Editor’s Note: Last week in The Spotlight, we introduced you to Tom Dyson. Today, we’re thrilled to bring you more exclusive research from Tom and his team at Bonner Private Research.

I (Porter) have known Tom Dyson for more than 20 years. He’s a fantastic analyst with a unique view of the financial markets that I believe every investor needs to be made aware of.

Unfortunately, most folks have never heard of him because – unlike us brash Americans – Tom doesn’t “market” himself, tout his track record (which is truly exceptional), or shout his ideas from the rooftops.

Instead, Tom simply lets his work speak for itself. But with these Spotlights, I’m going to do what Tom never would: pound the table about how outrageously good he is…

Tom Dyson is likely the greatest investor you’ve never heard of!

And in today’s Spotlight, we pick up from his issue last week with Tom answering his subscribers’ questions about his latest recommendation and giving you another new recommendation.

He also explores what he’s seeing in the markets right now and how to position yourself for the coming cascade of crises that are going to decimate many unsuspecting folks.

Enjoy.

(Note: all prices and data were correct at the date of Tom’s original publication.)

The S&P 500 has fallen since its top on July 16.

Despite all the headlines, it’s not a big deal yet. Just a routine correction for now.

With so much leverage in the system, many overcrowded trades and extreme valuations, all it takes is one negative headline or one trader to panic and everyone runs for the exit at the same time.

The ‘experts’ are all focused on the yen carry trade right now.

But really, the yen carry trade is just another example of a super-leveraged bet that’s overcrowded.

The real cause of the volatility is the gigantic and unstable debt bubble they inflated… and the exaggerated market tantrums we now get are just symptoms of liquidity drying up or risk appetite reversing.

Our core proposal is simple. The debt is now so huge, they must either keep inflating, or the economy will chaotically collapse. ‘Inflate or die’ is our model. We’re getting a little taste of ‘die’ this week.

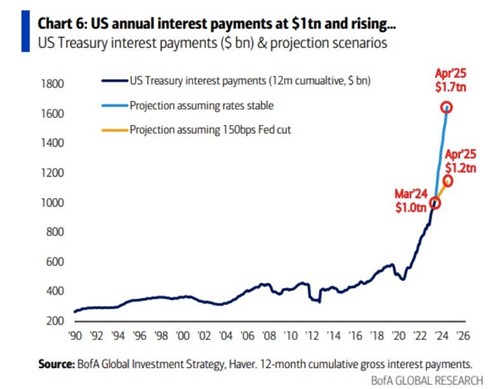

Look at this chart:

The US government is entering a debtors’ spiral. That is, the more interest it pays, the more credibility it loses with potential lenders, which results in even higher interest rates and even greater interest payments.

It’s a doom loop that ends in default.

The complacency is amazing. My sense is, most people understand that the government is broke, that there’s a reckoning coming. But they think “the Fed will bail us out, so might as well keep playing.”

I’ve always thought the biggest threat to the debt bubble would be a mood swing in the market. Not just a tantrum… but full-blown despair. Hardly anyone talks about market psychology, but to function, the system requires positive sentiment… faith that the stock market always rises, the economy is growing and there’ll be access to easy credit.

If that faith ever gets shaken, and the market starts cascading, it’ll quickly spread to businesses and consumers, and a doom loop of liquidation, layoffs, margin calls, falling stock prices, less consumption, less investment and lower profits will form.

And of course all this mauls the government’s tax base, causing the deficit to blow out.

In other words, risk is contagious. It spreads really quickly. And once contagion starts, it is very hard to reverse… or even slow.

So while I’m not reading too much into an 8% decline in the S&P 500 yet, it could quickly become something much bigger given the dynamics.

It’s like a hot ember landed in the box of fireworks. Usually nothing…but occasionally spectacular.

Our long term plan also remains the same… to preserve the purchasing power of our savings through what I expect will be a long and difficult bear market.

To do this, we’re using a three-way hedged portfolio consisting of 40% cash, 35% physical precious metals and 25% value stocks.

The cash and gold hedge us against falling prices. The metals and value stocks hedge us against inflation. And the cash and value stocks generate income, to keep our savings growing.

****

We’ve been tracking The Sounion, the fully loaded Suezmax tanker that’s on fire and adrift in the Red Sea. It’s been burning for four weeks now. Good news. They’re currently towing it to safety.

Here she is, surrounded by tugs and warships…

Source: EUNAVFOR (Euro Navy)

COMMENT: When I was growing up my mother used to always say “so goes GM, so goes the country.” And in those days it was very true since the auto industry was the biggest consumer of textiles and steel.

