Issue #47, Volume #2

Trump’s Attack On Wall Street Will Trigger A Civil War

What Happened Last Time A President Threatened Wall Street

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| The dollar-based, global financial system has provided America with an “exorbitant privilege”… Global banks will not see the U.S. as a safe haven forever… The dollar could lose its standing as a reserve currency… Andrew Jackson followed this path 200 years ago… Kinsale’s earnings and a special dinner invitation… |

Half of our subscribers support U.S. President Donald Trump’s tariffs and trade war.

Why? Because Trump says his policies will end what’s been happening in the U.S. Over the last 50 years, untethered from any fundamental limit (as existed before 1971 under the gold standard), the U.S. government has created an unimaginable amount of debt – more than $30 trillion in new Treasury bonds!

And banks around the world, using these bonds as their reserves, have in turn created unfathomable amounts of new money.

This dollar-based, global financial system has provided America with an “exorbitant privilege” – we are the only country in the world that can print money to settle our debts, including debts to our foreign trading partners.

That privilege – exchanging pieces of paper for valuable commodities and goods – is like a ring of power: it inevitably corrupts. And it has led the nation to outsource virtually everything. As a result, it’s left the U.S. economy a shriveled Gollum that can no longer compete in most industries.

But that’s not the worst outcome.

The system is fundamentally powered by government debt. The more the U.S. government borrows, the larger the world’s banking system grows. The result is more money being created. This never-ending spiral of debt and inflation – boom, bust, and bailout – has enabled a tiny cadre of government-connected financial elites (Goldman Sachs, BlackRock, Apollo Global Management) to amass massive wealth and power, all funded by leverage that couldn’t exist without the government’s explicit support.

And so, while you’ve worked for the last 50 years to merely sustain your earnings power, the elites have used their virtually unlimited access to credit to profit massively from endless inflation.

Homeowners have done the same thing, on a smaller scale: buy an asset with a long-term, fixed interest rate loan that wouldn’t exist without the government’s explicit support. But, of course, the financial elites are borrowing enormous sums, thus reaping far larger returns.

But there’s a new sheriff in town. There’s an outsider in the White House. He was elected by the fury of the forgotten – factory workers, truckers, small-town entrepreneurs. With a torrent of X posts, he vows to crush the financial elite, targeting a shadowy institution that controls America’s money. And he’s targeting the “globalist cabal” that’s rigged the economy for Wall Street and foreign powers. His plan?

Destroy the dollar-based, global financial system by breaking the links to other countries through tariffs.

And if he succeeds?

By 2026, the fallout will be brutal. Unemployment will soar to 25%, wiping out 40 million jobs. Manufacturing and construction – Trump’s heartland strongholds – will be the hit hardest, losing 30% of their workforce. Small businesses, the backbone of Main Street, will collapse as credit dries up – more than 40% of them will fail. Savings accounts will vanish as 800+ banks collapse, leaving families with nothing. Home values will plummet 60%, leaving millions homeless.

And that’s not the worst of it.

No, the worst outcome is that the U.S. dollar will no longer be the world’s standard. Prices will soar. Basic goods – gas, groceries – could double in price… imagine $8-a-gallon gasoline or $12 for a loaf of bread.

This isn’t just market “volatility” – it’s a depression that will break the average American, all because of the zeal to “drain the swamp.”

How do I know?

For the first time in more than 50 years, this emerging crisis hasn’t led to higher bond prices and a stronger dollar – the world usually turns to the U.S. as a safe haven, but not this time. Instead, the dollar is crashing along with the U.S. bond market. Value is flowing into gold, Bitcoin, and safe foreign currencies, like the Swiss franc. Foreign central banks are dumping U.S. bonds and buying gold in record amounts. Some are even now buying Bitcoin instead of the dollar.

This is the outcome I’ve been warning against since I produced my 2010 documentary The End Of America.

And, this isn’t a forecast.

Everything I wrote above has already happened.

