And It Offers up to 64% Upside as the ‘Smart Money’ Pours In

Editor’s Note: This and every Tuesday, we bring you research, insight, and investment ideas from outside Porter & Co. – from the analysts who Porter follows… many of whom Porter has known for years, if not decades.

Those in our Spotlight are the best in the world at what they do. That’s why we’re excited to bring you exclusive access to their ideas and insight, along with research that is normally available only to their paying subscribers.

If you’re new to The Big Secret on Wall Street and want to learn more about this membership benefit, you can read all about it here… and check out our previous Spotlights here.

The hardest part of investing today? No question about it: separating the signal from the noise.

And in the 25 years I’ve been in the investing business, the noise has gotten a lot louder.

You don’t need me to remind you of how things used to be: Checking the previous day’s stock movements in the newspaper… wandering through the shelves at the library… tracking down people through the phone book… finding a piece of paper and a pen…

You’d think that with all the technological innovations in recent decades, figuring things out would be easier.

But I don’t think so. If anything… it’s gotten harder.

Sure, you can find facts more easily, with the tap of a keyboard to find out what Mr. Google has to say. With AI, that’s only going to get easier.

But facts… are noise. Making sense of them, and applying some mental elbow grease to interpret them – that’s the difficult part. And it’s only gotten harder.

The signal is what we aim to pick out at Porter & Co. There’s lots of information about investing out there… insight, though, is vanishingly rare.

And no one gets this more than my friend and former colleague Marc Chaikin, who’s made a career out of creating signal out of noise.

Back in the 1960s – when computers filled entire buildings – Marc understood, long before anyone else, that there was gold in those numbers… that is, in the vast arrays of data in stock trading, as well as in the companies that were being traded.

For years, Marc focused on a specific dimension of stock trading: The money that was being put into, or taken out of, a particular security. After all, what drives a share price – or the price of anything, really – is one thing: Supply and demand.

Over a multi-decade career on Wall Street, Marc developed the revolutionary Chaikin Money Flow Oscillator, a tool that allowed him to get a read on the money behind a stock. The Oscillator was so powerful that it was built into the Bloomberg terminal – the financial data source used by every big bank, asset manager, and broker in the world (at Porter & Co. we have three Bloomberg subscriptions). And, decades later, it’s still on the Bloomberg terminal.

Then… Marc retired in 1999. But the Global Financial Crisis of 2008-2009 – and the havoc it wreaked on the portfolios of everyday investors – drew him back into the game.

And this time around, Marc created a tool to help normal people – who don’t have access to a Bloomberg (at around $2,500 per month, few people do!).

He created a set of tools called the Power Gauge. It collects and collates data from a vast array of sources, to look at price performance, fundamentals, insider buying, and expert consensus… all told, 20 different individual factors. It has these analytics for any publicly traded company in America.

When I first met Marc in 2020, I immediately saw the potential of the Power Gauge to help individual investors.

And Marc understood how he’d be able to help far more people through linking up with me (and Stansberry Research) than he ever could on his own.

Last week we shared with Porter & Co. readers the whole backstory of the Power Gauge… how it works… its incredible ability to see through the noise of a stock and assess its potential… you can read it here.

This week, we’re showing the Power Gauge in action. Below and here in PDF format [link] you can read a stock recommendation put together using the Power Gauge… the report is normally available only to paying subscribers to Marc’s Smart Money Trader service (if you’re interested in learning more about it… go here).

Janet Parker’s mother knew the doctor was wrong…

In August 1978, Janet started to feel sick. The 40-year-old medical photographer had a headache and muscle pains. And she soon developed red sores on her back, arms, and legs.

The first doctor to see Janet diagnosed her with chickenpox.

But Janet’s mother didn’t agree…

Her daughter had that disease as a child. And she knew that most people didn’t get it twice.

Plus, the sores looked different this time. They were more like pus-filled blisters.

Nine days after Janet began feeling sick, doctors admitted her to the hospital. By then, the lesions had spread across her entire body. And she was so weak that she couldn’t stand.