Today, maybe not. But I work for an auto supplier, every brand out there, tier 2, and all of our customers are slowing and where we used to get 6-9 months of firm orders, we now are begging for next month’s orders.

It hasn’t dropped off a cliff, but when people don’t commit 3-6 months out when they used to be twice that, something is afoot. I think the RV index is ahead of the rest and we will see a long cold winter.

MY RESPONSE: Thank you for your message. Chinese car companies are turning the global auto industry upside down. It’s fascinating to watch. I wonder if your observation has anything to do with this?

Earlier this week, I read about a new car from BYD – which stands for Build Your Dreams – that can go 2,100 kms on a full tank of gas and a fully charged battery. This means you could, in theory, drive this car across the USA and only have to stop for gas/charge once.

The car retails for $14,000.

It appears China’s new cars are so competitive, I can’t see how Western automakers like Volkswagen, Ford, Stellantis, GM, Volvo etc are going to survive. Maybe protective tariffs will buy them some time?

In light of this, your mother’s observation about GM seems rather bleak for America, and the other US automakers.

***

Each day, I spend many hours reading newspapers, company reports, press releases, interviews, opinions and investment ideas. I feel like I’m hunting for diamonds by sifting through sand.

The north star of our strategy is that the real (inflation-adjusted) value of US government debt must crash. The US Treasury is broke. The borrowing and spending is totally out of control.

Now foreigners are becoming increasingly reluctant to keep lending dollars. This is functionally the same thing as forecasting a run on the US dollar or a deflation of the unbacked paper currency system.

At our research service, Bonner Private Research, I’ve started tracking the price of the 30-year zero-coupon Treasury bond in terms of gold. This is the purest expression of the real value of the US government’s debt and the perfect way to track this insight.

If I’m right, the price of these bonds will decline against gold over time. It’s like the Dow/Gold ratio, except for the government debt. Let’s call it the Bond/Gold ratio.

Of course, normal people don’t use bonds as currency. We use them to preserve the value of our savings. But governments and big financial institutions use bonds as currency.

The financial system is built on the foundation of Treasury bonds.

The Treasury issued a new 30-year bond on May 15. The zero-coupon or “stripped” version of this bond currently trades at $300 (par is $1,000, redeemable on May 15, 2054). Gold is $2,500 an ounce.

Ten of these zero coupon bonds buy 1.2 ounces of gold at current prices. Let’s see how many ounces of gold these zero-coupon bonds are worth in thirty years.

If we’re wrong about the crash in the real value of Treasury bonds and the dollar’s purchasing power increases, our ten zero coupon bonds will buy more than 1.2 ounces of gold in 2054.

This core position entirely informs our long term strategy. We base our strategy on gold, silver, platinum, energy, shipping, resources plus the occasional opportunistic trade.

***

For the last two years, we’ve maintained a high cash balance.

We saw the Feds raising interest rates and acting tough on inflation. We wanted insurance against any crisis this might cause. It turns out, there wasn’t a big crisis, the official inflation figures — although still above the Fed’s long-term target — have receded enough for the Fed to cut interest rates in response to other forces in the economy (unemployment, for example).

They’re dropping the tough guy act.

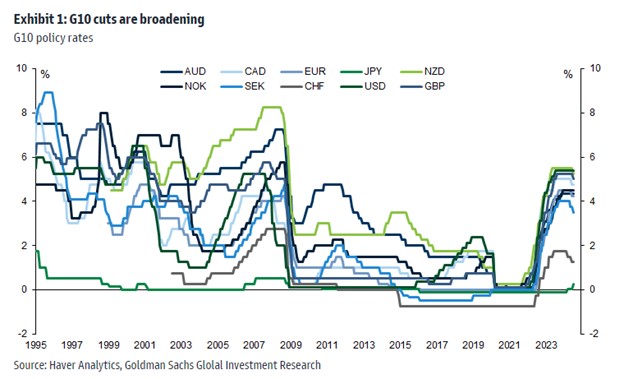

As this chart shows, the trend in short term interest rates across nine major currencies is definitely down. Japan is the one exception. The US will likely be cutting interest rates soon.

We’re also pivoting. I’m now anticipating a new period of weak dollar, in terms of other currencies. Two weeks ago, we reduced our cash balance by 5% and increased our precious metals balance by 5%.

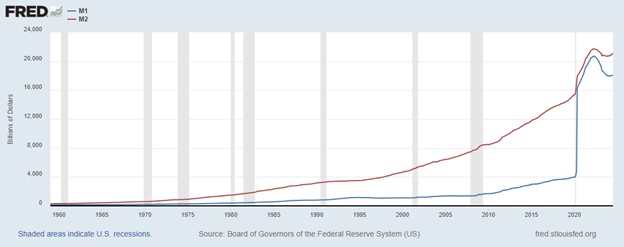

This chart shows the money supply. After two years of contracting money supply, they’ve finally taken off the governor and it appears the money supply is starting to rise again.

