| Welcome to Porter & Co.! If you’re new here, thank you for joining us… and we look forward to getting to know you better. You can email Lance James, our Director of Customer Care, at this address, with any questions you might have about your subscription… The Big Secret on Wall Street… how to navigate our website… or anything else. You can also email our “Mailbag” address at: [email protected]. |

This is Porter & Co.’s biweekly The Big Secret on Wall Street for paid subscribers, in which we review our portfolio of recommendations and highlight the “3 Best Buys” that we believe offer the most compelling opportunities at current prices. You can see the latest issues of The Big Secret, and our full archive, here.

We have included a free preview for non-paid subscribers below. If you’re not yet a subscriber, to access the full paid issue, the portfolio, and all of our Big Secret insight and recommendations, please click here.

Every broker in the financial-industrial complex will be announcing their forecasts of which sectors of the market will win and which will lose under the incoming Trump administration. Ignore them… they aren’t worth the paper they’re written on (along with most everything else they tell you!). The reality is that the conventional wisdom about this – as with much else in life – is mostly wrong.

For example… in 2016, the big idea was that Trump would be great for the U.S. oil industry (drill, baby, drill!). But the performance of shares in the oil sector was abysmal. The energy-sector component of the S&P 500 index returned negative 30% during Trump’s first presidency versus an 83% gain in the overall S&P 500.

Likewise, Joe Biden was supposed to kill America’s fossil fuel industry while boosting the fortunes of the electric vehicle (“EV”) and solar power sectors… Instead, energy stocks have returned 149% under Biden and oil production set new all-time highs. Meanwhile, exchange-traded funds that track the EV sector returned negative 14% and solar stocks returned negative 68% during the Biden administration.

Thus, history says to ignore the talking heads and their forecasts about how new presidential administrations might impact the different sectors in the stock market. It’s a losing game, and one we chose not to play. Instead, we’ll continue doing what we know works – tracking the earnings and growth prospects of individual businesses that we can understand.

And despite the wave of enthusiasm sweeping through the markets following Trump’s electoral victory, back on the earnings front, there’s reason for caution.

Corporate America is waving a warning flag in their latest financial reports, and the smart money is taking note.

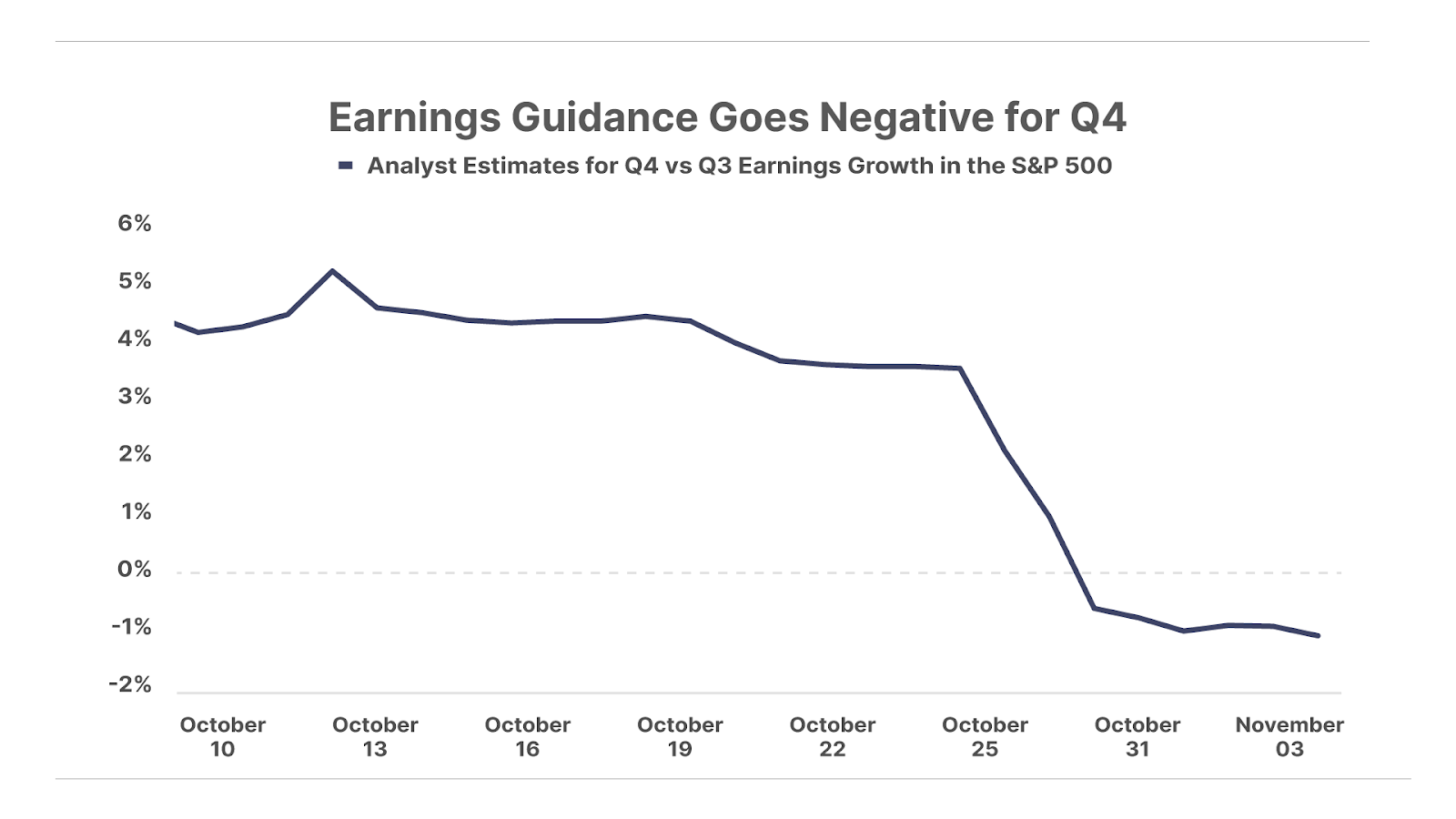

Over three-quarters of S&P 500 companies have reported Q3 numbers, with the aggregate index-level results at about $63 in earnings per share for the S&P 500. That’s up 9% year-on-year (“YOY”), and 5% quarter-over-quarter, continuing a trend of robust earnings growth over the last five quarters. But as we discuss below, this good news is now behind us, and the trouble lies in what comes next.

More than twice as many S&P 500 companies have warned of a drop in Q4 earnings versus those calling for continued growth. Analysts are penciling in a 1% drop in S&P 500 earnings from Q3 to Q4, a dramatic reversal from expectations of 5% growth just a few weeks ago:

And as we’ve noted in Porter’s Daily Journal, in recent weeks, analysts have likewise begun lowering their earnings outlook for 2025. Here’s why this stalling earnings momentum is a big problem for investors in the overall stock market…

Since the S&P 500’s low of 3,500 in October 2022, the index has gained more than 60% to 5,700 today. Over that same period, the trailing 12-month earnings per share for the index have increased by just 5% from $222 to $234. That means most of the price gains over the last two years have come from investors paying more for each dollar of earnings, rather than earnings growth. Since October 2022, the S&P 500’s price-to-earnings (P/E) ratio has inflated from 17x to a near-record high of 26x today.

With the earnings outlook dimming, any further gains can only come from investors continuing to pay ever-higher valuations. For perspective, the S&P 500’s valuation peaked at a 30x P/E ratio in 2000 during the height of the dot-com bubble. That means we are only 15% away from the valuation peak that preceded one of the sharpest declines in stock market history.

Another factor is that retail investors have already gone “all in” on the market – and therefore have little scope to pour more money into the market.

While retail investors are rushing into the stock market at near all-time high valuations, the “smart money” – institutional investors – is running in the opposite direction. According to Bank of America’s regular report on institutional investing, there were $6 billion in outflows from the U.S. stock market during the week ending October 25. That’s the largest selling spree in eight years, and the second largest in the bank’s data going back to 2010:

