Issue #44, Volume #2

Trump Broke Pax Americana, Leaving Few Silver Linings But a Once-In-A-Generation Stock-Picking Opportunity In Biotech

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

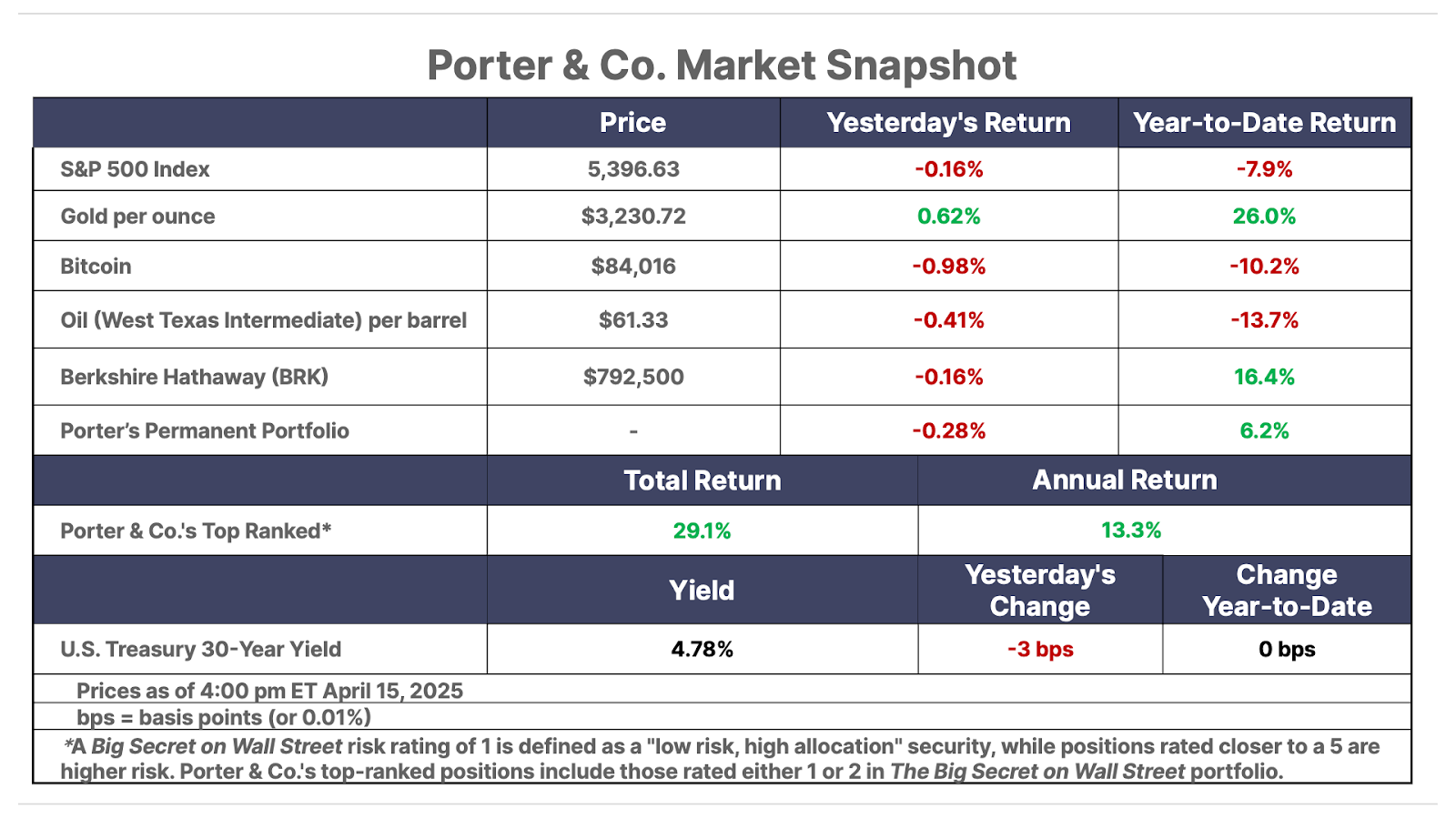

| One of the market’s most important correlations has broken down… Capital is fleeing the U.S… The selloff has created a paradox for the biotech sector… Rare value stocks with dramatic upside catalysts… Gold continues to shine… |

