Issue #87, Volume #2

Why We Love Investing In The Hershey Company

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| Investing in Hershey is boring… Why not invest in Bitcoin?… Hershey has had 15% annualized gains for 20 years… Start your own Hershey Retirement Fund… Share this with friends and family… Altria is up, and BTI might be tomorrow… |

I’d bet almost everyone reading this email has heard me talk about The Hershey Company (HSY) before.

Just like you’ve heard me “preaching” about property-and-casualty insurance. And the “irreplaceables”: Philip Morris International (PM), Deere & Co. (DE), and Domino’s Pizza (DPZ). (You can add Coke (KO) and McDonald’s (MCD) to the list too. We just haven’t had good opportunities yet to put them into my Big Secret On Wall Street portfolio. I did put them in Porter’s Permanent Portfolio, because it is hedged.)

Here’s the ironic part. These recommendations, without question, will end up being the most valuable ideas I ever give you. But guess what? Virtually all of you will completely ignore this advice. If the past is prologue, I’ll get dozens of emails about this Journal tonight, with everyone complaining about wasting their time writing about Hershey again.

The critics will complain: who wants to invest in a stock that everyone already knows about, that has very consistent earnings growth, and that can’t go up more than about 20% or 30% even in its best year? Why invest in stocks like Hershey when you can buy Bitcoin… or Coinbase… or the latest new technological widget, whose shares could (and sometimes do) rocket up 200% or 300%?

I love all my subscribers. You are wonderful people – and extremely intelligent. Your children are even smarter. And I have never seen such a beauty as your wife.

I am not looking my “gift horse” in the mouth. I’m just trying to lead that horse to water.

The one thing I’ve learned, for certain, about investing is that it’s woefully difficult to beat the after-tax returns you’ll earn if you can simply learn to buy Hershey at the correct price.

I’ve been recommending Hershey stock at below 15x trailing earnings consistently since late 2007.

That strategy has produced annualized gains of around 15%. That might not seem like much, but over 20 years, it adds up. And it’s very difficult, if not impossible, to beat. I respectfully doubt more than 1-in-10 of you have produced annual returns higher than that in your truly passive investments over the last 20 years.

But that’s not all.

The even better part of owning Hershey is the low risk and the constantly growing dividends. With volatility less than a third of the S&P 500 (beta: 0.29), you can safely lever this stock 2x. And the dividend will cover most (or all) of the margin loan. There’s hardly a better retirement plan in the world than simply “stacking” and compounding Hershey, along with Philip Morris, McDonald’s, Coke, Domino’s, and Deere.

The trouble is this advice doesn’t sell. And it’s incredibly easy to follow. Thus, no one is going to spend their lives leading the horse to this kind of water. There are no fees to be gained by doing so, or renewals to be earned either.

And, most frustratingly, even if there’s someone kind enough (and stupid enough) to teach these lessons, the advice will mostly go ignored. It isn’t exciting. There’s nothing fun about watching yourself get richer at the same pace as paint drying.

Here’s the part that is exciting. After you retire, if you’ve simply continued buying shares of Hershey at the right times, you’ll have ever increasing amounts of dividend income to live on.

Since I first recommended Hershey, the annual dividend (paid quarterly) has grown from $1.19 to $5.48 – a 4.6x increase!

If you’d put your retirement fund, say $2 million, into Hershey back then, the annual income would have been about $60,000. But today? $275,000.

And while I can’t know this for certain, I think it’s a lock that Hershey will raise its dividend again next year. The company just paid its 382nd quarterly dividend in a row. It has paid dividends consistently for 95 years! Talk about “Lindy.”

The company reported earnings today and what the market sees is a company that’s weathered an incredible storm and is beginning to make adjustments that will result in record earnings over the next two to three years.

Hershey’s latest:

- Q2 consolidated net sales of $2.6 billion, an increase of 26.0%. Sounds incredible, but it’s mostly just the impact of a late Easter this year. Absent these aberrations, first half net sales increased by only an anemic 1.7%.

- Tariff expenses for the full year will be between $170 million and $180 million. Trump supporters keep cheering the tariffs. They haven’t figured out yet who will have to pay for them.

