Editor’s Note: This month our Spotlight has been on the brilliant Tom Dyson and his equally-brilliant partners at Bonner Private Research, Dan Denning and Bill Bonner.

In their first Spotlight, Tom recommended the beaten-down Israeli cargo firm, ZIM Integrated Shipping, writing:

“Much can go wrong with this idea between now and the rest of the year, especially if the Red Sea opens up to shipping again. But given Zim’s massive cash position, we have a big margin of safety here. The recent pullback in ZIM’s stock is giving us an excellent entry point to take a position.

Since then, it’s up by more than 30%.

In his second issue for Porter & Co., Tom introduced our readers to the VanEck Emerging Market Local Currency Bond ETF (EMLC) as a way to protect against the continued decline of the U.S. dollar.

But for our final Spotlight, the guys are pulling out all the stops.

Below you’ll find their analysis into what Tom, Dan, and Bill call the greatest financial experiment of all time. And it’s their #1 trade for protecting and growing your wealth during this experiment.

This isn’t any trade, either… it’s what they call their “trade of the decade.”

Each decade, Bill Bonner and his partners release a trade of the decade – a big, macroeconomic play that they believe will produce market-beating returns over the next 10 years.

The first trade of the decade spanned 1999 to 2010, and it was exceptional: Dow down, gold up. The second was from 2010 to 2020, and in Bill’s own words in his conversation with Porter:

Bill: I was buoyed up by the brilliance of my first 10 years so I decided to go for Japanese stocks. Japanese stocks at that time had been going down for 20 years. I thought, “God, they can’t go down forever.”

Porter: They went down for a little bit longer.

Bill: They went down a little bit more. It was too clever. I was buying Japanese stocks and selling Japanese bonds because they had been going up for 20 years.

Porter: And they finally did crash.

Bill: Everything worked out. But it worked out not quite as well as I wanted and it took a little bit longer than I wanted.”

Below, you’ll find the third Trade of the Decade from Bonner Private Research, and why they believe this is the best time to enter the trade since they first issued it more than four years ago.

Before you continue though, make sure you go here to see the special offer the team at Bonner Private Research have set up exclusively for Porter & Co. readers while it’s still available.

Our desk is in panic, my phone is on fire, and the performance we’ve been building toward our year-end bonuses for months has collapsed in just one month. All my analyst and trader friends are losing their minds, several are sending me pessimistic DMs on Twitter and my wife and I are arguing. Beautiful oil market lol

– Anonymous oil trader, posting on X, as crude sunk below $66 per barrel last week

I’m out boys. Liquidated everything. I’m done with oil stocks after 10 years of stress & miserable returns. Wish you all the best, but at this point in my life, I don’t need the aggravation. Yes, I too am sure this marks the bottom, but so be it. Will put the cash into VOO.

– Another anonymous oil trader, posting on X last week

Welcome to a front row seat for the Greatest Financial Experiment of all time.

Each new intervention leads to greater distortions, bigger malinvestments, and even more distance from equilibrium. Gold is the fire alarm.

The Fed cut interest rates 0.5% last week, to 4.75%, with the cost of living still inflating, asset prices at all time highs and full employment. Remember how reluctant they were to hike interest rates when inflation first erupted in 2021? Now look how quick they are to cut. There’s an obvious bias.

It’s easy to understand Fed moves if you view them through one simple lens (they’ll never admit to this publicly):

The Fed’s job is to make the Treasury look solvent. Or said another way, the Fed exists to finance the government’s wars.

As you can see from this chart of the government debt presented by maturity date, which comes from the Treasury’s Monthly Statement of the Public Debt via X, the government loves to borrow short term money. About one third of the total public debt outstanding is ultra-short term and adjustable rate debt.

This means the Treasury is on a never-ending treadmill for rolling over its debt. Because of this great maturity wall, and the fresh debt it’ll issue, the Treasury will have to auction more than $10 trillion in bills and notes over the next twelve months… and then again every following year too! Quite a burden.

So by cutting interest rates this week, the Fed immediately reduces the government’s interest payable, and takes a little pressure off the government’s finances.

