Issue #37, Volume #2

Three Core Things To Do To Protect Yourself

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| Reader thoughts about Friday’s Daily Journal… What should I do today to protect myself from the global financial reset?… Coke is an example of a great business to own… Yes, a default by the U.S. government is possible… Goldman Sachs sees higher inflation coming… |

You guys surprised me.

Over the last 30 years, anytime I wrote anything that was, in any way, critical of Social Security, there was a tsunami of angry letters and cancellations.

But over the weekend, I didn’t get a single angry letter. Instead, I heard from dozens of people who, like me, are deeply concerned about our country and its enormous debt load.

Here’s a sample:

It was very depressing to read that article, but I do believe you are right… I feel so betrayed by the people like Richard Syron and a long list of others who have stolen our future and our children’s future…”

I have believed for over a decade that the only way the government can get out of this debt trap is to inflate their way out of it… If this is not managed, what about civil unrest and the fabric of society?”

I do not have the wealth or the knowledge that you have gained over the years. It is quite a bleak picture you have painted for us. I appreciate your wisdom but sometimes wish I didn’t read what you just wrote…”

Stay the course and keep telling the truth. Greatly appreciate you taking the time to dig in and give a real breakdown on things I’ve intuitively known but never had the urge to go quantify.”

If tariffs, a trade war, and unsustainable levels of U.S. government spending and debts will destroy the entire global financial system in the next four years, why did I just spend $10,000 to become a Porter Partner? What good is investing in good companies if the entire global financial system is going to hell?”

I have said basically the same for the last 20+ years – that in my lifetime (65 now) that the U.S. will default on their debt obligations at some point…. I’m a tad perplexed on keeping much, if any monies in stocks if the situation is truly doom-n-gloom. Would it not be better to go to gold and safer currencies than the U.S. dollar?”

How To Protect Yourself

I want to answer the two most frequently asked questions from readers.

First, if there’s a global financial reset and a U.S. default, what should I do today to help protect myself?

Friends, I’ve been teaching investors how to protect themselves from the government’s runaway debts and deficits since I wrote my first documentary about these problems (The End Of America) in 2010.

I believe there are three core things to do to protect yourself:

- The very best way to protect and continue to grow your wealth is to own a great business

- You MUST own gold, and I believe Bitcoin is becoming a world reserve currency, too

- You MUST raise cash, so that you’re prepared to take advantage of extreme volatility

There are dozens of other things you can also do – like using the relatively high value of the dollar today to buy productive real estate (farms, timber, well-located commercial properties) or buying foreign stocks. You can hold higher-quality currencies, like Swiss francs, or Singapore dollars. You can buy distressed corporate bonds, when they provide extremely high levels of yield (like we do with Marty Fridson in Distressed Investing).

The point is, you must make sure that your capital is out of long-duration, dollar-denominated debts, like U.S. Treasury bonds. You also must avoid investing in businesses that are vulnerable to higher interest rates.

But I don’t believe that means you should sell all your stocks. In fact, I believe the opposite: high-quality businesses are the very best form of asset protection.

There’s only one caveat: you must be well-suited intellectually and emotionally to be an investor. If you panic and sell your investments just because they fall in price, you shouldn’t own any stocks.

Why do I believe that great businesses are the best form of asset protection?

Because while the collapse of the Treasury-bond market and the end of the global dollar financial system will certainly be catastrophic for many companies, there are still plenty of great businesses that will continue to provide goods and services and earn good profits.

