Issue #33, Volume #2

Why Investors Should Prepare For A 50% Drop In Stock Prices

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| Winston Churchill’s famous “The Few” speech… The S&P 500 could drop 50% or more… Never has the spread between haves and have-nots been this great… Even the wealthy are spending less… This recession indicator says “not yet”… |

While Porter is fishing in Panama with his son Seaton (keep up with his adventures on Instagram), The Big Secret On Wall Street analyst Ross Hendricks is picking up the baton to write today’s issue of the Daily Journal.

In August 1940, British Prime Minister Winston Churchill delivered to the House of Commons one of the most rousing wartime speeches of all time.

In what became known as “The Few” speech, Churchill praised the heroic efforts of the UK’s Royal Air Force, outnumbered three to one against the German Luftwaffe during the pivotal Battle of Britain.

The signature line of the speech went down in history:

“Never… was so much owed by so many to so few.”

Something similar could be said of the U.S. economy and stock market, including:

- Never has the engine of America’s economy been so dependent upon a relatively “few” wealthy households

- Never has the financial health of these households been so dependent upon the gains from a rising stock market

- Never before has the U.S. stock market been so dependent upon the performance of a small handful of stocks that are trading at sky-high valuations

But unlike Winston Churchill’s speech, which roused a nation to emerge victorious in the Battle of Britain and in the war, “the few” who are currently propping up the U.S. economy cannot support the nation much longer – macroeconomic data is now showing clear signs of consumer distress among all sectors of the population. In fact, U.S. Treasury Secretary Scott Bessent recently described the need for a “detox” period to cleanse the U.S. economy of its imbalances.

As I (Ross Hendricks) will explain, all signs indicate this detox period is already in full swing. The Trump administration’s on-again, off-again tariff policies and its wide-scale efforts at cutting costs and programs from the federal government created a high degree of uncertainty that helped trigger the 10% drop in the U.S. stock market that wiped out over $5 trillion of wealth in just four weeks.

As we’ll explain below (and over two issues of the Daily Journal next week), U.S. stock prices could fall by 50%. The S&P 500 is currently trading at a sky-high forward price-to-earnings ratio of 21. With consumer spending falling, earnings for companies that make up the S&P will drop too, pushing valuation multiples even higher. Thus, it’s only a matter of time before market forces kick in and a selloff sends share prices down to a level where valuation multiples fall back to historical averages of around 16.

America’s Two-Tiered Economy

In today’s U.S. economy, it’s the best of times for the wealthiest top 10% of earners, and the worst of times for the bottom 90%.

A recent analysis by Moody’s Analytics showed that the wealthiest 10% of U.S. households – those making over $250,000 per year – account for half of all consumer spending. That’s a record-high proportion, and up from around 35% in the mid-1990s:

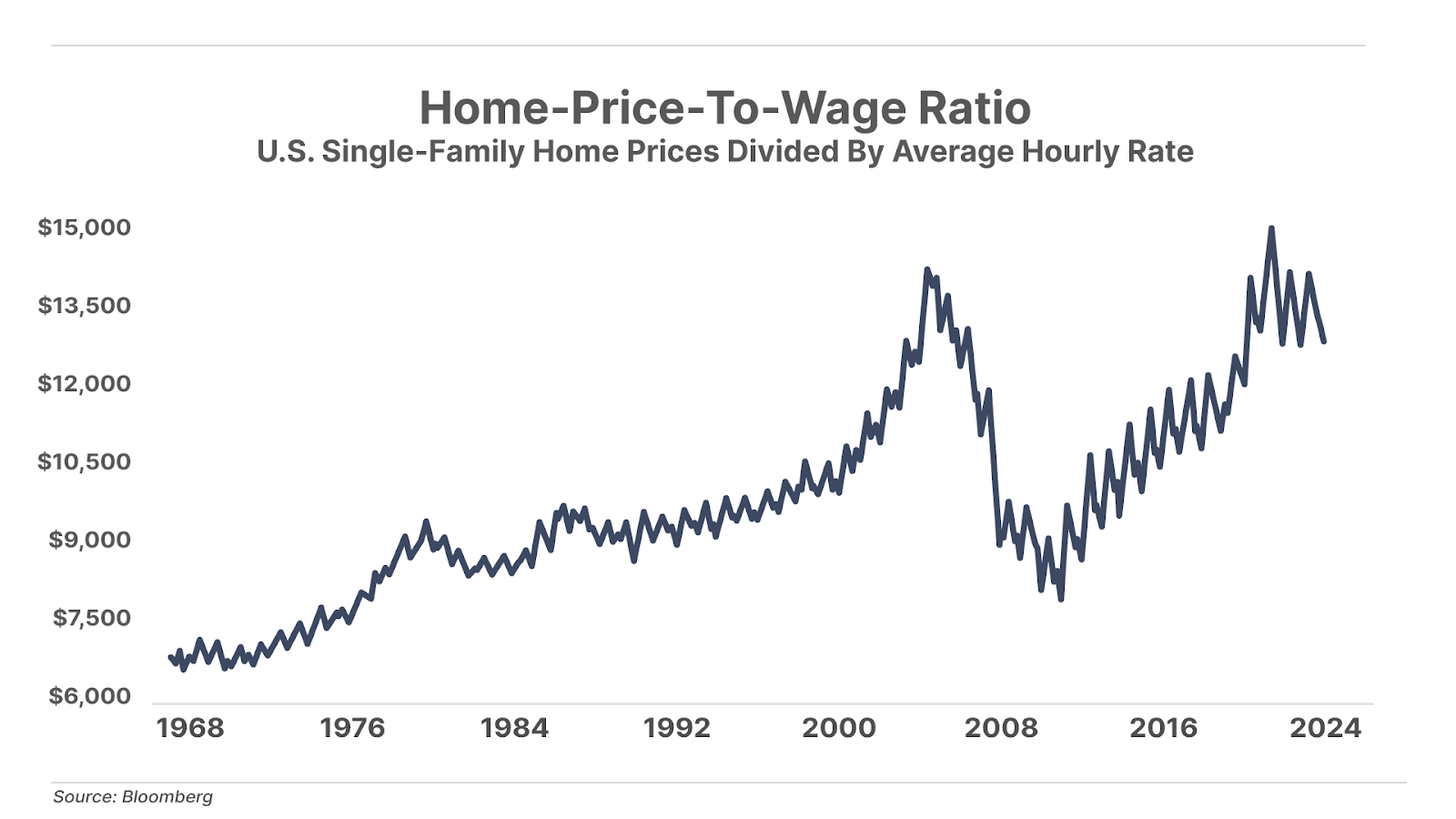

One driver of this record wealth gap between the rich and the poor is inflation. Inflation is the ultimate regressive tax – it steals from the poor and gives to the rich. While it does eat into the income of the top 10% to some degree, for the bottom 90% of earners who rely on wages (rather than assets) to survive, inflation is the silent thief that pushes up consumer prices at rates well ahead of their earnings growth.

Since 2019, average hourly earnings have increased by 30%, while prices for the key costs of living – including housing, food, insurance, education, and medical care – have risen more. While the CPI (the standard measure of inflation) has climbed 27% over that period, the real cost to consumers is higher, with the average mortgage payment up nearly 100%, car insurance up 54%, and egg prices climbing 15% in the month of January alone.

Conversely, the wealthy – who mainly generate their income from owning assets – have become the biggest winners during this period of rampant inflation. Historically, gains in asset prices tend to rise well above the rate of inflation – higher even than the elevated levels it has risen to in the last five years. Note the 89% total return of the S&P 500, and the 133% return in the tech-heavy Nasdaq 100.

