Editor’s Note: Last week, we asked who and what you wanted to be Spotlighted next. The responses varied from the totally expected, to the mildly surprising, to the completely unhinged.

Our team is working through the responses to put together a list of people we can hopefully feature in these pages.

One theme we saw in a lot of your responses was more analysis on gold and silver, which, given how the markets have shifted over the past year, makes perfect sense.

It’s also why for today’s Spotlight, we’re republishing two essays from Garrett Goggin – founder of Golden Portfolio – that walk us through the massive trends he sees unfolding in the precious metals sector.

Enjoy.

P.S. Many of you asked for analysts we have already featured, too. So don’t forget you can access our entire backlog of Spotlights for free, here.

Buffett’s Coming For Gold Stocks

By Garrett Goggin

Good things happen to companies with strong free cash flow (FCF).

I don’t measure the miners like everyone else. I really don’t care about ounces per share, or leveraged high cost plays, I simply follow the money.

Strongly profitable companies pay dividends, buy back shares, and pursue shareholder accretive growth projects, all which drive shareholder value. I’ve never seen the gold miners more profitable and more undervalued.

Famous investor Warren Buffett coined the phrase “Price is what you pay. Value is what you get.”

I’ve been covering the gold miners for over 15 years, and I’ve never seen a larger mismatch between the market price and net asset value (lifetime discounted profit stream).

Investors are able to spend dimes for gold miners that will generate dollars of profits. I believe Buffett will be attracted to the gold mining sector due to his “value you get” aphorism.