With volatility and uncertainty still riding high as a result of the Trump administration’s ongoing trade war, Porter is turning the Daily Journal over to Erez Kalir today. Though he leads Porter & Co.’s Biotech Frontiers, Erez has vast knowledge of the broader markets and years of experience with some of the best minds in finance… including working directly for Julian H. Robertson at Tiger Management during the Global Financial Crisis.

Here’s Erez…

For a time during my years as a hedge-fund manager, I had a ticket to one of the most exclusive clubs on Wall Street. It wasn’t officially a club. Instead, it was an informal roundtable convened by one of Wall Street’s “grand old men,” a former U.S. Treasury Secretary who had also run one of Wall Street’s most storied banks.

The group met every month or two, and its invited speakers were financial titans or senior government officials at the center of the action. I was generally the youngest attendee by at least two decades and had the smallest trading account by many zeroes. I tried my best to stay invisible at these meetings and simply soak up the worldly wisdom provided by the masters gathered there.

One of the most memorable meetings of this roundtable featured a senior government official who had led the Treasury Department’s response to the Global Financial Crisis in 2008-09. I’ll never forget what he shared about his daily routine during that time. He’d get to his office every day at around 5 a.m. and, first thing, fire up his Bloomberg Terminal to check the prices of global benchmarks.

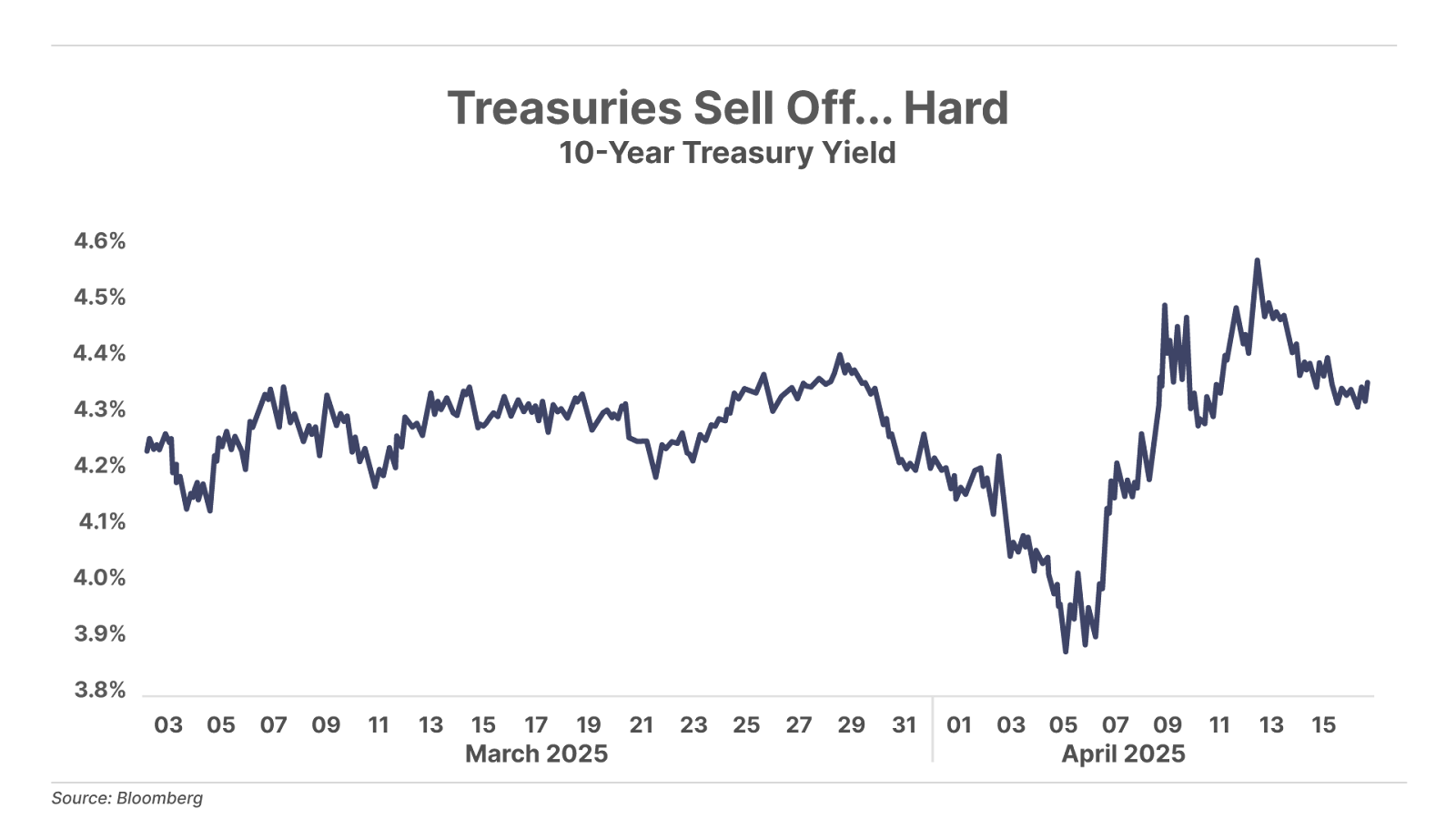

The numbers on a Bloomberg Terminal are color-coded: Green means the price is going up, red means it’s moving down. Day after day during the financial crisis, this official would launch his Bloomberg before dawn and observe a sea of red numbers – showing that stocks and equity futures around the world were selling off. But in that sea of red, one number remained consistently green: The 10-year U.S. Treasury note.

As the senior official recounted to our roundtable, “I knew that no matter how much blood there was in the equity markets, so long as the U.S. long bond stayed green, we’d be fine. I lived in fear of a morning when I’d come in and see the 10-year Treasury red alongside equities. Thankfully, that morning never came.”