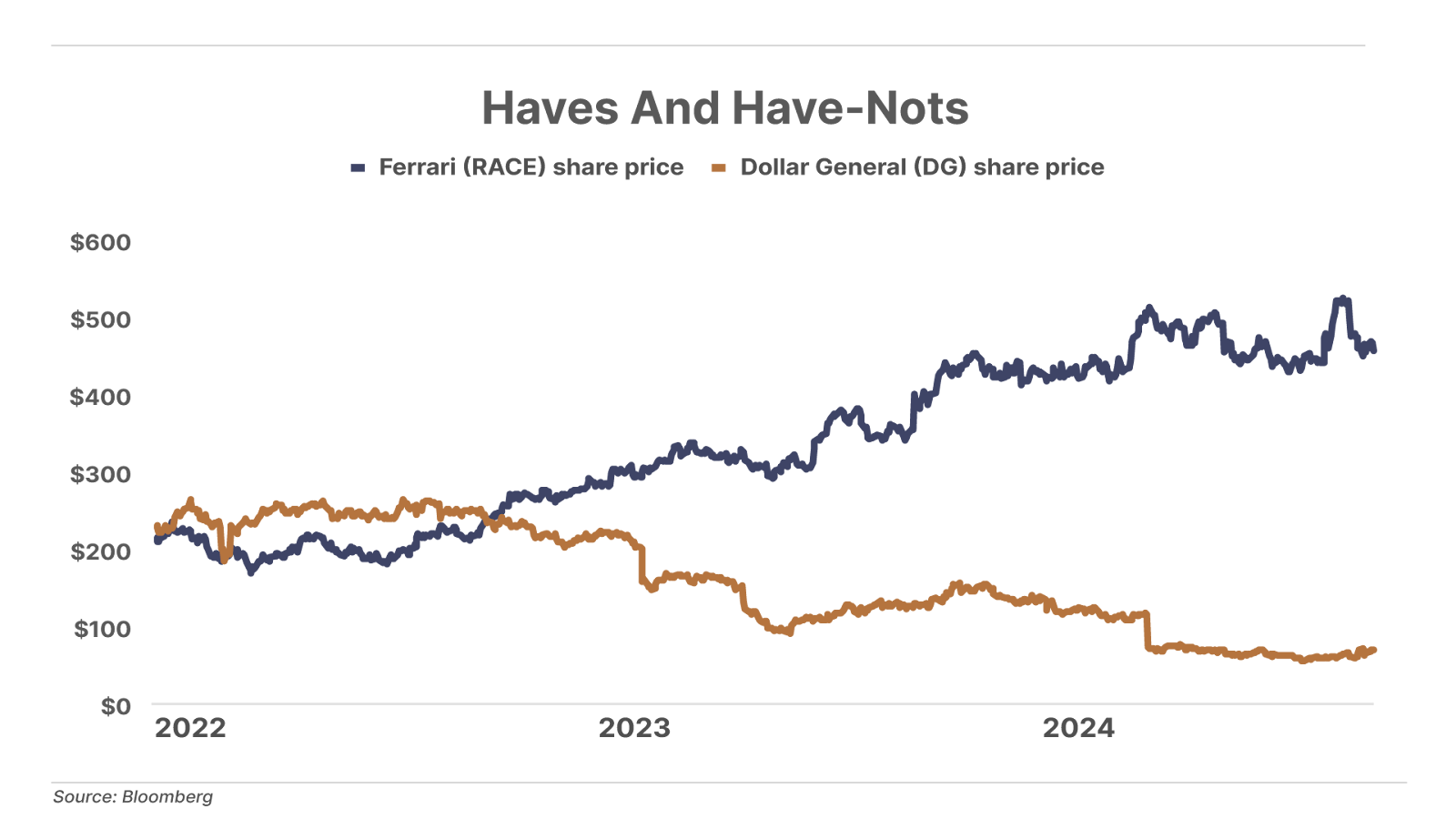

The diverging fortunes between wage earners and asset owners is how the U.S. economy has devolved into an increasingly fragile, two-tiered system of the haves and have nots. Perhaps the clearest sign of this is the difference in share-price returns of discount chain Dollar General (DG) and that of luxury-car maker Ferrari (RACE) over the last several years:

While many had hoped that the new Trump administration policies would breathe new life into the working class, all signs indicate their situation has only grown more tenuous. Consider the recent commentary from Dollar General’s management on its latest quarterly earnings call last week:

Our customers continue to report that their financial situation has worsened over the last year, as they have been negatively impacted by ongoing inflation. Many of our customers report that they only have enough money for basic essentials, with some noting that they have had to sacrifice even on the necessities. As we enter 2025, we are not anticipating improvement in the macro environment, particularly for our core customer.”

