Issue #52, Volume #2

Exploring An Investing Myth That Permeates The Financial World

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| U.S Treasuries are anything but risk-free… There is interest rate risk… There is default risk… Trump’s liberation day announcement created a large-scale sell-off… Don’t get misled by imprecise talk about risk-free and risky securities… What the Fed said today… |

In early April, President Donald Trump announced higher tariffs on U.S. trading partners than the market was expecting, and the financial world reacted… triggering mass selling of U.S. Treasuries by foreign central banks.

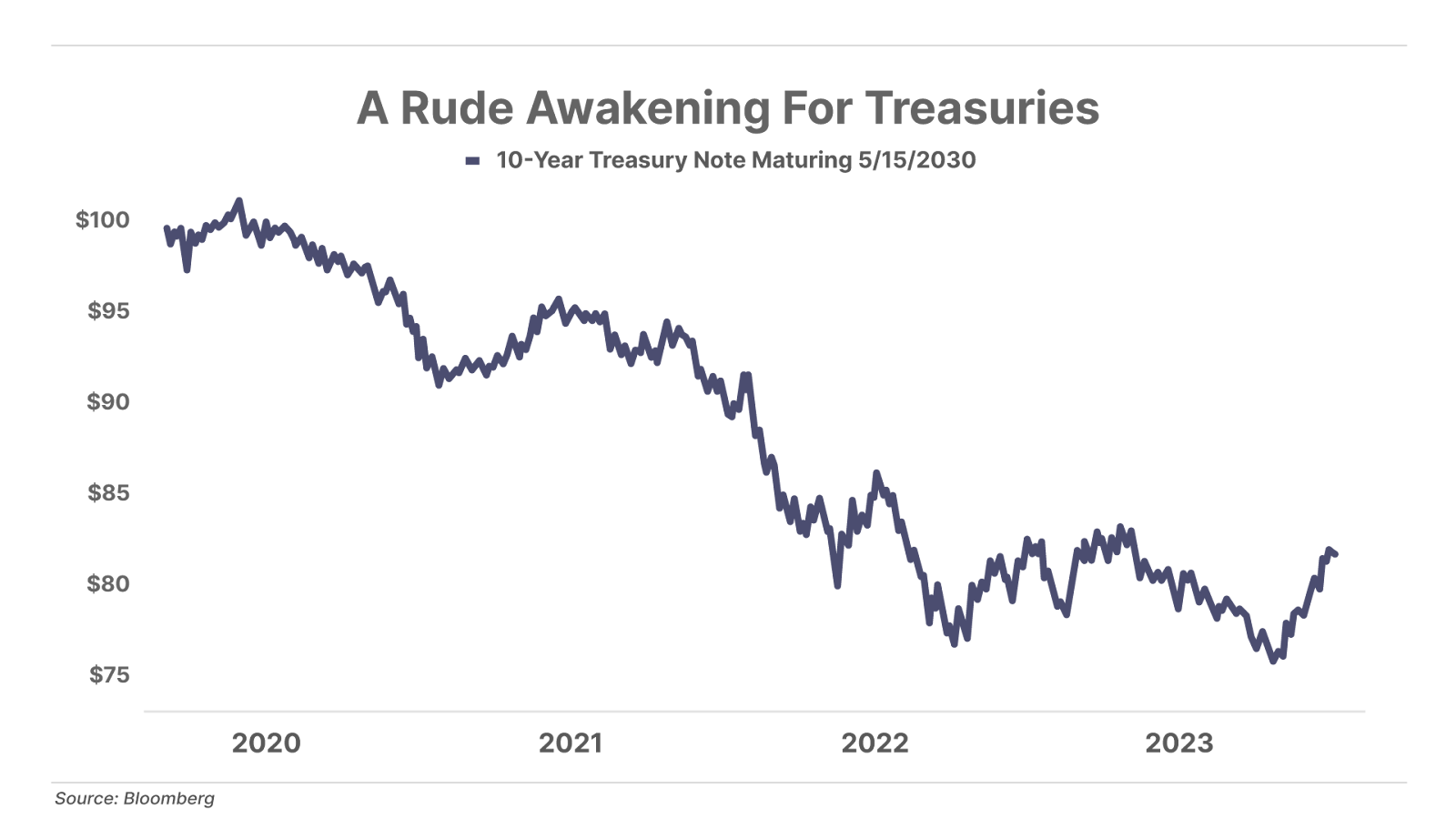

The 10-year Treasury bond’s price dropped 2.2% between April 2, when tariffs were announced, and April 11 – a big move in such a short period. The selloff was significant – and highlighted the higher-than-understood degree of volatility that comes with investing in Treasures, which are normally viewed as risk-free.

Today we’ve turned the Daily Journal over to Distressed Investing senior analyst Marty Fridson, who explains the risks involved in investing in U.S. Treasuries – something readers should consider as more of the same market uncertainty could be in store if Trump’s tariff policies continue to siphon away global confidence in the U.S. dollar.

Here’s Marty…

Perhaps the greatest of all the financial myths out there is that investing in U.S. Treasuries is a risk-free endeavor.

The truth is that a U.S. Treasury security with a 10-year maturity is anything but risk-free.

The risk-free rate is a theoretical value that financial theorists use to adjust return for risk, as in calculating a stock’s Sharpe ratio, which compares the return of an investment with its volatility. Risk-free rate is usually represented by the yield on 90-day U.S. Treasury bills, not by longer-maturity Treasury notes or bonds. Over the past 20 years, the T-bill rate has averaged 1.25 percentage points less than the 10-year Treasury rate, although the two happen to be very similar right now.

One type of risk that investors definitely care about is interest rate risk. As the Wall Street Journal frequently reminds its readers, when interest rates go up, bond prices go down.

And how!

Between June 2020 and July 2023 the yield on 10-year Treasuries rose from 0.54% to 5.46%. Anyone who thought those securities were risk-free received a rude awakening when their value dropped 25%.

What confused the unfortunate investors into thinking their Treasury bonds were “risk-free” had to do with another sort of risk, namely, default risk. Unlike many corporate bond issuers over the years, the U.S. Treasury has never failed to pay its contractual interest or principal due in full and on schedule. It’s widely believed that there’s no danger of that ever happening in the future, either. After all, the U.S. government can print money to meet its debt obligations, so how could it ever fail to make good?

There’s at least a shadow of a doubt on that point in the opinion of Standard & Poor’s. In 2011, the credit-rating agency dropped the U.S. Treasury from its highest category, AAA, to the next step down, AA+. That puts S&P’s assessment of Uncle Sam’s capacity to meet its financial commitments in-between “extremely strong” and “very strong.” By S&P’s reckoning, Johnson & Johnson (JNJ) and Microsoft (MSFT) are more reliable borrowers, as indicated by their intact AAA ratings. Note that all of these ratings address only default risk, which encompasses both the probability of default and the expected recovery of principal in the event of default. Credit ratings do not measure interest rate risk of the kind responsible for the above-mentioned 25% drop in the price of the 10-year Treasury bond.

The underlying reason for S&P perceiving a greater-than-zero risk of default for the U.S. is that the government is spending way much more than it’s taking in through taxes. Sure, the government can print money to avoid default, but that works only up to a point. If one day the resulting expansion of the money supply leads to such severe debasement of the dollar that America’s creditors suffer a ruinous loss of wealth despite being repaid “in full,” the credit-rating agencies will deem that a default. By the way, the Treasury’s rating will have fallen far below AA+ long before that ever happens.

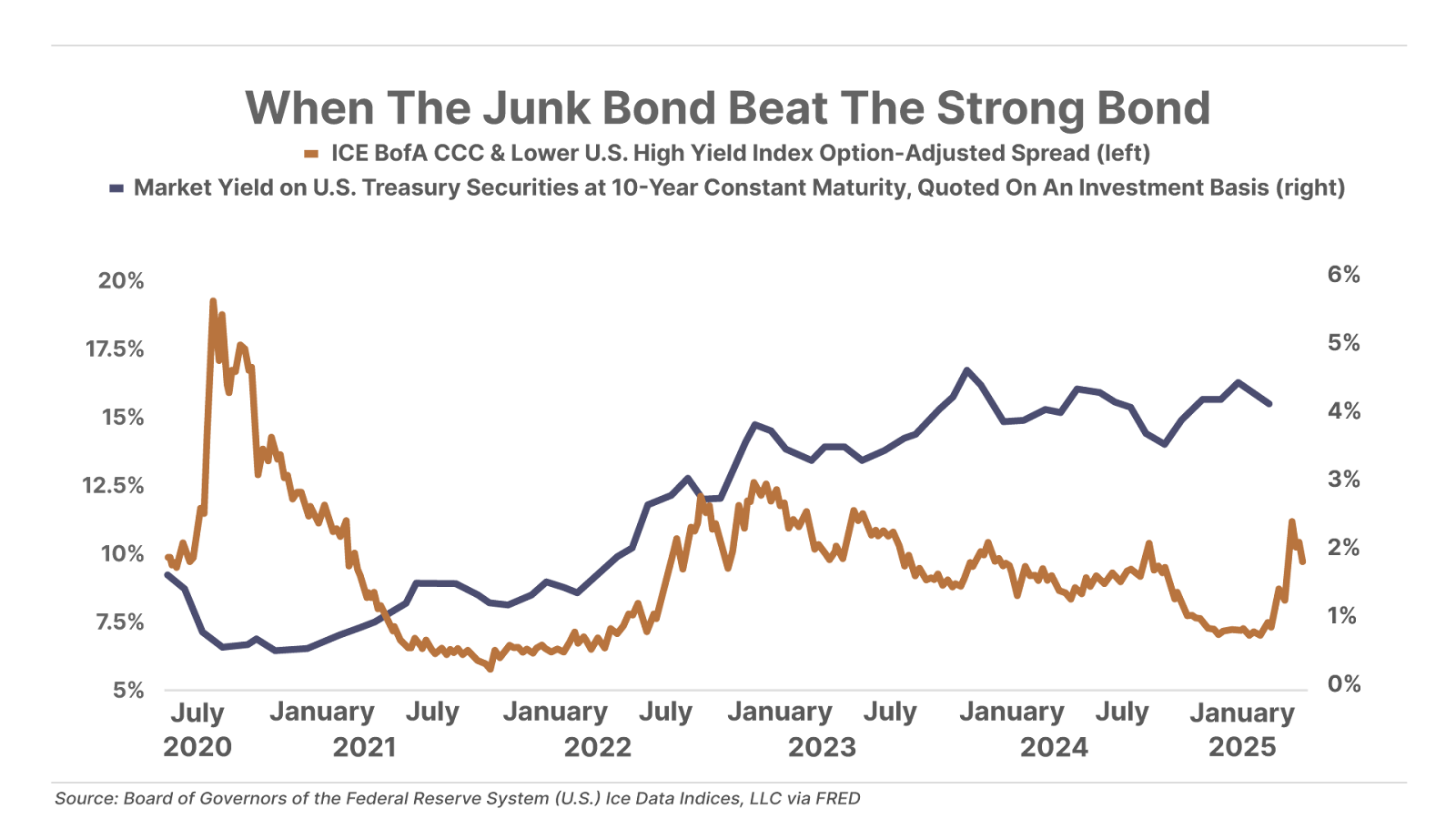

Why all this matters is that a full understanding of risk is essential to successful investing. In the case of bonds, default risk and interest rate risk can interact in surprising ways. Consider the polar opposites of “risk-free” Treasuries. If you search online for “risky bonds,” you will learn that the term is synonymous with “high-yield” or “junk” bonds. Those are speculative-grade corporate bonds, rated several tiers lower than Treasuries, BB+ or below. At the bottom of that category – excluding issues already in default – are bonds rated CCC, CC, or C.

In the 2020-2023 period of soaring interest rates, as the price of 10-year Treasuries sank 25%, the ICE BofA CCC & Lower U.S. High Yield Index experienced just a 3.5% price erosion. Taking into account the interest earned along the way, those junkiest of junk bonds won hands down, with a 25.5% total return versus negative 20% for the very / extremely-strong Treasury bonds.

This outcome will strike many readers as paradoxical, but it actually makes logical sense. As the economy rebounded from the pandemic-induced 2020 recession, default risk decreased dramatically for bonds rated CCC or lower. That variety of risk reduction cushioned the impact of the rise in interest rates that devastated the prices of long-term Treasury bonds. Because the likelihood of default is so minimal for Treasuries, there wasn’t a lot of room for them to benefit from a reduction in that risk category.

A further wrinkle in the risk-return relationship is that the bonds in the ICE BofA CCC & Lower U.S. High Yield Index have an average maturity of only 3.6 years. Price sensitivity to changes in interest rates is partly a function of maturity. Accordingly, the bottom-tier speculative-grade bonds had an advantage over 10-year Treasuries as interest rates began to escalate.

To add still one more piece to the picture, Treasury and high-yield bonds also differ dramatically in their exposure to a third kind of risk, the risk of illiquidity. When the high-yield market goes into the tank, we invariably start hearing the phrase, “Don’t try to catch a falling knife.” Translation: Any bond you buy today will be at a loss tomorrow, so don’t make any bids. The upshot is that from time to time, high-yield bondholders find themselves in the unenviable position of being unable to sell holdings to reposition their portfolios or to meet current cash needs. In contrast, Treasury investors never face that predicament because their bonds trade in the world’s deepest, most liquid market.

The flip side of always being able to get out of a Treasury bond is that, at times, that’s exactly what everyone wants to do. Most recently, President Donald Trump’s announcement of higher tariffs than the market was expecting triggered selling by foreign central banks. There was also large-scale selling of Treasuries by commodity traders scurrying to unwind leveraged “basis trades” aimed at exploiting disparities between spot prices and futures prices.

It was a classic case of more sellers than buyers. The 10-year Treasury bond’s price dropped 2.2% between Liberation Day, April 2, and April 11, a huge move for the Treasury market in such a short period. Investors currently contemplating a flight to the safety of U.S. government debt need to consider that more of the same could be in store if the present uncertainty surrounding tariffs gives way to certainty that global confidence in the U.S. dollar is waning.

Risk has several more dimensions than the average investor imagines, but the key takeaway is straightforward: Don’t get misled by imprecise talk about “risk-free” and “risky” securities. In some circumstances, even the distressed bonds we recommend in Distressed Investing – which have decidedly non-negligible default risk – deliver far better results than “gilt-edged” government obligations.

Porter recently released a documentary explaining how he is rebuilding his financial life using distressed debt as his foundation… To watch the video, click here, or call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447, for more information about getting access to Marty Fridson’s Distressed Investing.

Three Things To Know Before We Go…

1. The iPhone War begins. Tensions are flaring between India and Chinese-backed Pakistan, with India launching retaliatory missile strikes on its neighbor after Pakistani militants killed 25 Indian civilians last month. Not coincidentally, this follows recent news that – as a result of President Trump’s steep tariffs on Chinese imports – Apple will be making all iPhones in India rather than in China. President Xi Jinping will not allow this. This is how trade wars lead to real wars.

2. Credit ratings plunge as student loan delinquencies soar. As we warned in March, missed payments are piling up now that COVID-era forbearance has ended. According to credit-reporting agency TransUnion, the 90+ day delinquency rate on student loans has jumped to 20.5% – nearly double the pre-pandemic level of 11.5% – and credit scores have dropped by 171 points. The situation is only getting worse as the Department of Education will begin pushing harder on collections. As of May 5, borrowers in default will be subject to wage and Social Security garnishments. With credit scores in free fall, a broader consumer credit crunch may be just around the corner.

3. The Fed stands pat, but warns of stagflation. As expected, this afternoon the Federal Reserve kept interest rates unchanged in a range of 4.25% to 4.5%. However, it noted that the risks of both higher unemployment and higher inflation have increased as a result of President Trump’s tariffs. In his post-meeting press conference, Fed Chair Jerome Powell said it was still too early to know whether inflation or employment should be the central bank’s primary concern. As a result, he said the Fed is likely to continue to “wait and see” how tariffs affect the economy before adjusting interest rates – either up or down – again.

The Clock Is Ticking on the U.S. Market Meltdown

The markets are teetering on the edge of chaos. Inflation is running wild. The Fed is trapped. And the economy? It’s hanging by a thread. The last time we saw conditions like this, portfolios were wiped out in a matter of months. Some never recovered. But there’s one investment strategy that not only survived past crashes – it thrived.

And One More Thing… “Saturday Stock Screen” Finds A Winner

In the April 26 “Saturday Stock Screen,” in the Partners-only stock report, we introduced online resale platform ThredUp (Nasdaq: TDUP), noting that 2025 could be the year the company begins generating sustainable profits and cash flows… Yesterday, the company delivered, reporting $2.5 million in positive free cash flow for Q1 – the largest number since its inception as a public company. It also posted 10% year-on-year revenue growth, the fastest pace since mid-2022. Shares gained 42% on the news, rising 50% from when we reported on them two weeks ago.

To learn about becoming a Partner Pass member – gaining access to Saturday stock reports as well as everything else that we publish at Porter & Co. – call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.

Tell us what you think: [email protected]

Mailbag

Hi Porter:

A lot of what you publish is cautionary at best and more often downright bearish. At least that’s the way I read it. So if that’s a major theme of yours, why do you recommend selling puts? Seems like selling puts is the last thing you want to do if the market will be hitting big potholes.

The fact is selling options caps your upside and leaves you an unlimited downside. It’s an asymmetrical trade. Hedging with even more options/spreads, etc., quickly becomes counterproductive. I now limit myself to long option positions, and even that pretty rarely.