His intuition was simple and powerful: So long as the world responded to bad news by selling risk assets and buying more U.S. Treasuries – especially the benchmark U.S. 10-year Treasury – that was a vote of confidence in America’s financial system, the U.S. dollar, and ultimately the U.S. economy. The stock market might melt down completely. But if the world’s deepest pockets reacted by buying U.S. Treasuries as their safe haven, the integrity and preeminence of the U.S. financial system would remain intact.

The Trump administration broke this correlation last week – and of all the things they’ve broken in their brief stint in the White House, this one is likeliest to be the most expensive.

Last week, for the first time in my three decades in markets, the world responded to bad news not by buying U.S. Treasuries, but instead by selling them. And the world sold them hard.

Over the span of three trading days, the 10-year Treasury yield backed up by more than 50 basis points, from below 4% to above 4.5%, a selloff of staggering magnitude in what had been, up until that point, the world’s ultimate safe-haven security. Although we may never know for sure, I’m convinced that President Donald Trump’s sudden decision last Wednesday to reverse his “Liberation Day” tariffs on most of the world except China was entirely about this “air pocket” crash in the U.S. Treasury market. Someone, probably Treasury Secretary Scott Bessent, walked into the Oval Office or picked up the “red line” phone and said: “Mr. President, you’re breaking the most important bond market in the world – our long-dated Treasury market. Please stop before it’s shattered to pieces.”

Ironically, Scott Bessent is one of the most celebrated hedge-fund managers of his generation. His mentors are George Soros and Stan Druckenmiller, two of the greatest investors of all time. Collectively, this trio became the first small group of traders to make $1 billion in a day when they bet against the British pound in 1992, correctly predicting that Great Britain would need to leave the European exchange rate mechanism (“ERM”) and devalue its currency. Their wager against the pound, which is on every market historian’s shortlist of the greatest trades ever, became known as the one that “broke the Bank of England.” Scott Bessent was Soros and Druckenmiller’s crucial analyst when they pulled off this financial coup. He was in his 20s at the time. Now an eminence grise himself, Bessent, I’m quite sure, did not anticipate becoming known as the Treasury Secretary who “broke the U.S. Treasury market” when he took his current job.