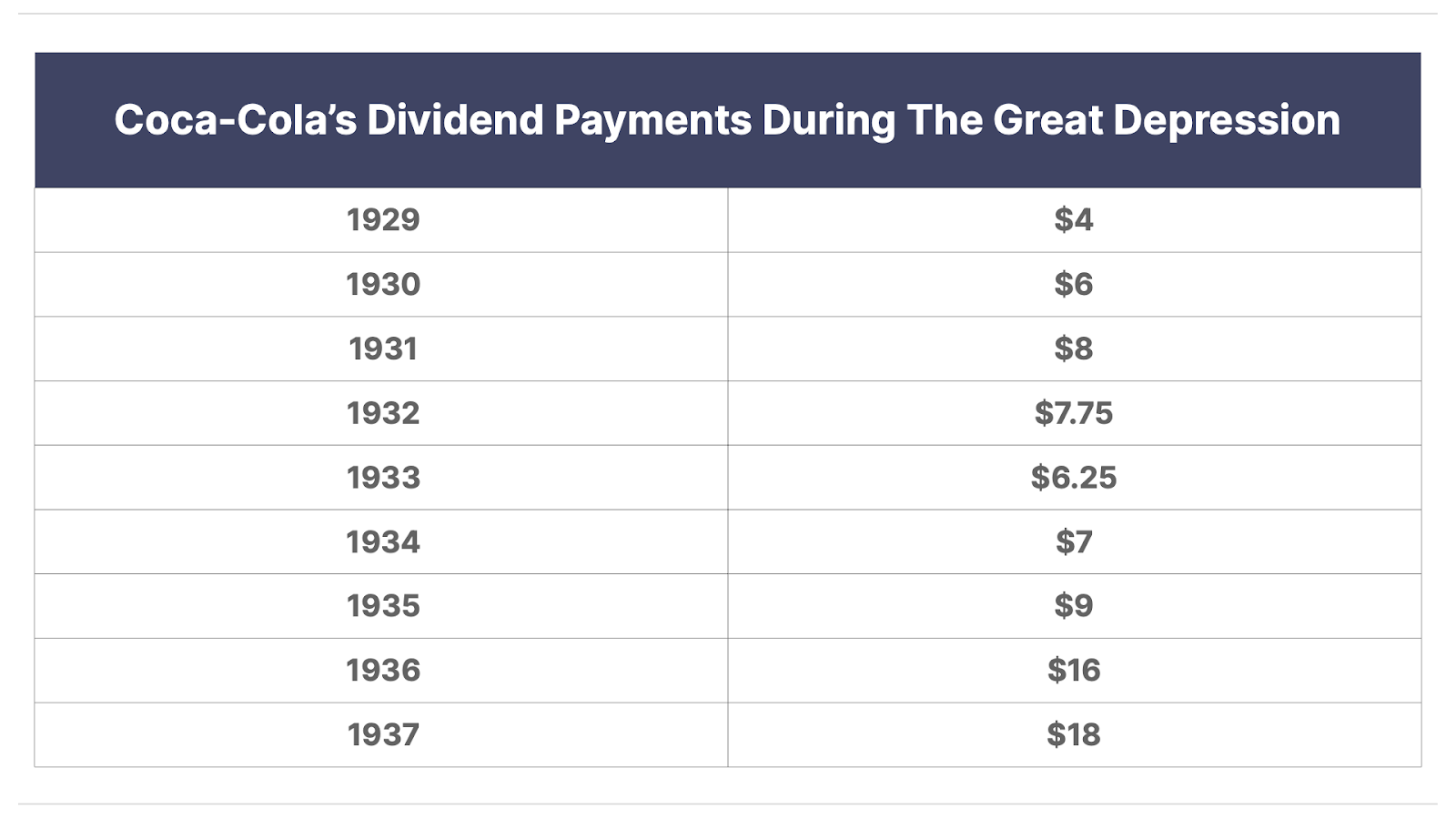

Here’s Coke’s (KO) dividend-payment record from 1929 through 1937 – during the Great Depression.

And the share price? Closed on the last day of 1927 at $127. By the end of 1937, it was trading at $114. But the nominal price of the stock is very misleading: there was a four-for-one split in November 1935. The real value of your shares grew 259%, from $127 to $456. And your dividends never fell below their 1929 level and ended 350% higher.

How should you allocate your assets?

Well, that depends on your circumstances and your risk tolerance, etc.

What I do believe everyone should do is read Porter’s Permanent Portfolio. This strategy outlined in this report is specifically designed to protect investors from the impact of higher and continuous inflation. Harry Browne, the economist and libertarian philosopher who discovered these ideas, taught them to me in the late 1990s. I’ve seen that this approach works.

Start with that framework and then change it to suit your circumstances.

Whatever you do, at the very least, make sure you’ve got at least 10% of your net worth in gold or gold and Bitcoin. Why? Because as the dollar loses its pricing power, gold and Bitcoin will protect the real value of your money.

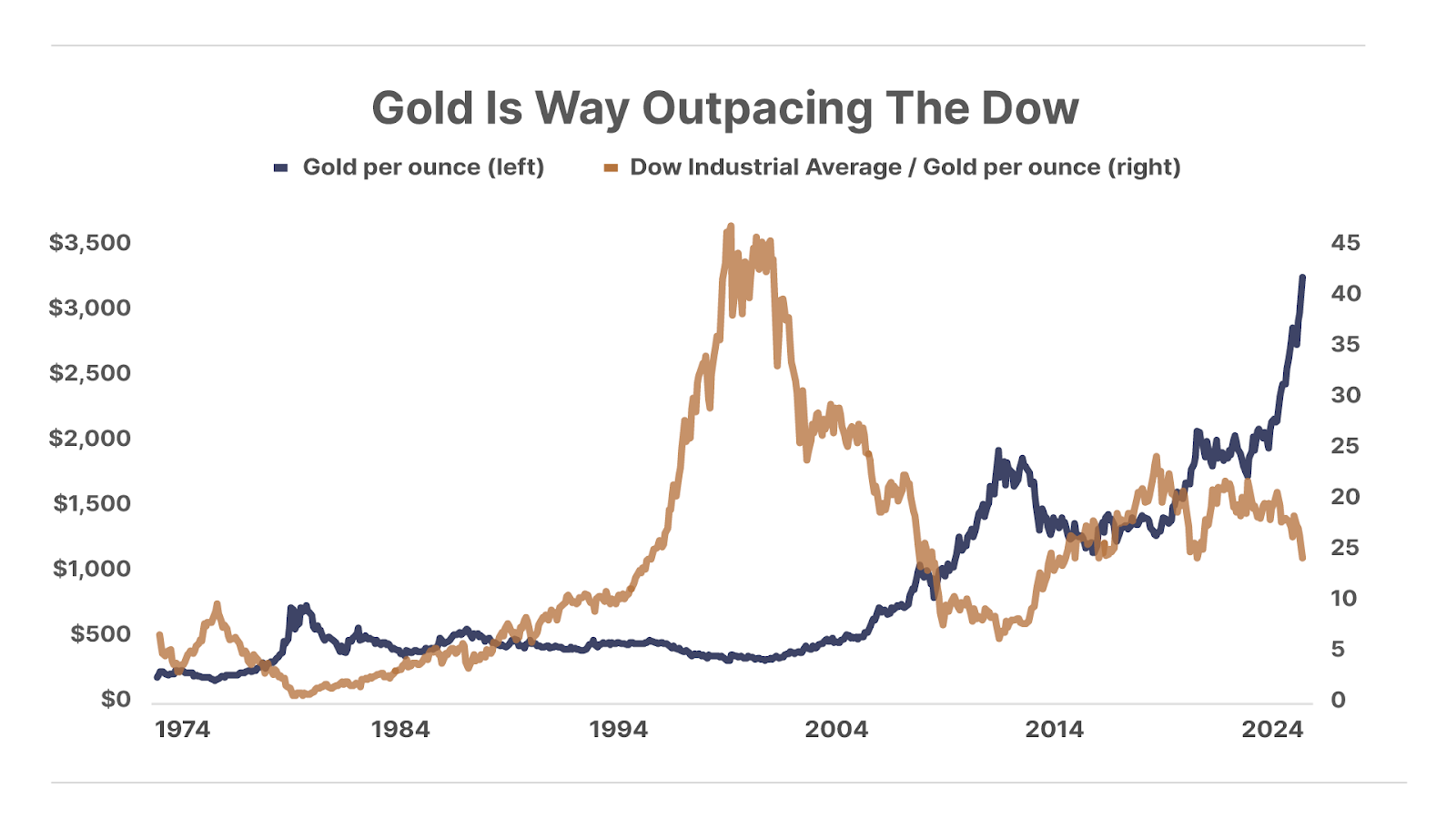

Look at this chart. It shows the price of stocks (the Dow Jones Industrial Average) measured in gold. What this chart shows you is that gold has been outperforming stocks since the 2000 bubble. I expect that will continue until the dollar’s final collapse.