That’s when doctors figured out what was wrong…

Janet had contracted smallpox.

Her case stumped doctors at first because the world was almost free of the virus-borne disease.

The World Health Organization (“WHO”) led a massive vaccination campaign in the 1960s. And by the late 1970s, cases of the disease had become extremely rare.

The last natural case of smallpox had been reported in Somalia a year earlier. And where Janet lived in the United Kingdom, officials hadn’t identified a case in five years.

After Janet’s diagnosis, WHO officials raced to the scene…

They questioned Janet’s husband and parents about where they’d gone since she got sick.

Smallpox has an incubation period of about 12 days. So officials feared that the virus had already spread undetected.

Within two weeks of Janet getting sick, officials vaccinated more than 500 people. They also fumigated her home and car. And they kept close contacts in quarantine for two weeks.

Fortunately, the WHO’s rapid response kept the outbreak in check…

Doctors diagnosed Janet’s mother with smallpox in early September. But since she had gotten vaccinated, her symptoms were minor. And no one else contracted the virus.

As it turns out, Janet got smallpox at the University of Birmingham Medical School.

She worked as a photographer in the anatomy department. And she spent a lot of time in a darkroom above the laboratory where researchers were studying the smallpox virus.

Janet died on September 11, 1978. She became the last recorded victim of smallpox.

Two years later, WHO officials declared the global eradication of the disease.

Put simply, smallpox was beyond terrible. It killed an estimated 300 million people worldwide from the start of the 20th century through Janet’s death in 1978.

But ultimately, the story became more about humanity’s triumph than anything else…

Smallpox is the only major infectious disease we’ve ever eradicated.

That brings us to why we’re sharing this story with you…

The world could be on the verge of eliminating another virus as a threat to public health. It has been around for four decades. And it has proved more difficult to contain than any other virus in history.

But now, an established biotech firm has made a major advancement…

You see, a drug that prevents the virus from spreading already existed. But patients had to take it daily. The newest version of the drug only requires two shots per year.

Because of that, the “smart money” is pouring into this stock. When we add in a recent Oversold Buy signal from the Power Gauge, it’s clear that we’ve found a great time to buy.

As you’ll see, this stock could soar as much as 64% over the next year.

Let’s get started…

A Closer Look at This 43-Year Pandemic

If you’re sick enough to go to the doctor, you’re likely dealing with bacteria or a virus…

Bacteria and viruses are similar in terms of how you get infected. The infection likely happens through human contact or contaminated food or water.

But in terms of treatment, they couldn’t be more different…

That’s because bacteria are “free living” cells. They can survive on their own – even outside of the body. And when it comes to cells, they’re big and easy to identify.

To treat bacteria, you just need an antibiotic…

Antibiotics attach themselves to the living cells. And they kill them by blocking reproduction.

Viruses are far more complicated…

They’re like zombie diseases. They’re neither dead nor alive. Instead, they’re in a suspended state – until they get inside the body.

Once that happens, they come to life by attaching themselves to “host” cells.

If you want to kill a virus, you need to kill the host cells as well. But that’s not always a good thing. In some cases, killing the host cells can be toxic for the person with the virus.

So the best hope with viruses is to prevent new infections.

That’s what vaccines do. They stop the virus from moving on.

As we learned, it worked with smallpox.

But other viruses have proved more difficult. We’ve seen that firsthand in modern history.

In the past 50 years, the world has experienced two notable viral pandemics…

We’re all familiar with the COVID-19 pandemic. A coronavirus causes the infectious disease.

In the case of COVID-19, we were relatively lucky. Scientists had discovered the similar SARS virus in 2002. So by 2020, they had already completed a lot of work on vaccines.

COVID-19 was an easy target as well. That’s because of two things…

First, it produces a very high immune response. Once you’re exposed to the coronavirus, you get sick fast.

That means scientists could isolate the virus while it was still active. And importantly, they could do that before it mutated.