But it may already be too late.

Ever since the end of World War II, the U.S., under the leadership of both major political parties, has worked steadfastly to create a Pax Americana. Economically, the Pax Americana has meant that the U.S. would anchor itself at the center of a global trading system with more-or-less free trade. Our trading partners would use the U.S. dollar and buy our debt. Because this global trading system has been dollar-denominated, we’ve enjoyed what’s called the “exorbitant privilege” of being able to print more dollars when we’ve needed to – and to trade these printed dollars for actual things of value. We’ve protected this global trading system militarily with the might of the U.S. armed forces. And we’ve grounded it in the rule of law through U.S.-led institutions such as the World Trade Organization (“WTO”) and multilateral trade agreements such as the U.S.-Mexico-Canada Agreement (“USMCA”).

In three short months, the Trump administration has taken a sledgehammer to virtually every piece of this Pax Americana. Above all, by declaring World (Trade) War III on the global trading system itself, we’ve driven capital out of U.S. assets – even what used to be the world’s chosen safety asset, U.S. Treasury bonds – and back to their home markets. That capital flight out of the U.S. is also why we’ve witnessed the dollar weaken at the same time.

It will be difficult, if not impossible, to fix the damage, if the Trump administration even wants to. Trust takes years, even decades, to build… but it can be destroyed in an instant.

I’m afraid I see very few silver linings in this mess. Precious metals, no pun intended, are one of them. But an even brighter one may lie in the domain I focus on for Porter & Co: biotech.

How on Earth could a collapse of confidence in U.S. stocks, bonds, and the dollar create opportunities in biotech? It’s a good question. Let me explain . . .

Biotech stocks, like other seemingly risky corners of the stock market, have been sold off over the past months like red-headed stepchildren. This selloff comes on the back of what has already been a brutal, three-year biotech bear market. Many biotech stocks are down 70%, 80%, even 95%+ from their highs.

But this selloff has created a paradox. The selloff in biotech has been so severe that today, hundreds of public biotech stocks trade for significantly less than the value of the net cash on their balance sheets. They are what Warren Buffett’s mentor Benjamin Graham dubbed “Net-Nets” – the ultimate “cigar butt” value stocks… struggling companies with one puff of value remaining.

But scientifically, these are no cigar butts: Many of these companies are benefiting from the greatest wave of scientific innovation we’ve seen in the life sciences over the past 50 years. Their innovations are poised to revolutionize medicine… and generate trillions of dollars in value over the coming decade. Best of all, biotech stocks, like the distressed bonds that Marty Fridson writes about in Distressed Investing, have hard catalysts that can propel them upward: events such as regulatory approvals, clinical trial results, and strategic partnerships that can cause biotech stocks to re-rate upward many hundreds of percent in a day.

For all of these reasons, the washout we’re living through in U.S. markets has created what I think is likely to be remembered as the greatest stock-picking environment for biotech of all time.

If you’re interested in learning more, I hope you’ll check out Biotech Frontiers.

To learn more about Biotech Frontiers, or to subscribe, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.

I also greatly enjoy hearing from our readers. I hope you’ve found the perspective I’ve shared here helpful – and regardless, I’d be delighted to read your feedback about it: [email protected]