(And we get a lower interest rate on our T-bill investments.)

If the Fed has to finance the government, then the Fed has no way to defend the purchasing power of the currency. (They’ll never admit this either.) So the expected after-inflation, real returns from longlife assets like stocks and bonds look terrible to me.

We don’t know how the next step of this Great Financial Experiment plays out. But we’re positioned for extreme outcomes.

Our strategy remains the same. We’ve got the dial set to “Maximum Safety.”

First, avoid all bonds and the major stock market averages. They seem to have terrible long term inflation-adjusted return prospects.

Then, own a hedged portfolio of a) precious metals, to protect against currency debasement b) high yielding shipping, energy and commodity stocks to earn a little inflation-protected income if the economy keeps expanding, and c) a pile of cash to protect against falling nominal prices in case there’s a growth scare.

Here are four decades of commodity prices, adjusted for inflation. It’s a story of three acts: a bear market in the 80s and 90s, a bull market in the 00s. And then another (more volatile) bear market starting in 2008.

(I’ve used the Goldman Sachs Commodity Index here, an index of 24 commodities with a 61% weighting to energy.)

The big picture is, billions of people from Africa, South America and Asia are aspiring to consume more commodities, more energy, and more meat. They want motorcycles, tuk tuks, washing machines, air conditioners, microwaves, and refrigerators full of fresh food, like we have.

And now, with the help of China as a trade partner, the new BRICS trading bloc, the petroyuan and physical gold (a neutral reserve asset for storing trade surpluses) this demand gets unlocked.

I’m not worried about demand for commodities. It’s massive. Meanwhile, society hasn’t invested enough in commodity supply.

Bottom line: I’m bullish on commodity prices, and whenever commodity prices dip, like now, we need to start buying.

(If you haven’t entered our Trade of the Decade (long energy, short dollars), which we’re expressing with the SPDR Oil and Gas ETF [XOP], this is the best time to get into the trade since we launched the idea at the beginning of the decade.)

As Investment Director, I’m always trying to see around corners… to handicap the future and place good bets with our savings. That’s all our long term investment strategy is… my attempt to preserve our wealth and the purchasing power of our savings through a period I think will feature a chaotic deleveraging, and a collapse of paper money’s purchasing power, all at the same time.

It’s all I think about.

I wish I could tell you to go “all in” on one asset class and then close your computer for ten years. But that’s not the way. Instead of trying to forecast the future and then placing one big bet, we’re trying to handicap the different outcomes and then tweak our bets like a bookie adjusting his lines the morning before a big race.

In the short term, we have been navigating by using a simple model with three camps — hard landing, soft landing, and no-landing boom.

Earlier this year, we observed week after week how almost all investors had moved to either the ‘soft landing’ or the ‘no landing’ camps. And almost none had stayed in the ‘hard landing’ camp.

I wrote this five months ago, for example…

I’ve noticed the “hard landing” and “recession” camp has really thinned out lately. Instead, the “no landing” and “runaway inflation” camp has become very crowded.

Call it a cognitive habit acquired over many years of speculating, but I always try to keep ahead of the crowd. You don’t find profit by being in the crowded trades. You profit by anticipating where the crowd will go next. It’s hard. But it gets a little easier with experience.

We then tightened the stop losses on our shipping and energy stocks… and braced to stop out of many of our trades.

Fast forward five months. We’ve seen the triggering of the Sahm Rule, a crash in the Japanese stock market, the un-inversion of the yield curve (a classic recession indicator), decelerating inflation, and the return of “risk off.”

Over the summer, we stopped out of 12 positions – all shipping and energy stocks – representing 95% of the positions on our Official List.

The five signallers of risk appetite — copper, interest rates, crypto, oil and the Japanese yen — have all been falling this summer. Even Nvidia is down 23% from its peak.

And of course, today we find many investors have joined us in Camp Hard Landing.

I’m always trying to stay two steps ahead of the crowd. Recently, we pivoted again. Now that the Fed is going to begin cutting interest rates, and the M2 Money Supply has started rising again, it’s time to assume we’re entering a weak period for the dollar.

