The Hidden Risk Behind The Mag-7’s “Cheap” Valuations

How The AI Arms Race Is Undermining Its Biggest Players

| This is Porter & Co.’s The Big Secret on Wall Street, which we publish every Thursday at 4 pm ET. Once a month, we provide our paid-up subscribers with a full report on a stock recommendation, and also a monthly extensive review of the current portfolio… At the end of this week’s issue, paid-up subscribers can find our Top 3 “Best Buys,” three newly added portfolio picks that are at an attractive buy price. You can go here to see the full portfolio of The Big Secret. Every week in The Big Secret, we provide analysis for non-paid subscribers. If you’re not yet a subscriber, to access the full paid issue, the portfolio, and all of our Big Secret insights and recommendations, please click here. |

Editor’s note: The major U.S. equity indexes fell by 4% to 6% today following President Donald Trump’s announcement of sweeping tariffs on Wednesday afternoon. We’ll provide some general insight on these moves in tomorrow’s Daily Journal. In the meantime, rest assured, if there are any important changes to any of the recommendations in The Big Secret On Wall Street portfolio in between our regular weekly issues, we will email all paid-up subscribers with a special alert.

In early 2020, just days after the first confirmed case of COVID-19 in the U.S., a different kind of risk appeared inside one of America’s most successful technology companies. And virtually no one – outside of a handful of industry accountants – noticed.