Not in Trump’s second term – but during Andrew Jackson’s 200 years ago.

President Jackson, just like Trump, believed the federal government had become corrupt, and he campaigned with a promise to “drain the swamp.” Like Elon Musk’s DOGE (Department Of Government Efficiency) today, Jackson initiated investigations into all executive departments and fired 10% of federal workers. Unhappy with the lack of reform, he demanded the resignation of his entire cabinet! Like Trump, Jackson supported tariffs too – and thought they could be used to reduce the government’s debt. His stand on tariffs eventually led the U.S. into a civil war, as South Carolina refused to allow tariffs to be collected and sought to “nullify” the laws. In the chaos that followed, Jackson would have been assassinated except the killers’ guns jammed.

Jackson’s primary target was America’s central bank, the Second Bank of the United States. To Jackson’s base – small farmers, laborers, shopkeepers – the bank was a parasite, siphoning wealth from the heartland. So in 1832, Jackson vetoed a bill that would have renewed the bank’s charter, setting in motion its collapse. After winning re-election, he went even further. He ordered federal deposits withdrawn, starving the bank of its assets.

And the outcome? It should serve as a warning to us all. Wiped out by Jackson’s order to distribute its assets to state-regulated banks controlled by his political backers, the Second Bank of the United States was forced to call in its loans, igniting a massive financial crisis that by 1837 had virtually destroyed the entire economy.

The Panic of 1837 saw 800 banks fail in two years. Unemployment hit 25% in industrial cities, with manufacturing and construction shedding 30% of jobs. Small businesses collapsed at a 40% rate in urban areas. Home and land values dropped 60% in certain areas of the country. Exports plummeted 50%, hammering farmers. Inflation surged – basic goods like flour doubled, equivalent to $12 for a loaf of bread or $8-per-gallon gas today. Savings evaporated. The depression, which lasted into the 1840s, crushed the working class that Jackson swore to protect, yet his populist legacy endured, reshaping American politics.

Today, Trump’s supporters – factory workers, rural voters, small business owners – see the Federal Reserve in the same light: as a globalist tool, prioritizing Wall Street over Main Street. Trump’s posts on X amplify this message, with hashtags like #FirePowell – referring to Fed Chair Jerome Powell – trending among supporters. His foes – Powell, corporate media, and G7 allies – sound like Jackson’s critics, decrying his threats as destructive. Both Trump and Jackson turned financial battles into cultural wars, rallying heartland voters against a coastal elite, even as their rhetoric deepened national rifts.

But the stakes are much larger today. If Trump succeeds in wrecking the global financial system, the resulting depression will be worldwide. And it will last well into the 2030s.

I support Trump’s efforts to reform our economy. I recognize that the current path is unsustainable and will lead, inevitably, to a crisis. I’ve known that – and been writing about it – for 15 years. But the reform we need – less government spending, less regulation – should result in strengthening the U.S. dollar and the bond market. That isn’t happening. And that should worry every American. Meanwhile, attacking our trading partners (who are also our biggest creditors) is a suicide mission. And our economy and your savings are in danger of being destroyed.

It has happened before.

And, if Trump persists, it will happen again.

Three Things To Know Before We Go…

1. Consumer companies are warning about tariffs. President Trump’s tariffs have yet to kick in, but they’re fully affecting consumer behavior. Several notable companies – Procter & Gamble (PG), PepsiCo (PEP), and Chipotle (CMG) – have cited growing consumer weakness as the reason for slashing full-year sales and earnings forecasts in their recent quarterly report. As P&G CFO Andre Schulten noted, “It’s not illogical to see the consumer adopt the ‘wait and see’ attitude, and we saw traffic down at retailers.” There are signs of potential de-escalation in the trade war between China and the U.S, but barring a significant reduction in tariff rates soon, the damage may already be done.