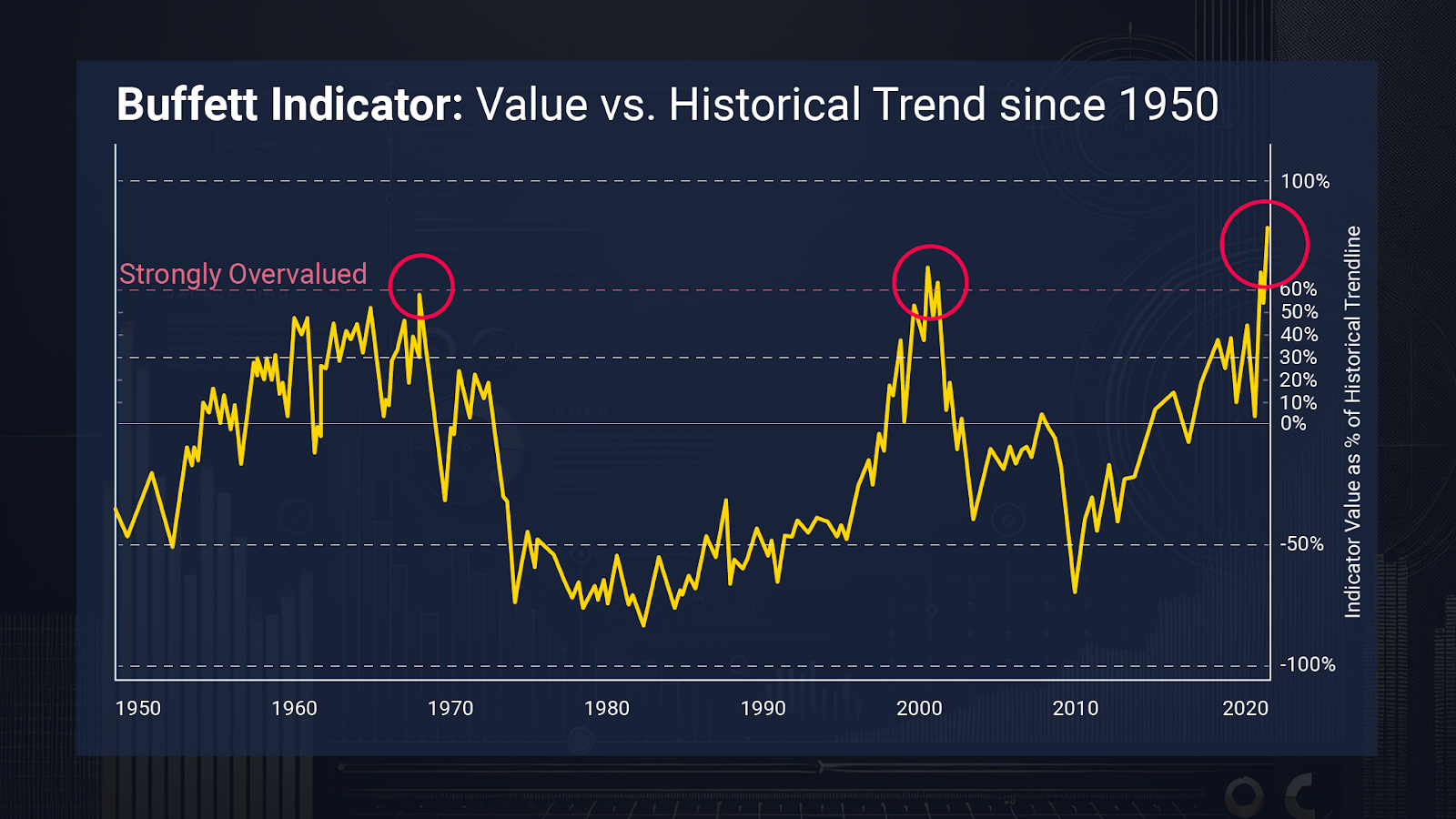

Buffett’s famous market indicator shows us we are at the beginning of a decade-long secular shift between overvalued growth assets and undervalued real assets. This is a perfect storm for gold miners with gold over $3,000/ounce, extreme undervaluation, and lack of any significant investor interest.

Buffett Indicator And Gold

Buffett relies on his famous Buffett Indicator to allocate his reserves.

The metric compares the market cap of the Wilshire 5000 to underlying U.S. GDP.

When the Wilshire 5000 rises above the U.S. GDP, stocks are overvalued, and when the market cap of the world’s largest index is below U.S. GDP, stocks are undervalued.

The Buffett Indicator was the highest ever at 209% at the beginning of this year, and the Oracles of Omaha was selling stocks. He amassed a $334 billion cash reserve. That’s a massive 54% of his portfolio, because he knows stocks are too high.

He built reserves, waiting for the market to decline so he can once again buy FCF at a discount. I know exactly where he’ll find it.

The Buffett Indicator is also a measure of growth stocks versus cyclical deep value real assets. When the world’s economy is vibrant, growth equities soar.

But as we now enter a period where the world’s trade splinters due to tariffs and deglobalization, economic growth takes a hit.

Long overlooked underpriced commodity assets are gushing cash. Buffett will buy profits at a discount, no matter the source. He’s invested in candy makers, furniture stores, and now he’s coming for the gold producers.

And this won’t be the first time Buffett came for real assets like gold and silver.

Buffett famously built a 130-million-ounce silver position in May 1998, as the internet bubble gained steam, pushing his Buffett Indicator to an elevated 150% level.

Mr. Buffett also purchased shares in Barrick Mining (GOLD) in 2020. Again at a time when his Buffett Indicator was well overvalued at 200%.

Now his Buffett Indicator was even higher at the beginning of this year and the opportunity for gold and real assets is even greater.