Second, once in the body, COVID-19 doesn’t mutate quickly. All viruses mutate. But since COVID-19 takes its time, scientists could develop a vaccine before it changed too much.

As a result, it didn’t take long for humanity to find a way to protect against COVID-19. And now, less than five years after the initial outbreak, we’ve significantly reduced the death toll.

The other notable pandemic is AIDS. It’s caused by the human immunodeficiency virus (“HIV”).

The HIV pandemic started in the early 1980s. So we’re more than four decades into it.

HIV is different from COVID-19…

It can hang around in the body for years before producing an immune response.

That’s why people rarely feel sick after being exposed to HIV. Or if they do feel sick, it’s so mild that they often think it’s just a common cold or the flu.

And HIV mutates faster than any other known virus.

So far, those two traits have made it impossible for scientists to develop a vaccine for HIV. And without a vaccine, HIV is as dangerous as ever…

According to the WHO, roughly 40 million people were living with HIV at the end of 2023. Of those folks, around 1.4 million were children 14 years old or younger.

New HIV infections are still happening every day, too…

Last year, roughly 1.3 million people were diagnosed with HIV. And around 120,000 of those cases involved children.

AIDS doesn’t kill nearly as many people as heart disease or cancer. But around 630,000 people died of AIDS-related illnesses in 2023. That’s more than one person every minute.

Despite these grim statistics, there’s some hope…

The United Nations has set a goal to eliminate AIDS as a threat to public health by 2030. That’s six years from now. And eliminating the spread of HIV is key to that plan.

The company we’re looking at this month might be able to get us there. Seriously.

And the thing is, this company doesn’t need some type of future technology to make it happen. It doesn’t require unlocking a secret about viruses or any other science fiction.

The real key to ending HIV will likely be just making the preventive drug easier to take.

Let me explain…

This Breakthrough Could End the HIV Pandemic

Gilead Sciences (Nasdaq: GILD) started as a biotech research company…

After becoming a doctor, Michael Riordan worked at venture capital firm Menlo Ventures. And he created Gilead in 1987 to focus on antiviral medicines.

Gilead initially created small strands of DNA to target specific genetic-code sequences. But the company struggled for many years. It almost went out of business several times.

In fact, Gilead didn’t see much success until the company was nearly 10 years old. And even then, its first huge break didn’t come until 2006…

That’s when the company got U.S. Food and Drug Administration (“FDA”) approval for the first once-a-day pill to fight HIV.

Gilead named the pill Atripla. It combined two of the company’s drugs with a third from Bristol-Myers Squibb (BMY). Because of that, experts referred to it as a “cocktail” therapy.

Gilead built on the cocktail’s success. And it quickly became a powerhouse in HIV treatment.

The company’s revenue more than doubled over the next three years. It went from roughly $3 billion in 2006 to around $7 billion in 2009.

Then, in 2012, the company figured out a new way to battle the HIV/AIDS problem…

Its drug, Truvada, received FDA approval for preexposure prophylaxis (“PrEP”). This daily pill prevents HIV infection in high-risk people.

That was a giant breakthrough.

You see, without a vaccine, the only way to contain the spread of HIV/AIDS is through preventing new infections. And that’s exactly what this form of Truvada does.

If someone takes the pill every day, it reduces the person’s chance of HIV infection by 99%.

In the three years after that breakthrough, Gilead’s stock went up nearly 400%. It peaked in June 2015 at more than $120 per share.

But as the business grew, Gilead began to lose its way…

In short, it became a serial acquirer of other drug companies. And it mostly focused on targets that worked on unproven cancer therapies.

The acquisitions were big, too. Gilead bought Kite Pharma for $11.9 billion in 2017. Then, it bought Forty Seven and Immunomedics for a combined sum of nearly $26 billion in 2020.

But several years later, none of these moves has paid off…

In its most recent quarterly-earnings report, Gilead reported just more than $800 million in revenue from cancer drugs. That’s only 11% of the company’s $7.5 billion in total revenue.

It’s a lousy payoff for billions of dollars in acquisitions.