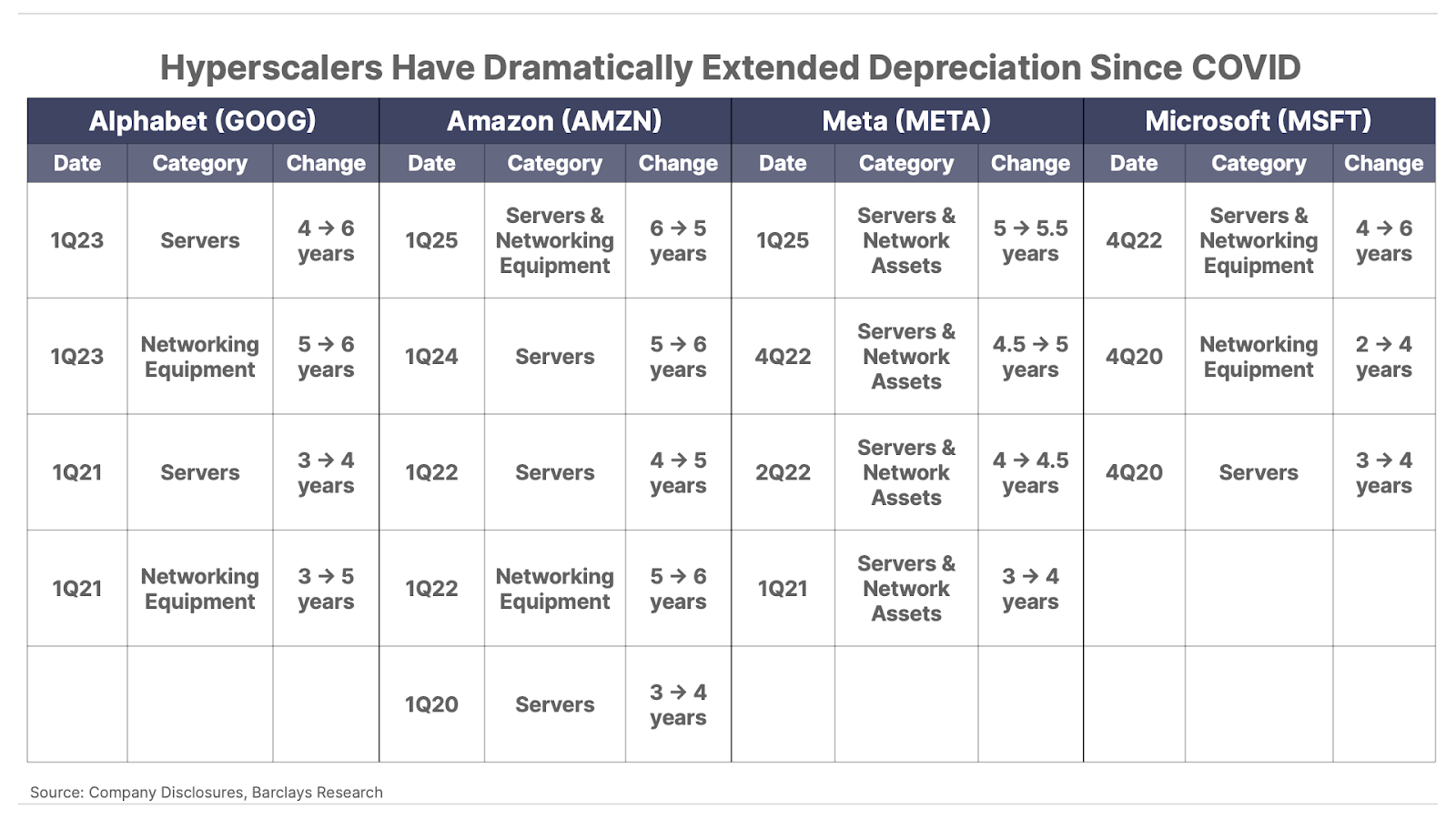

Amid headlines of stellar fourth-quarter sales and earnings growth, Amazon (AMZN) announced it was increasing the estimated “useful life” of the servers powering its Amazon Web Services (“AWS”) business. As a result, those servers, whose cost was previously depreciated over three years, would now be spread out over four years.

It sounded mundane… but this small tweak ultimately allowed Amazon to report more than $2 billion of additional operating profit in 2020, without requiring an additional cent of revenue. And the company’s Big Tech competitors took note.

Within a year, Alphabet’s Google (GOOG), Meta Platforms (META), and Microsoft (MSFT) all followed suit, extending the useful life of their data center equipment. By 2023, the average assumed lifespan for a server or networking equipment at these companies had roughly doubled from pre-2020 levels.

Extending the depreciation of these assets reduces reported annual operating expenses, allowing the company to record an increase in operating income. This subtle accounting maneuver has delivered a windfall of profits for these companies over the past several years. But today, in 2025, it may now be coming back to hurt them.

