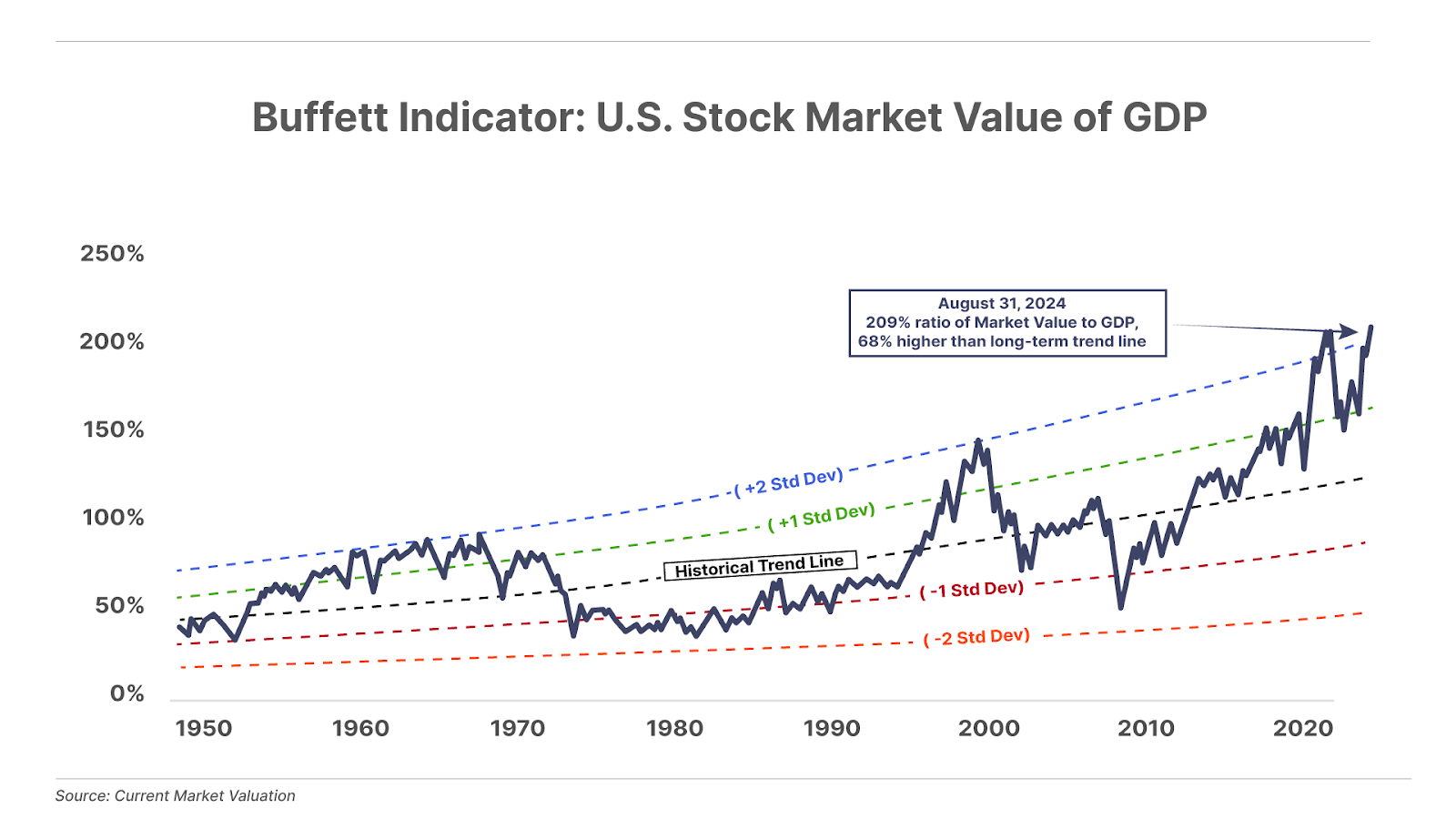

2. Meanwhile, investors (aka, asset owners) are euphoric. The “Buffett Indicator” of stock market sentiment (the Russell 5000 index / U.S. GDP) just reached a new, all-time high, at 209%, which is fully two standard deviations above the trend line. This measure of valuation shows stocks are trading at their highest relative value, ever. Not coincidentally, the amount of equity investment per U.S. household is likewise at an all-time high. And there are a host of other market indicators, like corporate bond market risk spreads that confirm investors’ beliefs that the future has never been more bright. And that’s led to big profits for wealthy investors.

Inflation means different things to different people. For asset owners, it looks like a risk-free path to more relative wealth. For wage earnings, it means poverty. That’s why, given our paper-money system, you can have economic environments that are terrible (rising debt, rising inflation, the risk of a bond market collapse, etc.) and still see equity prices soaring.

(And along those lines… congrats to Erez Kalir and the subscribers of his incredible publication, Biotech Frontiers. They just booked their second 100% gain (!) with one of Erez’s inaugural recommendations. First recommended back in January, this $5 stock quickly soared to $20, resulting in Erez selling half of the position on that original recommendation. Then, in September, after the stock fell to below his original buy price, he recommended it again. And, once again, it has more than doubled, resulting in booking additional profits. I can’t recall ever booking multiple 100% gains in the same stock, in the same year. Please: if you’ve benefitted from Erez’s work, take a minute to let us know. It will make Erez’s day to know that you’ve make huge gains from his work this year: [email protected])

3. The gold bull market is only beginning. As I detail in the essay below, there’s a very good reason why central banks have been buying record amounts of gold since COVID, including a new record buying in the first half of this year. This is not the “normal” diversification of bank assets – this is a run on the dollar. The inevitably of significant dollar devaluation and a corresponding collapse in the U.S. Treasury bond market grows more obvious by the day. Our trading partners (including the Saudis) are abandoning the dollar. That’s why I’m posting a conversation I had last week with Marin Katusa, who is the world’s foremost expert on gold trading and who has contacts at the highest levels in the gold markets. Please, don’t skip today’s essay and do not miss this conversation with Marin. There’s no better way to safeguard your wealth from the collapse of our currency.

And one more thing (from Porter & Co.’s Distressed Investing senior analyst Marty Fridson)…