Buffett’s Coming For Newmont

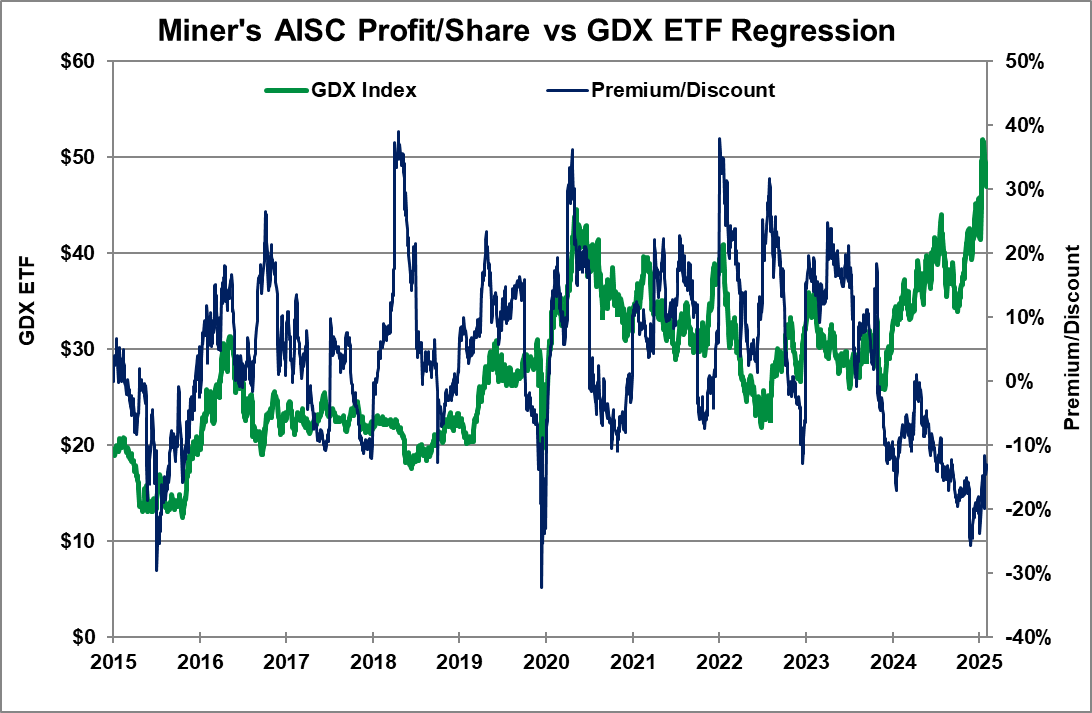

GP tracks its own Buffett Indicator for gold stocks based on AISC (all-in sustaining costs) profit/share versus the GDX ETF. The GDX has a 89% correlation to AISC profit/share of the large-cap gold miners (Agnico Eagle Mines, AngloGold, Barrick Mining, Kinross Gold, and Newmont).

GP runs a regression study that predicts GDX price using current AISC profit/share of the five major gold miners based on the latest quarter’s annualized production and AISC using the daily closing gold price of each day.

The GDX is currently trading at a large 20% discount to fair value based on projected AISC profit/share at the current gold price.

Only twice before, in 2015 and 2020, has the GDX traded at a larger discount to AISC profit/share. Both prior times marked a low in gold stocks, and the GDX rose 100%+ over the next few months.

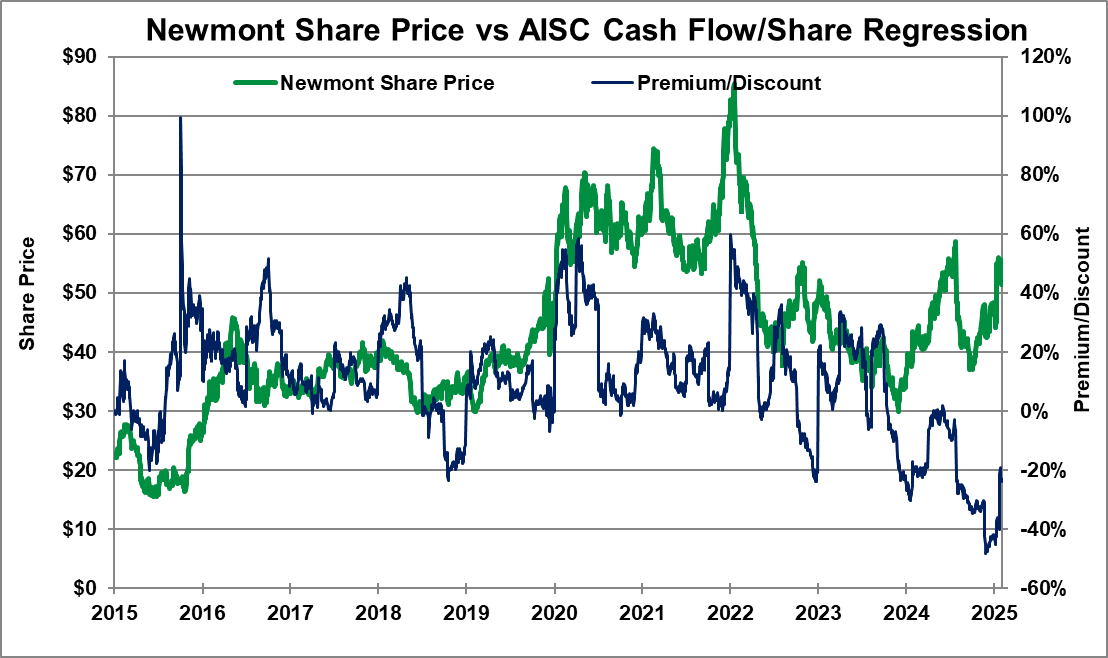

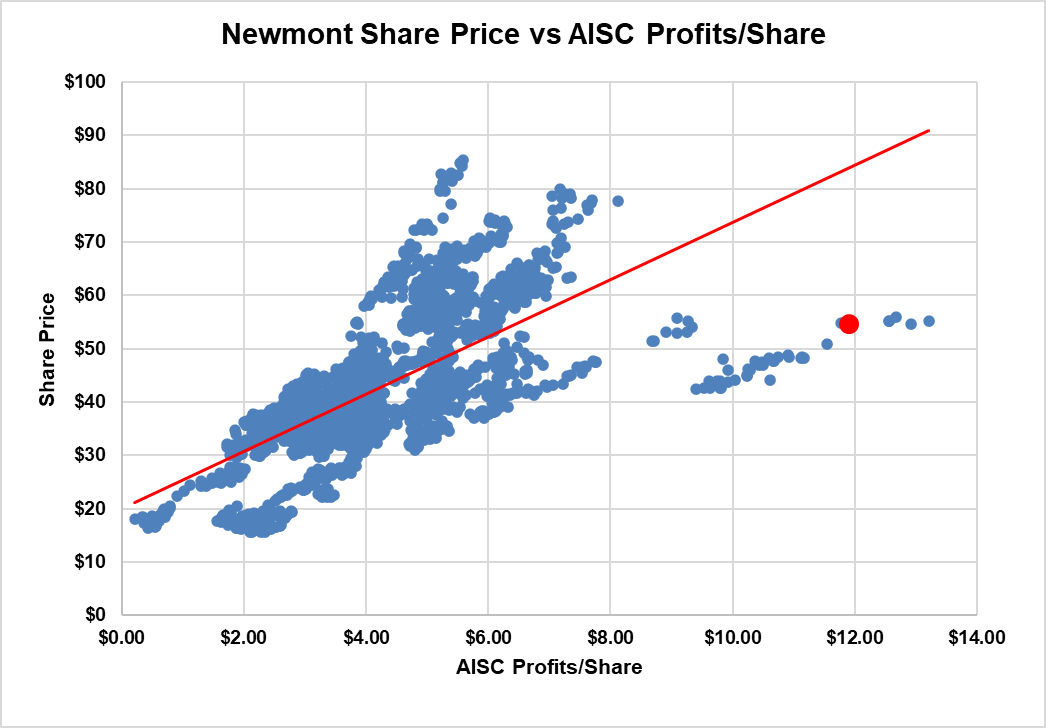

Newmont (NEM) reported $1.25 per share earnings last week for Q1/25 versus analyst expectations of only $0.92.

Newmont should generate a whopping $11,308 million AISC profit over the next year, equal to $9.78 per share, using the gold price of $3,000/oz.

Newmont was trading at a massive, never-before-seen, 47% discount earlier this year based on $9.78 AISC profits/share. Newmont’s fair value based on AISC profit/share is $80.41.

The stock has moved higher over the past weeks and now trades for $51.44 – at a 20% discount.

In 2024 Newmont traded at a 31% discount to fair value based on AISC profit/share and the stock doubled in six months. Newmont is set up for a big run here.

Total projected Newmont AISC profits of $11,308 million represents a significant 21% AISC profit yield based on current $60,700 million enterprise value (EV). Good things happen to companies that generate strong profits.

Dividends increase, shares are repurchased, and investments are made to drive shareholder value while dilution is minimized.

AISC profit yield is a measure of the amount of profits vs the market value of these profits. The higher the better. High 20%+ AISC profit yield is how GP identified Newmarket Gold, which was acquired by Kirkland Lake, then Agnico Eagle, which resulted in 10X+ stock price performance.