2. Credit card companies turn to recession playbooks. Though the full effects of Trump’s tariff policies have yet to show up in hard economic data, lenders are already preparing for a downturn. JP Morgan Chase (JPM) and Citigroup (C) are raising cash to brace for rising delinquencies, with JP Morgan’s CFO noting the “unusually uncertain” environment during a recent analyst call. Subprime lender Synchrony Financial (SYF) is tightening lending standards, signaling concern over consumer credit quality. Meanwhile, like the other lenders, U.S. Bancorp is battening down the hatches: pivoting its focus toward more affluent customers – those better positioned to weather a downturn.

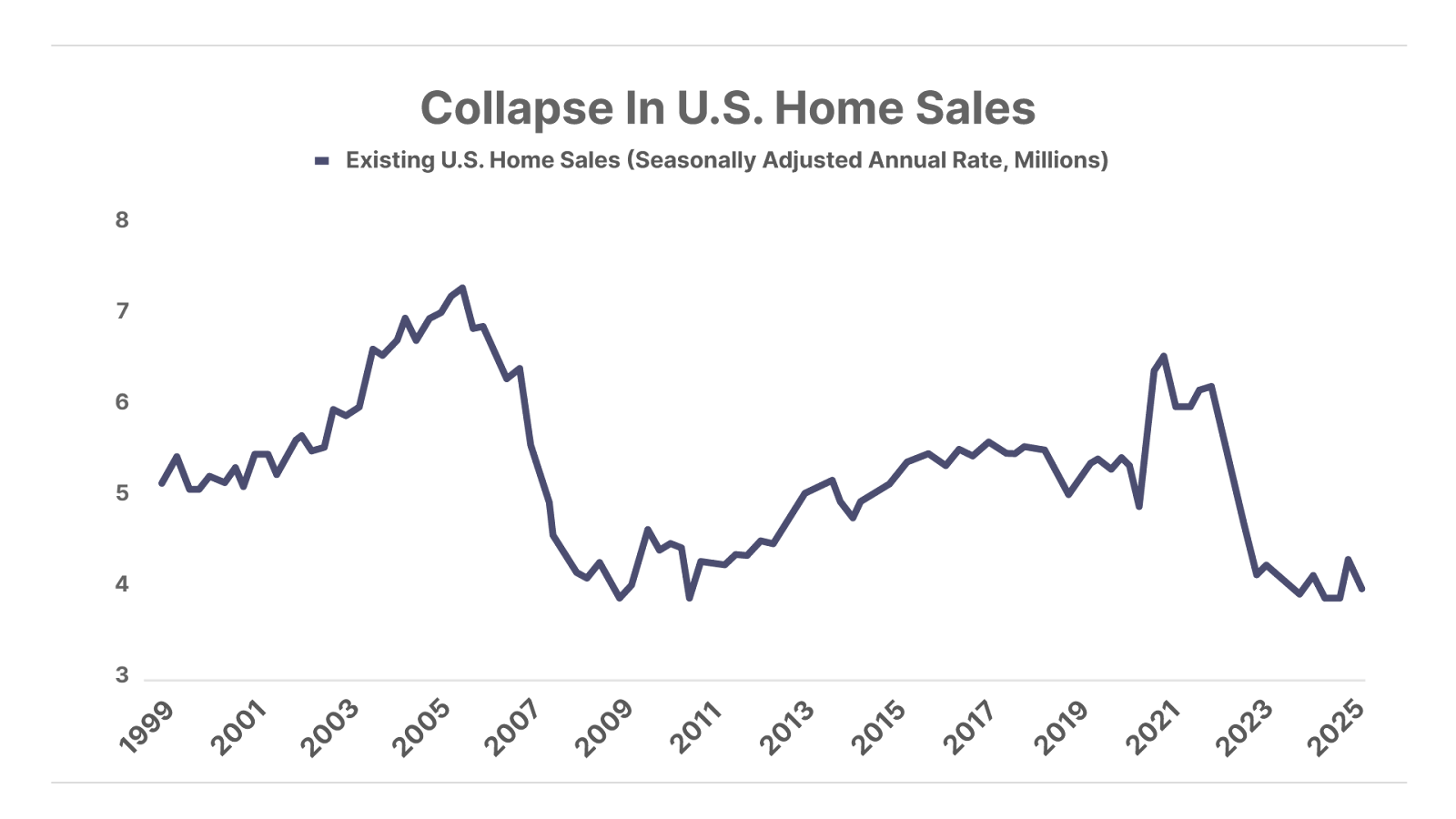

3. Rising rates crush the housing market. The number of sales of existing U.S. homes fell to a seasonally adjusted annual rate of 4.02 million in March, the lowest level since 2009. Affordability remains the key culprit, with the recent jump in borrowing costs pushing the 30-year mortgage rate to over 7%. Now, unsold homes are piling up, with the inventory of those for sale rising 20% from last year to 1.33 million units. America’s housing market remains frozen.

And One More Thing… Kinsale’s Earnings Cause Shares To Drop

In Wednesday’s Daily Journal, we wrote about Kinsale Capital (KNSL) ahead of the company’s earnings call today. We referred to Kinsale as “the very best property-and-casualty insurance business in the country.” But we warned that despite its industry-leading expense ratio, combined ratio, and technological advantage over its competitors, it tends to sell off after earnings news. And right on cue, shares of Kinsale dropped as much as 18% (as of 2 pm ET today), setting up a phenomenal buying opportunity.

The first-quarter results were solid from a profitability and underwriting perspective, but growth slowed as competition caused a pullback in new policy premiums. The company posted a combined ratio of 82.1% (expenses and claims incurred per dollar of premiums collected) – best in class, and well below the 86.9% consensus analyst expectations. Revenue growth slowed to 14%, but earnings per share of $3.71 beat estimates by 14% ($3.26 consensus).

