100 Years Of History Has Proven As Much

And How You Can Protect Your Portfolio

| This is Porter & Co.’s The Big Secret on Wall Street, which we publish every Thursday at 4 pm ET. Once a month, we provide to our paid-up subscribers a full report on a stock recommendation, and also a monthly extensive review of the current portfolio… At the end of this week’s issue, paid-up subscribers can find our Top 3 “Best Buys,” three newly added portfolio picks that are at an attractive buy price. You can go here to see the full portfolio of The Big Secret. Every week in The Big Secret, we provide analysis for non-paid subscribers. If you’re not yet a subscriber, to access the full paid issue, the portfolio, and all of our Big Secret insights and recommendations, please click here. |

A president threatening to set up a new revenue agency for the federal government isn’t good news. It’s horrifying.

In his inaugural address after being sworn in as president, Donald Trump announced that he wanted to create a new federal revenue agency, the External Revenue Service. It’s an idea that he has continued to develop and pursue during his first term.

The name shows he doesn’t know much about history: America already established an external revenue service.

President George Washington established The Revenue Cutter Service in 1790. And the first revenue sailing vessel built was The Massachusetts, commissioned in 1791.

Congress granted extraordinary powers to this branch of the government. Among other things, Revenue Cutters were entitled to search any vessel without probable cause.

Yes, that’s a clear violation of the Fourth Amendment – “protecting people from unreasonable searches and seizures.” But the Supreme Court has consistently upheld these privileges as necessary to the Revenue Cutters because of their role in generating revenue for the government.

Or, in other words, our civil rights – supposedly granted by God, our creator – don’t count when they interfere with the government’s right to confiscate our property.

Hmmm… Maybe those lofty words about “establishing a more perfect union,” etc., were just propaganda. In fact, Cutters’ extraordinary powers were most recently upheld in a 1983 Supreme Court case (United States v. Villamonte-Marquez).

But wait… the Revenue Cutters were abolished in 1915 – and the service became the U.S. Coast Guard, whose mission is (supposedly) to aid coastal navigation and mariners. Why would they need the right to ignore the Fourth Amendment?

Well, as the only agency legally entitled to search whatever it wants, whenever it wants, the government wasn’t about to let the Coast Guard go to waste! It became the government’s primary weapon in the “war on drugs.”

(By the way, I believe we should refer to “war on drugs” as The First Pointless And Unwinnable War Against Human Nature, which was followed by The Second Pointless And Equally Unwinnable War Against Climate Change.)