Two weeks ago, I told you about a container shipping stock Zim Integrated Shipping [ZIM.]

Then last week, we introduced the Vaneck emerging market local currency bond ETF [EMLC].

It’s currently paying $0.13 a month, which is a 6.3% dividend at its current price.

Instead of keeping 100% of our allocation to cash in developed world currencies (for most of us, US dollars), we’re now going to diversify our cash holdings into a broad basket of emerging market currencies, and earn an even higher interest rate. (EMLC currently pays a 6.3% yield.)

I’m not introducing any new ideas today. But I’m not done shopping yet either. Any time the market offers us a good entry point, I am intending to bring some of the energy and shipping ideas we’ve been following since Covid back into our official coverage… and continue reducing our cash balance.

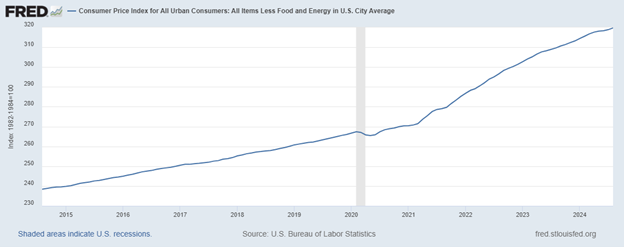

They published the August inflation print earlier this month. It looks to me like inflation slowed down for a bit at the beginning of the year but is now accelerating again.

This ten-year chart shows the absolute level of the Core CPI (minus food and energy), the inflation series that the Fed pays most attention to. Pay attention to the slope of the chart in recent months. It clearly looks like inflation is beginning to accelerate upwards again after the line briefly flattened.

I’ve been thinking about EMLC since we introduced it to our strategy last week. It’s going to be a useful tool for us. What return can we expect from EMLC? I’m hoping to make a return of around 7% a year, in dollars. The dividend is 6.3%, so in short, I’m happy if EMLC continues to trade between $24.50 and $25, and all our return comes from its dividend. This will represent a win for us, because we’re only making 5% on our deposits in short term government bills.

EMLC is a cash equivalent with a high interest rate. Please don’t expect much of a capital gain… unless the dollar starts dropping against emerging market currencies, in which case we could make some capital gain.

Please send your questions to [email protected] or drop them below this article in the comments section. Please note, I’ll do my best to answer your questions, but I can’t give personal investment advice…

QUESTION: My concern with EMLC is its exposure to future Chinese and Brazil communist government confiscation of U.S. assets. Are there any other funds that do not have exposure to communist government confiscation?

MY RESPONSE: Let’s think this through for a second. We’re lending our capital to the governments of Brazil, China and about seventeen other governments. EMLC has a 10% exposure to Chinese yuan, and a 9% exposure to the Indonesian rupiah and an 8% exposure to Malaysian ringgit. These are its biggest three currency exposures. You’re afraid they won’t pay us back in full, with interest? That’s called a default and throughout history, it’s happened quite frequently, especially in the 80s and 90s.

The thing is, there’s a strong incentive for these countries NOT to default, because it destroys their access to international debt markets. Take China for instance. If this BRICS alliance is going to work, it’s critical that China has a strong currency so that other countries will be willing to use its currency in trade. Is it any wonder that the Chinese government is not bailing out its stock market or property developers? But instead, its bond market is the strongest in the world, at all time highs.

My assertion is the script has flipped. Emerging markets are now the good credits. And developed markets are now the bad credits. Japan and the UK are just the latest examples of bad government credits… both developed markets. And eventually, it’s going to be the US government causing a debt crisis. So I now have more confidence that the Emerging Markets will pay us back than the Developed Markets. I still prefer gold over both, but EMLC looks like a good home for a portion of our liquid cash assets.

QUESTION: I appreciate and understand your recent “weaker dollar trade” and how that comes out of cash allocation, rather than stocks. It’s an exciting recommendation, even though you generally warn us away from bonds. It did cause me to realize though, that I don’t understand the “cash” allocation parameters as well as I thought I did. Can you elaborate?