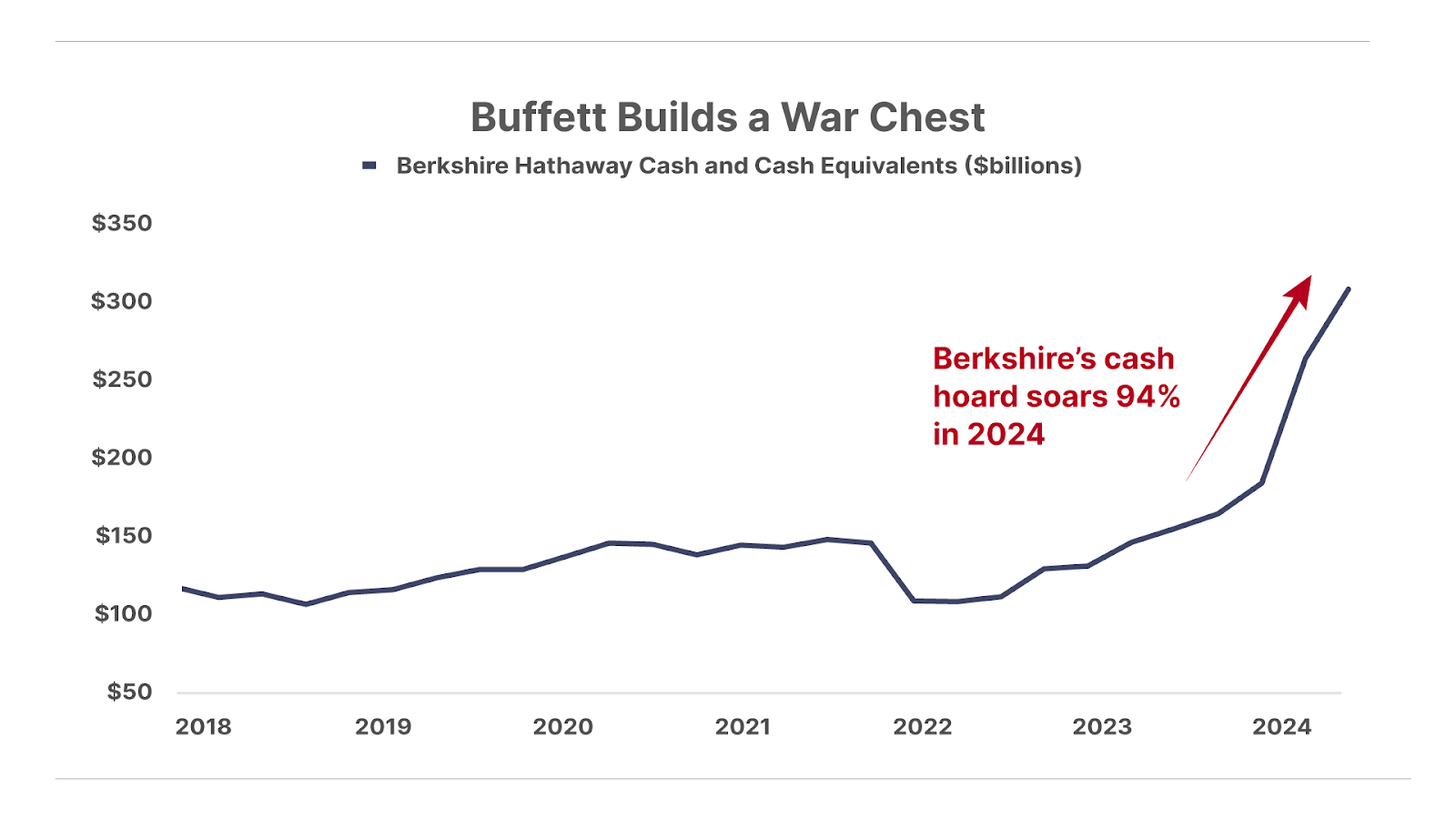

This includes Warren Buffett, who is cashing out in a big way. Berkshire Hathaway (BRK) revealed in its Q3 financial report on November 2 that Buffett continued a stock-selling spree that’s now gone on for eight consecutive quarters. The company also reported no repurchases of its own shares for the first time since 2018.

In total, Berkshire liquidated $34.6 billion from its stock portfolio in Q3. This brought the conglomerate’s cash holdings up to a record high of $325 billion, up 94% year to date.

So who’s on the right side of this trade – the mom-and-pop crowd going all in or Buffett and other institutional investors cashing out?

Our money is on Buffett, and we remind readers of his sage advice to “be fearful when others are greedy, and be greedy when others are fearful.”

Regardless of what changes an incoming Trump administration might implement, we believe it’s only a matter of time before greed shifts to fear, and prices fall by 50% or more. Those who raise cash now, like Buffett, will be in a position to buy world-class businesses at bargain-basement prices.

In the meantime, even in today’s generally overvalued stock market, bargains can still be found. In this portfolio update, we’re reviewing the latest corporate results from five companies in The Big Secret portfolio that we believe offer compelling value at current prices.

Four of these companies trade at significant discounts to the S&P 500, ranging from 25% to 50%, while their earnings grow at rates well above that of the index. We’re raising buy prices on two of these companies, while adding another into the top “3 Best Buys” section of the portfolio.

This content is only available for paid members.

If you are interested in joining Porter & Co. either click the button below now or call our Customer Care team at 888-610-8895.