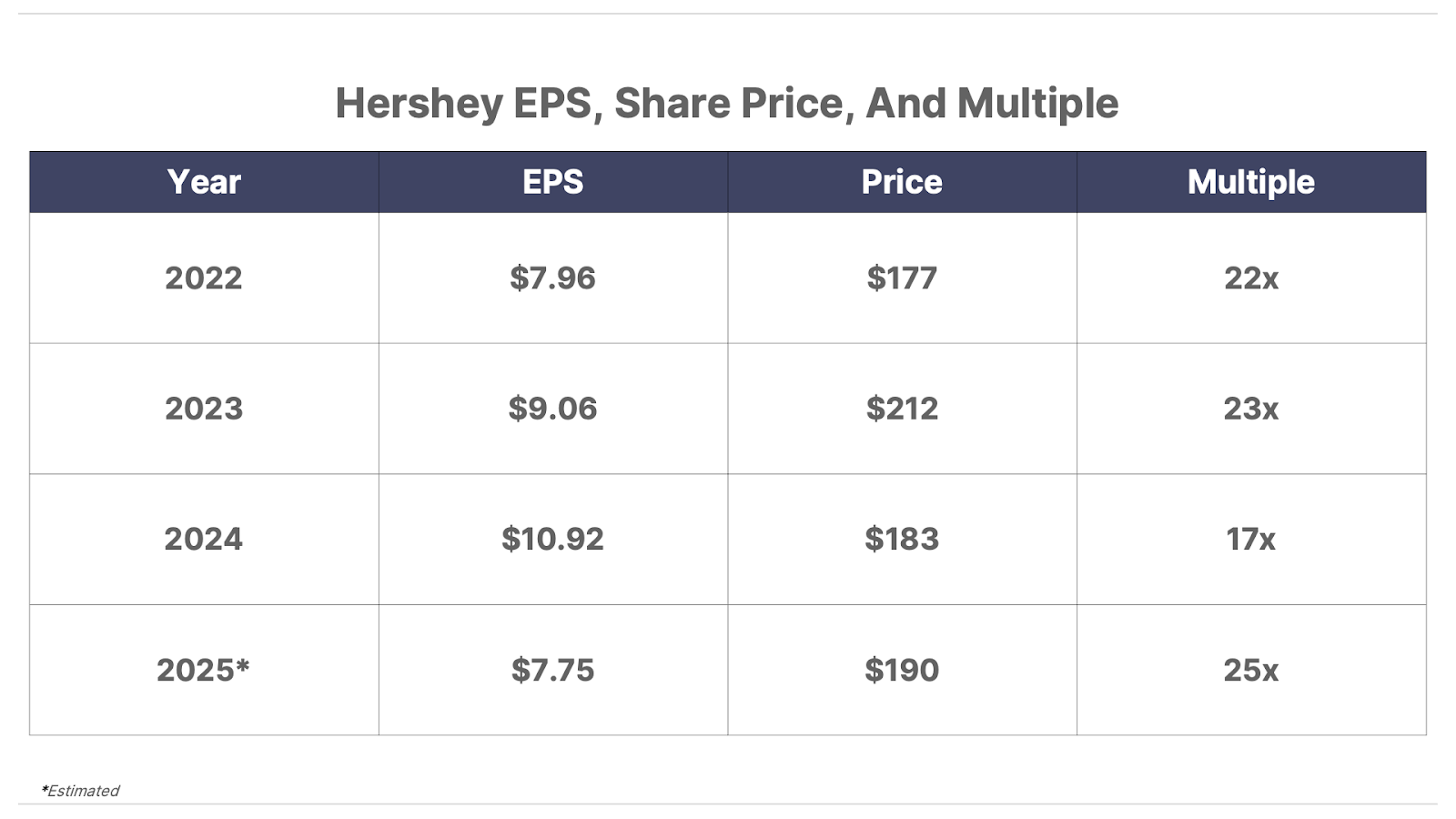

- The combination of higher cocoa prices and tariffs has driven gross margins down from 40% to 30%, which is having a very negative impact on profits and earnings per share (“EPS”). The company now predicts adjusted EPS will decline by at least 35% from last year, to between $5.36 – $5.69.

Why on Earth would I be bullish?

Because, in the fine print, the management explains a major factor:

Adjusted 2025 projected earnings per share-diluted, as presented above, does not include the impact of mark-to-market gains and losses on our commodity derivative contracts.

Last year, Hershey made $460 million from its hedging activities. With about 204 million shares outstanding, that’s $2.25 per share in earnings from hedging, or around 20% of total earnings.

I have no idea how much Hershey will earn (or lose) this year on its futures contracts. I have zero visibility into its hedge book. To date they’re reporting $200 million in hedging losses (mark-to-market), but it’s impossible to know what this will mean by the end of the year. During the earnings release conference call this morning, the company said it has locked in 2025 cocoa prices “well below the market” through robust hedging practices.

The key fact to remember is, if they lose money on the hedging, they will have higher margins on their products. And reported gross margins in the Q2 were terrible – 30.5%, down from 40.2% last year. That’s why I expect they will make money on their hedges. How much won’t be disclosed until the Q4 report, which typically occurs in mid-February.

Let’s say the company earns $5.50 in operations and another $2.00 in hedging. That’s $7.75 per share.