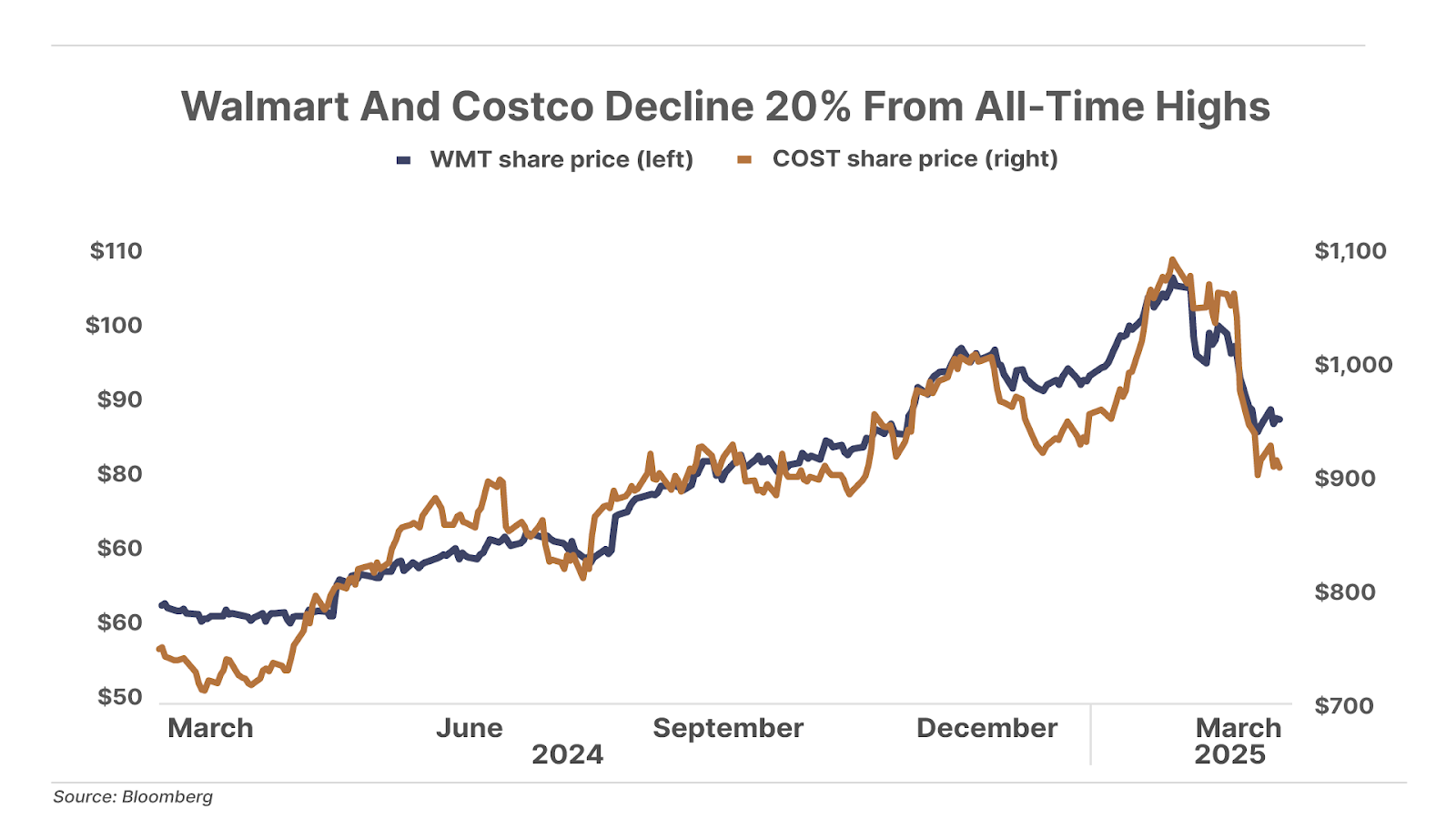

Until recently, consumption of the top 10% was enough to offset the economic distress among lower-income households. But in the last several months, it’s become clear that even the top 10% are spending less.

This includes the sudden deterioration in business among retail giants Walmart (WMT) and Costco Wholesale (COST). Over the past few years, both companies benefited from an influx of new consumers with six-figure incomes who were trading down to the discount retailers, leading to stellar operating results and new all-time highs in their share prices.

But now, that momentum has fizzled. Both companies have lowered their earnings outlook for 2025 in response to the weak spending trends the companies have observed so far this year. Both stocks have since dropped by 20% from all-time highs in late February.

Perhaps the biggest warning sign of the growing strains on the higher-income consumer cohort is coming from the travel-and-leisure sector, which is primarily driven by wealthier households.

According to recent survey results from the U.S. Conference Board, the percentage of Americans planning a vacation in the next six months dropped to a 15-year low in February (excluding 2020, when COVID-19 shut down the travel industry).