Silver Crest Mining also traded at a 20%+ AISC profit yield back in 2015 when it was acquired by First Majestic Silver. SilverCrest Mining spun out SilverCrest metals as a free stock spinout to shareholders that represented another 10X+ winner for my followers.

I don’t often gamble, but when I visit Las Vegas for a conference I often play blackjack.

I keep a running count of 10s and non-10s as the cards leave the shoe. I sit for hours without an edge playing basic strategy as the 10s and others flow in and out.

But when the deck is rich in 10s I load up my bet as the dealer breaks more often than average and I get 20 or 21 at a high percentage.

A deck rich in 10s does not equal a sure winner, but the odds are greatly in my favor, and I try to leverage the opportunity.

The largest gold stock in the sector, Newmont, is now trading at a 21% AISC profit yield, representing an extreme opportunity. The deck is rich in 10s. Good things happen to miners with 20%+ AISC profit yield.

Value investors will come.

Retail will pile on and assets will return to the gold sector. You can be sure Buffett is watching Newmont, no doubt attracted by its strong 20% AISC profit yield.

When Buffett’s next 13F for Q1/24 hits the tape, don’t be surprised when you see him holding a new position in Newmont (NEM). When the media is in a frenzy, remember GP, where you heard it here first.

While Newmont isn’t a Golden Portfolio or Golden Portfolio 10X recommendation, it’s the largest gold stock in the world — and when Newmont rises, the sector tends to do well.

The Golden Portfolio and Golden Portfolio 10X recommendations are likely to perform multiples better.

Get Out Of Growth Stocks And Into Gold Stocks

The Buffett Indicator is a measure of debt-fueled excess in financial markets.

GDP is straight-up economic growth. The Wilshire 5000 is the market price of these assets, or multiple, which is influenced by many factors including inflation, interest rates, investor expectations and money supply.

The Buffett Indicator is also a measure of growth assets versus real assets, like gold.

When money is easy, investors chase growth, pushing asset prices to ridiculous extremes… but there is a limit to the financial engineering. And the 209% Buffett Indicator shows we are there now, with financial assets trading richly versus underlying GDP.

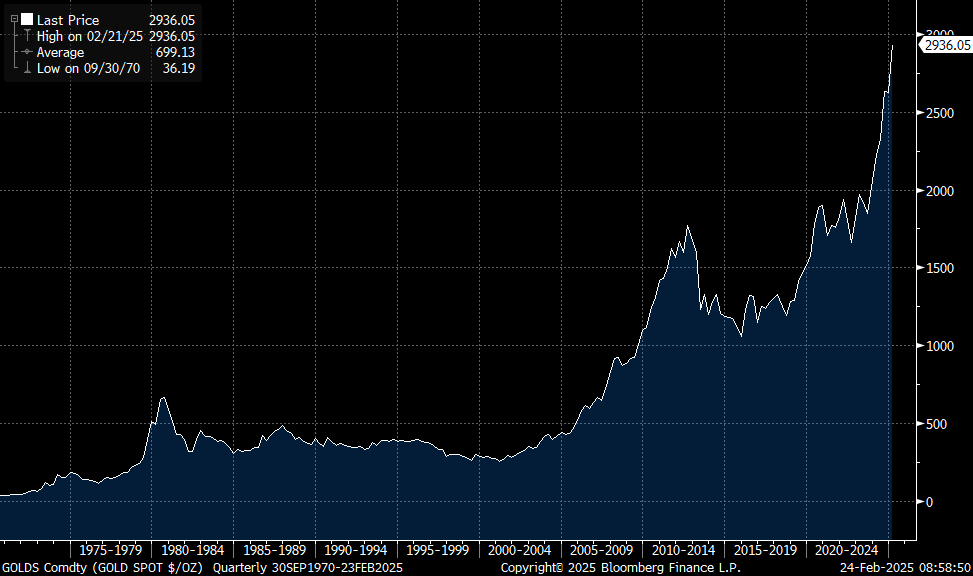

Prior peaks in the ratio were 88% in 1970, 163% in 2000, and 200% in 2020. Stocks then struggled while gold went on a decade-long run higher, every single time.