Gilead hopes to make a third of its revenue from cancer therapies by 2030. So it has a long way to go over the next six years.

Importantly, Gilead says it’s putting acquisitions on the back burner for now. On the company’s first-quarter earnings call in February, Chairman and CEO Dan O’Day said…

We feel we have everything within Gilead right now to achieve our ambitions over the second half of this decade.

In other words, Gilead isn’t making any more big acquisitions right now. And since it has struggled in that area over the past several years, that’s a huge win for shareholders.

It gets better…

In July, Gilead announced the results of a study that could change how humanity works to contain HIV. And in turn, this breakthrough could reignite the drugmaker’s growth…

It relates to a drug called lenacapavir (also known by the brand name Sunlenca).

Lenacapavir is like Truvada. But instead of a daily pill, it’s a twice-per-year injection.

That’s a huge advantage over the company’s PrEP offering. If the PrEP isn’t taken every day, its effectiveness declines rapidly. That puts people back at a greater risk of contracting HIV.

A twice-per-year injection could increase buy-in from high-risk people…

After all, a stigma still exists around HIV/AIDS. Especially in less-developed countries, folks on the PrEP treatment are suspected of being HIV-positive or viewed as being promiscuous.

But if someone only needs to get a semiannual shot, the hope is that it will lead to better protection for at-risk populations. And in turn, that would boost Gilead’s business.

As we said earlier, the United Nations has a goal of ending HIV/AIDS by 2030. But a vaccine doesn’t exist yet. So if people aren’t protected, the virus will continue to spread.

Lenacapavir holds the key to protecting more people. And at some point, it could end the HIV/AIDS pandemic. It’s part of Gilead’s second-to-none drug franchise to fight the virus.

Humanity has only ever eliminated one infectious disease – smallpox. But we’re getting closer with HIV/AIDS. And Gilead’s advancements are a major part of that progress.

Gilead generated about $7.4 billion in free cash flow last year. In its most recent quarter, the company returned $1.3 billion to shareholders through stock repurchases and dividends.

And as sales of lenacapavir kick in, Gilead should start to grow again.

That’s a great setup for shareholders. And the Power Gauge sees the coming opportunity…

Our ‘Smart Money’ Opportunity With Gilead Sciences

Folks, Gilead currently trades around its highest level since early 2016…

The stock closed at $91.35 per share yesterday. It got as high as almost $99 per share earlier this month. But it has since pulled back about 8% over the past few weeks.

Here’s the thing, though…

The Power Gauge helps us see that Gilead’s big turnaround is only just beginning.

Institutional investors who carefully study the drug industry understand the importance of lenacapavir. And yet, the rest of us aren’t that focused on new drug developments.

That’s why our smart-money indicator is so important. It’s telling us that Wall Street’s biggest institutions see something special in Gilead right now. And we should take note.

I’m talking about the Chaikin Money Flow indicator, of course.

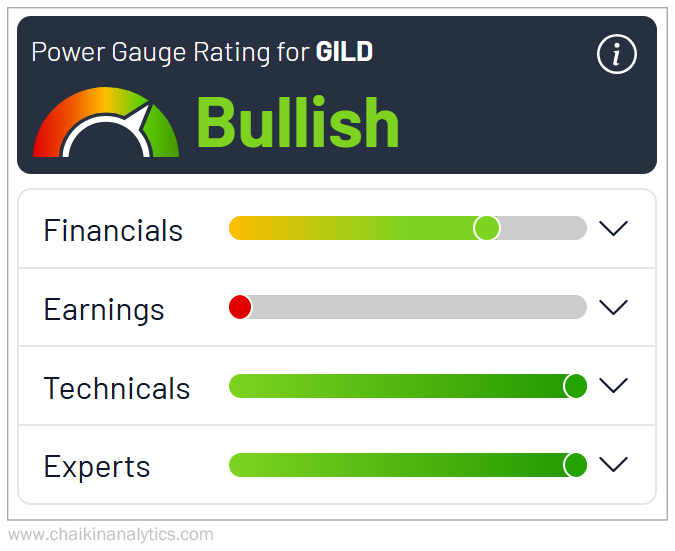

But before we get to those details, let’s start with the Power Gauge’s take on Gilead. As you can see in the following screenshot, the company gets a “bullish” rating today…

In short, a “bullish” rating means the Power Gauge sees a positive outlook on Gilead.