MY RESPONSE: Good question. Strictly speaking, cash is no one else’s liability, and doesn’t pay any interest. As soon as you deposit cash into the bank, it becomes the bank’s liability and you start earning interest, so it’s not really cash anymore. It’s a demand deposit, which means you can have it back anytime you want, which for most people, means “as good as cash.” Are T-bills cash? No. They’re a loan to the US government. But they’re so liquid, you can exchange them for cash whenever you want. So as short-hand, I call them cash, even though they’re not.

Is EMLC cash? No, definitely not. EMLC invests in bonds issued by emerging market governments like Brazil, Thailand, Colombia, China, Turkey etc. While T-bills are loans that by definition mature in less than 12 months, some of the bonds EMLC owns won’t mature for five or seven years.

Perhaps we’d be more correct to use the term “liquidity” than “cash” for our T-bill or EM local currency bond holdings. But I’ll probably just keep using the term “cash” for short. The important quality of these assets is, we can convert them to cash whenever we want at — or close to – par value.

QUESTION: My question relates to Bullionvault as a place to gain direct exposure to PMs. I opened an account with them and have a small starter position, to diversify away from the other bullion shop I use. I pulled up though when I realized that I can’t take physical delivery of the gold that I have with them (can only take delivery if you’re a UK customer). Isn’t that a problem? I thought the whole idea of having a bullion account in an offshore location (I’ve elected to buy physical gold stored in Singapore) was so that one could fly there and collect their hard money? What am I missing?

MY RESPONSE: You don’t use a service like BullionVault as a way to take possession of physical gold. It’s just not an efficient way for retail investors to take physical possession of precious metals, as you’re discovered. The best way to take possession of physical metal, is to buy from a dealer. There are many out there… from your local coin shop, to the big online gold retailers. Then it’s up to you how you secure your metal.

BullionVault and other vaulting services are useful for owning physical gold when you want to own physical gold but you don’t want to take possession of it. They’re depositories, not retailers.

QUESTION: I have not bought any gold. Is it too late?

MY RESPONSE: No. It is not too late, but I sympathize with you feeling that way as you look at the chart. I’m as excited about gold’s future returns as I’ve ever been. One way to think about it, which might make it easier to buy gold at $2,500 an ounce, is to think of gold as money. And the price isn’t the price of gold, but the price of the USD. Start by going to an online gold retailer and ordering one gold coin. The premiums are low. For example, I see one coin store offering Kruggerands for $7 over spot. Another store is offering Maple Leafs for $20 over spot. These are the best prices I’ve seen in years. Once you’ve broken the ice, you’ll find it easy to keep going.

QUESTION: You guys already have a gain of 112% in XOP, the Trade of the Decade, so do you expect future gains at the current price?

MY RESPONSE: Yes.

QUESTION: I do not have any physical gold or silver because then what do I do, put it in a safety deposit box? It seems to me from meager research I’ve done that there is a substantial commission when buying or selling physical gold and silver. I have GGN, PHYS, SA and TFPM as my precious metals. Do you think this is as good as physically holding precious metals?

MY RESPONSE: Yes, you put it in a safety deposit box, or a home safe, or bury it in the backyard. I’m an impulsive person. I find it hard to hold a position long term in an online brokerage account, when I can sell it with two clicks of a mouse anytime I open my computer. I’ve tried so many times, and I always end up selling too soon. Holding physical gold, on the other hand, is like owning a house. Most of the time, selling it never even crosses my mind. I’ve owned physical gold for years and never sold an ounce… or even wanted to.

It’s true that the commissions are a little higher when you take possession of physical gold in coin or bar form. But the payoff, in my opinion, is absolutely worth it.

Now if you don’t have this problem of impulsive trading, then you can ignore this message and continue holding gold in your online brokerage account.