The Trump Trade Wars

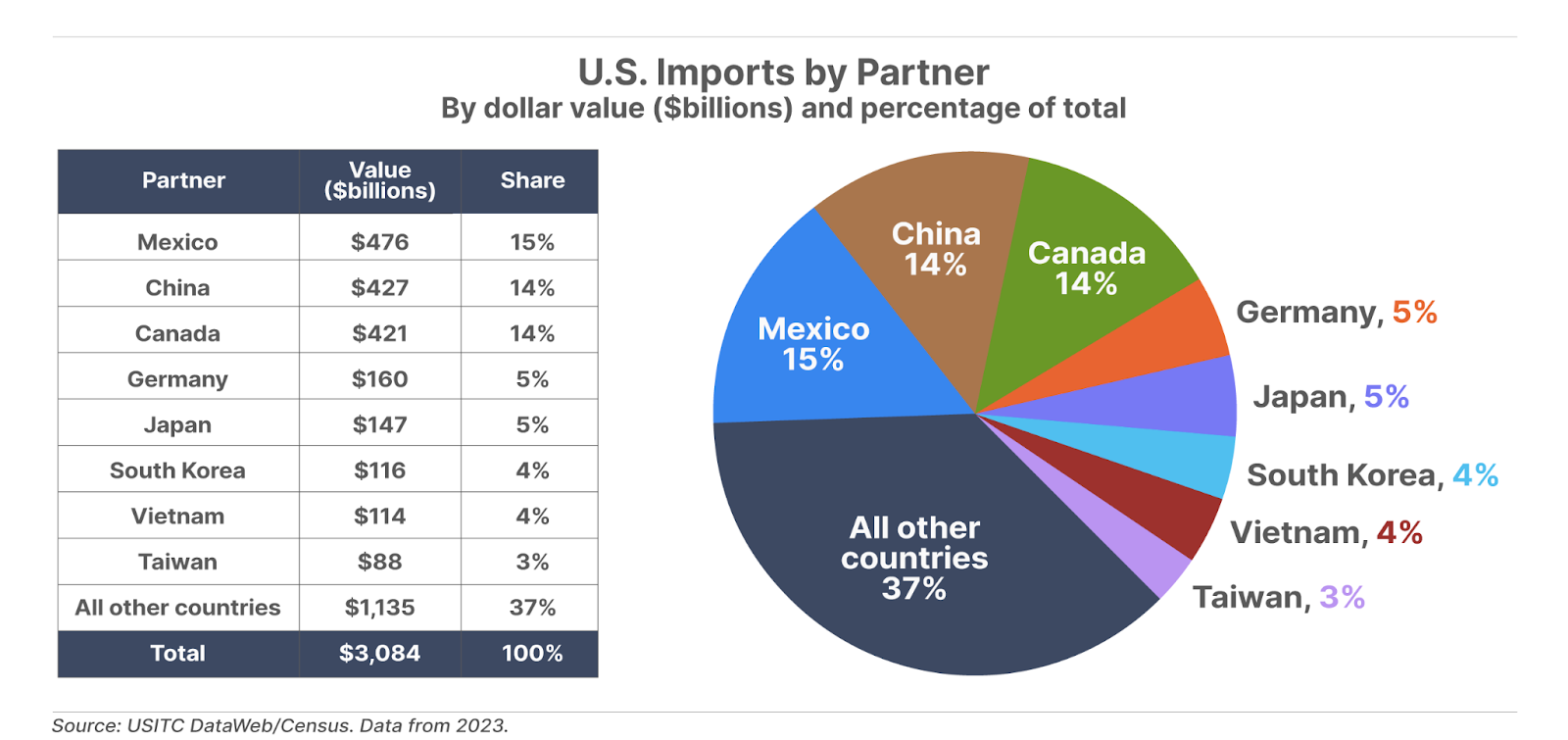

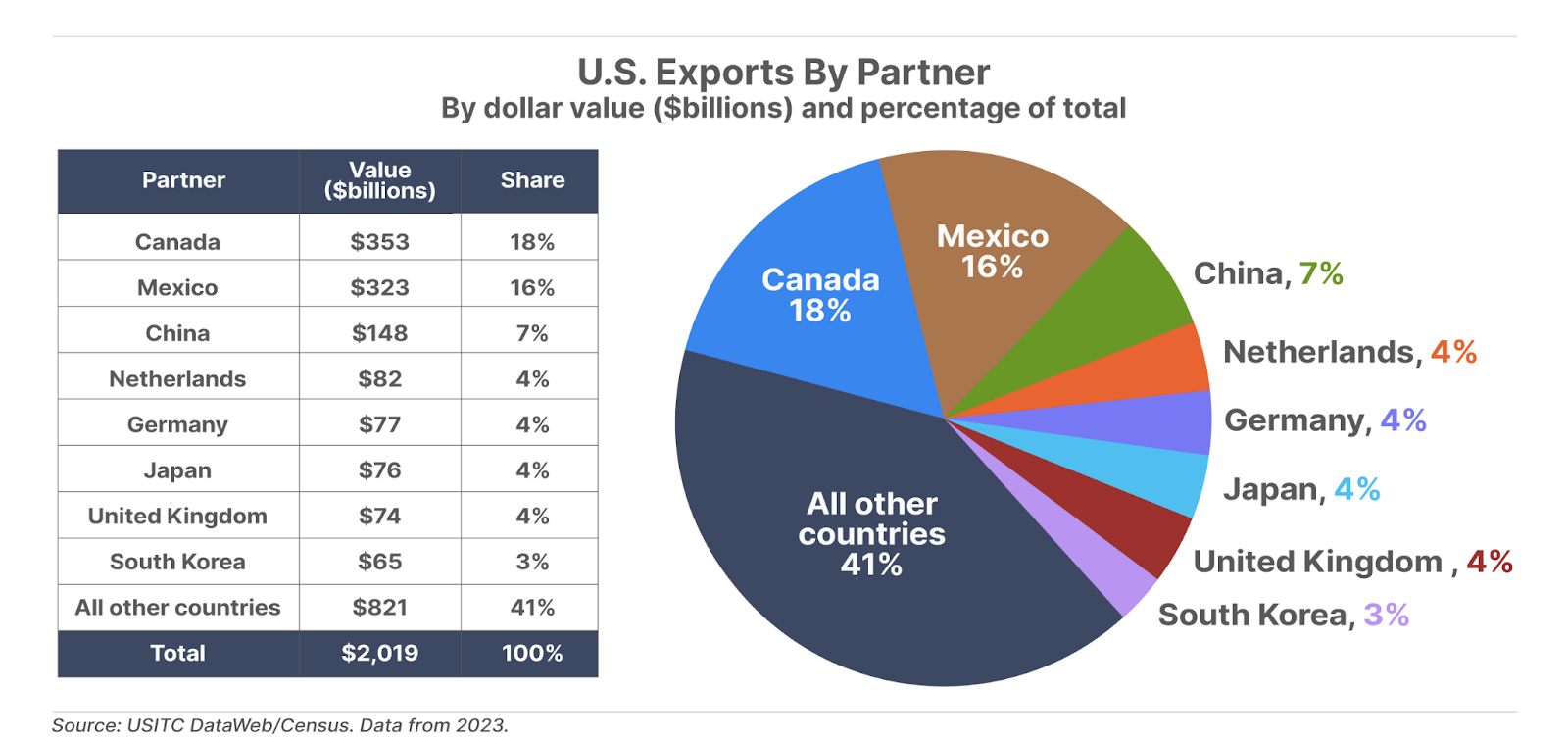

Now, it seems that Trump is going to use these incredible extra-Constitutional powers – once again – to collect revenue for the nation. In early February, Trump launched a trade war against America’s two closest allies, Canada and Mexico – until agreeing to delay the planned 25% tariffs on imports from both countries for a month after they submitted to some minor concessions. Soon thereafter, a 10% tariff on imports from China was implemented.

Ironically, this emerging trade war has Trump’s most ardent libertarian-leaning supporters excited. They believe Trump’s moronic claim that the External Revenue Service will enable America to fund the government by taxing foreigners, instead of taxing our own citizens.

First of all, if that’s his plan, then I’d suggest he at least shut down the Internal Revenue Service (the IRS) first. (Watch: that won’t happen.)

And, more importantly, most people who can read and think (and who choose to do so) realize there’s no practical way to tax businesses or our trading partners. These costs must be passed along to the ultimate consumers – us. If the cost of the additional tax renders the business (or the trade) unprofitable, then it will simply cease.

Wonderful, you may think. That will open opportunities for American businesses. America first! Well, be careful what you wish for. There are millions of things Americans, and the U.S. economy, either aren’t any good at (because of supply chains, labor rates, culture, climate, natural resources) or, even worse, have very low returns on capital (stuff we don’t want to be any good at).

These economic realities – known to economists as comparative advantage – explain why global trade is so important to increasing wealth and living standards all around the world.

There’s a reason nobody tries to grow bananas in Iceland. Doing so won’t make Iceland richer – it will make it poorer, as the energy and effort will be supremely inefficient and take capital and resources away from where they can be profitably employed.

(These aren’t new ideas… the theory of comparative advantage has been around since economist David Ricardo first introduced it in his 1817 work On The Principles Of Political Economy And Taxation. And while we still call it a “theory,” chances are that if a theory has been around for more than two centuries, it has a lot of claim to being “fact” at this point.)