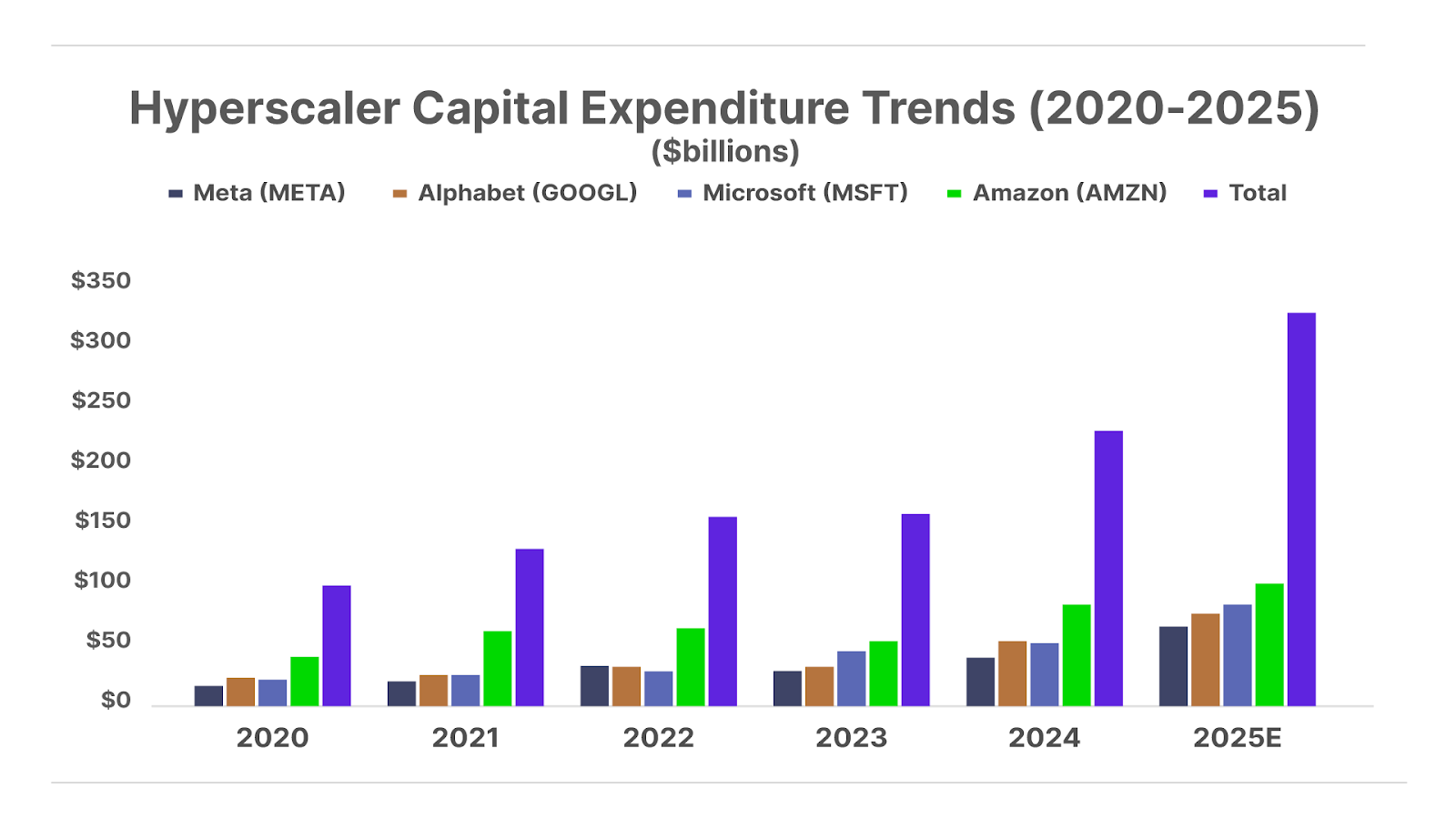

You see, as the artificial intelligence (“AI”) boom has exploded over the past few years, these same four companies (Amazon, Meta, Google, and Microsoft) have become the leading “hyperscalers” – companies that provide the massive cloud-computing and data-management resources required to develop, train, and deploy AI models at scale. This role has required these companies to make massive new capital expenditures (“capex”) on servers and networking equipment.

However, the AI hardware arms race – fueled by Nvidia’s (NVDA) revolutionary graphics processing units (“GPU”) chips – is advancing so quickly that equipment is becoming obsolete at an ever faster pace. Which means that, sooner or later, these companies will have to reverse course, and shorten the reported useful life of their servers and networking equipment significantly. When they do, the earnings boost they’ve enjoyed for the past several years will shrink.

Below we’ll take a closer look at how these changes inflated Big Tech earnings, why this trend is likely over, and what it means for investing in these stocks today.

Billions In Phantom Profits

Over the past five years, the four leading hyperscalers – Amazon, Alphabet, Meta, and Microsoft – dramatically extended the lifespan assumptions for their data-center servers and networking gear. The chart below illustrates this collective shift:

It’s no coincidence that the four hyperscalers moved in lockstep. Amazon’s initial change was justified by an internal study suggesting that servers were lasting longer due to better software and maintenance. The following year, Microsoft, Google, and Meta quickly came to the same conclusion, upping their useful lives to four years.