With our government struggling to avoid bankruptcy – launching tariffs, trade wars, and, inevitably, much higher taxes – there will be periods of panic and volatility in the markets. You will want cash in those moments to buy great businesses. Coke’s share price fell from $171 in 1928 to $75 by the end of 1932, before rising again, as we showed above.

If you’ll use gold and Bitcoin as your “cash reserves” you will have the opportunity, from time to time, to buy great assets.

And think about this…

We’ve seen four massive bubbles in financial assets in the last 25 years: the dot-com bubble (1999), the real estate bubble (2006), the COVID bubble (2020), and the artificial intelligence (“AI”) bubble (2024). Each of them has led to a crash within 24 months. You’ve seen this happen again and again. Why? Because our monetary system is broken. It will continue to lurch between bubbles and busts, and the volatility will get worse. You can think of the dollar-based global financial system as a child’s toy – a top that’s spinning and losing speed. As it fails, it’s going to wobble and eventually topple.

Is Default Even Possible?

The second question I got from virtually everyone over the weekend was: Is a default even possible – why won’t the government just print all of the money it needs to pay these debts?

You should ignore anyone who says the government will not default because it can simply print all of the money it needs. That is absolutely false.

Why? Because most ($70 trillion) of the government’s obligations are linked to transfer payments that are protected, by law, from inflation. Printing more money will only make these obligations grow: they can’t be printed away.

Almost immediately after President Richard Nixon defaulted in 1971 (by refusing to honor the Bretton Woods monetary agreement), Congress passed the Social Security Amendments of 1972. This law introduced cost-of-living adjustments (“COLA”), which became effective in 1975. These are automatic annual adjustments to Social Security benefits based on increases to the Consumer Price Index for Urban Wage Earners (CPI-W).

As it was originally written, there was a “safety valve” of sorts in this law: these adjustments required a 3% annual threshold before taking effect. Thus, as long as inflation was under 3%, COLA adjustments wouldn’t occur automatically. But the Omnibus Budget Reconciliation Act of 1986 eliminated that provision and instead requires the Social Security Administration to calculate and apply annual COLA adjustments to benefits whenever the CPI-W increases by more than 0.1% between the third quarter of the previous year and the third quarter of the current year. This is an automatic increase to benefits every year that is required by law.

But even that isn’t the biggest threat to the Treasury.

The real “hole in the tub” is the Orwellian-named Inflation Reduction Act of 2022, which caps Medicare beneficiaries out-of-pocket prescription drug costs at $2,000 per year and limits insulin costs to $35 per month.

These laws are ticking time bombs because they grant unfunded and unlimited financial benefits as a matter of law.

We all, I’m sure, have different opinions about whether the government should be in the business of providing healthcare to citizens. But whether you agree or disagree with the law, simply mandating something doesn’t make it so. Someone must make those drugs and someone has to provide that healthcare. If the government is paying, you can bet it’s going to cost about 10 times more than it should.

The entire Social Security system is completely unaffordable and unworkable. And there is no chance that these laws get reformed. No one is even allowed to discuss these problems.

We’re sleepwalking into a financial collapse.

Three Things To Know Before We Go…

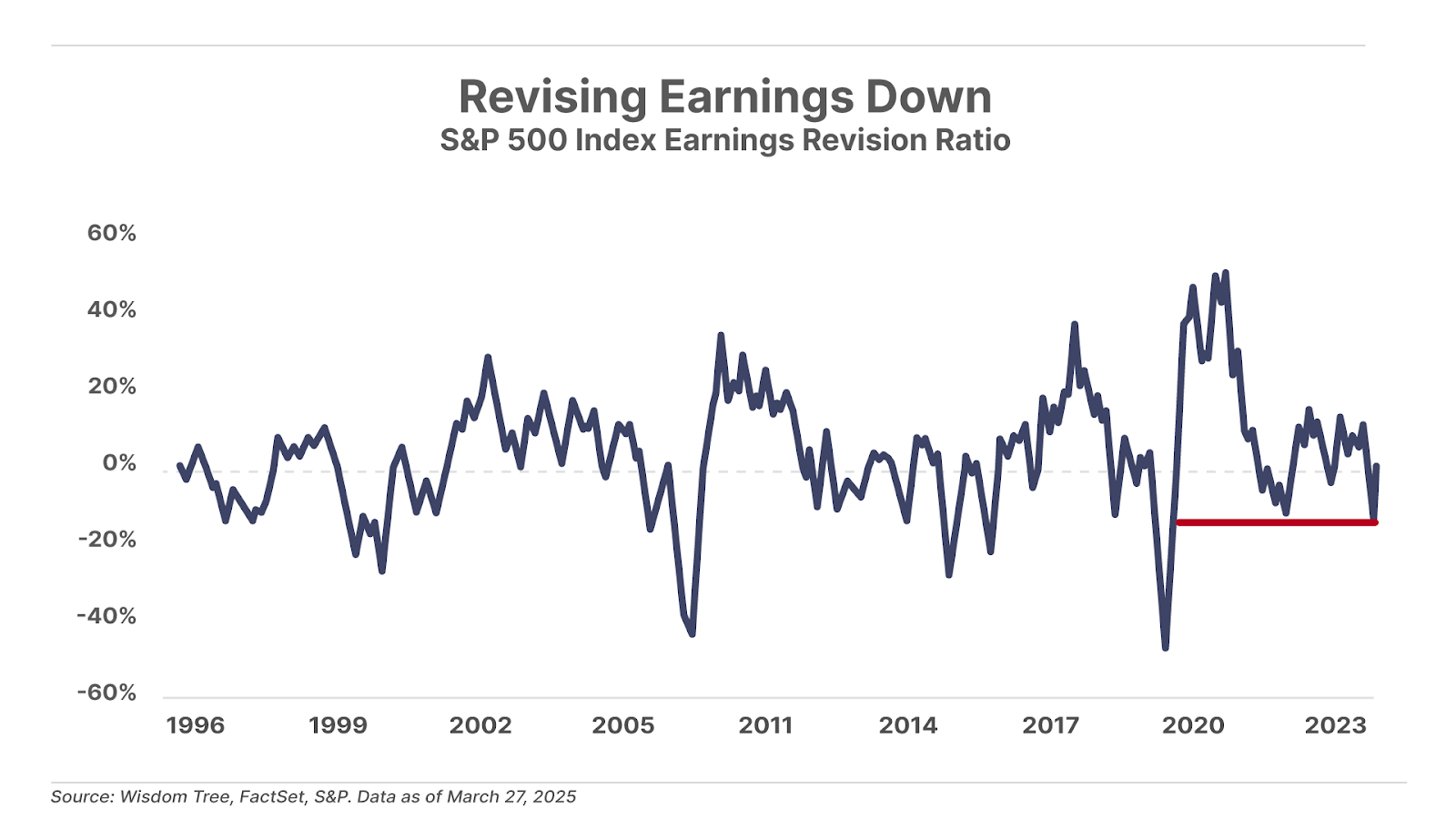

1. Earnings outlook deteriorates. Wall Street analysts are revising down their expectations for S&P 500 earnings growth by the largest margin since the 2020 COVID-19 shut down. Now, analysts expect Q1 earnings for S&P 500 companies to increase by 7.3%, down from an 11.1% expected increase at the start of 2025. Of course, stock prices typically go the way of earnings.