So it is unbelievably naïve to believe that trade enriches one country at the expense of the other. Instead, both parties gain – or else the transactions would not occur. And today the links between various economies are extremely intricate and important to the function of all the major economies.

How Tariffs Work (And Why They Don’t Work)

I’m not alone in this view. The Wall Street Journal in late January called Trump’s proposed tariffs on Mexico and Canada “the dumbest trade war in history.”

To state plainly what most readers already know… a tariff is simply a tax on imported goods. When these taxes are imposed, they aren’t usually absorbed by the foreign manufacturer – but instead passed on, in whole or in part, to U.S. consumers through higher prices.

For example: If a toy manufactured in China used to cost, say, $15 at Walmart, and that toy (along with all other Chinese-made goods) is now subject to a 60% tariff, the $9 tax on the toy isn’t going to get eaten by the manufacturer – and certainly not by China. It’s going to be reflected in a new, higher price at Walmart – probably something close to $24.

A different kind of example… America is producing a lot of crude oil, and most of it is “light sweet” crude. But it so happens that our refineries – that make gasoline – were designed and built to process heavier crudes, much of which we import from Canada. So, if you think we’re going to enrich ourselves by impoverishing Canada with a 25% tariff, you’re a moron: all of those costs will be passed along to you, the consumer. Meanwhile, a wholesale tariff at that level will simply destroy the economics of all kinds of supply chains, making the U.S. economy vastly less efficient. That will make everyone – us and our trading partners – poorer.

Think about it this way. Why aren’t there tariffs between states? According to President Trump, Florida would be wealthier if it charged tariffs against the smaller economies in Georgia and Alabama. Those smaller states have been “living” off Florida buying cheap vacations from them for decades. It’s time they paid their fair share!

Does that make any sense? Of course not.

Neither does the completely nonsense idea that we can tax (or tariff) our way to prosperity.

What we should want is for Canada (and any other trading partner) to become wealthier by making us wealthier – by everyone doing what they are best at and keeping the goddamn government out of the way.

What people all around the world need is vastly less government, not borders we can’t cross and goods and labor we can’t exchange fairly.

Nevertheless, Trump is serious about tariffs. In fact, tariffs were a centerpiece of his economic policy throughout his campaign – and in his first term as president. And while (as of this writing) tariffs on Mexico and Canada are in a holding pattern, they’ll likely be back on the agenda shortly. And meanwhile, the UK and the European Union are anxiously anticipating when they, too, will be threatened with tariffs… and China is likely pondering when the 60% tariffs that Trump promised will be imposed.

While some commentators have suggested Trump is threatening these tariffs as a negotiating tactic and won’t actually implement them, his track record during Trump 1.0 suggests that, despite delaying tariffs on Mexico and Canada for the moment, he will make good on his promises. During his first term, Trump imposed 30% to 50% tariffs on imported solar panels and washing machines, 25% tariffs on steel, and 10% tariffs on aluminum. Collectively, first-term Trump tariffs covered about 4.1% of U.S. imports.

This time, the tariffs he has promised cover a much broader swath of America’s imports from its three largest trading partners.

Hello, Inflation… Goodbye, Common Sense

That inflation is the obvious and natural result of tariffs isn’t just common sense. It’s also borne out by historical economic data.

In 2019, economist David Furceri and his colleagues at the International Monetary Fund published the most comprehensive analysis ever on the impact of tariffs. Their study encompassed 151 countries and nearly 60 years of data, from 1962 forward. What did they find?

No prize for guessing: Tariffs cause a substantial increase in inflation… and the higher the tariffs, the bigger that increase.

No major academic economist has been more “right” about important things in recent years than Harvard University’s Larry Summers. Summers – a Democrat who served as Treasury Secretary under President Bill Clinton – loudly warned the Biden administration early in its term that its post-COVID economic policies would unleash massive inflation. At the time, these warnings made Summers a pariah within the Democratic Party. But he was proven right.