A similar pattern played out when Amazon extended the useful life of its equipment a second time in 2022 – its peers followed with their own extensions shortly thereafter.

In short, once Amazon showed that extending depreciation was “allowed” – meaning, it would be well-received by investors – the others were quick to jump on the bandwagon.

From a corporate perspective, this move was perfectly legal and arguably even rational: if software optimizations truly make hardware last longer, a company would be foolish not to take advantage of the extended useful life on its books. And during the 2020–2022 period, there were indeed efficiency gains and pandemic-driven delays in hardware upgrades.

But as we will explain, the financial impact of these changes was huge – and not all of it can be attributed to genuine technological improvements. Rather, much of it merely looks like an opportunistic accounting trick to goose earnings.

In simple terms, it works like this: a fully paid-for server that was once expensed (depreciated) at $10,000 per year over three years ($30,000 total cost) might now be depreciated at $5,000 per year over six years. Extending the useful life essentially cuts the company’s related annual expenses in half.

These changes don’t reflect any new revenue or improved cash flow. They are purely accounting adjustments. Yet, they can still have a profound effect on a company’s results… A lower depreciation expense directly boosts operating profit and net income, since depreciation is counted as an expense on the income statement.

The cumulative effect of these depreciation tweaks was to add billions of dollars of “phantom” profits across the hyperscalers – profits that did not come from additional sales or improved operations, but simply from accounting changes.

In total, these four companies added well over $20 billion of cumulative income in recent years via these depreciation changes alone.

Naturally, Wall Street’s reaction was broadly positive: higher reported earnings usually justify higher share prices. And because these changes were disclosed in footnotes or brief remarks (often framed as technical adjustments), the narrative remained: “Big Tech is managing costs well and squeezing more out of their capex.”

However, there’s a reason we referred to these gains as “phantom” profits. Depreciation is a non-cash accounting entry, but it represents the very real cost of equipment wearing out. By postponing that expense into later years, the tech giants created a flattering short-term picture. The risk is that those expenses eventually catch up to them. And indeed, cracks are already beginning to show.

Ironically, the same trend that encouraged longer useful lives – rapid tech improvement – is now making those lives too long. The last few years saw iterative improvements in cloud hardware efficiency, which justified some extension of server use. But the emergence of generative AI in 2023-2024, spearheaded by Nvidia’s powerful GPUs and specialized AI chips, has dramatically accelerated the hardware upgrade cycle. Suddenly, data center equipment from just a few years ago looks woefully outdated for cutting-edge AI workloads.

This puts the hyperscalers in a bind. They stretched their depreciation schedules, assuming hardware would actually remain useful for five or more years. Yet to stay competitive in AI, they must continue to replace and upgrade their equipment at an increasingly faster pace.

Now, those extended depreciation schedules are colliding with reality. Companies face the prospect of writing down equipment early or reverting to shorter lifespans, which would bring hefty expenses back onto the income statement.

Controversial computer algorithm helps you know when to sell your stocks before they crash…

Any day now, we could see the biggest financial bubble in history burst as investors realize that the Magnificent 7 stocks are overpriced, overhyped and completely unsustainable…

To find out more about the algorithm with the potential to help you save your family’s portfolio, click here.

Amazon Appears To Be Leading This Shift… Again

Amazon’s latest earnings call suggests this reversal is already underway. After years of extending its depreciation schedules, the company announced that it is now decreasing the useful life of certain servers and networking gear from six years back down to five years, effective January 2025.

Why? Because of “an increased pace of technology development, particularly in [AI and machine learning],” according to CFO Brian Olsavsky. In plain English, new AI chips are coming so fast that some hardware will need to be replaced sooner than they previously expected.

This reversal will hurt Amazon’s earnings. The company expects 2025 operating income to decrease by approximately $700 million due to higher depreciation expense. And that follows a $920 million impairment charge Amazon took last quarter for accelerating depreciation on equipment it had retired early.