2. Student-loan repayments resume – more delinquencies will follow. With the end of the pandemic-era student-loan forbearance program, new delinquencies will lower credit scores. Under the forbearance program, many delinquent borrowers saw credit scores boosted due to paused payments allowing them to settle other debt. Between 2019 and 2024, credit scores for previously delinquent borrowers jumped 103 points, while those in default saw a 72-point increase. With forbearance gone, missed student-loan payments will drag down credit scores again – more than 9 million borrowers are expected to see major credit score drops this year. More delinquencies lead to higher borrowing costs, reduced credit limits, and tighter lending standards.

3. Americans are getting really worried about inflation. The latest University of Michigan Survey of Consumers shows long-term inflation expectations – expectations of the average annual inflation rate over the next five to 10 years – rose to 4.1%, the highest level in 32 years. One-year inflation expectations also surged to 5.0%, nearly doubling since the start of 2025. Separately, analysts at Goldman Sachs raised their forecast for core personal consumption expenditures (“PCE”) – the Federal Reserve’s preferred measure of price inflation – from 3% to 3.5%. With inflation expectations rising sharply, the Fed is less likely to consider additional interest rate cuts, even as the economy shows signs of needing them.

And One More Thing… Today’s Poll

Goldman Sachs also raised its 12-month recession probability from 20% to 35% on higher tariff expectations and weakening consumer confidence. So we ask…

Mailbag

We received a flood of emails about Friday’s Daily Journal, “Why Musk Won’t Save Us.” In it, Porter detailed some absurdities perpetuated by the U.S. federal government: one, pretending that Social Security is a guaranteed retirement plan and not a Ponzi scheme, and two, that forcing banks to lend to people with poor credit will help those people with home ownership. He wrote…

Banks can’t offer mortgages to people with poor credit histories, low incomes, and on homes that can’t readily be resold. Doing so results in soaring default rates and loan-loss severity.

Everyone knew these facts. And everyone pretended that there wouldn’t be a reckoning because, in the short term, these policies enabled enormous amounts of political capital (they bought a lot of votes) and, even better, virtue signaling.”

The first letter comes from Kathy D. who wrote:

Wow! Your column definitely falls in the tough love reality check. To be honest, it scares me to death that you will be right.

I found the information about housing and minority purchases very believable since I was in the wood products (manufacturing) industry for over 40 years and was a casualty at 59 when the sh*t hit the fan in the 2008-2009 housing meltdown. We were well aware of all the loans being given to people who had no business buying a home, not due to racial makeup, but their financial situations. Now I understand it further.

Thank you for the drill down of what actually happened.

What I take from all this is buy more gold!”

Porter, it saddens me to say this but you are spot on with your analysis.

Chuck C.”

Good afternoon, Mr. Stansberry. Thank you for writing the Musk article.

I have followed your work for a while now and take your writings and recommendations seriously.

As a retired senior citizen on a fixed income, your paragraphs on Social Security concern me.

I had no idea we citizens are not guaranteed any sort of Social Security monies. Like many of my fellow senior citizens, I count a great deal on what my wife and I receive in Social Security payments.

But I am also concerned about our country and the direction things are going. Not politically, but financially. Regretfully, there are few avenues through which we citizens can get a complete and accurate picture of the financial health of our country.

So please continue to educate your readers. We enjoy and look forward to your writings. Even if, at times, what you write isn’t the best of news.

Anthony O.”

Very informative, albeit depressing!

If anyone cancels or calls you racists for just reporting those quite disturbing facts on the 1992 “study,” then good riddance.

I’m feeling grateful for being a subscriber and being armed with knowledge to help avoid the worst of it (I hope!).

Jim M.”

