Issue #70, Volume #2

A New Form Of Money That Will Disrupt Banking

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| The U.S. Senate passed the GENIUS Act… Stablecoins are a new form of money… The biggest change to the global monetary system since Bretton Woods… There will be no reason to ever use a bank again… Central banks are cutting rates… |

Well, that escalated quickly.

Yesterday the U.S. Senate passed the Guiding And Establishing National Innovation For U.S. Stablecoins Act of 2025 – aka, the GENIUS Act.

That happened a lot faster than I expected. I hope you’re paying attention…

As I outlined on Monday, this legislation enables the most important changes to the global monetary system since the Bretton Woods agreement following World War II.

In short, this legislation enables the creation of virtually unlimited new forms of money, as it carves out a new legal framework for stable–coins.

Specifically, the GENIUS Act defines a “payment stablecoin” as a digital asset designed for use as a means of payment or settlement, pegged to a fixed monetary value (typically the U.S. dollar), and backed by fiat currency or high-quality liquid assets on a 1:1 basis.

This law explicitly states that payment stablecoins are not securities, commodities, or investment company products under federal law.

What are they? Stablecoins are a new form of money.

That’s critically important because stablecoins facilitate what’s known as “DeFi” – decentralized finance.

While this concept will be difficult for most people to understand, the services that banks provide you – primarily security and reliable payments – can be easily provided today, virtually for free, via software and the internet. Blockchain technologies are perfect ledgers, which means they are the ultimate in security. And the internet connects everyone, for free.

What’s been needed to unlock innovation in banking and payment services has been a digital currency that’s stable and backed by a legal and regulatory framework. Stablecoins have the cryptological features necessary to facilitate distributed financial applications, and now they will have the legal and regulatory framework under the U.S. government to be widely adopted. This will enable immediate and free transfers and payments across the internet.

And, over time, this will lead to a complete revolution in banking. As I explained on Monday: this is like Netflix (NFLX) coming for Blockbuster. All of the reasons physical banks needed to exist just disappeared.

Here’s a critical fact to understand: Even without any legislation protecting it, stablecoins saw $28 trillion (yes, trillion with a “t”) in transaction volume last year, as stablecoins have been facilitating exchanges between different cryptocurrencies.

That’s more volume than Visa (V) and Mastercard (MA).

Payment processors, like Stripe and Shopify (SHOP), will now be able to integrate stablecoins, like Circle Internet’s USDC, directly into their applications, allowing for instant trade settlement and avoiding the use of any private payment network, lowering merchant costs.

Again, this is the biggest change to the global monetary system since Bretton Woods.

Back then, the paper dollar was the “stablecoin.” We promised to back the dollar with gold bullion reserves – something we conveniently forgot to do. Paper currency (the dollar) allowed banking reserves to grow without physical reserves (gold). That enabled lending to grow rapidly and it enabled a huge expansion of global trade – helping to rebuild Europe and ensure that the dollar would become the world’s reserve currency. The dollar as the “stablecoin” of its era enabled trade to be settled using secure communication networks (“SWIFT”), instead of actually shipping bullion around the world. Over time, that led to the growth of private payment networks, like Visa and Mastercard.

And that’s the system we’ve had since 1946. But not anymore.

Instead of shifting payments from hard assets (bullion) to paper receipts (the U.S. dollar) via private networks, stablecoins will allow payments – and all other kinds of financial services – to occur over the internet.

As you’ve seen over the past 40 years, digital technologies and the internet have continuously reshaped industries – from publishing to retail to communications. And now it’s banking’s turn.

Plus, there’s a reason the government is moving so fast: it wants to ensure that as this technology revolution occurs, stablecoins are backed with U.S. Treasury securities.

To gain protection under the new law, U.S. stablecoins must:

- publish monthly reserve composition reports on their websites, certified by CEOs and CFOs, and examined by a registered public accounting firm

- undergo annual financial statement audits, covering related-party transactions, and disclose results publicly and to regulators

- and, most importantly: maintain reserves backing stablecoins on a 1:1 basis with U.S. dollars or high-quality, dollar-denominated liquid assets, such as U.S. Treasury bills, with a maturity of 93 days or less

Currently stablecoins (like Circle’s USDC) make money by using their float to invest in U.S. Treasury bills, the income from which they keep. Circle has a big first-mover advantage, but this law will unleash a huge wave of innovation with large retailers like Amazon (AMZN) and Walmart (WMT) and large banks, like JPMorgan Chase (JPM) moving to create new stablecoin networks.