The message to other hyperscalers is loud and clear. Amazon has officially admitted that some servers it originally planned to use for six-plus years simply won’t survive that long in the age of AI. And as technology continues to advance, we suspect useful lives will continue to contract.

So far, the other hyperscalers haven’t publicly reversed their depreciation extensions, but they are clearly watching.

For example, Meta’s recent change to 5.5 years explicitly excluded its AI-specific servers, which appears to be a tacit admission that they have shorter lives. This suggests Meta is wary of pushing the envelope too far. If AI demands force it to retire regular servers earlier, the company could eventually face the same choice as Amazon.

Microsoft and Alphabet are further behind the curve here. Both are still depreciating much of their equipment over six years as of the latest quarter. Meanwhile, both – along with Amazon and Meta – are continuing to pour massive amounts of capital into AI data centers. And a lot of that spend is for cutting-edge hardware that will likely not have a six-year useful life.

Eventually, Alphabet and Microsoft will capitulate as well… and when they do, investors will likely see a wave of depreciation charges hitting the companies’ income statements, reversing some of the phantom profits they’ve heralded since 2021.

A Valuation Reality Check

We’ve noticed a growing consensus in the financial media that these tech giants are currently trading at cheap valuations following the recent market correction. Given this backdrop, let’s look at how “cheap” these hyperscaler stocks really are.