In 1970 gold rose 20X from $41/oz to $800/oz in 1980. In 2000, gold rose 8X from $250/oz to $1,900/oz in 2012. Gold traded at only $1,500/oz in 2020. Now gold is already at $3,000/oz, and this secular shift between growth and real assets has only just begun.

We all know gold’s value is tied to the money supply and debt outstanding.

The more money outstanding, the higher the gold price will rise. In 2000 the Fed slashed rates to 1% from 5%.

In 2020 with rates already at 0%, it wasn’t enough, so the Fed stepped in and purchased troubled assets, driving their balance sheet 3X higher from $3 trillion to $9 trillion.

The U.S. is $37 trillion in debt. Financial imbalances are the largest ever.

President Donald Trump is bringing gold back to the U.S., while Fort Knox is going to get audited.

Treasury Secretary Scott Bessent seeks a new Bretton Woods that will bring gold back as a monetary asset. China has been buying tonnes of gold over the past 10 years instead of U.S. Treasuries.

Gold is the ultimate store of value. It’s the only asset that’s truly independent, unencumbered, that represents no one’s liability.

The U.S. can delete our trade partners with a simple push of a button if they run afoul of U.S. foreign policy. It’s no surprise countries around the world are choosing gold, instead of Treasuries.

Buffett said it best in his latest annual letter to shareholders.

“Paper money can see its value evaporate if fiscal folly prevails. In some countries, this reckless practice has become habitual, and, in our country’s short history, the U.S. has come close to the edge. Fixed-coupon bonds provide no protection against runaway currency.”

The Buffett Indicator shows us we are at the cusp of a decade long secular shift between growth vs real assets. Gold has done well, now at $3,000/oz, but other peaks in the Buffett Indicator in 1970 and 2000 marked the low for gold and gold stocks.

Over the next decade, from the prior peaks of the Buffett Indicator, gold and gold stocks rose multiple times in value as the U.S.’ debt-laden economy was forced to reset.

Nobody Is Invested In Gold

Gold will continue to climb higher until the masses come, and we have a long way to go.

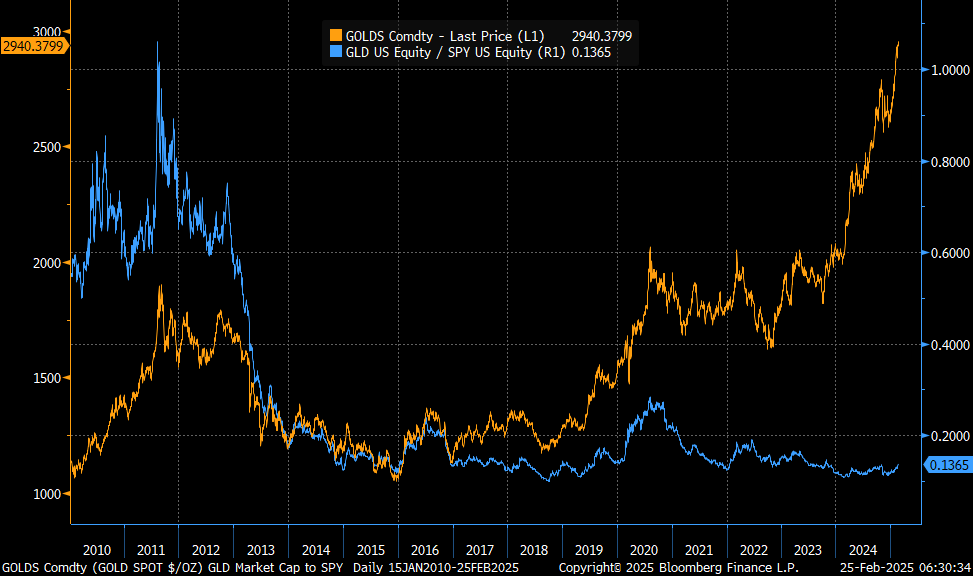

The GLD ETF held $75 billion in assets in August 2011 just before gold’s last major peak at $1,900/oz in 2022. This was more than was invested in the popular broad equity market SPY ETF that only held $71 billion.

You can see the GLD/SPY market cap ratio rise above 1.0 in 2011 below.