QUESTION: Did I understand you to say that you’ll eventually have half of your liquid cash invested into EMLC? That seems like a huge position size for just one ticker, and very risky. Especially since you said you could be wrong about the weak dollar trend in terms of foreign currencies. Why did you rate this trade at such a low risk level of 1.5, and with no stop loss? Don’t you feel that since this is still the stock market that you could lose 50% of your cash stack overnight from some sort of crash? And comparatively, wouldn’t a T-bill or CD prevent this type of catastrophic loss? You’re the one who trained me to ask myself these types of questions when trying to avoid “the big loss”. What am I missing?

MY RESPONSE: Yes, I’m intending to move half our cash holdings into EMLC, which would be a very large position. But remember, EMLC isn’t a company or a single stock. It’s a fund holding local currency Emerging Market government bills and notes and it’s very stable. Even during the Covid panic and liquidation, from top to bottom, it only lost 12% as the dollar spiked. The biggest risk to EMLC is a soaring US dollar, which is possible but doesn’t seem likely anymore. And of course, we’ll still hold a big position in T-bills as a hedge.

QUESTION: Your thoughts on artificial intelligence investments would be appreciated. I feel like I’m missing the boat.

MY RESPONSE: Here at Bonner Private Research, we don’t know anything about artificial intelligence. We don’t even know if it’s a real thing. But history is pretty clear on this… these great investment booms usually don’t work out so well for initial investors.

QUESTION: Who is all the debt owed to and why can’t the debt be simply canceled, that’s what the broke Roman Senate did a couple of times as their empire slowly collapsed. The lenders lose their money but the debt disappears?

MY RESPONSE: In very general terms, the debt is held by those who control the world’s wealth. The same pool that holds all the other assets, too. Debt securities are assets, which means they’re just another form of wealth… unless, of course, the borrower doesn’t pay the loan back, in which case they’re a wealth mirage.

Our big hypothesis is they blew a giant wealth bubble, based on paper money, by inflating both debts and the assets collateralizing the debts. You could call it a “balance sheet inflation.” It’s a form of pyramid scheme, built on permanently rising asset prices. The bubble grew far faster than the actual, real value of the productive assets these debts lay claim to, just like a successful pyramid scheme grows to become much bigger than the actual value of cash in the bank account.

So there’s a big hole in the accounts. The only way to fill this hole is to cancel some of the debts and write down some of the assets, as you suggest. Or… to water down the dollar, which is another way of closing the hole by inflating the nominal value of real assets. I suspect we’ll see a bit of both… which is why we hold both productive assets and gold but also cash.

Until next week,

Tom

P.S. News came late last week that they’re going to restart one of Three Mile Island’s reactors and sell the electricity to Microsoft in a 20-year contract. Microsoft wants the electricity to power its data centers. Nuclear re-starts are extremely rare, so this is an auspicious omen for the nuclear renaissance, and uranium demand in particular. The Sprott Physical Uranium Trust [SRUUF] is our safe play on this trend. I marked SRUUF as “accumulate on weakness.” It’s currently down about 19% from the high it hit in January. Probably a good time to accumulate some now if you haven’t already…

Editor’s Note: If this last month of seeing behind the curtain of Bonner Private Research hasn’t convinced you of the brilliance of Tom, Dan, and Bill – nothing will.

I (Porter) have been in the financial world for close to three decades, and I can tell you there aren’t many real geniuses here. The majority aren’t worth listening to, and better still should be avoided at all costs.

Tom and the team at Bonner Private Research are the minority. You should carefully listen to everything they say. And while we don’t agree on everything – and I’d worry if we did – Tom’s research is essential for all investors.

There are few people who can match his multi-decade track record, his ability to see around corners, or his skill in managing the emotional side of investing and not being swayed by the crowd.

Quite honestly, the reason you should read Tom Dyson each week isn’t merely because he is a genius at investing and will bring you outrageously good investment ideas.

You should read him each week because he understands the emotional challenges of putting capital at risk, and, unlike anyone else in this business, he can guide you through those challenges.

Tom won’t just give you great investment ideas: he will sit in the foxhole with you and fight. That’s why I’d urge you to take advantage of the special offer his team has put together for my readers.

All the details are here for you. Don’t miss it.