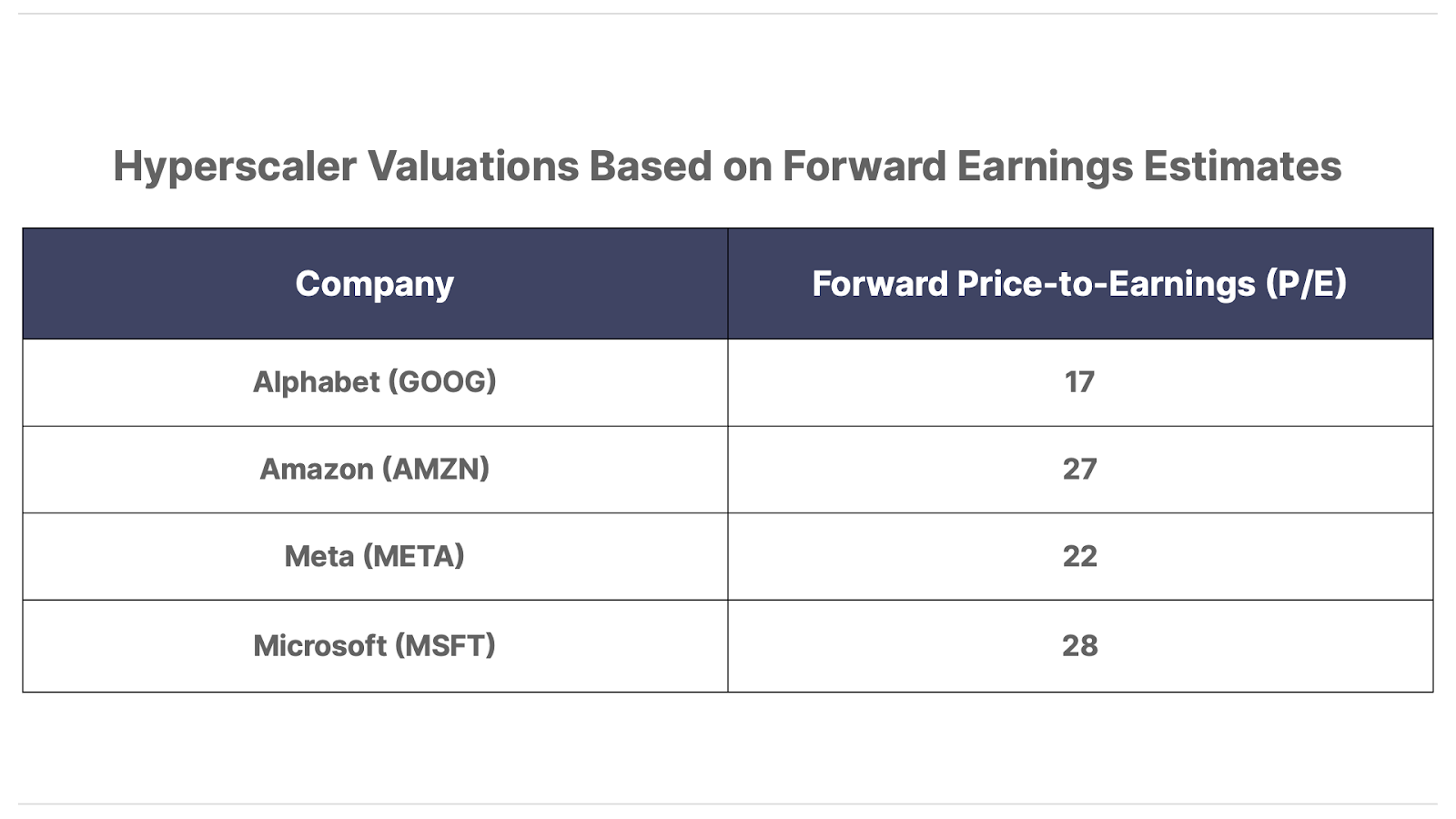

It’s true that on a forward price-to-earnings (“P/E”) basis, these stocks don’t appear unreasonably priced.

However, if those earnings have been partially inflated by accounting quirks (like lower depreciation) – and may be at risk of normalizing – the P/E multiple alone might not be telling the entire story. Earnings multiples also tend to ignore the heavy capital spending and dilution (via stock-based compensation) these companies increasingly rely on to produce those earnings.