The GLD ETF now holds $83 billion in assets versus the SPY at $602 billion for a 13.65% ratio. GLD assets need to increase 7.3X to match the SPY. Despite gold rising nearly 30% in 2024 investors haven’t climbed aboard the GLD ETF yet, but they will.

Every major gold top is marked by a surge in retail demand who flock to the GLD ETF pushing shares out and market cap significantly higher.

Gold has to climb much higher to create a surge in investor demand that will once again coincide with the next major top in the gold price.

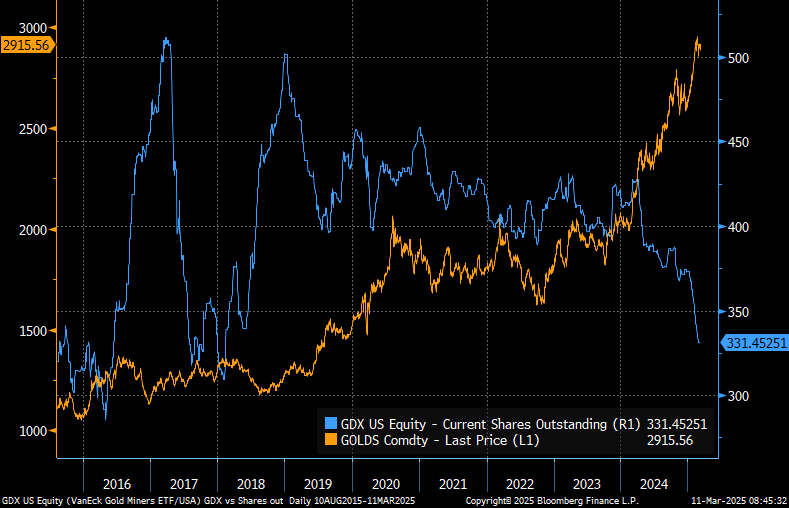

Look at the GDX VanEck Gold Miners ETF. When gold rose from $2,000/oz in March of last year to $3,000/oz now, GDX shares outstanding plummeted 22% to 331 million now from 427 million in March. Investors are fleeing the sector.

The average investor always does the opposite of what they should do: Rushing in to create market tops, and selling all exposure marking the market bottom.

Gold miner AISC profit valuation shows us gold stocks have rarely been cheaper. The deck is rich in 10s. The odds are in our favor. Opportunities like this are rare. It’s time to load up for the next leg higher.

This Is Your Golden Opportunity

Everyone thinks gold is too high. Let me tell you, it’s not.

Based on the prior peaks of the Buffett Indicator which mark the peak of a debt cycle, gold is going to continue to rise significantly over the next few years.

Everyone believes gold stocks are too expensive. I’ve shown you above they’ve never been this cheap. The Buffett Indicator shows we are beginning a rare secular shift from growth to cyclical assets.

As investor assets begin to flow back into the gold sector, AISC profit multiples will rapidly expand and drive gold stock prices higher.

After 15 years of working at Stansberry Research and the Gold Stock Analyst, I went out on my own in 2023 and created the Golden Portfolio, the best way to invest in Gold.

My gold stock portfolios have crushed the benchmarks. My GPIV product is up 259% since 12/31/23 while the GDX Gold Miners ETF is only up 51%.

Don’t worry, you haven’t missed the boat. GPIV companies are still woefully undervalued. One GPIV holding is a gold developer that is building a project worth $3.2 billion NAV at $3,000/oz gold and the stock is only trading for $770 mil market cap.

When in production in late 2026 market cap should rise to match NAV, the lifetime sum of FCF profits from the mine.

Others in the GPIV portfolio are trading for even deeper discounts.

We are going higher until the masses come.

Part II: USD Shock

Buffett made some bold statements about the real story behind gold’s rise, and the state in which he believes the U.S. dollar (USD) currently finds itself…

I created the Golden Portfolio system as the ultimate solution to beat monetary debasement.

Better than physical gold, and gold stock ETFs, my GP portfolios contain deeply undervalued gold stocks that simply need to execute to drive value regardless of the Gold price.

A rising gold price is simply the “cherry on top” of the entire shareholder value creation process.

