Issue #73, Volume #2

Why We Believe In Capital Efficiency And Owning Individual Stocks

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

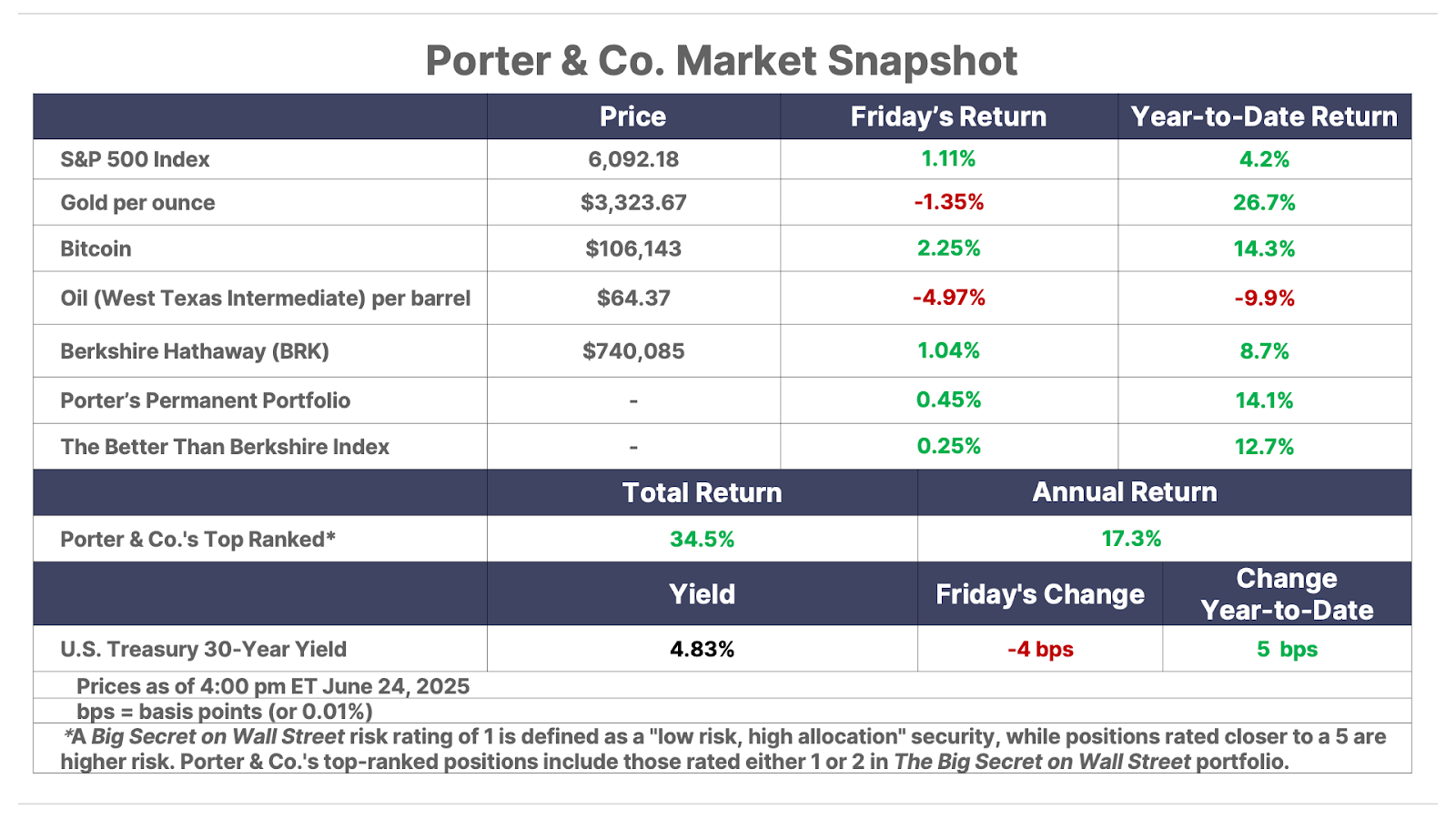

| Conservative investing should not be defined by “indexing”… Charlie Munger said to invert – turn the question upside down… Owning the S&P 500 means owning lots of bad businesses… Buy high-quality, capital efficient businesses… Is Trump going to fire Powell? |

Everything you’ve probably been taught about investing is wrong.

Most people have been brainwashed by Vanguard and Fidelity to believe that prudent, conservative investing is defined by “indexing” – owning a huge basket of stocks, to minimize volatility – and dollar-cost averaging. These firms produce volumes of research that “proves” this massively-diversified approach to investing is the safest and best way.

But it’s complete nonsense.

There are three massive flaws of logic inherent to index investing.

Berkshire Hathaway’s vice chair, the late Charlie Munger, always taught that good thinking happens backwards. The best way to solve difficult logical puzzles with many unknown variables was to “invert”: turn the question upside down. Start with the answer. Then work backwards. Want to figure out how to get someplace you’ve never been before? Start there on a map and then work backwards to where you are located.

What do you want to achieve as an investor? Outstanding results that compound over the long term, producing enormous wealth, without any risk of permanent loss of capital.

Can you achieve that by owning the S&P 500? Not very efficiently. And, most likely, not at all.

Since 2000, 52% of the Fortune 500 has ceased to exist – many because of bankruptcy. Notable failures include: Bear Stearns, Lehman Brothers, Merrill Lynch, Enron, Pacific Gas & Electric, Chrysler, Texaco.

If you own all of the stocks in the S&P 500, you’re guaranteed to own a lot of failing businesses.

The professors claim that index investing is safer, but they’re simply wrong. Why? Because they define risk as price volatility. Why? Because they can measure it. But is volatility actually risk? Of course not.

Over the last 25 years, Berkshire Hathaway has declined by more than 50% twice. But was its business actually at risk of failing or being permanently impaired? Absolutely not. In the real world (not the classroom) the volatility of a stock’s share price is not, in any way, fundamentally related to its actual business risk. And by focusing on avoiding volatility the professors have ignored the obvious risk to their approach: actual business failure.

So there’s logical error #1: the financial industry’s strategy locks you into failing businesses, instead of avoiding them.

But, that’s not even the biggest logical error.

The biggest logical fallacy of indexing is that it equates a high nominal market cap as “good” and a low nominal market cap as “bad,” as the leading indexes are market cap weighted, with the most expensive stocks receiving the most amount of your capital.

I think this might be the dumbest thing that most, otherwise smart, humans believe. It makes absolutely no sense.

In the first place, a company’s market cap isn’t even the best measure of its size. Many companies, for good reasons, finance their businesses with debt, as debt can vastly lower a company’s cost of capital. Completely ignoring this valuable part of the capital structure is ridiculous. If you were going to invest in businesses according to the size of their capital structures, you should be using enterprise value not market capitalization (market cap only tallies up the value of the outstanding equity).

But beyond measuring the wrong thing, the entire approach is well-proven to be deeply flawed. It “crowds” investor capital into a small number of very large stocks, which, because of their size, attract still more indexed capital… and grow larger and larger… which seems like you’re winning… except none of this increase in value is sustainable. It isn’t based on business value, but merely size. This strategy is a 180-degree perversion of how the market is supposed to function.

And so you’ll never guess what happens next: collapse. Look at what happened to these once index-leading businesses over the last 30 years: AT&T, GE, and IBM. Will Apple be next? Wouldn’t surprise me.

A 2019 study by Goldman Sachs found that the top 10 S&P 500 stocks underperformed the broader index over the subsequent 12 months in 60% of cases when concentration was high (top 10 stocks made up more than 20% of index weight).

So… do you want your capital spread across dozens and dozens of companies that will fail? Do you want to be heavily skewed into investing in companies with the most expensive (and overvalued) stocks?

No.

What are you looking for? You’re looking for one of a very small number of businesses that will compound your wealth over a very long period of time, at market-beating rates. How many stocks can do this…?

In 2018, Hendrik Bessembinder produced a landmark study of actual equity performance by measuring the outcomes of 26,000 different stocks between 1926 and 2016. He found that only 4% of stocks (approximately 1,000 stocks) accounted for all of the net wealth creation in the U.S. stock market. And there were what he called “power law winners” inside that larger Pareto group: Just 86 stocks (0.33% of the total) were responsible for 50% of the total wealth creation. Meanwhile, approximately 58% of stocks failed to outperform one-month Treasury bills over their lifetimes.

Most stocks are lousy investments.

And that leads us to the worst logical fallacy of index investing: that there’s nothing investors can do to accurately handicap businesses. Buying all of the stocks is the abandonment of judgment and reason. The professors’ excuse? There’s no other way to do reliably better.

That’s nonsense.

Any experienced business owner could tell you there’s a huge difference in the returns available to owners of businesses that scale and businesses that don’t. Why, for example, are restaurants such tough businesses? They don’t scale. Each location requires the same amount of capital and the same amount of labor. Gross margins can’t be improved meaningfully by adding more scale to the business. Contrast that with software. Or media. Or even manufacturing, where capital investments can vastly improve productivity.

The key to finding power law winners in the stock market is simple: invest in businesses that have outstanding economics.

I know that works because I’ve proved it throughout my career – most famously with my 2007 recommendation of Hershey (HSY), which I correctly predicted would go on to be the most profitable recommendation of my entire career. Not because it would boom. Or come to the top of the S&P 500. But because it was capable of compounding capital at a rate roughly twice that of other American businesses and was likely to continue to do so virtually forever.

I call this characteristic capital efficiency. You’ll find it in businesses that can produce very high returns on invested capital and therefore have high free cash flow margins.

To prove this isn’t merely luck or a fluke, I asked our in-house Non-AI analyst (Jared Simons) to conduct a long-term study of the outcome of investing in all businesses we would characterize as high-quality and capital efficient every year.

Specifically, we tested a systematic approach that assumed we invested in all of the available stocks that met these criteria: free-cash-flow (“FCF”) margins above 10%, return on assets (“ROA”) above 15%, more than 10% of revenue returned to shareholders, revenue growth of more than 5%, operating margins above 10%, and return on invested capital (“ROIC”) greater than 20%.

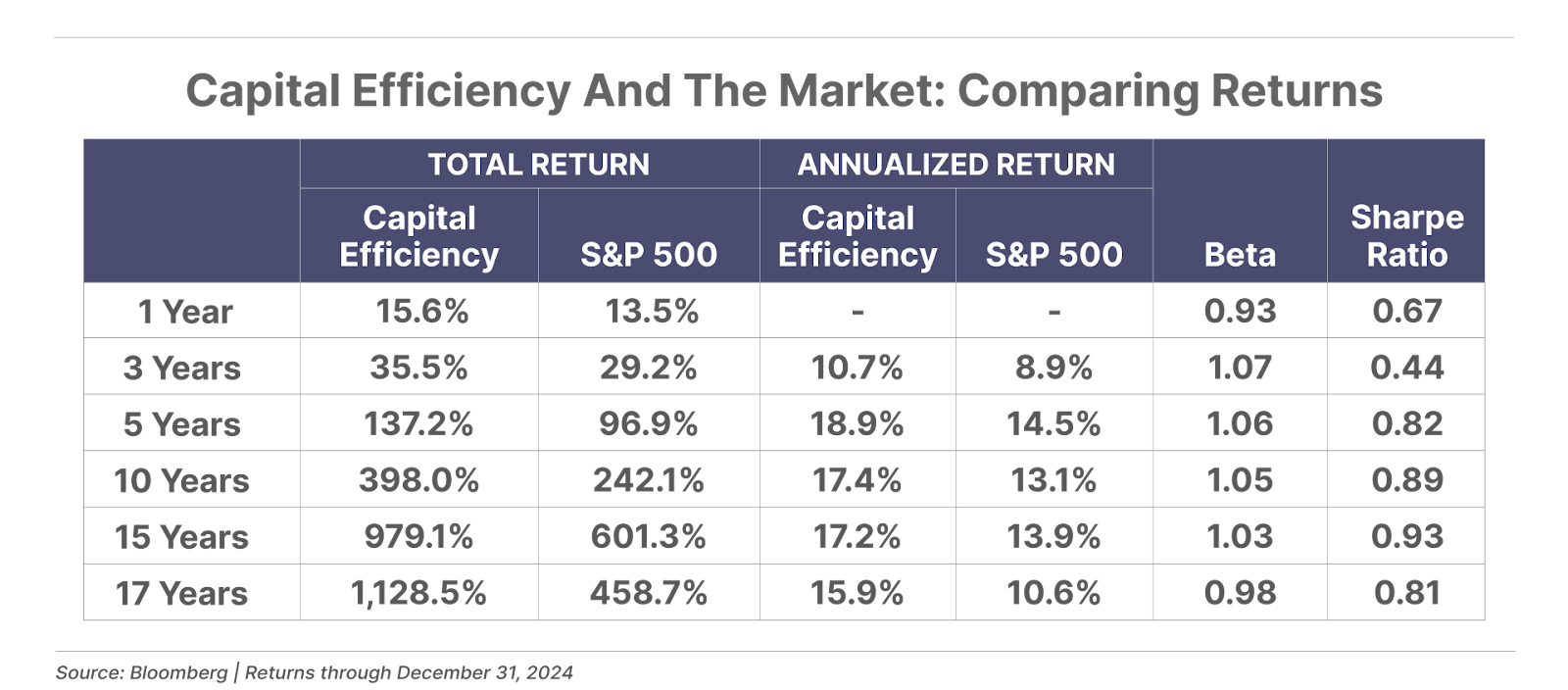

We were able to access high-quality data going back 23 years, from which we’ve produced 17 years of outcomes. (Our approach requires five years of prior data to produce reliable results.) This system produced a reasonable amount of stocks to buy each year. The largest total was 44 stocks. And the smallest group was only 22 stocks.

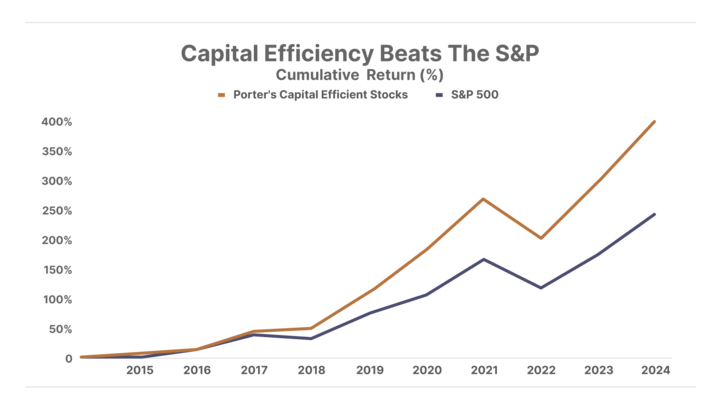

What you discover in these results shouldn’t surprise you: better businesses lead to better investment outcomes, especially over time. Over the last decade, this approach produced returns of almost 400% (17.4% annualized), outpacing the S&P 500’s 242% return by a wide margin. (Don’t forget, the last decade has been among the best ever for the S&P 500.)

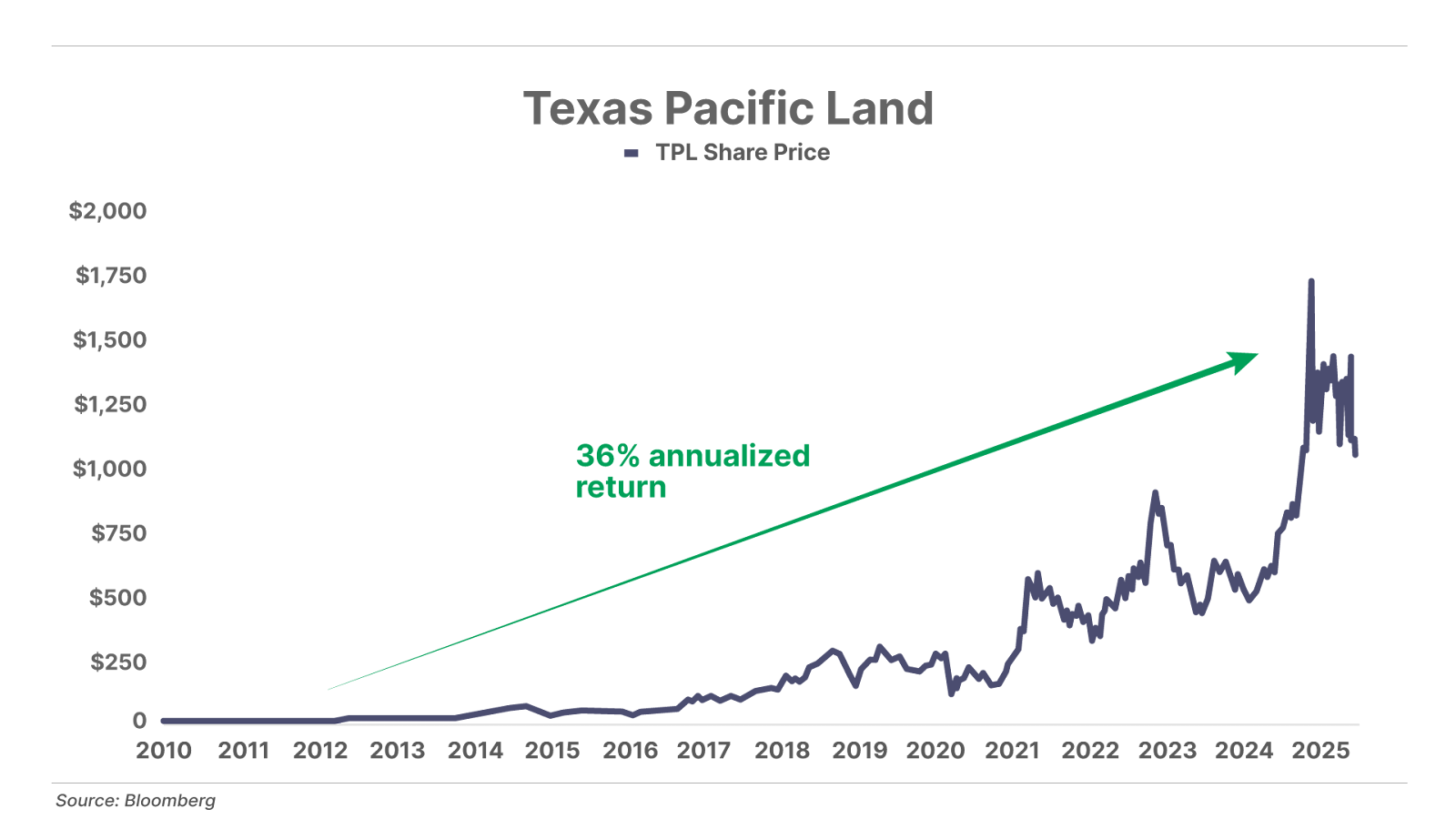

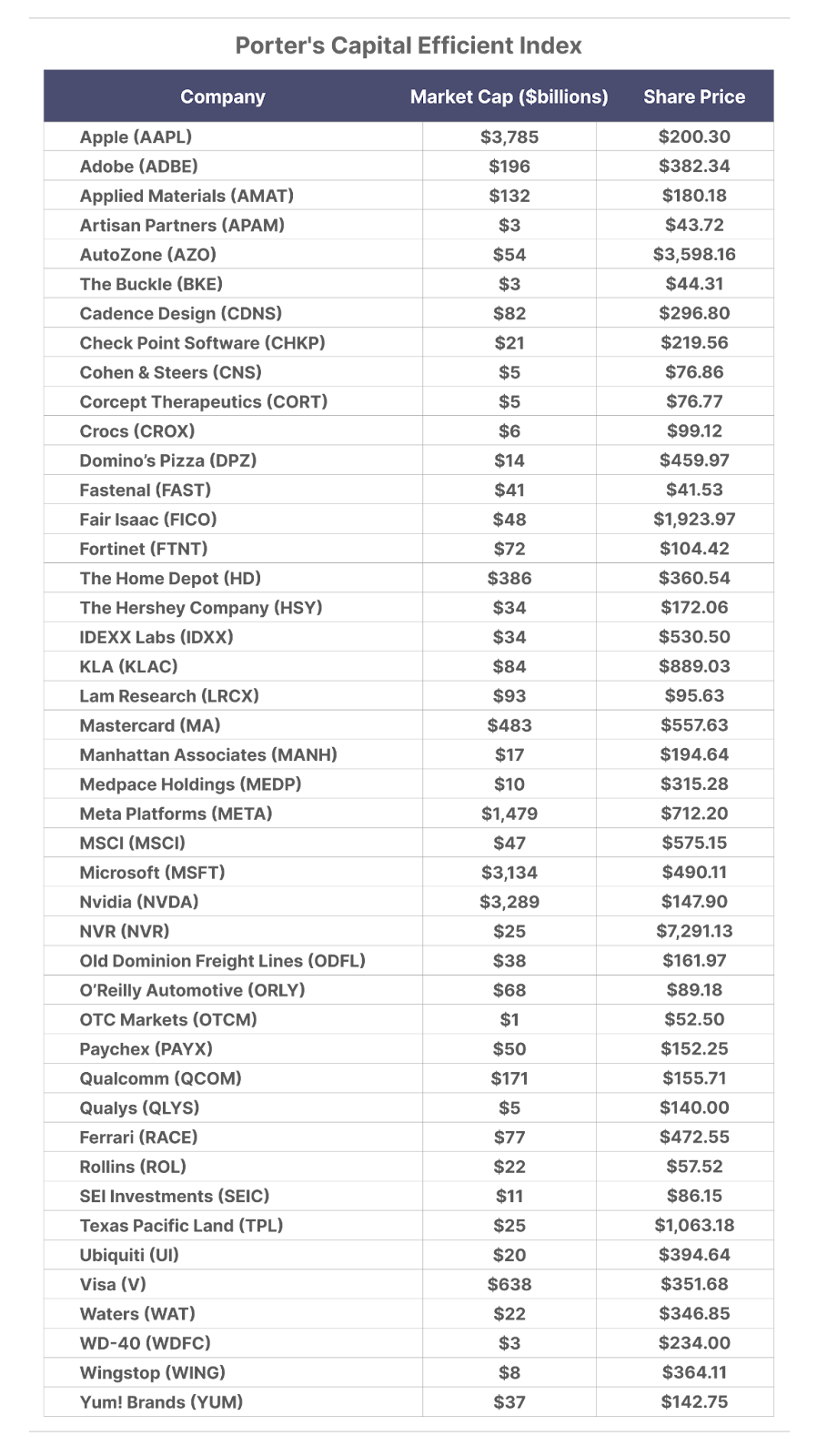

While I don’t subscribe to the idea that volatility equals actual risk, a highly volatile approach to investing will make following the strategy impossible for most people. As you can see, over the full period (17 years) not only did this approach far outpace the market’s results (1,128.5% versus 458.7%), it did so with less volatility (beta: 0.98, where the market is 1).I’ve included the list of the stocks from our most recent capital efficiency screen below. You’ll recognize many of the names. What was the highest scoring stock on our most recent screen? Texas Pacific Land (TPL), which has been one of my best recommendations ever, since I first recommended it in 2012.

If you want to achieve extraordinary investment results, the very best strategy is to own extraordinary businesses. Here’s a list of them:

P.S. You might wonder why we’d freely publish such a valuable approach to investing. Well, there’s a wrinkle to applying this screen into an actual portfolio to achieve these results. We’re not giving that part away.

The Man Who Beat Buffett By 18,034%

Garrett Goggin’s gold royalty picks outperformed Warren Buffett’s returns by a stunning 18,034%. If you invested just $250 into the top gold royalties, it would have turned into $727,641. Now, you can get details on Garrett’s top three Gold Royalty picks – for free.

Click here to access Garrett’s Gold Royalty Retirement Portfolio – before the next gold wave begins.

Three Things To Know Before We Go…

1. Tension at the Fed. On Monday, we reported on dissension at the Federal Reserve – with two Fed governors pushing for interest rate cuts to come sooner than the official Fed position of “wait and see,” led by Fed Chair Jerome Powell. Today, President Donald Trump said he has narrowed his choice for a new Fed chair to “three or four people” – without actually saying he would fire Powell, whose term ends in May 2026.

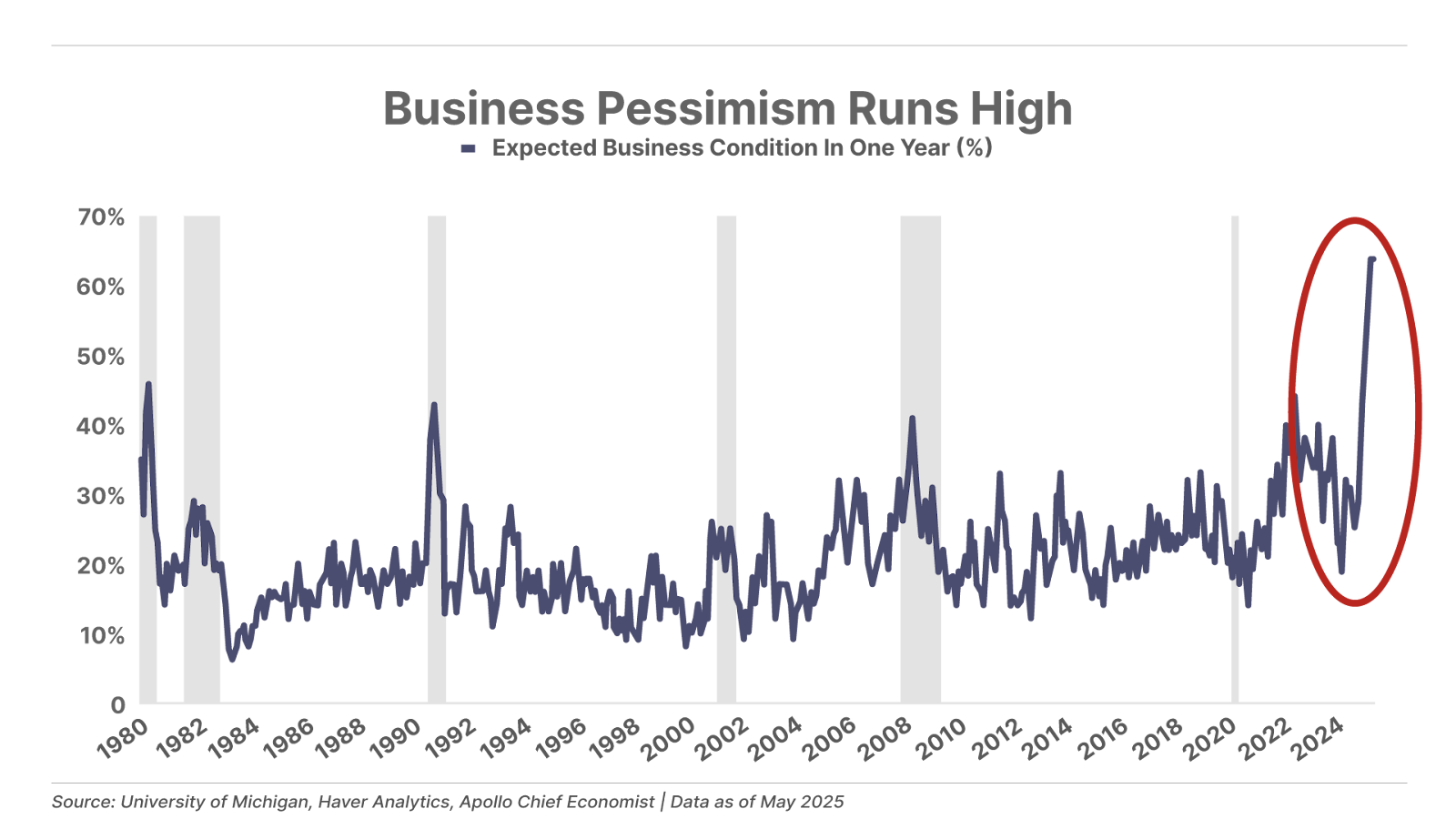

2. U.S. businesses have never been more pessimistic. Over 60% of respondents in the latest University of Michigan survey for May expect business conditions to worsen over the next year – the highest level of pessimism in the history of the data series going back to 1980. Levels above 40 have only occurred during recessions.

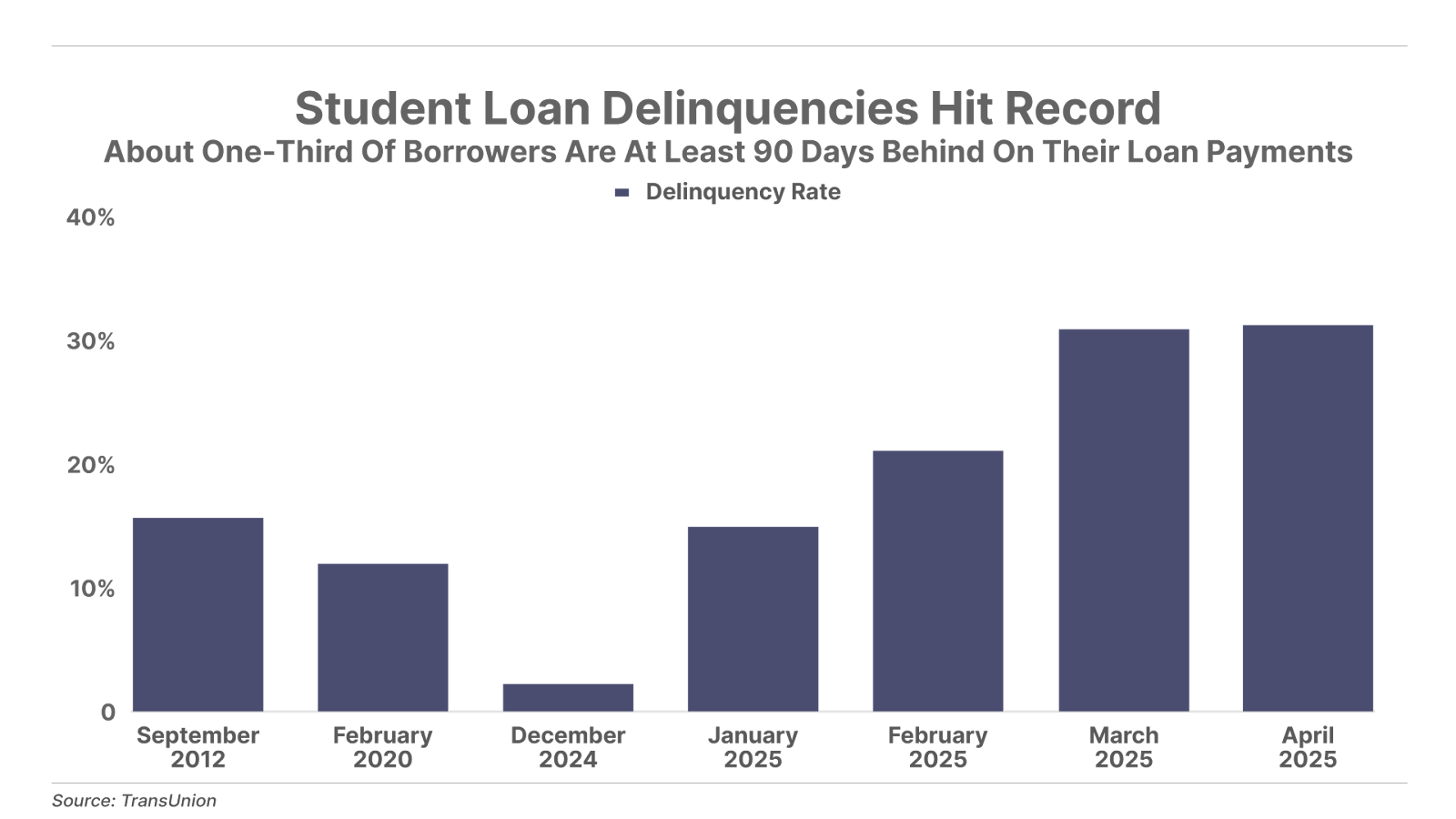

3. Student loan delinquencies surge. Nearly one-third of federal student loan borrowers – about 5.8 million people – are now more than 90 days delinquent, a sharp increase from the 12% delinquency rate seen before the pandemic. Since the Department of Education resumed collections on loans in May, a growing number of borrowers are falling behind, squeezed by worsening financial conditions – and it’s only getting worse. Borrowers more than 270 days past due will soon face wage garnishment, with up to 15% of their paychecks automatically seized.

And One More Thing… Poll Results

Last week, Porter reported on the growing presence of stablecoins as a reliable digital currency. Concluding a two-day series on the topic, on Wednesday, he wrote:

What’s been needed to unlock innovation in banking and payment services has been a digital currency that’s stable and backed by a legal and regulatory framework. Stablecoins have the cryptological features necessary to facilitate distributed financial applications, and now they will have the legal and regulatory framework under the U.S. government to be widely adopted. This will enable immediate and free transfers and payments across the internet.

And, over time, this will lead to a complete revolution in banking. As I explained on Monday: this is like Netflix (NFLX) coming for Blockbuster. All of the reasons physical banks needed to exist just disappeared.”

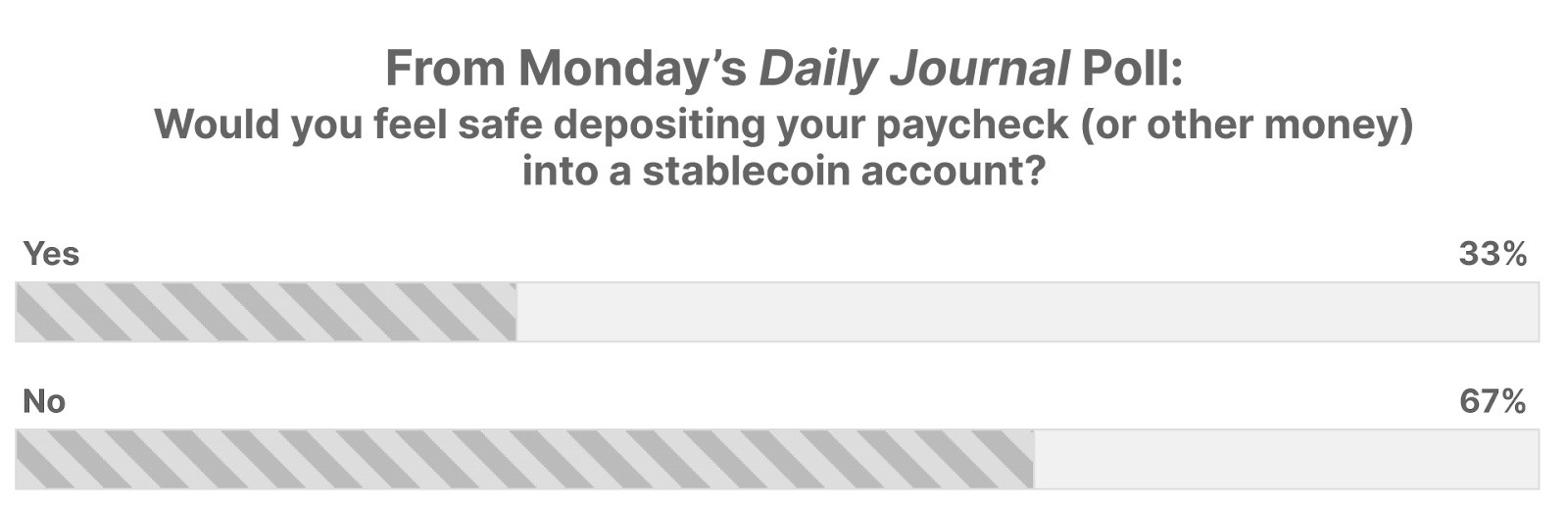

So, on Monday we asked readers “Would you feel safe depositing your paycheck (or other money) into a stablecoin account?”

Two-thirds (67%) of survey takers answered “no,” while the other third said “yes.”

Tell me what you think: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.