Summers not long ago gave an interview to News Items (on Substack) journalist John Ellis (a conservative who is a cousin of former President George W. Bush). The interview is well worth listening to in full. Here is the relevant excerpt on Trump’s proposed tariffs:

The more important part is he’s talked about a big tariff on every good that we import, which means higher import prices, also means higher prices for everything that competes with imports… that’s substantially inflationary.

Summers has shown that his economic predictions are accurate and not politically biased. He was witheringly critical of Biden’s economic policy. And just as he was right about Biden’s policies being inflationary, his call about the inflationary impact of Trump’s tariffs will likely turn out to be on the money as well.

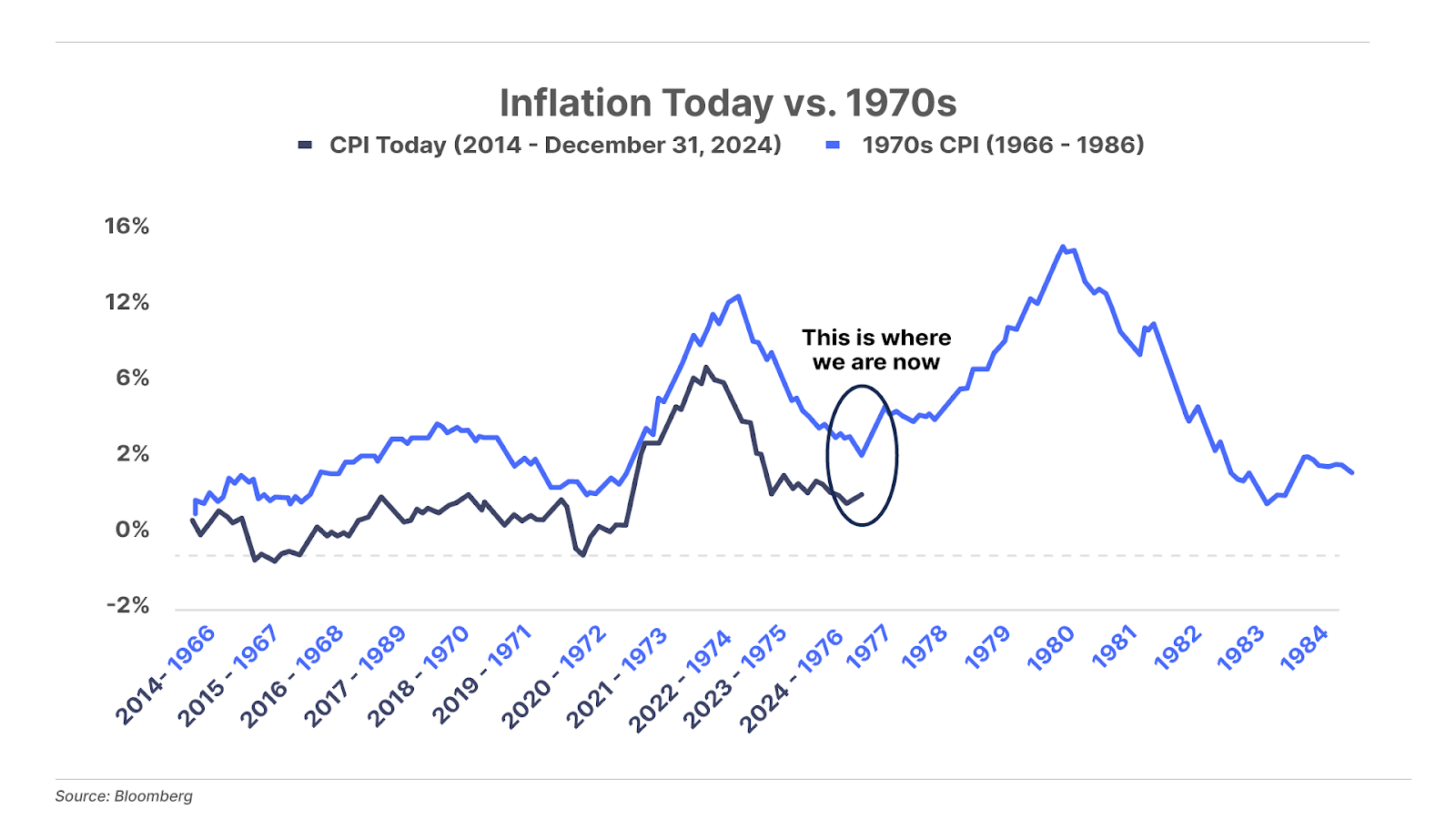

We’ve been writing for months about how inflation – contrary to what the headlines suggest – is nowhere close to being defeated. In many ways, inflation is closely tracking what unfolded in the disastrous 1970s (see the graph below). History is already looking like it will rhyme. And a Trump tariff-fueled boost to inflation will make a 1970s replay all the more likely.

How Bad Could It Be? History Has Thoughts

The all-time granddaddy of economic collapses can be directly traced to tariffs. The tariff that set in motion the economic forces that led directly to the Great Depression was not Smoot-Hawley, as your American history teacher probably taught you.

It wasn’t. A quick history lesson…

In 1921, following the end of the first World War, American farmers were reeling from a decline in agricultural exports. Up to that point, U.S. farmers had had their best years ever from 1914 through 1919. But a global pandemic, the end of the war, and the restart of Europe’s farms had, understandably, reduced demand for American agricultural products. Gross U.S. farm income fell from an all-time high of $18 billion in 1919 to about $10 billion by 1921.

A mild recession in 1921-1922 made things worse. But nothing was going to stop the U.S. economy from growing – thanks to the ongoing miracle of the auto industry. Sales of passenger cars in the U.S. grew from 181,000 in 1910 to over 4.5 million in 1929. And with all these cars came enormous numbers of new jobs building roads, making spare parts, and servicing the vehicles.

The U.S. advantage in manufacturing in the 1920s is hard to imagine today. The war had wrecked Europe’s manufacturing base, and it took a long time to recover. Germany, where the car was invented, made a total of just 18,000 cars in 1928. The U.S. made 4.3 million. Russia? Of course not. Communism isn’t great for making anything: Russia wasn’t producing even 1,000 cars a year by 1928.

The only thing our government needed to do in 1922 was simply get out of the way.

But what about the poor farmer? There were all kinds of things that the American farmer could have done (and would eventually have to do anyways) to improve productivity. In 1920, only 2% of farms had a truck and 4% had a tractor.

Instead of letting farmers figure out how to increase productivity and compete in the world’s markets, Republicans had a “better” idea: let’s make our agricultural trading partners pay our taxes!

Congress held hearings to determine (and this isn’t a joke) how to create a “scientific tariff” to equalize the production costs among countries for agricultural products. No country should be allowed to undercut prices charged by American companies, they said. Trust the science, they said – yes, they really did say that!

This led to the Fordney-McCumber Tariff of 1922, which put up to a 50% tariff on virtually every item imported into the United States. As President Trump would have said, “We’re going to make our trading partners pay their fair share.”

And so, 100 years ago, all of these same political promises that we’re hearing today were being made to the same uneducated, poor people (blue-collar workers and farmers), by the same group of people who are smart enough to know better (rich Republicans).

Simple question: how did the Fordney-McCumber Tariff work out for everyone?

Well, the first thing that happened was our trading partners (most notably Germany) all began to default on their war loans. By 1923, Germany was experiencing hyperinflation. Thus, Fordney-McCumber was one of the main causes of Nazism and World War II. For our closest allies (England and France), we began lending to them heavily to prevent their defaults. Thus, a global credit bubble began to build… and build… and build. And you know what happened next, don’t you?

But what about the poor farmers! Something had to be done. Well, something was done. They got what they deserved, as they always do, good and hard.

All of our trading partners raised their tariffs on our goods in retaliation – some to as high as 100%. American farmers, who had been net exporters, now had to fight against the weather and every other country’s taxing authority. According to the American Farm Bureau, U.S. farmers lost more than $300 million (about a 12% decline) annually in export revenue as a direct result of this tariff.

And they asked for it!

But even that wasn’t the worst outcome.

Global free trade is incredibly important to supply chains. If you haven’t yet, read “I, Pencil.” In explaining the complex division of labor that goes into making a simple pencil, this powerful 1950s story makes clear that interfering with the free market’s invisible hand stifles progress.

When governments begin imposing tariffs on leading industries and export goods, they end up impacting virtually every kind of production all around the world in ways that are impossible to predict, due to the enormous complexity of the world’s supply chains.

I said it above, but it’s worth repeating: the single most important concept in free-market economics is comparative advantage. The reason I’m better at financial research and economic history is because I’ve been doing it all day, every day, for 30 years. But this is all I am any good at.

For everything else, I’m going to need someone who has been doing what they do for 30 years. And it’s the free market – aka, trade – that enables me to focus on what I do, and allows them to focus on what they do.

Free trade allows intensive specialization of labor and capital. Every step in a supply chain has an industry somewhere that’s based on maximizing the production of just that one thing. Free trade enables everyone in the world to benefit from this extreme specialization.

But tariffs wreck the whole system in part because they simply increase prices, and also because they are applied capriciously, which creates tremendous uncertainty – which completely stops investment.

Soon It Was Tariffs Across The Board

By 1926, basic farming supplies (harnesses, plows, wagons, etc.) had all doubled in price. The Department of Labor found prices had increased substantially in all 32 major American cities.

And, of course, costs for consumers went up – for everything except farm products. So farming fell into an even deeper and worse depression.

How could it have been otherwise? Taxes are never good for any industry. And no, my dear Trumper, it doesn’t matter whether you call them tariffs or not. They add enormous costs, which drives down demand.

Just because the Fordney-McCumber Tariff didn’t work to protect farmers (or anyone else) didn’t seem to matter. Soon every industry in America began clamoring for even higher tariffs. And an entire new kind of political patronage was in play. Washington could now extort any industry it wanted.

In 1928, Republican presidential candidate (and eventual president) Herbert Hoover pledged to expand America’s tariffs and make them permanent. And that’s what led to the Smoot-Hawley Tariff Act of 1930 and the destruction of the entire global economy.

It was the dumb, leading the dumber, directly into oblivion. And cheering for it!

U.S. imports from Europe declined from a high of $1.3 billion to just $390 million by 1932. U.S. exports to Europe fell from $2.3 billion to $784 million by 1932. Overall, world trade declined by 66% between 1929 and 1934. And because the dollar was the reserve currency used to settle foreign trade, the collapse of the trading system led to bank failures – first in Europe and then, of course, in the rest of the world.

The U.S. economy has of course rebounded since then, but it took more than a decade and cost millions of jobs and billions in wealth. And new and lasting tariffs could drag us down once again.

How To Protect Yourself

America has an incredible economy. We have as big an advantage today in computing and technology as we had in manufacturing in the 1920s. There are all kinds of things our manufacturers and our farmers can do to drive productivity and beat the rest of the world, like automation and robotics.

What our government needs to do is simple: we must reform our entitlement system because it’s bankrupting us. We need to cut $2 trillion from spending and freeze the federal budget until the government is less than 15% of our economy (compared to 36% now). That’s the only solution that will lead to a higher standard of living and a thriving economy.

Trying to foist these costs on the rest of the world won’t work. It will put the entire global financial system at risk. And it will delay us making the important cuts to our government that must be made to ensure our continuing prosperity.

But… if Trump does go forward with these plans… there’s a simple road map to protecting yourself.

First, hedge against the collapse of the dollar by owning gold. As shown in the graph below, gold was one of the best ways to preserve value during the Fordney-McCumber era… and it probably will be again in coming years. Over the past half century, the price of gold has risen more than 7,500% in U.S. dollar terms.