Is the multiple high? Sure, but earnings are, in my view, at a cyclical low. Hershey is responding to the tariffs and the higher raw materials costs, by raising prices substantially by around 20% this year. I expect another price increase next year too. Tariffs aren’t free. Neither are higher taxes and never-ending inflation.

Since 1969, when Hershey famously began increasing prices on its core Hershey’s bar product, it’s consistently kept pace with inflation, maintaining its excellent profit margins and its extraordinary return on equity. Over time, these price increases will grow the business substantially, proving, once again, the value of Hershey’s incredible brand and its unique position in America’s economy.

Historically you’ve done very well buying Hershey below 15x trailing earnings. That’s around $1.63 currently, using full-year 2024 earnings.

This year, the stock traded in that range from mid-January through mid-February. And then again from mid-May until about three weeks ago. Since July 9, shares have traded higher virtually every day, from $160 to $190.

Subscribers often express frustration with me because strategies like this are long-term and don’t offer good entry points.

This year has been a great opportunity to establish your own “Hershey Retirement Fund,” and I hope you’ve taken advantage of it.

If you have, I’d love to hear from you. Likewise, if you have been a long-term investor in Hershey, I’d love to know how using this strategy has impacted your retirement (or your retirement planning): [email protected]

Also, while we hope you won’t share our work routinely, if you know someone who could benefit from understanding this strategy and why it works so well over the long term, please feel free to pass it along. Especially if you have children (or grandchildren) who are interested in building a great retirement fund.

LIMITED TIME ONLY: Backdoor Exposure To SpaceX

Presented by Crowdability

🔑 Inside this limited-time presentation, a private equity expert reveals how you can use a simple 4-letter ticker symbol to gain pre-IPO exposure to Elon’s next trillion-dollar company — SpaceX.

👉 Get the ticker symbol now, completely free, no strings attached.

Three Things To Know Before We Go…

1. The U.S. needs to borrow a massive amount of money. Earlier this week, the U.S. Treasury Department announced it expects to borrow over $1 trillion in the July-through-September quarter, nearly double what it originally announced in April. This represents a huge increase in borrowing. This morning, the Treasury Department noted it will largely meet this issuance through short-term borrowing while keeping longer-term debt issuance steady. It also said it plans to increase its debt-buyback program – targeting older, less liquid 10- to 30-Treasury securities – from $30 billion per quarter to $38 billion. Together, these moves can be seen as an attempt to help keep the government’s increased borrowing from pushing long-term Treasury yields higher. However, they also expose the Treasury to greater interest rate risk should short-term yields begin to rise.

2. Altria earnings foreshadow a British Tobacco beat. America’s largest tobacco company Altria (MO) reported Q2 earnings today. One notable highlight: sales of Altria’s on! brand of nicotine pouches increased 27% year-on-year… but its market share dropped 2.3 percentage points. This follows the mildly disappointing results from Philip Morris’ (PM) ZYN brand of nicotine pouches last week, where shipments fell quarter-on-quarter for the first time. This suggests that a third brand in the booming nicotine-pouch market is gaining significant market share. And we suspect that this market share gainer is the VELO brand from British American Tobacco (BTI), which sets up for a positive earnings surprise when the company reports Q2 results tomorrow. We’ll be watching.

3. A bellwether feels the pinch. Procter & Gamble (PG) – whose household products fill the pantries of the rich and poor across the country – announced on Monday that U.S. consumers are holding back and looking for bargains. “The consumer is under some level of stress,” said CFO Andre Schulten. He adds that the slowdown is across all demographics – with lower-income levels buying fewer things and the higher-income shoppers looking for deals. Echoing a sentiment perhaps shared by other companies, outgoing P&G CEO John Moeller said: “The company faces more challenges now than any time I can remember.”

And One More Thing… Wingstop (WING) Flying High

Chicken-wing franchisor Wingstop (WING) released blowout Q2 results this morning – reporting 12% revenue growth and a record high $1 per share in earnings, 15% ahead of analyst expectations. Plus, ravenous franchisee demand led to a 19.8% increase in its store count in Q2. These results are all the more impressive considering that the world’s best-performing fast casual brands – such as Chipotle (CMG), Starbucks (SBUX), and McDonald’s (MCD) – are struggling among sluggish consumer demand. We believe Wingstop can become one of the greatest long-term wealth compounders in the fast casual industry. We first recommended the company in The Big Secret On Wall Street last November, dubbing it the “Chicken Wing King.” Shares are up 29% year-to-date but we see more upside ahead.

Monday’s Poll Results

In Monday’s Daily Journal, we reported that the CBOE Volatility Index (VIX) tends to jump above 22 in the fall months, prompting us to poll readers with the question: Will the VIX climb above 22 by October 1?

Most readers think so… with 86% of survey takers saying yes, and just 14% saying no.

Tell me what you think: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland