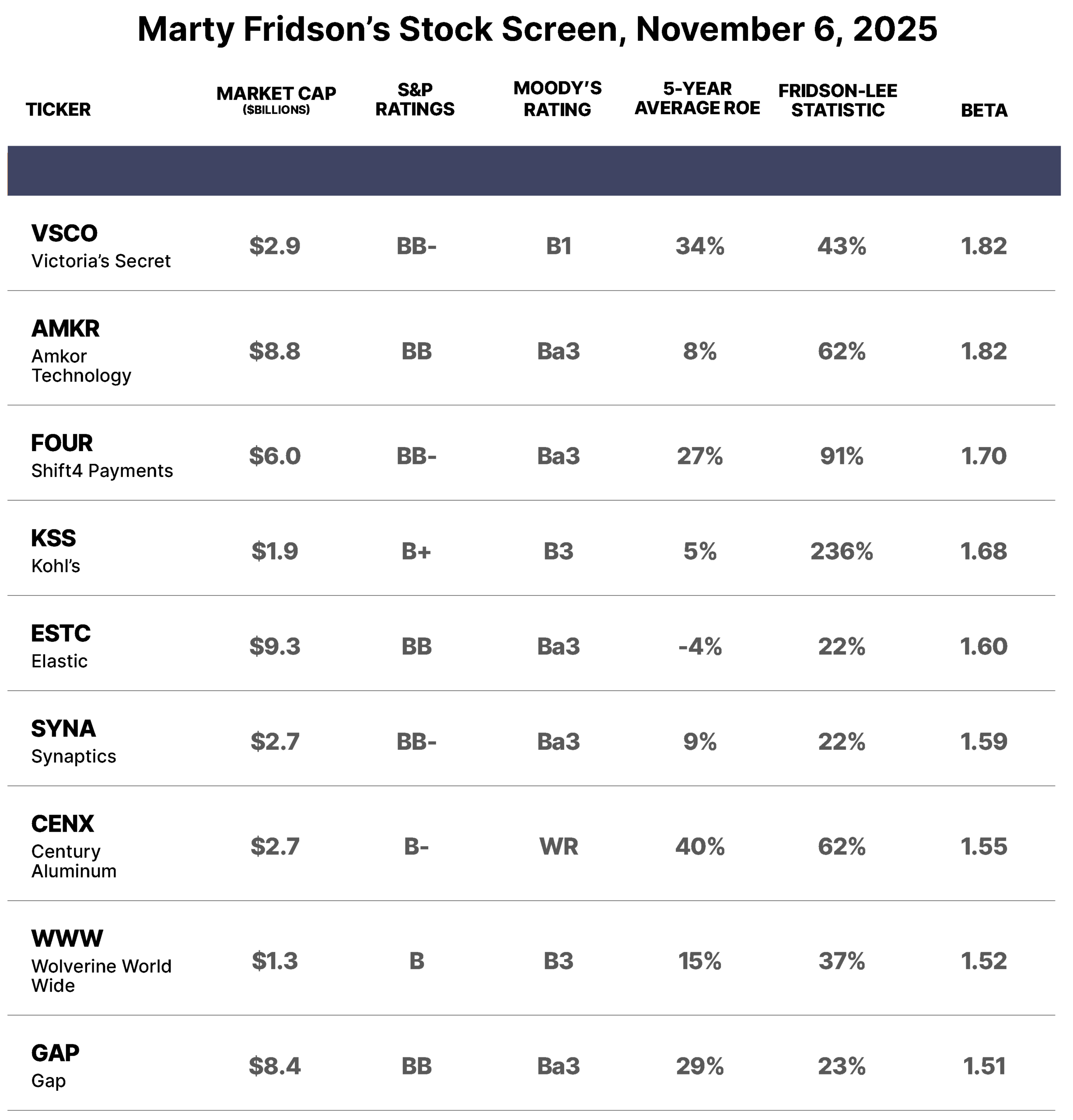

This screen is based on the characteristics Distressed Investing analyst Marty Fridson identified in The Little Book Of Picking Top Stocks, which he published in 2023, as the common features among the market’s best-performing stocks.

The applied screening criteria:

- Price volatility over the previous year of at least 1.5x that of the stock that ranked #250 that is the median of the S&P 500 by total return

- Market capitalization equivalent to 50% or less of the market capitalization of the stock that ranked #250 by total return in the previous year (some #1 stocks have been exceptions to this rule)

- Bond ratings of Baa3 or lower by Moody’s and BBB- or lower by Standard & Poor’s

- Fridson-Lee statistic of 18% or greater – meaning analysts’ estimates of the company’s earnings per share (“EPS”) vary widely

Click here to access previous Marty Fridson Stock Screens.