The main source of weakness came from an 18% year-over-year (“YOY”) decline in premiums written in the commercial property division, the company’s largest underwriting segment. Management noted rising competition has led to lower policy premiums, which will likely result in slower growth this year. But this is part of Kinsale’s strategy: as one of the best-run and lowest-cost insurers in the business, management is intentionally pulling back as the market softens. For some context, Kinsale has increased the policy premiums in this division by 20x over the last five years. And excluding this division, Kinsale increased its policy premiums from its other segments by 16.7% YOY.

Another earnings drag came from Kinsale’s catastrophe losses, which rose to $18 million in Q1, up from just $500,000 a year ago. This was largely due to the one-time impact of the recent California wildfires. Despite these challenges, Kinsale’s cost advantage and underwriting strength still delivered a best-in-class combined ratio.

Of course, traders love to dump shares on seemingly bad earnings, but for long-term investors, this is exactly the kind of price correction you want.

If you’re thinking about owning Kinsale for the next 10 years, you’ll want to be at our special Porter & Co. cocktail reception and dinner presentation on May 21, in Richmond, Virginia, where I’ll teach you everything I know about property-and-casualty investing.

Good investing,

Porter Stansberry

Stevenson, MD

P.S. Will Trump match FDR’s unprecedented four terms?

Not since Franklin Delano Roosevelt has a U.S. president served more than two terms. The conventional wisdom says it would require a Constitutional amendment for this to happen again. But former presidential advisor Jim Rickards, who has spent 50 years in Washington advising the CIA, Treasury, and four U.S. presidents, believes the impossible is becoming probable.

“The groundwork is being laid for a third Trump presidency,” says Rickards.

Thanks in large part to a move… which could make him one of the most popular presidents in history.

“Thanks to a wildly controversial decision by Trump’s Supreme Court,” says Rickards, “we’re witnessing a moment eerily similar to what FDR accomplished in the 1930s.”

It traces back to a recent Washington development involving a $150 trillion national asset that could soon be released to the public.

When it happens, it could make “Trump 2028” a reality and enrich a whole new generation of Americans.

For the incredible back story, click here.

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.