Bitcoin is another good protective option (and it’s an asset Trump has actually been great for). Thanks in part to the pro-cryptocurrency attitude of the incoming Trump administration, Bitcoin is up 130% over the past year, and has regularly traded above the $100,000 level since Trump took office.

Created at the nexus of computation and energy, Bitcoin is unique among assets – a secure self-regulating decentralized network, governed by a series of rules that eliminates the need of any central authority. With supply capped at only 21 million coins (but divisible into virtually limitless fractions), Bitcoin could become a much better, new global reserve currency. It’s by definition immune from currency devaluation, and eliminates the silent theft of purchasing power through inflation that plagues sovereign currencies.

And finally, own bonds – because tariffs will destroy corporate earnings.

The basic premise of holding a bond is that you’re buying predetermined future cash flows that an entity is obligated to pay. Basically, you’re like the banker who holds a mortgage. Just as a homeowner has to repay the loan to the bank, a company that issues a bond must repay the bond holder (you) with principal and interest. If the company doesn’t pay, the bond holders can “foreclose” on the business, forcing it into bankruptcy where its assets are liquidated to repay the bond holders. It’s a lot like a homeowner who loses their home because they stopped making their mortgage payments to the bank. Tough on them!

Debt investors love bonds because the cash flows are predefined. When a company issues a bond, it is obliged to pay off the debt, in addition to making interest payments.

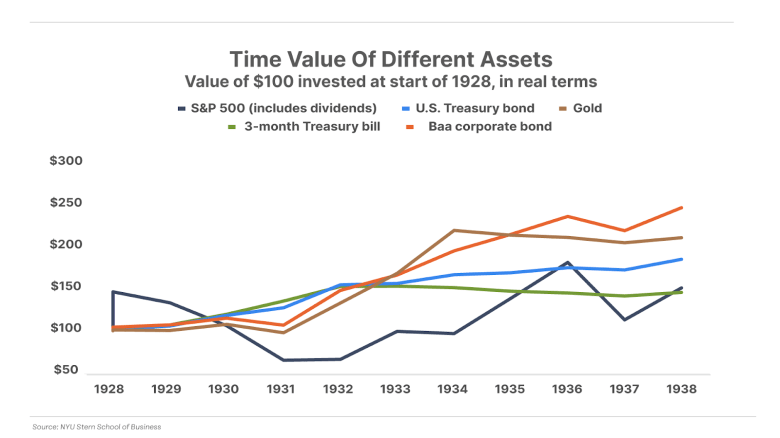

There are various types of bonds, such as Treasury bonds, which are issued by the U.S. government, and municipal bonds, which are issued by state and local governments. But we’re most interested in corporate bonds (as the chart above shows, they have held their value better than most other assets during the last 100 years). These are tradable promises to pay, backed by companies’ assets and earning power.

For the investor, bonds offer an opportunity to invest in corporations without exposure to the volatility of the stock market. And if things go terribly wrong and the company ends up in bankruptcy, bond holders, as creditors, are usually the first in line to be repaid.

A world of punitive tariffs will likely result in a wave of corporate distress – and while stockholders get pummelled, bondholders will benefit.

And nobody knows more about bonds – particularly distressed bonds – than Porter & Co. Distressed Investing senior analyst Marty Fridson. Marty has seen it all… from the legendary bond trading floor of Salomon Brothers, to the high-yield research teams at the who’s-who of Wall Street banks. Month after month in Distressed Investing, Marty and his team have shown that distressed bonds – the right distressed bonds – are a fantastic place to put your money. In fact, eight of the nine open bond positions have increased in value since being recommended, and overall, the Distressed Investing portfolio is up more than 25%. As the U.S. economy deteriorates, we’ll be entering a sweet spot for buyers of the debt of troubled companies.

If you’re not already a subscriber to Distressed Investing… see what we’re talking about here, or call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447, for more information on becoming a subscriber.

Porter & Co.

Stevenson, MD

This content is only available for paid members.

If you are interested in joining Porter & Co. either click the button below now or call our Customer Care team at 888-610-8895.