Three Things To Know Before We Go…

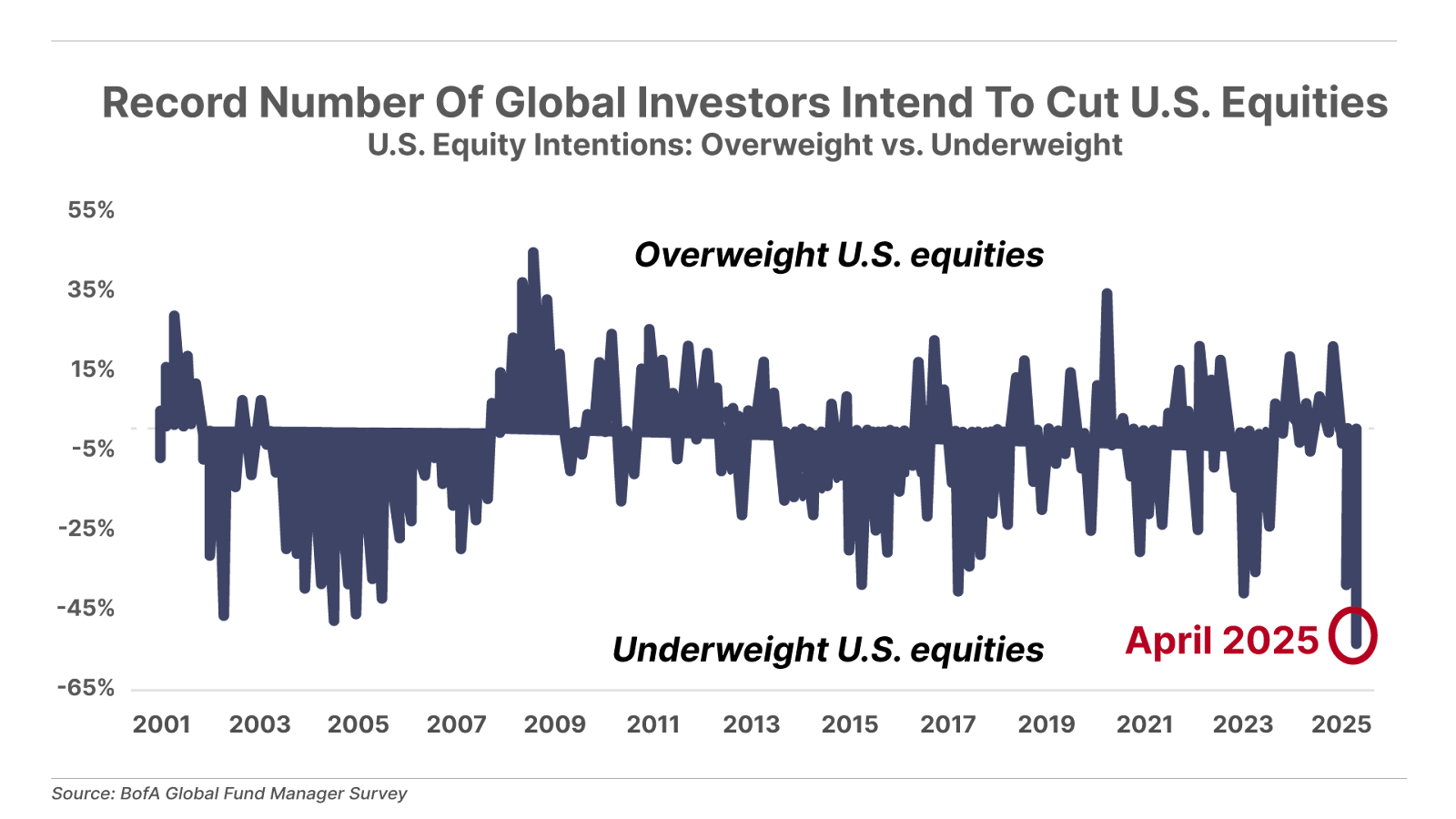

1. Fund managers flip their outlook on U.S. equities at the fastest pace ever. According to the latest Bank of America Global Fund Manager Survey, a record number of fund managers now plan to cut exposure to U.S. equities, with 82% expecting a weaker global economy. Just two months ago, that same survey showed cash levels at U.S. mutual funds hit a 15-year low, while managers were overwhelmingly bullish and fully invested in U.S. stocks. Clearly, the tide has turned. In February, we warned about the heightened risk of forced liquidations due to dangerously low cash reserves. Now, with sentiment shifting sharply bearish and managers rushing for the exits, we see the potential for attractive buying opportunities ahead.