This will dramatically lower transaction costs for consumers and retailers and put pressure on private payment networks, like Visa, Mastercard, American Express (AXP), and PayPal (PYPL).

And this is only the first step.

The real transformation will come when stablecoins are allowed to pay interest to their holders – perhaps even by the minute. When that occurs, it will be the end of banking as you know it.

How will that work?

Today, your paycheck is direct-deposited into your bank account. But your bank pays you virtually nothing. And it invests your money, keeping the income it earns. When you want to use your money, you have to pay fees – to wire it, to use ATMs, to use checks, to use Visa.

Or, contrarily, you could simply ask your employer to pay you in a stablecoin, emailed directly to you. The money is instantly transferred to your software via the internet, using blockchain technology. You can spend it virtually anywhere you want, without any transaction fees. And every minute you hold it in your software wallet, you’ll earn 75% of the full 90-day T-bill rate. If you ever need a loan, all of the assets that you have “onchain” can be used as collateral and you can borrow the money for an hour, a day, a week, a month… or five years.

There will be no reason to ever use a bank again.

And while some people won’t like this, perhaps the best part of DeFi and stablecoins is that they will make it much harder for the government to watch our bank accounts. Sure, stablecoin issuers will have to follow the Know Your Customer rules, etc., but as the number of stablecoins grows, there will be so many more on-ramps and off-ramps to the financial system that it will be virtually impossible for the government to spy on you without a warrant – as it should be.

What should you do about all of this right now?

Well, if you have some risk capital, you might buy a small position in Circle Internet (CRCL) – I did. And, if you don’t own any Bitcoin, this is a good time to buy some. While U.S. stablecoins must be backed with U.S. dollar assets, there will certainly be other stablecoins that are backed by Bitcoin and can provide holders with a yield that’s derived from Bitcoin-backed lending. All of these new forms of money will ultimately create more demand for Bitcoin. And there will only be 21 million Bitcoins ever mined. We all know, they’re going to keep printing those dollars.