I could be wrong about the weak dollar trend in terms of foreign currencies. But it’s still prudent to diversify some of our cash into non-dollar and non-euro currencies at this juncture.

Today, I want to introduce a new weak dollar ETF.

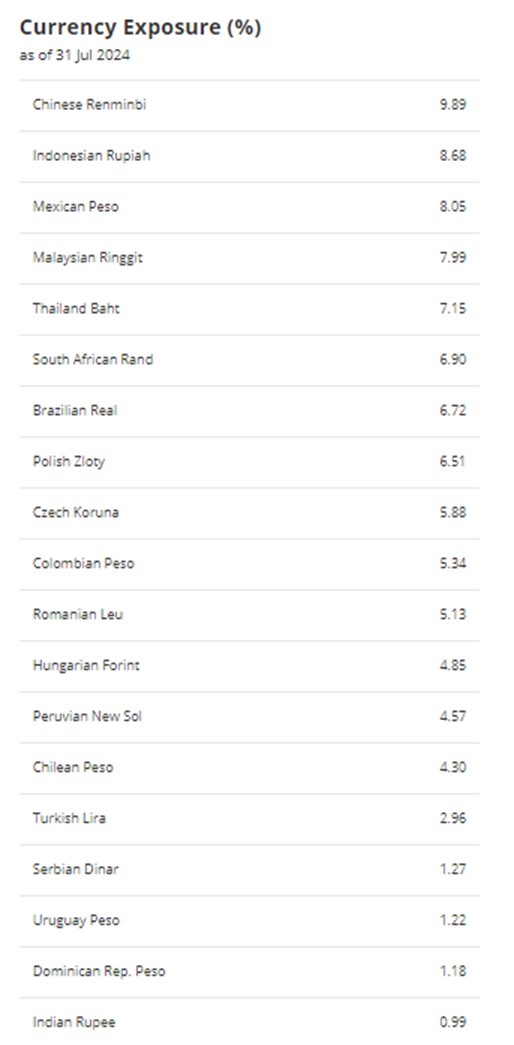

We can use this ETF to protect ourselves from a falling dollar trend. It holds the currencies of Brazil, Mexico, South Africa, China, Indonesia, Thailand, Colombia etc.

It pays a 6.3% annual dividend and it’s very cost efficient. The annual expense ratio is only 0.3%.

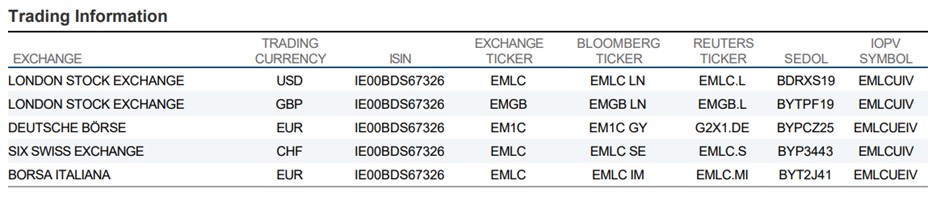

Let’s start using the Van Eck Emerging Market Local Currency Bond ETF [EMLC].

Because these are just short term bonds denominated in foreign currency, I’m giving EMLC a risk-rating of 1.5 on our 0-5 risk-rating scale (0 is safe and 5 is risky.) We won’t use a stop loss here.

Please note, we’ll put EMLC to work in our “35% cash” allocation, not our “25% stock” allocation. How much of our “35% cash” allocation should go into EMLC? I’m aiming to slowly build up to 50% our cash savings, that we currently hold in Treasury bills, into EMLC.

EMLC is safer and more diversified than dollars. It also pays a higher yield than T-bills (6.3% vs 5%.)

This ETF should be easy for anyone to buy. It trades on both US and European stock markets, with the following symbols…

EMLC holds dozens of local currency government bond issues from emerging markets. The average duration of these bonds is about five years, which means EMLC won’t be especially sensitive to changes in interest rates.

The “local currency” label is very important here. Many emerging market bonds are issued in dollars or euros.

In the bond world, they call these “hard money” bonds. And many emerging market bond ETFs contain both hard money and local currency bonds. We don’t want hard money bonds. We want local currencies only, to get us out of the dollar.

Here’s the currency composition:

This is just another form of insurance. By holding EMLC, we’re diversifying our cash holdings from the dollar into a basket of many currencies from around the globe.