Gold stocks have been ignored for decades, and right now they’ve never been cheaper. Now, for the 1st time ever, we’ve seen the USD and bonds sell off along with stocks.

This hasn’t happened in over 50 years. It’s truly the end run for the USD and its $37 trillion debt, and Mr. Buffett knows it.

On May 5, 2025, at the most recent Berkshire Hathaway shareholder meeting, Buffett painted a bleak picture for the U.S. dollar, he stated:

“I mentioned very briefly in the annual report that fiscal policy is what scares me in the United States because of the way it’s made, and all the motivations are toward doing things that can cause trouble with money.

But that’s not limited to the United States – it’s all over the world, and in some places, it gets out of control regularly. They devalue at rates that are breathtaking, and that’s continued.

People can study economics and you can have all kinds of arrangements, but in the end, if you’ve got people who control the currency, you can issue paper money or engage in clipping currencies like they used to centuries ago.

There will always be people who, by the nature of their job – I’m not singling them out as particularly evil – but the natural course of government is to make the currency worthless over time.“

If that’s not a green light for precious metals investors, I don’t know what is.

Warren Buffett has been no fan of gold.

He’s been famously critical of the metal, essentially saying it’s not very useful.

He once said:

“I will say this about gold. If you took all the gold in the world, it would roughly make a cube 67 feet on a side…Now for that same cube of gold, it would be worth at today’s market prices about $7 trillion—that’s probably about a third of the value of all the stocks in the United States.

For $7 trillion…you could have all the farmland in the United States, you could have about seven Exxon Mobil (XOM), and you could have a trillion dollars of walking-around money.

And if you offered me the choice of looking at some 67-foot cube of gold and looking at it all day, and you know me touching it and fondling it occasionally…call me crazy, but I’ll take the farmland and the Exxon Mobil.”

That’s all true, but Buffett is being a bit disingenuous here. He’s comparing a physical commodity to securities and productive farmland. But they’re all different assets.

Sometimes you have to pay more attention to what someone does, because Buffett is no stranger to owning physical precious metals.

In 1997, he bought nearly 3,500 tonnes of physical silver at a price between $4-$6/oz.

He sold this silver in 2006 between $9-$13/oz – an easy 100%+ gain – earning Berkshire Hathaway ~$650 million in less than 10 years.

Buffett also bought Barrick Gold (NYSE: GOLD) in 2020. I believe he’s now coming for Newmont Mining (NYSE: NEM). Newmont is gushing cash and trading at a deep 35% discount-to-profit-based fair value.

In 2024 alone, Newmont paid out $1,145 million in dividends, bought back $3,860 million of debt, and repurchased 1,246 million shares.

So far this year, Newmont has paid $282 million in dividends, bought back $985 million of debt and repurchased $348 million shares. Annualized, this is $6,460 million in value creation equal to a massive 10% shareholder yield.

When Buffett comes, and Newmont rises, my Golden Portfolio IV (“GPIV”) (more below) contains five smaller gold miners and developers that will soar multiples higher.

When the world’s greatest living investor warns you about the devaluation of global currencies, you should take note.

He’s not just talking about his book.

At this point, he’s retiring and he’s in his early 90s.

If you agree with Buffett that central bankers are doomed to continually and drastically devalue their currencies, then you only have one rational move as an investor.

I created the Golden Portfolio as your ultimate gold investment. My GPIV contains five of my top gold stocks. GPIV’s performance is unsurpassed, up 287% since the end of 2023.

My GPIV portfolio has done great, but there is much more to come.

GPIV stocks represent the best projects the gold industry has to offer, world class assets trading at massive discounts-to-FCF profit-based fair value.

The rising price of gold has driven significant value into the underlying assets of these companies and the stock prices have yet to catch up.

GPIV holdings are still deeply undervalued; one still trades for an extreme discount of 97%. Get on board now while there are still bargains to be had before the masses come.

Best,

Garrett Goggin, CFA, CMT

Chief Analyst and Founder, Golden Portfolio

Editor’s Note: If you want more from Garrett, check out his presentation here, where he details why the “Buffett Indicator” predicts gold could be set to dominate for the next decade…

And the four gold stocks Garrett thinks are most likely to benefit from the coming monetary shock.