2. Semiconductor stocks suffer collateral damage from the escalating trade war. Shares of chipmakers traded sharply lower today after Nvidia (NVDA) warned it could be hit with billions in charges tied to new U.S. export restrictions to China. The restrictions apply specifically to high-end chips used in artificial intelligence applications, including Nvidia’s H20 and AMD’s MI308. Nvidia said it stands to incur up to $5.5 billion in write-down charges in the first quarter – and could potentially lose billions more in revenue in coming quarters – while AMD (AMD) warned it could see up to $800 million in charges. Separately, ASML (ASML) – which supplies the advanced machines required to manufacture high-end chips – reported much weaker-than-expected first-quarter orders due to increasing tariff uncertainty.

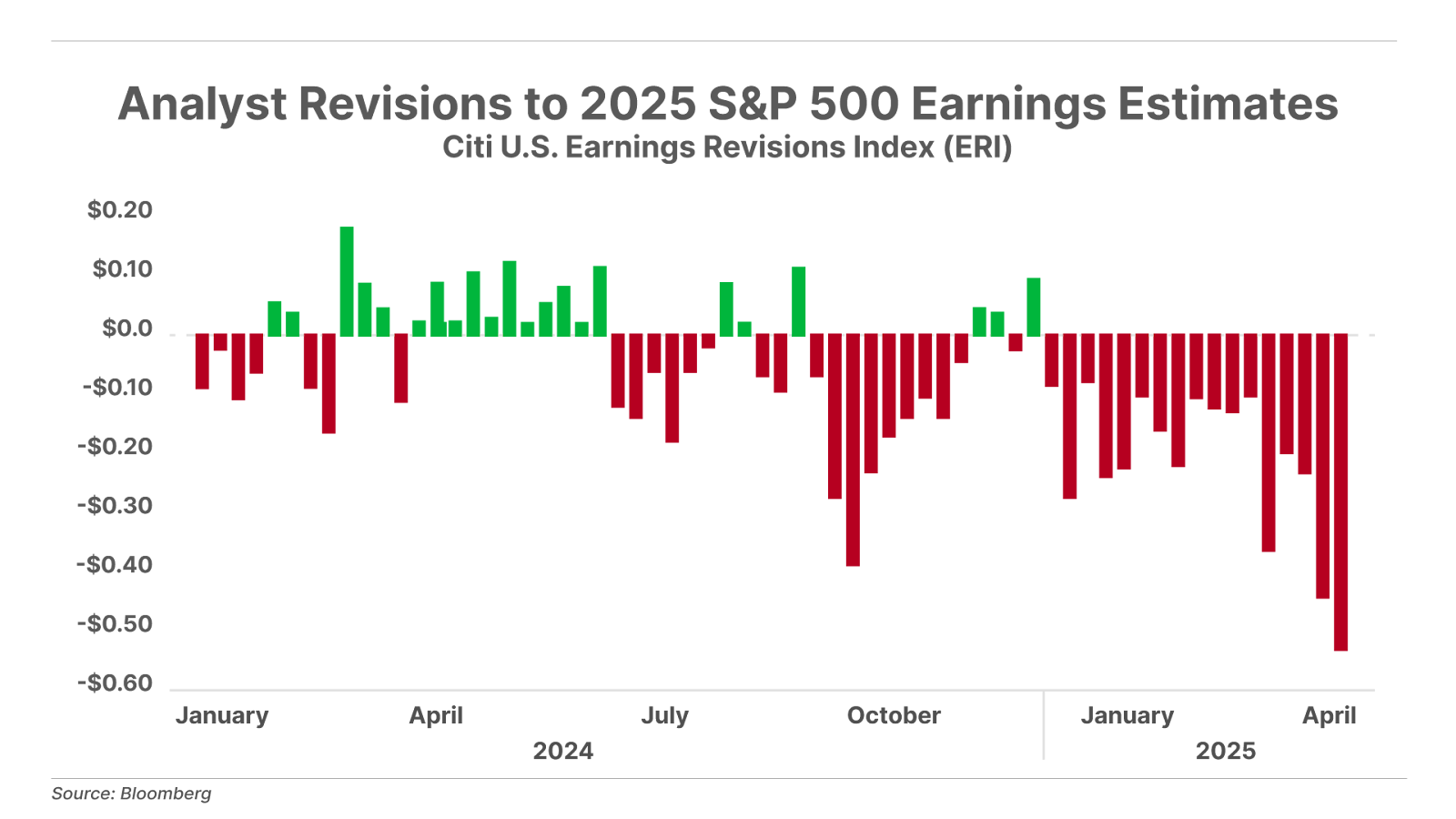

3. Analysts slash earnings expectations. Wall Street analysts have cut their 2025 earnings estimates for S&P 500 companies for the last 17 weeks in a row. Going into the year, the consensus forecast called for $273 in earnings per share (“EPS”) for the index this year. But after nonstop negative revisions in this year’s earnings outlook, the 2025 S&P 500 EPS forecast has now dropped to $267. Since stock prices follow earnings over the long run, we’ll likely need to see a reversal in this trend before the broad market indices can regain their footing and stage a sustainable recovery.