Three of the four factor categories are “bullish” or better. Only the Earnings category is negative. But that’s OK since we believe Gilead is at an inflection point in earnings growth.

In early August, Gilead announced a significant beat on its earnings projections…

Consensus estimates called for about $1.60 in earnings per share (“EPS”). But the company reported $2.01 in EPS. In other words, the company topped expectations by about 26%.

Then, three weeks ago, the company reported that it beat earnings estimates again in its most recent quarter. This time, its $2.02 in EPS topped the $1.55 estimate by 30%.

In other words, Gilead appears to be turning a corner. And the grade for Earnings should soon start to reflect this shift. That means the Power Gauge’s report should only get better.

Gilead also has a perfect Pre-Trade Checklist right now. Take a look…

In other words, the Power Gauge clearly believes now is a great time to buy Gilead.

And the technicals get even better.

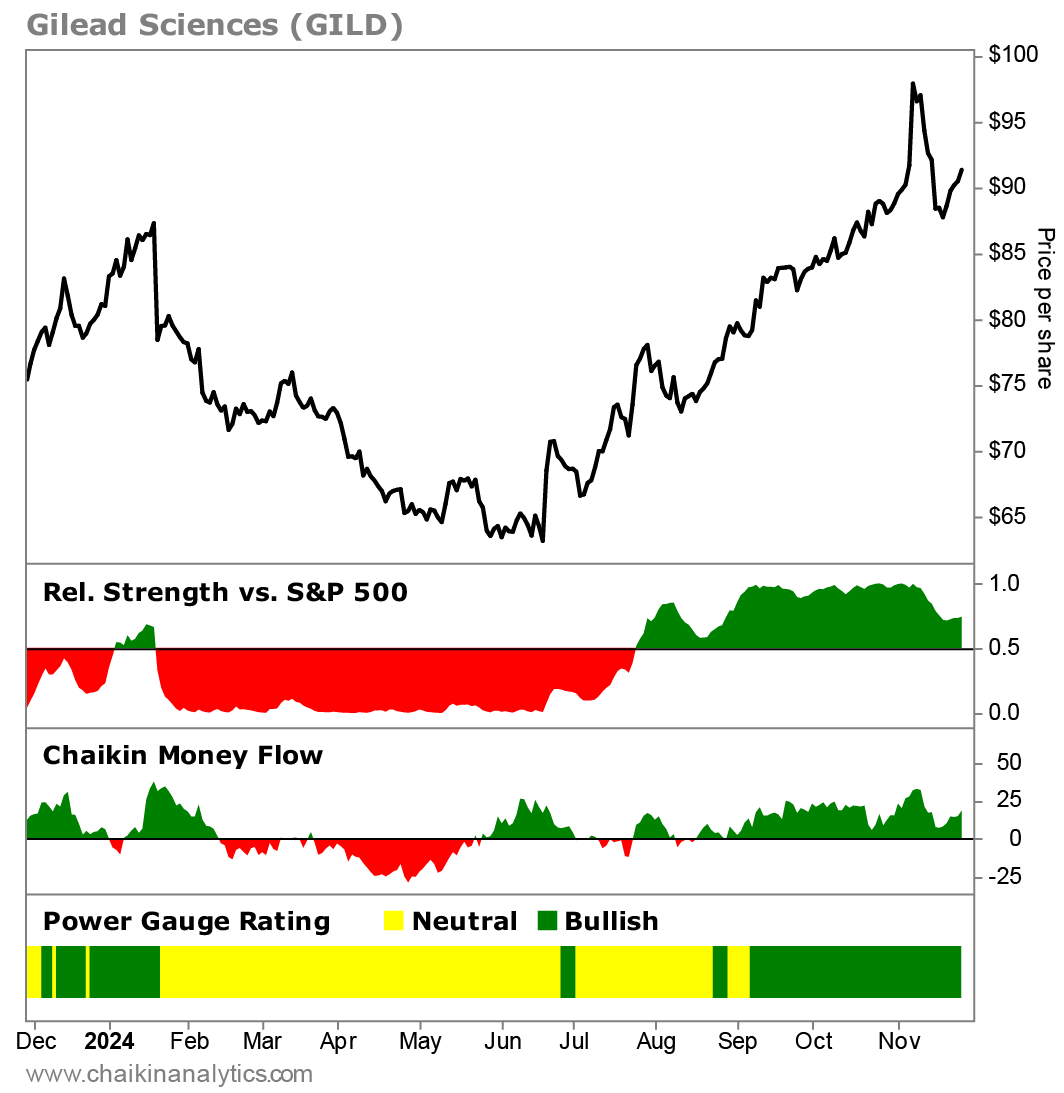

To see what we mean, let’s turn to the stock’s one-year chart…

Gilead ended an extended period of underperformance over the summer. Then, it started to beat the broad market.

You can see what we mean in the relative strength panel below the main chart. This indicator’s coloring flipped from red to green in July.

The timing makes sense…

In late June, the company announced the success of its Phase III HIV-prevention trial for lenacapavir. The results showed 100% effectiveness with the drug.

Next, look at the Chaikin Money Flow indicator in one of the other bottom panels…

The smart money spotted that development and started moving into Gilead.

You can see that the smart money’s buying spree gained momentum as summer turned to fall. And the Chaikin Money Flow indicator has been positive and persistent since then.

That means institutional buyers continue to pour money into Gilead. And it’s happening even as the stock moves down from its highs. That setup is playing out right now.