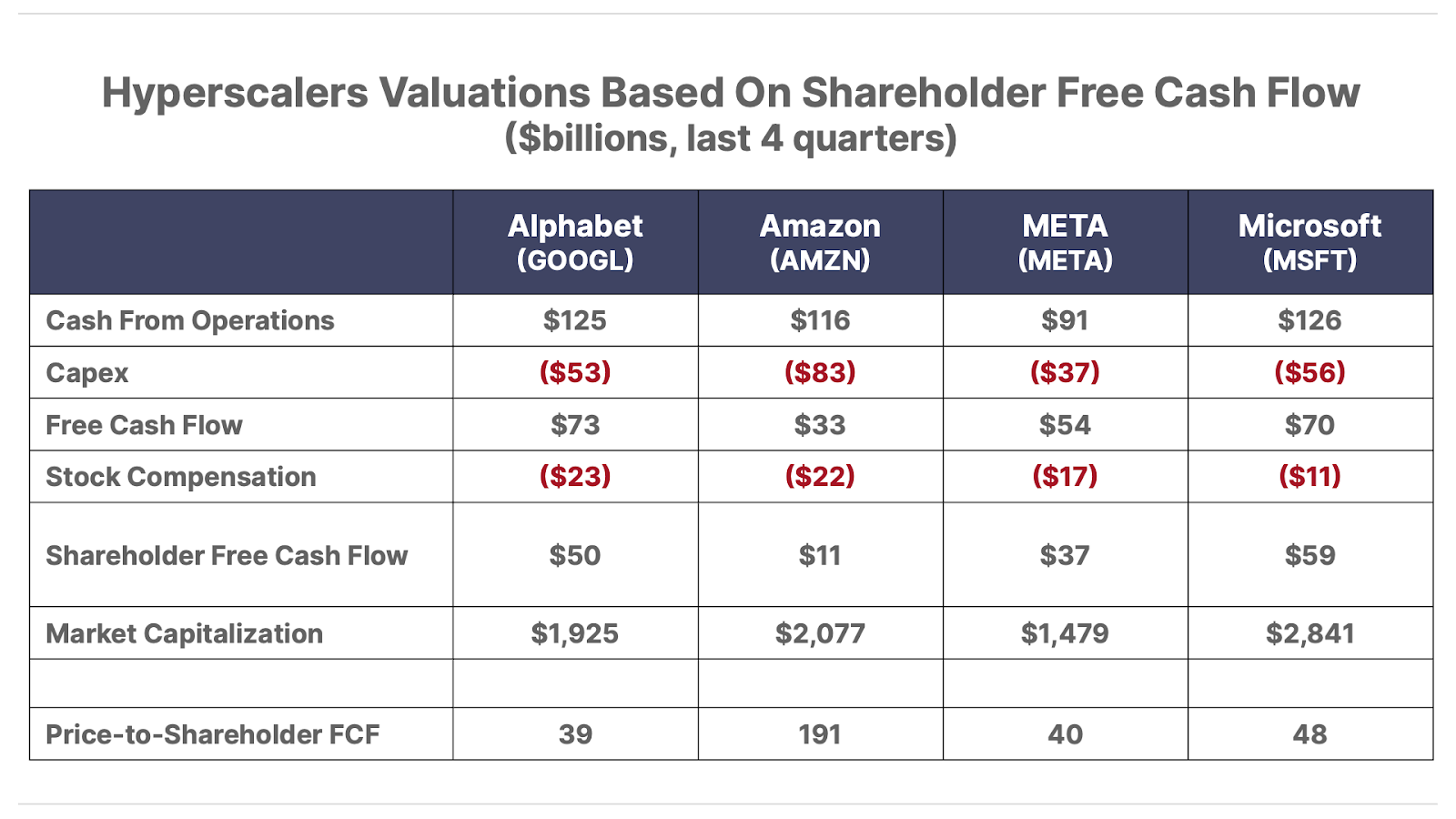

A more balanced view comes from looking at free cash flow, which isn’t impacted by depreciation changes like earnings can be.

When valuing hyperscalers, we’re particularly fond of a metric we call “shareholders free cash flow,” which is simply the amount of cash flow left over for shareholders after accounting for capex and stock-based compensation. (The standard free cash flow computation accounts for the former, but not the latter.) And when using this metric, these stocks look quite different.

Paying 40x to 50x cash flow is not cheap at all – in fact, it’s reminiscent of late-1990s tech multiples. And if the market shifts to valuing these companies on actual cash generation rather than rosy earnings, their current stock prices could easily be cut in half or worse

Finally, there’s also a risk that extends beyond just these four hyperscalers. These companies’ race to build AI infrastructure has been a boon to chipmakers – Nvidia foremost among them. Shares of Nvidia began to soar in 2023 as it became clear the Big Tech firms would spend almost indiscriminately on AI hardware. Indeed, Nvidia has been the one Magnificent 7 company – which also includes the four hyperscalers above, along with Apple (AAPL) and Tesla (TSLA) – that is clearly benefiting from the AI boom in terms of surging sales and profits.

But here’s the catch: Nvidia’s gains have come mainly from its largest customers – Amazon, Microsoft, Alphabet, and Meta. Those companies are Nvidia’s biggest GPU buyers, and they’ve been plowing billions of dollars into AI equipment, even as it strains their cash flows.

If these hyperscalers start to feel earnings and cash flow pressures – whether due to depreciation costs coming back or simply investor demands for financial discipline – their appetite to pour hundreds of billions of capital into AI data centers could diminish.

In other words, Nvidia’s remarkable growth could slow if its top customers decide to tighten their belts. Already, both Microsoft and Meta have faced tough questions from investors about sky-high AI spending in late 2024. And a more disciplined stance by even one or two of these giants would translate into significantly lower sales for Nvidia.

Porter & Co.

Stevenson, MD

This content is only available for paid members.

If you are interested in joining Porter & Co. either click the button below now or call our Customer Care team at 888-610-8895.