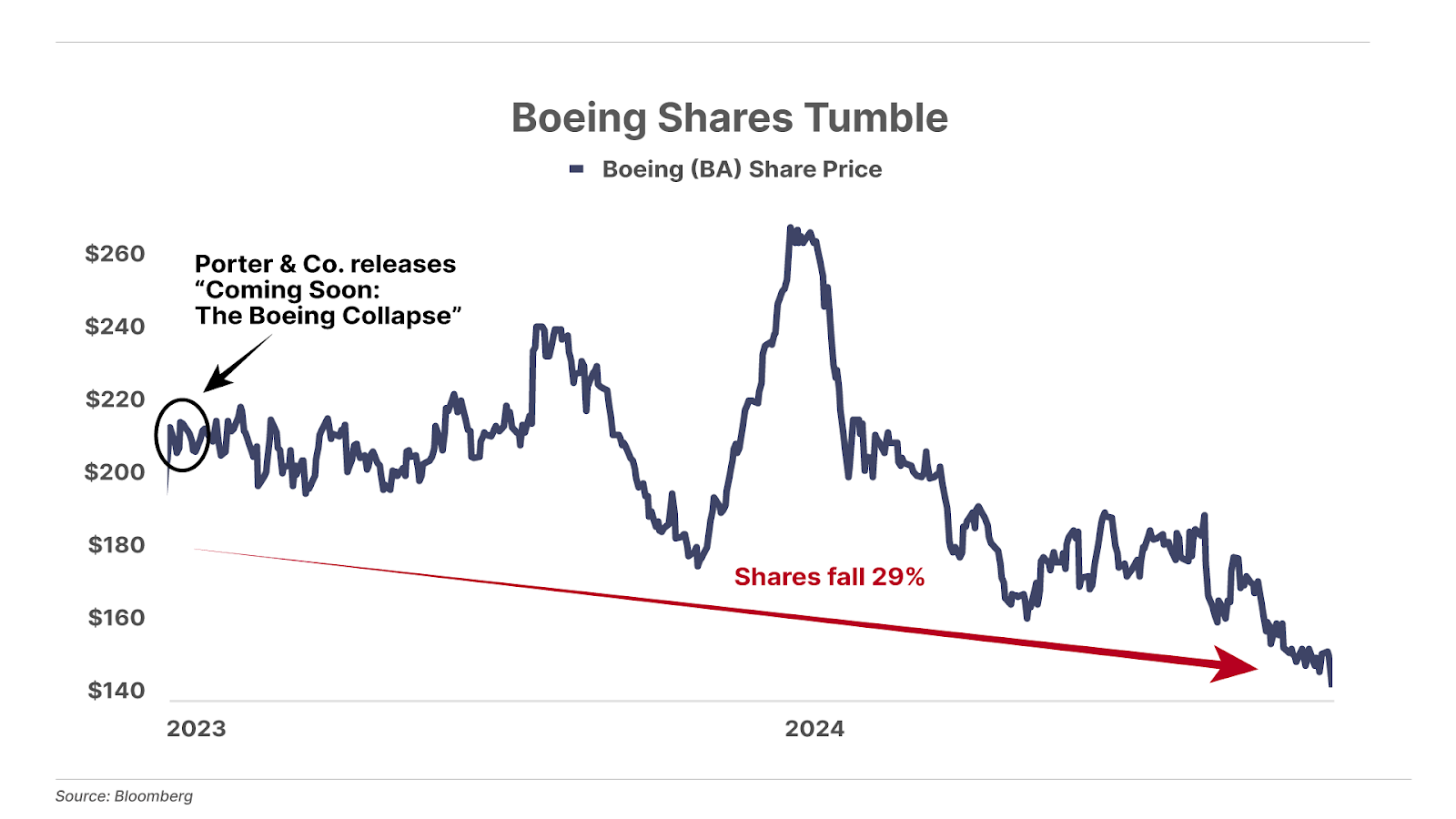

Since we first wrote in January 2023 that investors should avoid shares of Boeing (BA), the aircraft manufacturer’s troubles have worsened considerably. The Federal Aviation Administration grounded a large portion of its fleet, and then the company announced that it would reduce its workforce by about 10% and that its third-quarter loss would be larger than Wall Street analysts were expecting.

Over the past month, both Moody’s and Standard & Poor’s watchlisted the company’s credit ratings for downgrading to speculative grade, or junk. If that happens, it will compound Boeing’s problems by raising the cost of new borrowing. Boeing would be the biggest-ever “fallen angel,” a term for companies that drop below the investment-grade category into speculative grade.

Conscious of the financial pressure that a rating downgrade would create, the company has said that it expects to raise at least $10 billion in new equity, beginning now and into the next year. That may persuade Moody’s and S&P to hold off any rating action for now.

When bondholders become convinced that a downgrade is certain, they don’t wait for the rating agencies to act – they reprice the company’s debt to trade as if the rating reduction had already occurred. For the time being, Boeing’s bonds are trading at yields consistent with ratings of Baa3/BBB-, the lowest level in the investment-grade category and thus just above junk range. The market’s verdict seems to be that a downgrade is less likely than it had been last week.

But this doesn’t mean Boeing is out of the woods. The ongoing strike by Boeing employees continues to compound its cash crunch. So avoiding a downgrade to junk is no sure thing.

For potential buyers of Boeing bonds, the risk-reward would be more attractive if Boeing’s bonds were trading as if they were already downgraded to speculative grade and in line with Ba1/BB+ issues. In that case, a reprieve from the rating agencies would trigger a pricing improvement to the Baa3/BBB- level.

(Distressed bonds – the right distressed bonds – are a fantastic addition to any portfolio. And as the U.S. economy deteriorates, we’ll be entering a sweet spot for buyers of the debt of troubled companies. If you’re not already a subscriber to Distressed Investing… see what we’re talking about here, or call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447, for more information on becoming a subscriber.)

Why the Next Decade Will Look Like the 1940s, Not the 1970s

It’s like OnlyFans owner Leonid Radvinsky’s warning about the dangers of pornography.

Yesterday, the IMF (International Monetary Fund) warned the world’s largest governments that their debt levels are growing at unsustainable levels and threaten the stability of the world’s financial system.

As the IMF astutely notes, the biggest risks to the system stem from America’s out-of-control government spending, which has unleashed inflation around the world.

The Wall Street Journal provided this helpful summary of what’s happening:

Uncertainty about the future path of U.S. budget policy is likely to have a big impact on other governments, the IMF warned. Increasingly, changes in the interest rates that governments pay are driven not by changes in their own circumstances, but by changes to the outlook for U.S. budget policy and the interest rates set by the Federal Reserve.

Apparently, no one at The Wall Street Journal even chuckled at the supreme irony of the IMF calling out the world’s global economic hegemony for putting its own system of paper money slavery at risk.

Remember, the IMF was created by the victors of World War II to create a new form of monetary colonialism, with the U.S. dollar at its center. The entire reason the IMF exists is to enable governments to build up huge debts, thereby creating an endless cycle of devaluation, higher taxation, and paper-dollar dependency. When these governments inevitably end up unable to repay their foreign loans, the IMF prescription isn’t less government or sound economics: it’s to raise taxes and devalue the local currency. This further entrenches corrupt governments, while transferring trillions in value from these countries into the dollar-based global financial system. Since the Great Financial crisis, the IMF has spent $540 billion on “bailouts” to 90 countries.

If you’re tired of the U.S. government printing away the value of your wages and your savings, imagine how the people of Pakistan must feel. They’ve been “gifted” with IMF bailouts 23 times over the last 75 years.

And pity the Argentines. Over the past 63 years, Argentina has been the IMF’s biggest “customer” with 21 separate loans, including the largest loan ever disbursed, $57 billion in 2018.

Prior to Argentina’s involvement with the IMF, its citizens enjoyed real per capita income higher than most of the developed world, including its former colonial master, Spain. Service to its new colonial master, the IMF, hasn’t gone as well.

On a constant-dollar basis, Argentina is now much worse off than when it joined the IMF in 1958.

In this way, the resources (and the people) of Argentina, and the entire world, have been profitably exploited by the West.

The value that’s constantly stolen by all the world’s governments via inflation ends up being converted into dollars and deposited in major western banks. Most of the world grows constantly poorer, relative to the West, as a result.

This system is virtually identical, economically, to the British Empire, which it was modeled after. However, rather than the pound sterling being the reserve currency into which value flows following World War II, the reserve currency has been the dollar. And the dollar is about to die, just like the British pound did, in an orgy of inflation, devaluation, and violence.

The first major challenge to the dollar’s hegemony came during the 1960s.

During the 1950s, rather than enjoying a “peace dividend,” the U.S. embarked on the largest buildout of military might in history, spending 20% of GDP on the military for most of the decade.

We did so mostly because of very effective propaganda. Americans were convinced that a bankrupt and destroyed communist nation that was so poor it later had to import grain from us, threatened our existence. It’s laughable – but the “Red Menace” dominated U.S. politics for the next 25 years. People will believe anything.

Russia, which lost almost 30 million citizens during World War II, might have been an “evil empire,” but it was a feeble empire as well, both economically and militarily. It didn’t have a single aircraft carrier. Or a single nuclear-powered sub. By 1960, Russia had built four (yes, four) nuclear weapons that were capable (maybe) of reaching U.S. territory. Nothing in the USSR worked, including their tanks, as we well knew from our U-2 spy plane overflights.

But our politicians campaigned throughout the 1950s by lying about a “missile gap” and the supposed dangers of the “Reds.” Such lies led to our involvement in dozens of civil wars, in places most Americans couldn’t find on a map, and the absurdity of our nuclear buildup: we’d go on to stockpile thousands and thousands of nuclear warheads, with enough explosive power and toxic nuclear radiation to destroy every city in the world hundreds of times over.

Thus, instead of paying down the debts of World War II (the largest in our country’s history), the government’s total debt continued to grow rapidly through the decade – by more than 50%. We were firmly on our path to Empire status, using more and more debt to power more and more military spending. These large debts (and the continuing deficits of the 1960s) led our trading partners to exercise their rights under the Bretton Woods agreement to exchange dollars for gold at the fixed exchange rate of $35 per ounce.

By the early 1960s, with our creditors all demanding gold, we set up swap lines with other central banks to control the peg to gold. U.S. President John F. Kennedy, like all politicians, promised not to devalue the dollar – famous last words. But when the central bank’s “gold pool” failed in 1968, more than half of our gold left the country. Finally, President Richard Nixon defaulted in 1971, ending the dollar’s tie to gold and beginning a long period of substantial inflation, which the government used to inflate away its debts.

The only reason the dollar standard was preserved was because of America’s military might.

In 1974, after the stock market had collapsed by more than 50% and during a 50% collapse in U.S. Treasury bonds, we made a secret agreement with Saudi Arabia to save the Treasury bond market. This so-called “petrodollar” agreement assured that oil (the largest global commodity) would only trade in U.S. dollars and that there would be a constant bid for U.S. Treasury bonds, as the Saudis agreed to invest their oil profits in U.S. bonds.

In return, we guaranteed the Saudi regime’s power. (While we were willing to fight for human rights and democracy in Soviet Russia, we weren’t so interested in doing the same for the Saudis… ironic isn’t it?)

What happened when one of the Gulf states decided to sell oil in a currency other than the dollar? In 2001, Iraq decided to exchange its oil for euros under the UN’s “oil for food” program. Soon Iraqi President Sadam Hussein was hanging by a U.S.-tied rope.

Today, with America as the world’s leading oil producer (and with Saudi Arabia a debtor nation), the petrodollar agreement isn’t what’s important. What is important is that the world’s central banks continue to settle trade, of all kinds, by using the U.S. dollar and the U.S. Treasury market.

Why? Because without this “bid,” the American economy would collapse, overnight.

There’s no other way to finance the enormous growth of our government’s entitlement programs and interest payments. And it’s not even close.

Total annual U.S. savings are about $900 billion. The deficit this year will be $2 trillion.

So, even assuming 100% of domestic savings went into Treasuries (which is impossible), we’re still $1 trillion short to finance just this year’s deficit.

These deficits can’t be contained because they’re driven by increases to mandatory transfer payments. So, we must have foreign buyers of Treasury bonds. The trouble is, much like in the 1960s, the rest of the world is looking at our economy, our military aggression, and our balance sheet and saying: “No thanks. I’ll take the gold.”