Thanks, Willy G.”

Porter’s comment: Willy, that’s a great question! I am “downright bearish”!

And, I hope you’ll see why below, where I give a pretty detailed explanation.

I believe interest rates are going much, much higher. And I think that will lead, eventually, to a U.S. government default, which most people believe is impossible.

But, first, just to answer your question directly about options:

Options provide incredible financial benefits to investors who know how to price them. Much like stocks, options are frequently badly mispriced, creating additional opportunities for investors, especially during periods of market panic.

I believe that over the next two to four years we are going to see frequent bouts of substantial market volatility. I’m talking about massive dislocations and a dramatic preference for safe liquidity. I’m talking about periods like the summer of ’32. The Nixon panic of ’73. The panic of ’07. The winter of ’09. The COVID collapse of ’20.

At some point, history books will be written about the default of ’29. And those books won’t be about 1929, but about 2029.

These are the macro cards we’ve been dealt. And they are not bullish for freedom, for peace, or for equity investors.

But, ironically, that’s the good news.

You see, investors pay a very high price for a sunny outlook. And it’s during periods of crisis and volatility that fortunes can be made. Like the famous 19th-century speculator Daniel Drew explained: “I never made more money or had four years that were all in all more genuinely prosperous, than those four years of the War,” in reference to the markets during the American Civil War.

We had a period just like that last month. And, at these moments of panic, you can make incredible returns. I just closed out the puts I sold on Hershey (HSY), which I told you about last week, for a profit of $53,560!

Making these kinds of trades can dramatically increase your total returns. The trick of course is limiting your risk. I was selling puts on a business I’d very much like to own, at a price I was happy to pay. By rolling these puts forward, I can continue to build a premium, or supply of cash, that I’ll later apply to buying actual shares. I think there’s a reasonable chance that the premiums will end up paying for 50% to 75% of my intended $1 million investment into Hershey.

There are plenty of companies – Philip Morris International (PM), Hershey, Coke (KO), Lockheed Martin (LMT), Franco-Nevada (FNV) – that are likely to do better during these hard times.

I firmly believe these kinds of stocks are the very best way to protect yourself during a monetary crisis. They are also the best way to continue to build wealth for decades.

But that doesn’t mean that you won’t see volatility in their share price. You will! And during periods of volatility (like we saw last month) the premiums on put options on these stocks will soar. During these episodes, you can do very well selling puts on stocks you’re happy to own.

Think of it this way – if the market gives us a 30% discount from intrinsic value on, say, Microsoft (MSFT), and you can sell a put with a 20% premium and a strike price that’s 10% below the market, you’ll be getting a 50%+ discount from intrinsic value if you’re put the stock. Thus, there are two potential outcomes: you make a great investment that you plan to hold through the crisis, at a very attractive price; or you pocket a 50% to 100% gain on margin in a matter of days.

My point is, there’s no downside – as long as you carefully follow our rules about selling puts. And, of course, you will need enough capital and a margin account to follow this strategy. You’re saying this “caps your upside” and leaves you with unlimited risk. But that’s not true.

Your upside is unlimited. You may be put the stock and you’ll keep the premium, no matter what happens. In that case, your upside is unlimited. And, whether you’re simply buying the stock or buying with a premium, your downside is the same.

I’d argue there’s zero additional risk from selling puts, provided you’re doing so on stocks you genuinely want to own at a price that you’re happy to pay. Investing in stocks requires emotional discipline and time: never buy a stock you can’t hold for at least five years – and 10 years is safer. But you won’t convince me that getting paid a handsome premium on a strike price that’s below the market is more risky than simply buying the stock. It’s objectively less risky.

As you’ll see in our forthcoming Trading Club, we plan to maximize our gains on these increasing periods of volatility in four ways:

#1. Selling puts, at points of maximum pessimism – when the CBOE Volatility Index (VIX) is over 30 – on the highest-quality stocks in the market and only at strike prices that we believe are far below intrinsic value.

#2. Buying puts, at moments of maximum optimism (VIX below 20) on companies with flawed business models or situations, like Apple (AAPL) currently, where there are real and major headwinds on a highly overvalued stock. These positions will be scaled to be about 1/10 the size of our put-selling campaigns. These positions are “hedges” designed to protect us from a sudden collapse in equity prices.

#3. Selling calls to generate income on positions we hold that we believe are fully valued. Our strategy here is to always select a strike price that we believe is unlikely to be filled, or where we’d be happy to sell.

Now… why I am I so certain that we’re heading for a serious economic crisis?

As Warren Buffett noted last week in his annual address to shareholders, we’re on an unsustainable course. A serious reset must soon occur. I’ve predicted that we will default on our debt within the next four years.

Here are the facts: So far in fiscal year 2025, the U.S. government has spent $3.57 trillion, which is a $315 billion increase from the $3.25 trillion spent during the same period in fiscal year 2024. That’s about $2 billion more spending, every single day, or about 10% more spending.

And counter to the Trump administration’s propaganda, the spending isn’t going to stop.

Trump’s current budget request for 2026 reveals a decrease of 7.6% in discretionary spending, which is a reduction of… wait for it… $139 billion. That’s, potentially, a 1.8% decrease in total spending. Meanwhile, Trump can’t do anything about the real problem: soaring growth in mandatory spending (Social Security, Medicare, and interest on the debt). These costs have risen 6% so far this year and they make up the vast majority of the Federal budget ($4.1 trillion in 2024 out of a total of $6.8 trillion).

Here’s the thing that nobody is willing to say out loud: the more money the government prints to cover its deficits while controlling interest rates, the higher inflation will go.

This is the doom loop: deficits and debt refinancing this year will exceed $10 trillion in new Treasury issuance. Total domestic savings are around $5 trillion. And foreign Treasury buyers are now selling, in part because of our relentless money printing and in part because of the trade war. That’s why the price of gold is soaring.

These market realities (we can’t sell $10 trillion worth of Treasury bonds without much higher interest rates) will lead to the most expedient answer: print money to buy bonds. And that’s exactly why the Fed bought $35 billion worth of bonds this week.

The printing will never stop because the spending will never stop.

More printing will lead to more inflation. And more inflation will lead to both higher interest expenses and much higher mandatory spending.

Social Security and Medicare are indexed to inflation via legally required, automatic, annual cost-of-living-adjustments (“COLA”), using the urban consumer price index (“CPI”). Thus, as more and more money is printed to maintain stability in the bond markets, automatic and legally mandatory spending will grow in equal measure.

This is a death spiral: the more we print, the more we owe. The more we owe, the more we spend.

This is how all Ponzi schemes end. And, eventually, the demands for income overwhelms all of the assets. I believe we’re on the brink of that happening. The expenses of the Social Security system have grown 22% faster than GDP for the last 30 years! It’s like a tapeworm eating the entire economy. As a result, mandatory federal spending has increased 50% relative to its 1995 levels… from 10% of GDP to 15% of GDP.

These obligations have a current net present value – as of today – of almost 200% of GDP: $70 trillion. And that does not include future liabilities as more people are added to the rolls. Since automatic COLAs were legislated by Congress in 1975, the U.S. has been walking down the primrose path to socialism and its corresponding economic problems.

And we won’t stop. Today direct payments from the federal government (Social Security and Medicare mainly) make up more than 25% of the total income of more than 50% of the counties in the United States.

Thus, in virtually every Congressional district in the U.S., the most important item on the agenda is to ensure this spending continues: without it, these counties collapse. And because the COLA increases are both legally required and automatic, the president can’t stop them. Congress would have to vote to rescind these increases – and that will never, ever happen.

Thus, collapse is inevitable. And it’s going to happen a lot faster than anyone expects because of the powerful dynamic of inflation, soaring interest rates, and rising costs.

Don’t believe me?

Here’s another way to view these risks.

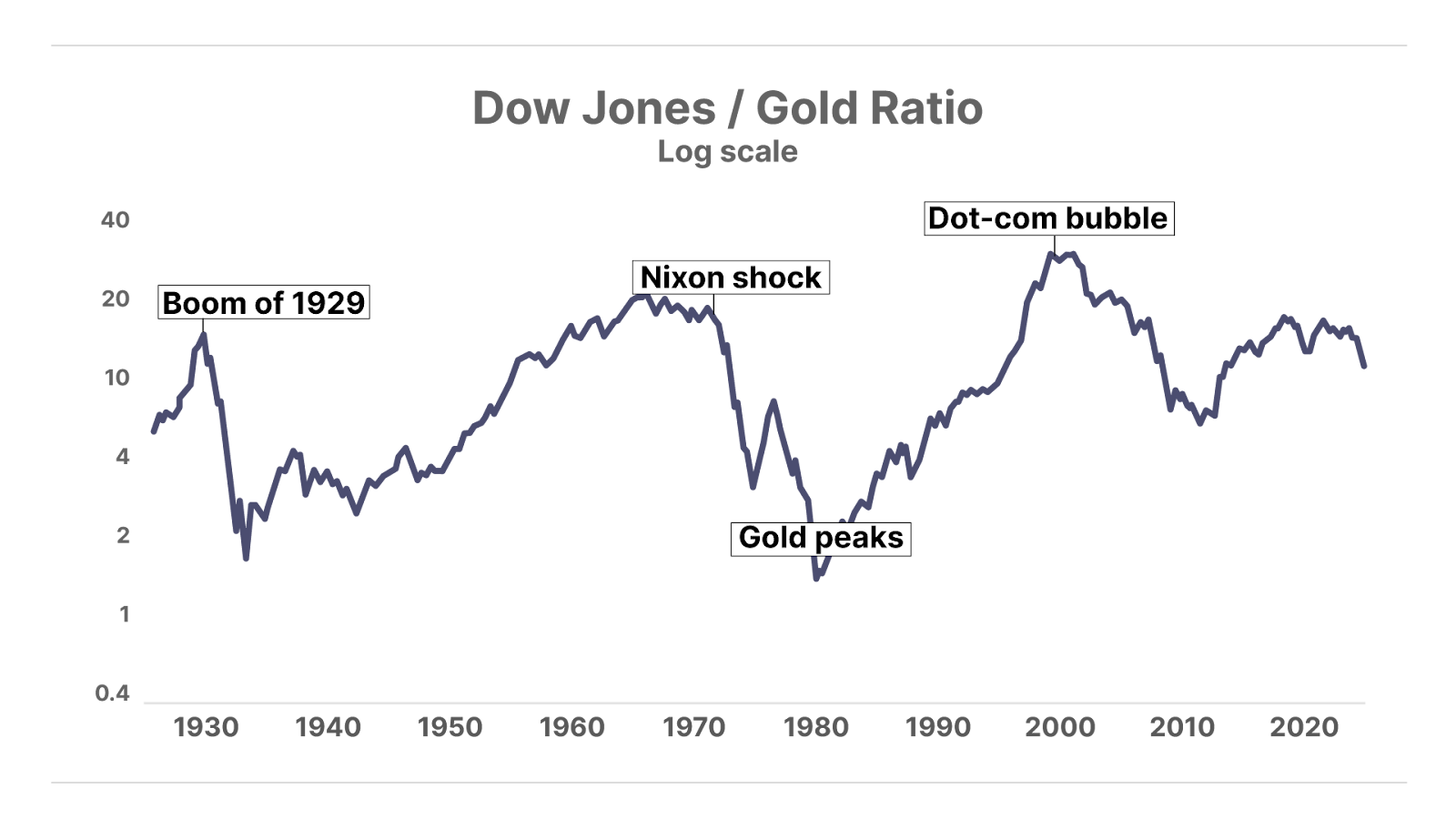

Look at the value of equities relative to gold. While this measure of valuation isn’t commonly embraced by Wall Street, I believe it shows something that is extremely important. This is a measure of financial stability: it reveals how much faith and trust most people have in the financial system – stocks, bonds, trade, currency, etc. – on a relative basis.

When people dramatically prefer gold to stocks, there is no trust and society begins to collapse.

You can see the market’s distrust of financial assets and preference for gold has historically peaked after crisis periods – like after President Franklin Roosevelt shut down the banks, seized privately owned gold, and launched the New Deal. And like after President Richard Nixon shut the gold window and instituted a range of price controls in the 1970s. We are heading toward a crisis like that – a major depression. I know because we haven’t seen a peak for gold yet, even though the Dow/gold ratio has been falling since 2000.

Consider this: Even though gold has outperformed Buffett’s Berkshire Hathaway for the last 25 years (!), we’ve yet to see a real mania for gold. I’d bet that almost no one you know owns any of it – not even an ounce. Perhaps that’s because Bitcoin has absorbed some of the demand for a more trustworthy form of money, but I doubt it. In a real crisis, people will want gold. And that’s why central banks around the world have been buying it at record levels.

So before this cycle ends, we are very likely to see a Dow/gold ratio well below 5, meaning that three ounces of gold will buy the entire Dow. Today that ratio is around 12. And, remember, the bottom will come after the government defaults.

We’re about to enter a period unlike anything we’ve seen in America since the 1860 and 1870s. We’re heading into something akin to a civil war.

On the one side will be asset owners. And on the other side, people who support efforts for the government to redistribute wealth – through Social Security and Medicare, through wage and price controls, through federal funding for housing and education and through direct payments, like New York State just announced: refund checks for poor people because of inflation! Imagine the lunacy of fighting inflation through more government redistribution! That’s what’s coming.

This war on private wealth will happen across the West. See Australia’s plans to place a 40% tax on all retirement accounts above $3 million in value. Think that won’t happen here? Just watch.

The entire Western, democratic world is broken.

And there’s not much more dangerous than a bankrupt mob.

But it will also be the greatest period of speculation of our lifetimes.

Pass the popcorn. Let’s watch the show!

Good investing,

Porter Stansberry

Stevenson, Maryland

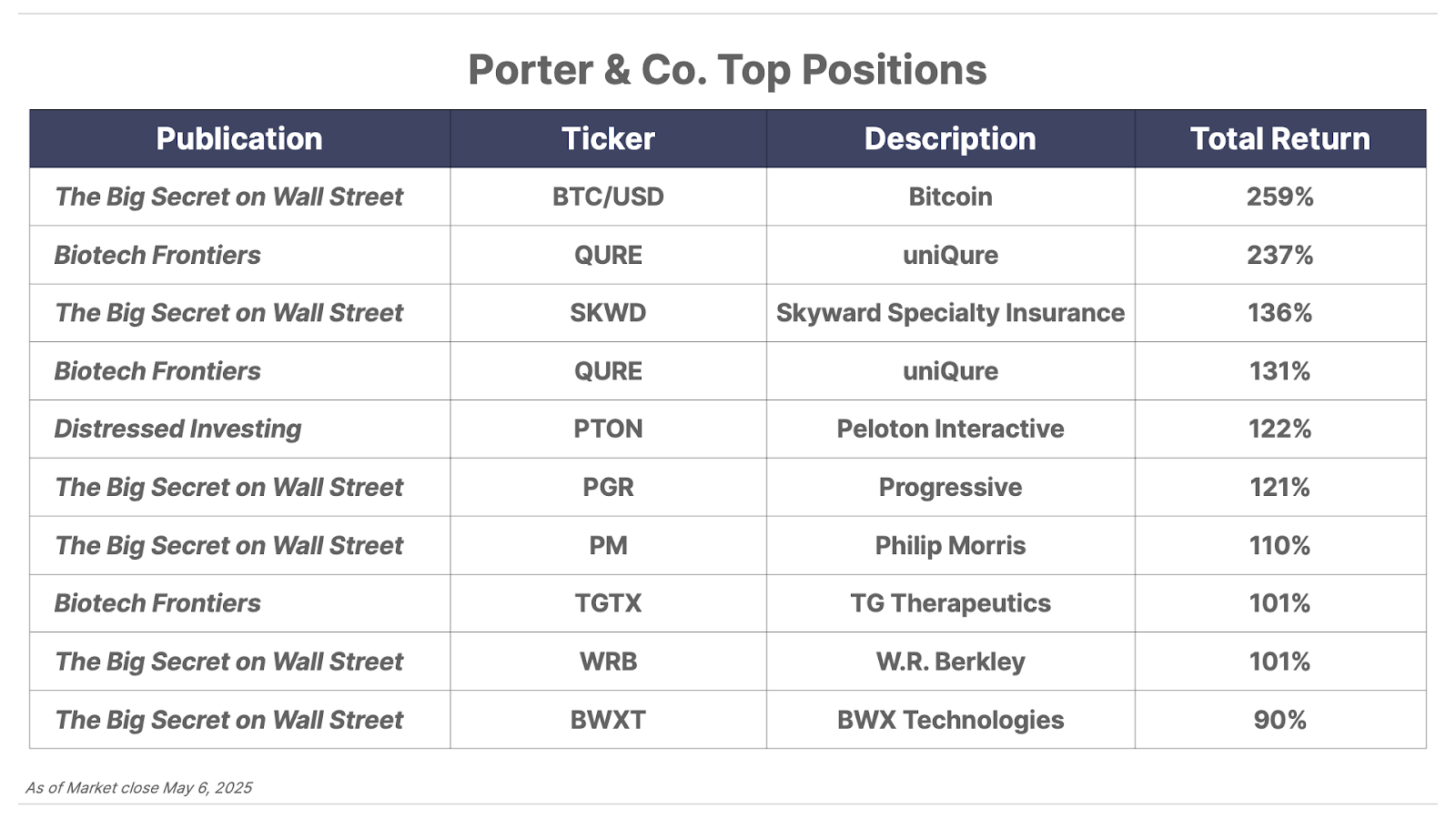

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.