And U.S. airlines are feeling the brunt. In the past several weeks, all four major airlines have slashed their earnings and revenue outlook for 2025. This includes a March 11 announcement from Delta Air Lines (DAL), cutting its expected Q1 sales growth from 8% to 3.5% while lowering its earnings per share (“EPS”) expectations by 50%, to $0.40.

Just hours later, American Airlines (AAL) cut its Q1 outlook from 4% revenue growth to 0%.

Perhaps more alarming than the magnitude of these downward revisions was the speed in which they changed direction – both had published previously positive guidance in January.

The sudden reversal in guidance sent airline stocks down by 30% to 50%, with similar weakness spreading across the entire travel and leisure sector, ranging from casino and hotel stocks to the shares of cruise-line operators.

On Monday, Ross will highlight the key vulnerability facing the U.S. economy: the end of the record wealth effect created from the greatest bull market of the last 50 years, which removes the key pillar of strength holding up the U.S. economy.

Three Things To Know Before We Go…

1. Recession signal flashes green… for now. A Fed recession-probability model based on the yield curve just recorded a sharp drop – signaling no recession in the short term. The model calculates the probability of a recession based on the 10-year versus 3-month yield… Historically, a rise above 20% signals recession, while a drop below 20% suggests recovery. Most sharp declines occur after a recession begins, but this is only the third time since 1967 and 1999 that it has fallen significantly without a recession. In both cases, the S&P 500 rallied 20% over the next 12 months before eventually falling around 30%. If history repeats, markets could see short-term gains before a big downturn.

2. High prices drag down the housing market. Existing U.S. home sales fell by 1.2% year on year to a seasonally adjusted annual rate of 4.3 million in February. Despite fewer buyers, prices continued rising. The median U.S. home price reached a record high of $398,000 in February, the 20th consecutive monthly increase. The number of unsold homes sitting on the market rose 5% from January to 1.24 million. The housing market remains frozen as affordability remains out of reach for a growing number of Americans.

3. Sign of the top: Buy-now-pay-later on your doorstep. Klarna – one of the biggest purveyors of the buy-now-pay-later (“BNPL”) convenience – just announced that it’s teamed up with DoorDash, which will deliver on demand pretty much anything available at a store or restaurant. That means that consumers whose credit cards can’t handle the full price of that Big Mac with fries (or gallon of milk) will have the option of paying for it in four equal interest-free installments. Someday – and it’s getting sooner – the illusion that we (consumers… the government… everyone) can “pay for it later” will come crashing down, as “later” finally arrives.

And one more thing… Recession Or No?

The Fed’s yield-curve recession indicator (above) points to no recession on the near-term horizon. But sky-high stock market valuations, weak consumer-spending data, and turbulence caused by mixed policy messages out of Washington suggest otherwise… What do you think?

Ross Hendricks

Houston, Texas

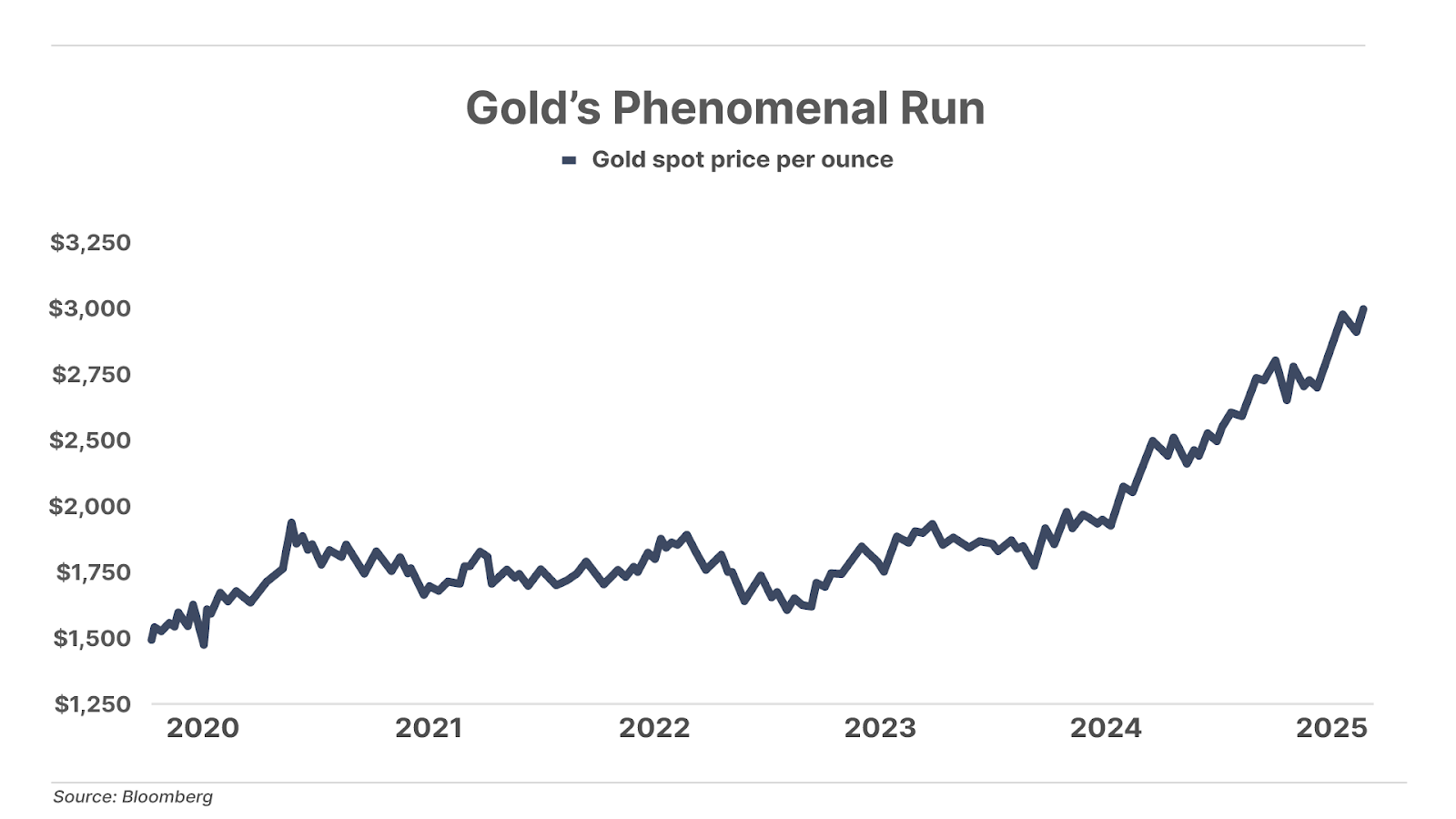

P.S. Gold hit yet another fresh all-time high this week.

It’s up 38% over the past year… a lot better than the S&P 500’s 7%. And since the S&P’s peak, the stock index is down 8.6%… while gold is up 2.7%.

Gold is more than just portfolio insurance… it’s more like portfolio jet fuel.

What’s going on? Porter & Co.’s go-to source for insight on what’s happening with gold is Marin Katusa – a friend of Porter’s who’s one of the world’s premier experts on natural resources… and gold in particular.

Marin breaks down gold’s story – and whether now is still a good time to invest in it – in a new presentation… check it out here.

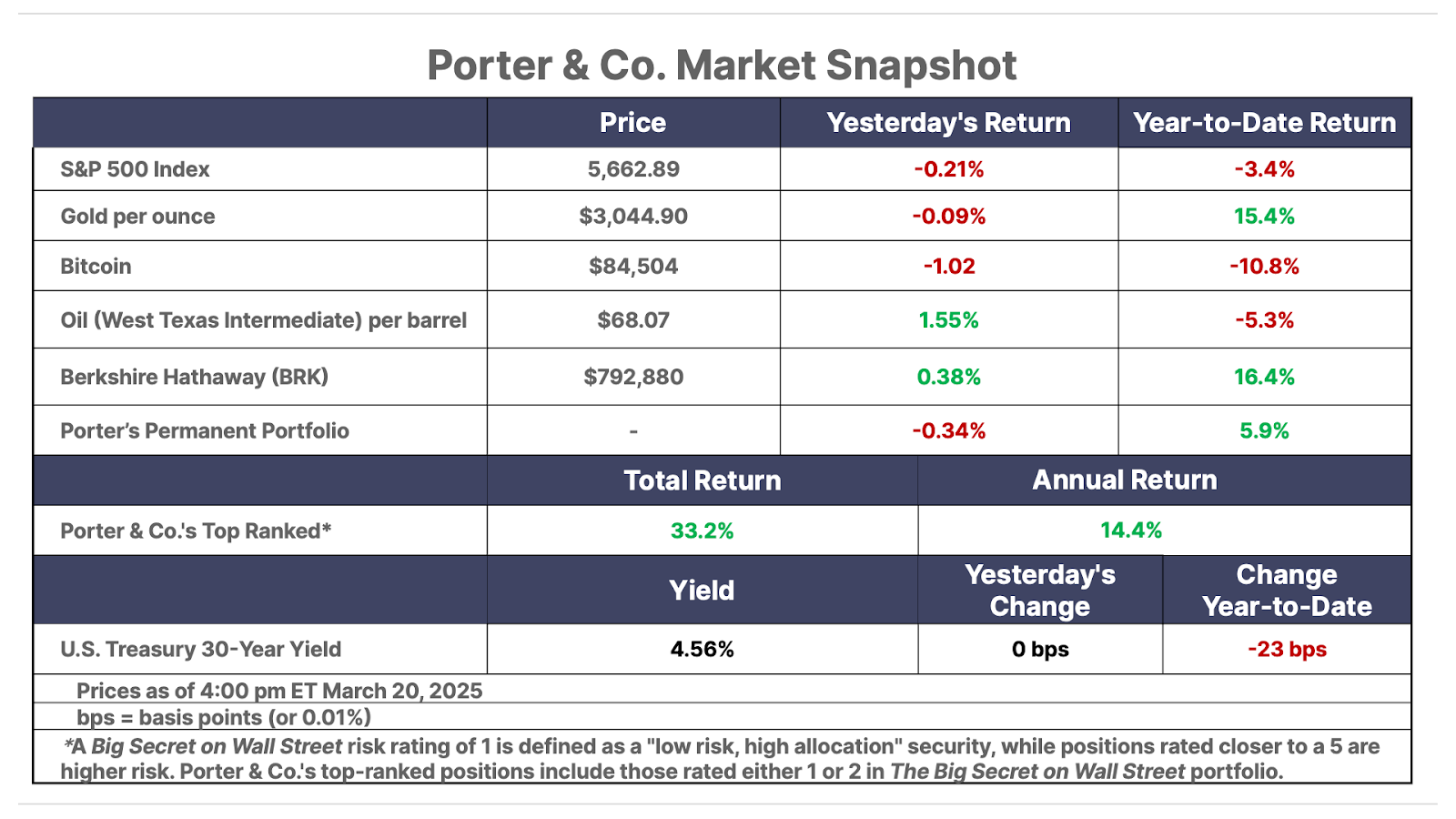

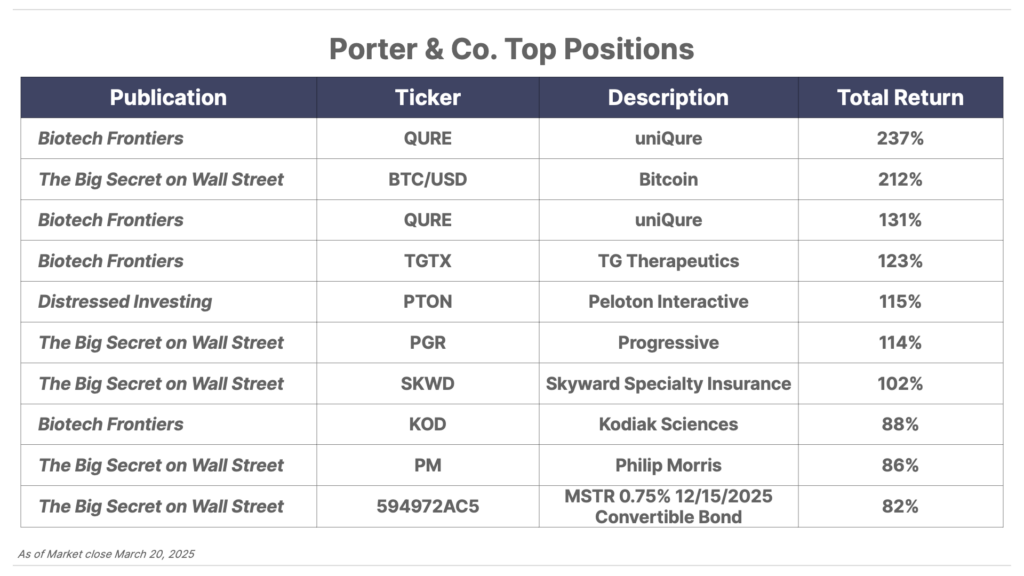

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.