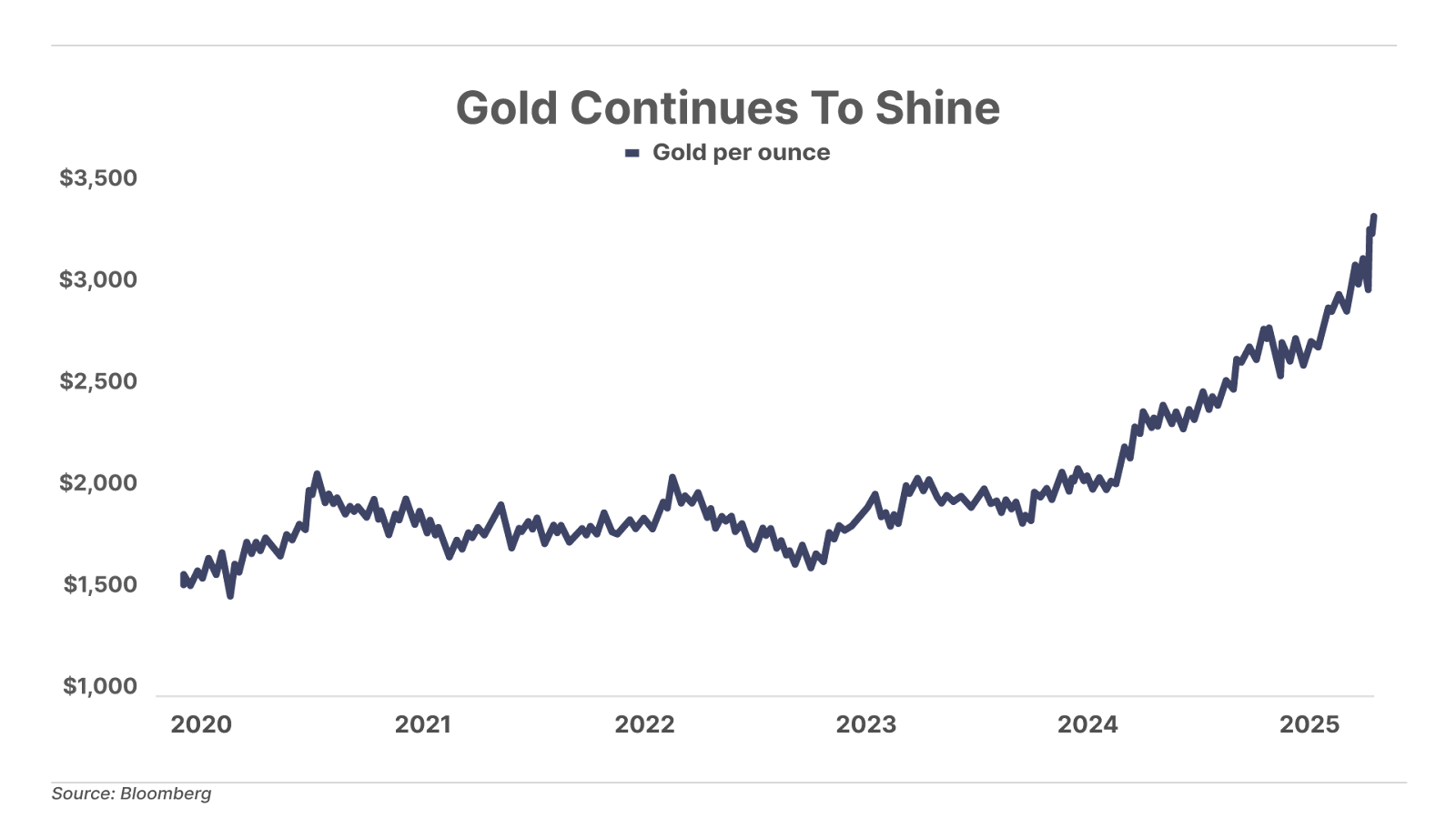

And one more thing… Gold continues to shine

Gold remains the biggest beneficiary of the recent uncertainty. As investors have fled from both stocks and bonds, gold funds have seen a massive $80 billion in net inflows year-to-date – more than double the previous full-year record set in 2020. The precious metal traded above $3,300 per ounce for the first time today, and is now up nearly 27% so far this year.

Gold has, over time, shown to be astonishingly good portfolio insurance: When the world is going down the drain, gold