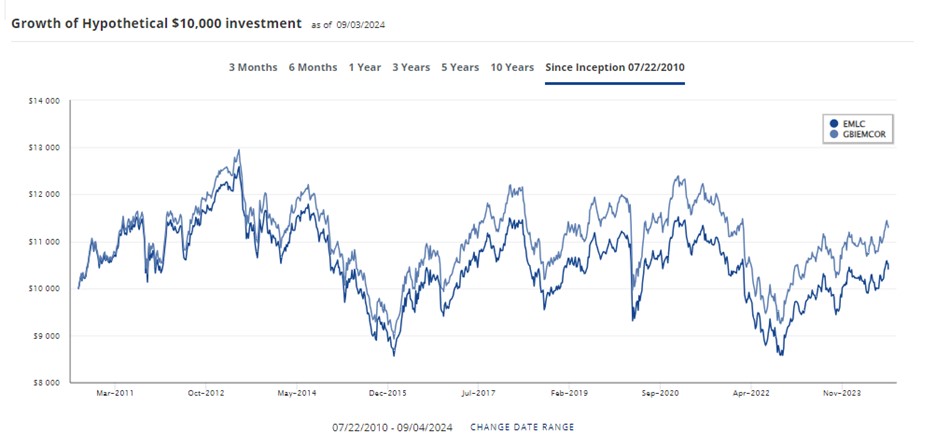

Here’s the performance of EMLC, including dividends, since the launch of the ETF in 2010. The summary is, emerging market local currency bond investors haven’t made any return in 14 years. Adjusted for inflation, they’ve lost more than 25% of their purchasing power. It’s been a terrible investment.

But now the big indebted major currency issuers are cutting interest rates. Meanwhile, emerging markets are in much better shape to deal with inflation and maintain high real interest rates.

Zim Integrated Shipping [ZIM] is the container shipping stock I told you about last week.

ZIM is a container shipping company. The thesis is simple. ZIM is sitting on a mountain of cash… almost equal to ZIM’s total market value.

Furthermore, it’s making giant quarterly profits, which it has promised to pay out as cash dividends. One analyst suggested on Monday that ZIM could report $10 EPS in Q3 and another $10 in Q4. (It’s an $18 stock.)

The bulls argue that it’s almost impossible to lose with ZIM. It’s so cheap, so rich in cash and making such great profits, we’ll likely make a 50% dividend in the next six months. After that, almost anything can happen in the markets and we’ll still come out ahead.

The bears argue that ZIM’s profitability is temporary, there’s an enormous structural overcapacity of containerships, and ZIM’s business could collapse any day and then ZIM will face many loss-making years ahead, which will incinerate ZIM’s cash pile and extinguish all hopes of dividends.

The key variable is therefore how much longer rates will stay at the current levels. Our bet is that the Red Sea will remain closed to the container trade for the rest of the year and supply of ships will stay tight.

This is definitely not a long-term investment. We’re renting this idea for three months at most, in the hope of getting a gigantic dividend. Every day counts.

***

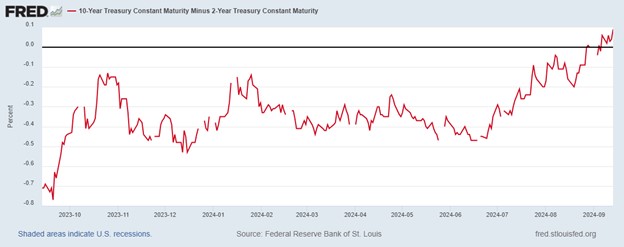

The yield curve has uninverted.

One of the surest signs of recession is an inverted yield curve that stops being inverted. I’ve read arguments why this time might be different.

But I wouldn’t bet against this signal. Especially when it’s accompanied by rising unemployment, falling commodities and falling cyclical stocks.

By the way, I’ve mentioned this before, but my favorite place for checking government bond yields is on this page at Bloomberg.

You can toggle between five different countries. And for each country, you can see short term, medium term and long term rates, plus inflation-protected rates.

https://www.bloomberg.com/markets/rates-bonds/government-bonds/us

Editor’s Note: If you want more (which you almost certainly will), check out the special offer Tom has put together exclusively for Porter & Co. readers by clicking here.

You’ll get his full portfolio – where the average return is already 30%+ – ongoing buy and sell recommendations, plus much, much more.

With a recession looming there’s arguably nobetter guide for getting you through the storm than Tom. His portfolio construction and investing approach will not only safeguard your wealth but grow it too.

Do not make the mistake of not following Tom. Because after 20 years in the trenches with him, I can tell you he’s a true investing genius. Get more from Tom here.