Good investing,

Porter Stansberry

Stevenson, MD

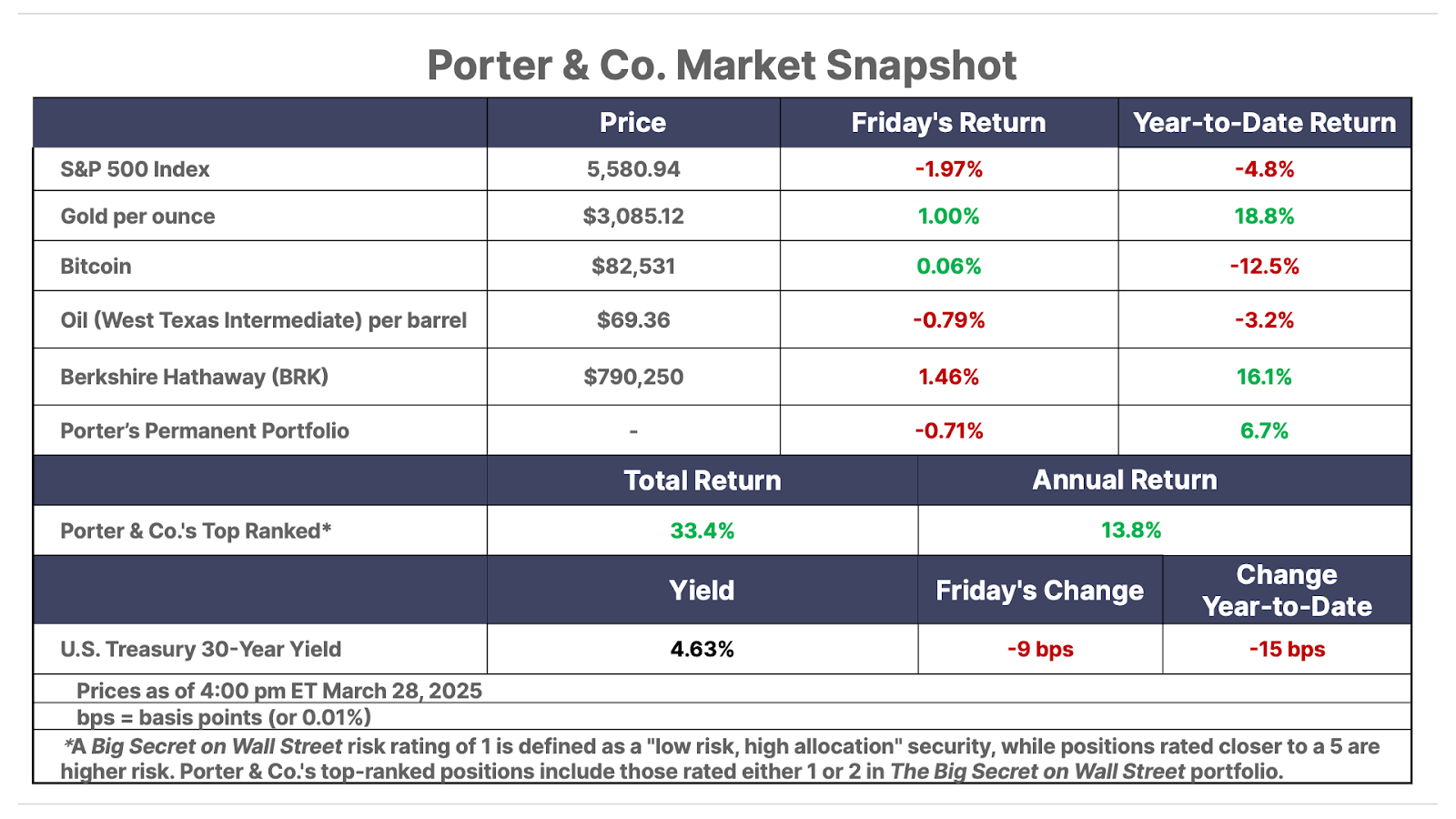

P.S. Through it all, gold continues to rise… today, the price of gold again cracked the $3,100-per-ounce level.

Gold has over time shown to be astonishingly good portfolio insurance: When the world is going down the drain, gold consistently stands – and gains – ground. And in recent months, it’s been far more than insurance – it’s been portfolio fuel.

But there are good ways to invest in gold… and better ways to invest in gold.

Which is which? Marin Katusa has thoughts. Marin – a friend of Porter – is one of the world’s premier experts on investing in natural resources, and gold in particular.