consistently stands – and gains – ground. And in recent months, it’s been far more than insurance – it’s been portfolio fuel.

But there are good ways to invest in gold… and better ways to invest in gold.

Which is which? Marin Katusa has thoughts. Marin – a friend of Porter – is one of the world’s premier experts on investing in natural resources, and gold in particular.

To hear what Marin has to say, see his presentation here.

Best regards,

Erez Kalir

Oakland, California

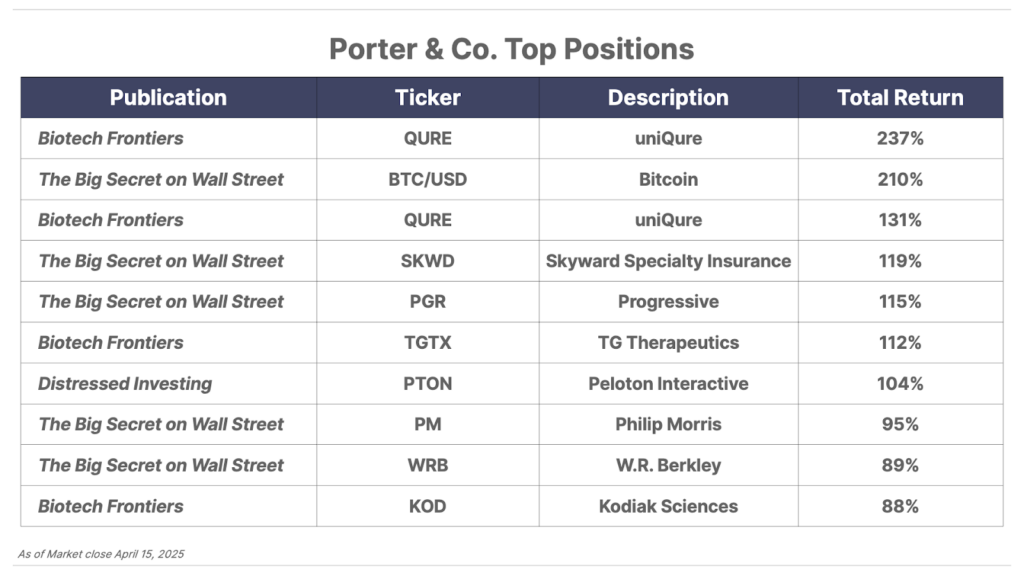

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.