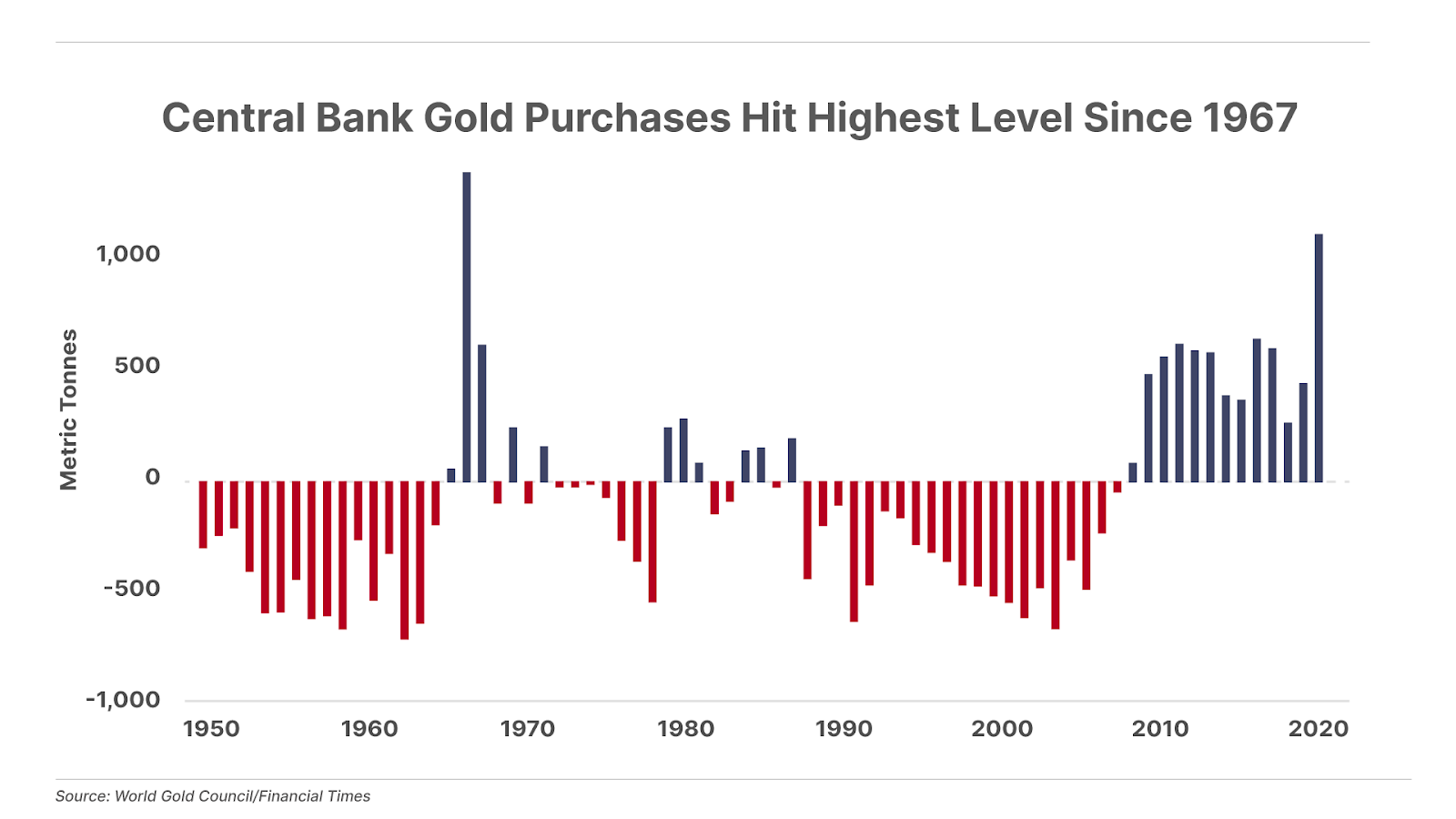

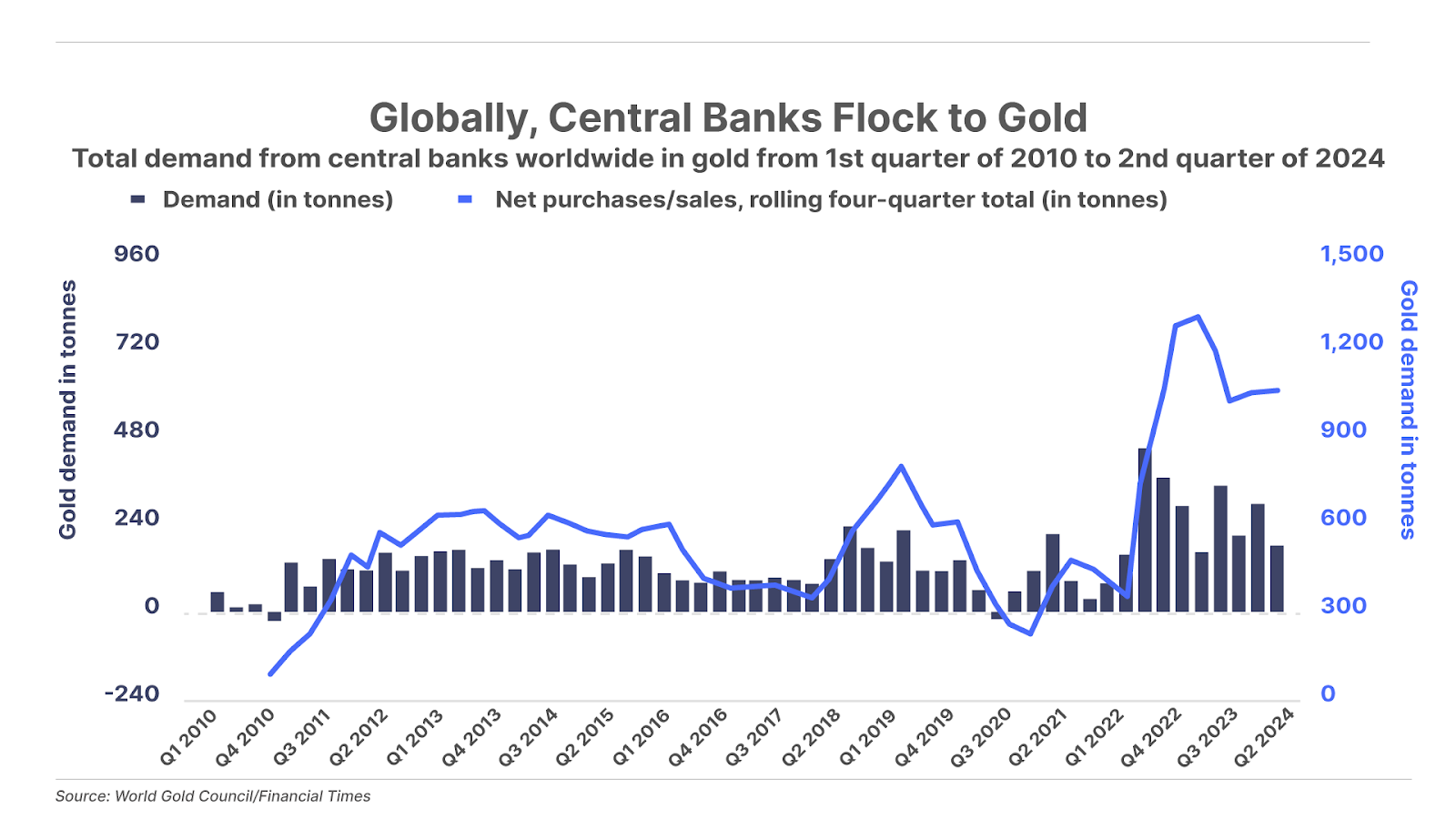

Central-bank gold buying, which has grown steadily since the Great Financial Crisis, increased enormously after COVID, with central banks buying more than 1,000 tons in both 2022 and 2023. So far in 2024, demand is surpassing those record amounts, with 483 tons purchased in the first half of 2024 – a new record. Who is buying? The countries that have firmly rejected American hegemony: China, Turkey, Poland, and India, most notably.

Empires are built with economic systems that enrich societies, allowing for the creation of military might. They die when those militaries consume more wealth than their economic systems can create. And they die violently.

The British Empire and its economic hegemony didn’t collapse after the disastrous stalemate of World War I – despite its enormous expense. It collapsed because in the face of these huge debts, it abandoned free trade, adopted socialist policies, raised taxes, and devalued their currency. And what the British could no longer afford by trade, they tried to retain with force. They tried to guarantee Poland’s sovereignty in the face of Russian aggression. There was no way to win that fight – or to afford it.

Wars aren’t good for empires. Or their bond markets.

Today, America, impoverished by both its enormous Cold War debts (which have never been repaid) and its own version of communism (its nonsensical domestic transfer programs and massively progressive tax system) is attempting to guarantee the sovereignty of Poland (I mean Ukraine… I always get them mixed up)… in the face of naked Russian aggression.

Gee, I wonder how this will all play out?

Throw nuclear weapons into the mix, war with Iran, and the fact that Americans have never been more violently political (as defined by the number of assassination attempts against a presidential candidate), and I think this essay won’t merely be prophetic.

It will be wildly wrong because it underestimates the chaos, violence, and destruction that we’re about to experience.

One thing is for sure: the U.S. dollar standard will not survive. Our creditors have seen what the IMF is warning about: a projected U.S. 10-year deficit of more than $30 trillion, which implies a doubling of our total debt issuance in the next decade.