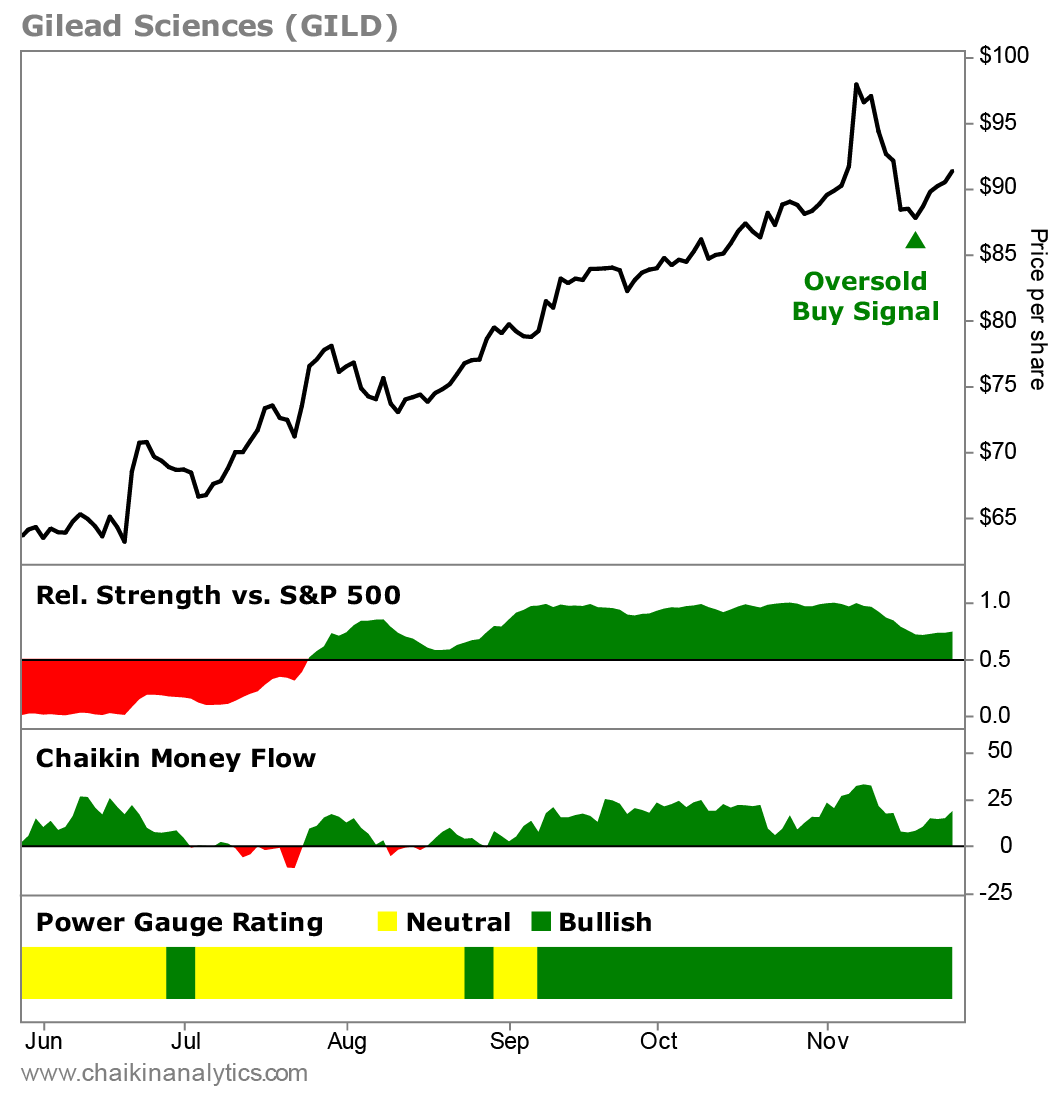

Next, let’s zoom in with a six-month chart…

This shorter-term view helps us clearly see that the smart money has supported the stock along each brief pullback. And now, we’ve got the signal we’ve been looking for…

The green arrow.

In this case, the green arrow points to an Oversold Buy signal. When that signal combines with strong smart-money support, we know that we’re seeing a considerable opportunity.

Take a look…

At roughly $90 per share, Gilead’s stock currently trades at 20 times its 2024 earnings.

That might sound expensive at first. But it’s in line with the average price-to-earnings ratio for many Big Pharma and related biotech companies.

The revenue from Gilead’s current drug portfolio grows in the high-single-digit range.

And lenacapavir represents a whole new growth opportunity. It could bring in billions of dollars in revenue.

The consensus EPS estimate for 2025 is $7.50. So at 20 times earnings, that gets us to a target price of $150 per share. That’s roughly 64% upside from its current level.

Gilead doesn’t even need to hit that mark, though. As business rises with the new drug, its stock should still move significantly higher in the months ahead.

Put simply, Gilead is starting to push the drug that could help end the HIV pandemic…

The Chaikin Money Flow indicator helps us see that the smart money is buying into the company’s stock today. And even better, the stock just triggered an Oversold Buy signal.

It’s exactly the kind of opportunity that we want to capitalize on in Smart Money Trader…

Action to Take: Buy Gilead Sciences (Nasdaq: GILD) up to $100 per share. Plan to hold the stock until the company’s next earnings report in early February. If the smart money doesn’t continue to pile in, we’ll move on quickly. We’ll protect our downside with a 25% trailing stop loss.

P.S. In addition to Gilead Sciences, we have five more active “smart money” recommendations waiting for you inside my newest research service, Smart Money Trader. For a short time only, I’ve re-opened our best-ever Charter Membership terms exclusive to Porter & Co. subscribers, backed by our 30-day 100% satisfaction guarantee. For full details, click here.

Right now, Marc is seeing a big rotation of capital in the “smart money” – that is, large institutional investors – from the sectors that have been leading the market.

He’s using his proprietary tools to capitalize on this rapid-fire shift over the next 12 months… and he’s put together this presentation to show investors how they can do it, too. Watch it here.

Good investing,

Porter Stansberry

Stevenson, MD