To see what Marin has to say, see his presentation here.

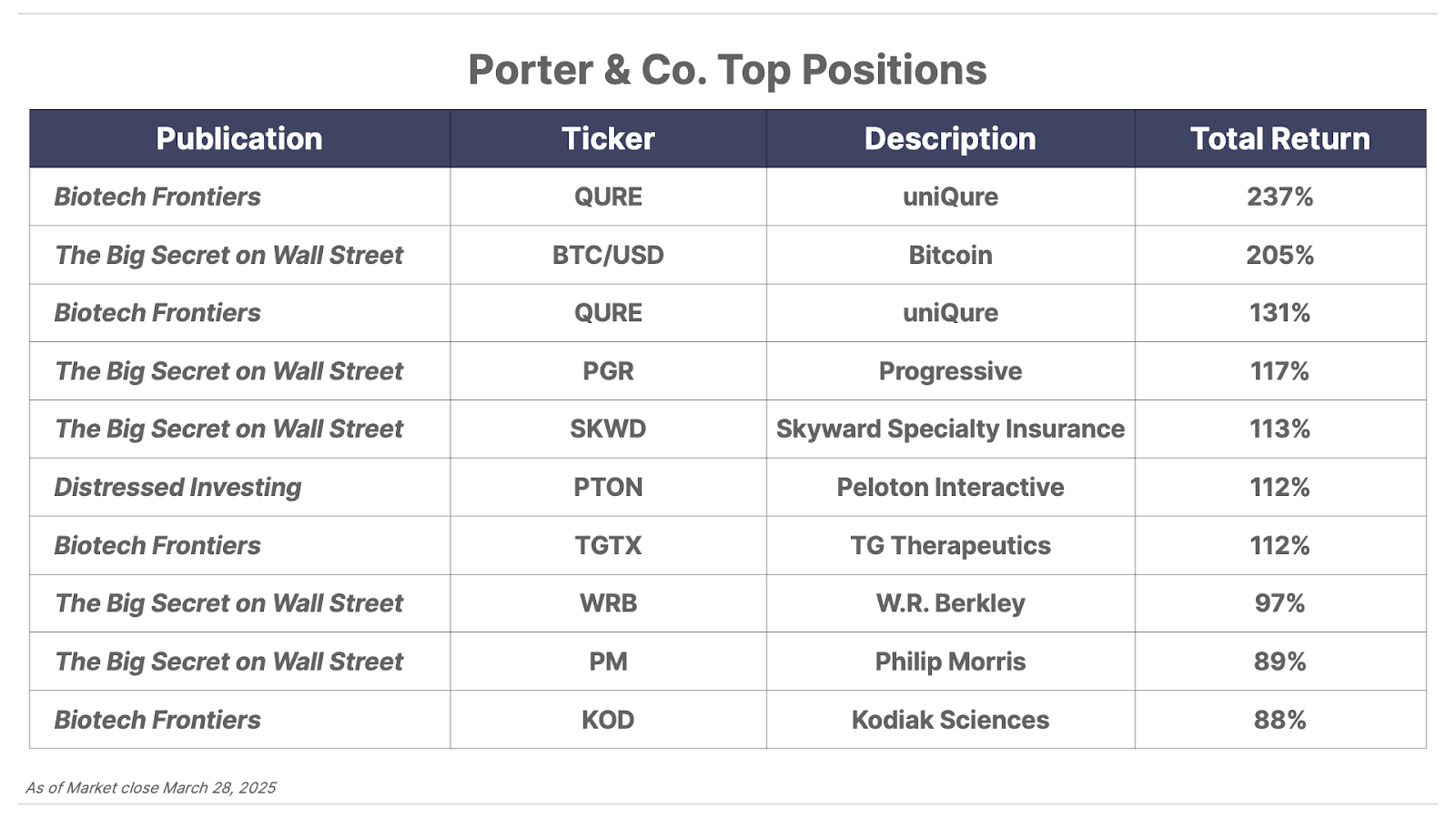

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.