Three Things To Know Before We Go…

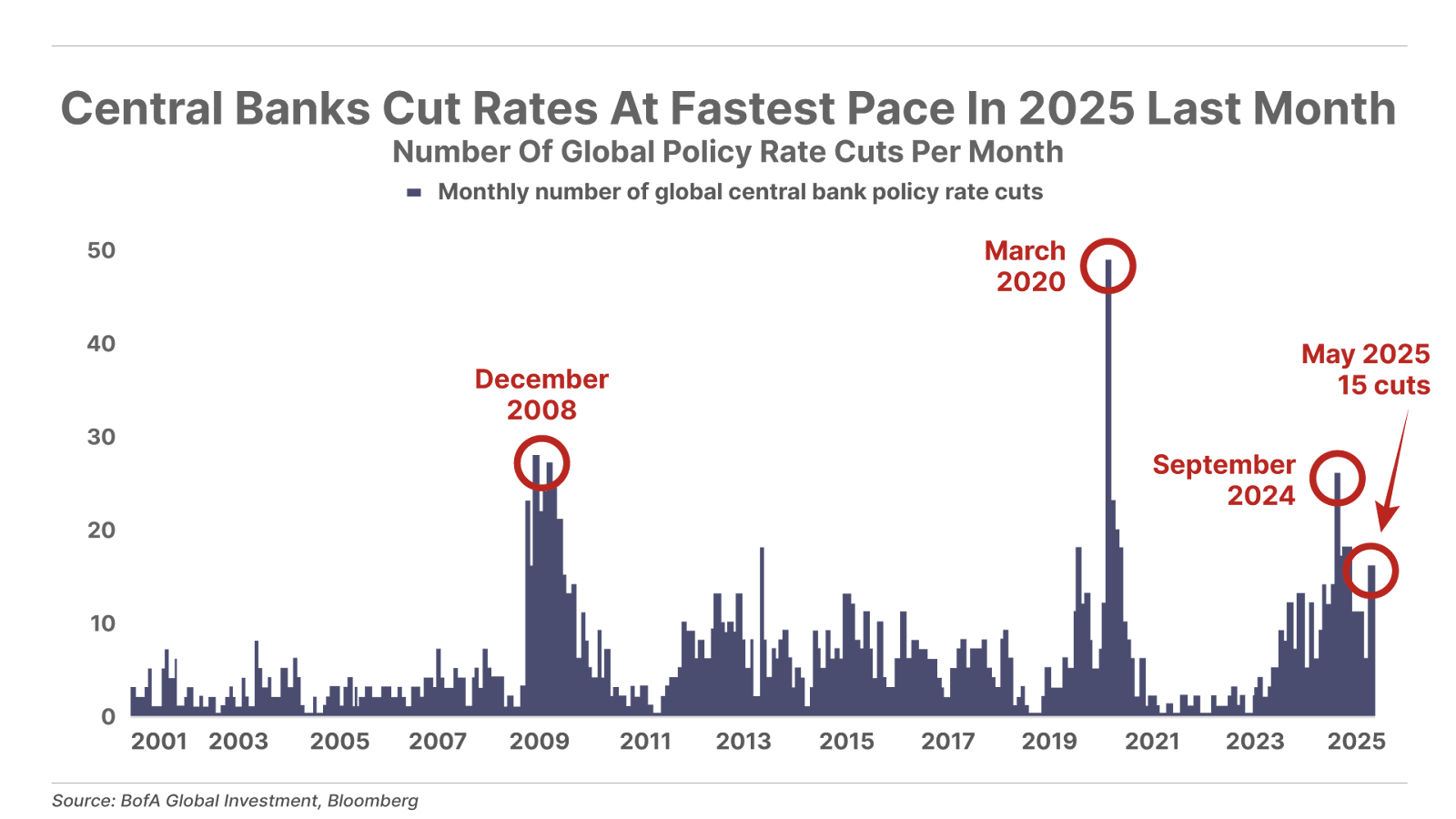

1. Central banks embark on a rate-cutting spree. The number of interest rate cuts by global central banks rose to 15 in May, the fastest pace this year. This comes as economic forecasters expect global growth to slow significantly in 2025, with the World Bank recently calling for global GDP to fall to 2.3% this year – the weakest level since 2008. If these trends continue, we could see interest rates continue to fall globally.

2. Surprise Index goes negative. Bloomberg’s U.S. Economic Surprise Index, a measure of economic indicators coming in above or below economist expectations, has dropped into negative territory. This is a key signal of future economic growth (or lack thereof), and the severity of its decline in recent months points toward a sharp reduction in U.S. economic growth.