The market will soon be “no bid,” as no rational creditor will step in front of that amount of issuance. And, according to some reports, the Saudis have officially ended the petrodollar agreement, which means oil might soon be priced in many different currencies.

And what does the IMF recommend?

Says The Wall Street Journal:

According to the Fund, there is scope to increase tax revenues in both the U.S. and the UK, where they are at a relatively low level as a proportion of economic output compared to rich-country peers. In the U.S., the IMF sees room to raise revenues from sales taxes, as well as taxes on higher incomes.

As always, the IMF recommends more government.

It would be funny, if it wasn’t such a tragedy.

So, beat the rush: make sure to watch my conversation with legendary gold investor Marin Katusa.

Good investing,

Porter Stansberry

Stevenson, MD

P.S. Next week, Porter will interview best-selling writer Michael Lewis – author of Liar’s Poker, The Big Short, Moneyball, and most recently Going Infinite about Sam Bankman-Fried and FTX – at the Stansberry Conference on October 21-22. Tickets to attend in Las Vegas are sold out. But access to livestream Porter’s discussion with Lewis – and the full lineup of speakers – can be purchased through October 18.

From the comfort of your own home, you can watch – live, as if you were at the Stansberry Research conference – great financial thinkers such as futurist and former OpenAI exec Zack Kass, baseball analyst Billy Beane, Retirement Millionaire editor Doc Eifrig, leading real-estate investor Ronan McMahon, and others. In addition to being able to watch live, you also get high-quality video files, summaries, and presentation materials that you can review at your convenience – over and over again… whenever you like…

Of course, the highlight of the conference, which you can watch live, is Porter’s discussion with author Michael Lewis on topics ranging from the bond world depicted in Liar’s Poker to what Lewis learned about crypto markets and what Sam Bankman-Fried was doing with FTX… and with Porter asking the questions, you know it will be a fascinating exchange. Go here to be able to watch Porter interview Michael Lewis, all the other speakers, and receive videos and notes from the entire two days.