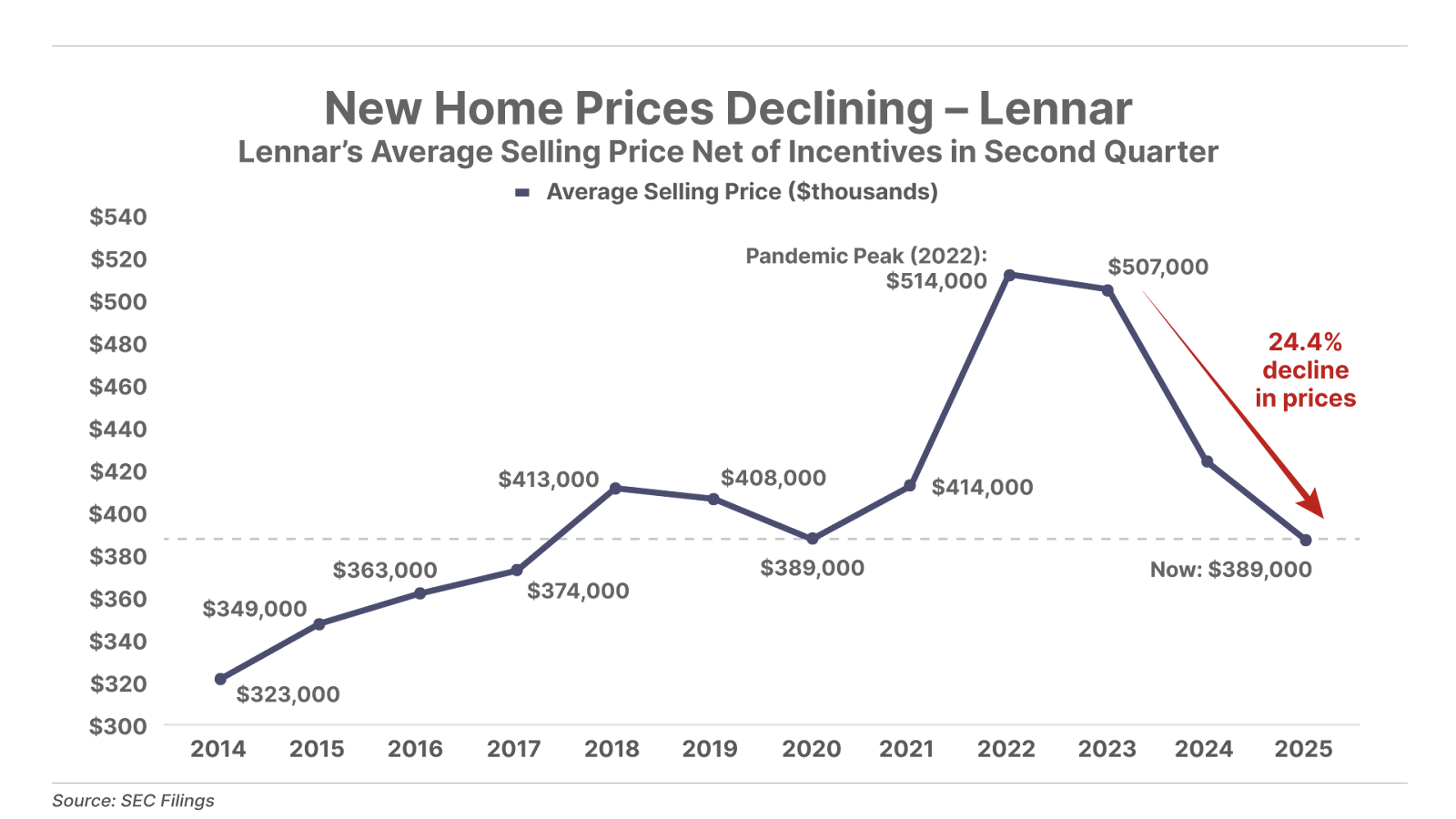

3. The housing market is losing steam. Lennar, the second-largest U.S. homebuilder, just reported disappointing earnings: revenue fell 7% year-over-year, and the average home sale price dropped 9% to $389,000 – down 24% from the pandemic. To sustain sales, Lennar is offering its most aggressive buyer incentives in over a decade – slashing prices and buying down mortgage rates – as affordability worsens and consumer confidence fades. Even with a record number of homes built in Q2, the company’s profit margin fell to 18% – its lowest since 2018 and second weakest in the past decade.

Tell me what you think: [email protected]

Mailbag

On Monday, as he did today, Porter wrote about the emerging trend of stablecoins that he says will disrupt the banking industry. Titled “Bank Of America Is Fucked,” Monday’s Journal said:

If you can use and hold stablecoins safely, you simply won’t need a bank anymore. It’s like Blockbuster: nobody needs to rent DVDs anymore. Nobody needs to hold dollars in a bank, ever again. You can hold them with stablecoins, yourself.”

A number of readers wrote in to share their thoughts on the essay and its headline.

Thanks, Porter, for a great essay.

Banks are nothing more than licensed Ponzi schemes. If you withdraw $100,000 they go chasing deposits to replace it.

Kind regards,

Adrian W.”

I agree with the premise of your argument. To take it a step further, I think that Ether will become significantly more important in the future as it is the backbone of many of the applications that will provide services that will replace banks if regulations permit.

Peter C.”

Thank you for a very “short” but succinct explanation of the banking, credit card Circle of Love! I always felt like it was a losing game trying to move from bank to bank to get lower fees. Please keep us informed as to when and how we acquire stablecoins. Digital Wallets and how you set them up will be a necessary element for us novices.

Terri M.”

You are a professional. Please do not use the “f” word. It makes you a smaller person. Thank you.

Tom B.”

Please, no profanity or vulgarity. It is demeaning to readers and erodes your credibility.

Ray S.”

Good investing,

Porter Stansberry

Stevenson, Maryland

P.S. Something extraordinary is happening in Washington.

For the first time in over a century, a sitting president could release a national treasure that’s been tied up in red tape, for generations.

I’m talking about a $150 trillion American asset that’s scattered across all 50 states.

Former White House economic advisor Jim Rickards just came forward with a shocking prediction: “This summer, President Trump could announce the largest wealth transfer in American history.”

The window to act is extremely narrow, he says. Because once this story breaks, the biggest gains could already be gone.

Click here to watch the exclusive interview before it’s too late.

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.