Issue #7, Volume #2

And Everyone Is Wrong

How Emotions Drive The Market

This is Porter & Co.’s free e-letter, the Daily Journal. Paid-up members can access their subscriber materials, including our latest recommendations and our “3 Best Buys” for our different portfolios, by going here.

Three Things You Need To Know Now:

1. America’s 47th president is set to race out of the gate. Donald Trump today was inaugurated as the new – for the second time – president of the United States. Trump is said to have in the works a flurry of executive orders on immigration, federal worker status, and energy. His first major challenge, though, comes on Tuesday, when the U.S. government hits its debt limit – when the Treasury Department will have to start to take extraordinary measures to pay its bills (as the debt load continues to escalate… see below…).

For months, the “Trump trade” – that is, the assets that will most benefit from the policies of the new administration – discussion has been talking head fodder. The U.S. dollar will do well… Tesla is a buy… sell China… and so on. But thanks in part to Porter’s close connections in the new White House, here at Porter & Co. we have a unique perspective on a handful of stocks – chances are you’ve never heard of them – that are set to rise with the start of the new presidency (one is already up 50%… but is just getting started). If you’re already a Big Secret subscriber or a Partner Pass member, you can access our report, here… and if you’re not, find out more by watching Porter’s special presentation, here.

2. A pre-inauguration coin toss. On Friday night, January 17, as many in the cryptocurrency industry gathered in D.C. for a pre-inaugural Crypto Ball hosted by Trump’s Crypto Czar David Sacks, Trump (or someone close to him) quietly launched a crypto memecoin. Over the next 36 hours, $TRUMP rose from an initial price of $0.18 to as high as $75.83, a gain of over 42,000%, with a peak market cap of $75 billion – greater than that of more than half the companies in the S&P 500. Trump’s team then launched a second memecoin yesterday – $MELANIA, named after the First Lady – which reached its own peak valuation of $13 billion (and which caused $TRUMP to fall around 40%, before partially rebounding). With roughly 80% of the supply of both coins reserved for their creators (presumably Trump and his team) and just 10% available to the public, these moves appear to be a backdoor way for the project’s instigators to create enormous wealth (around $60 billion at current prices) for themselves.

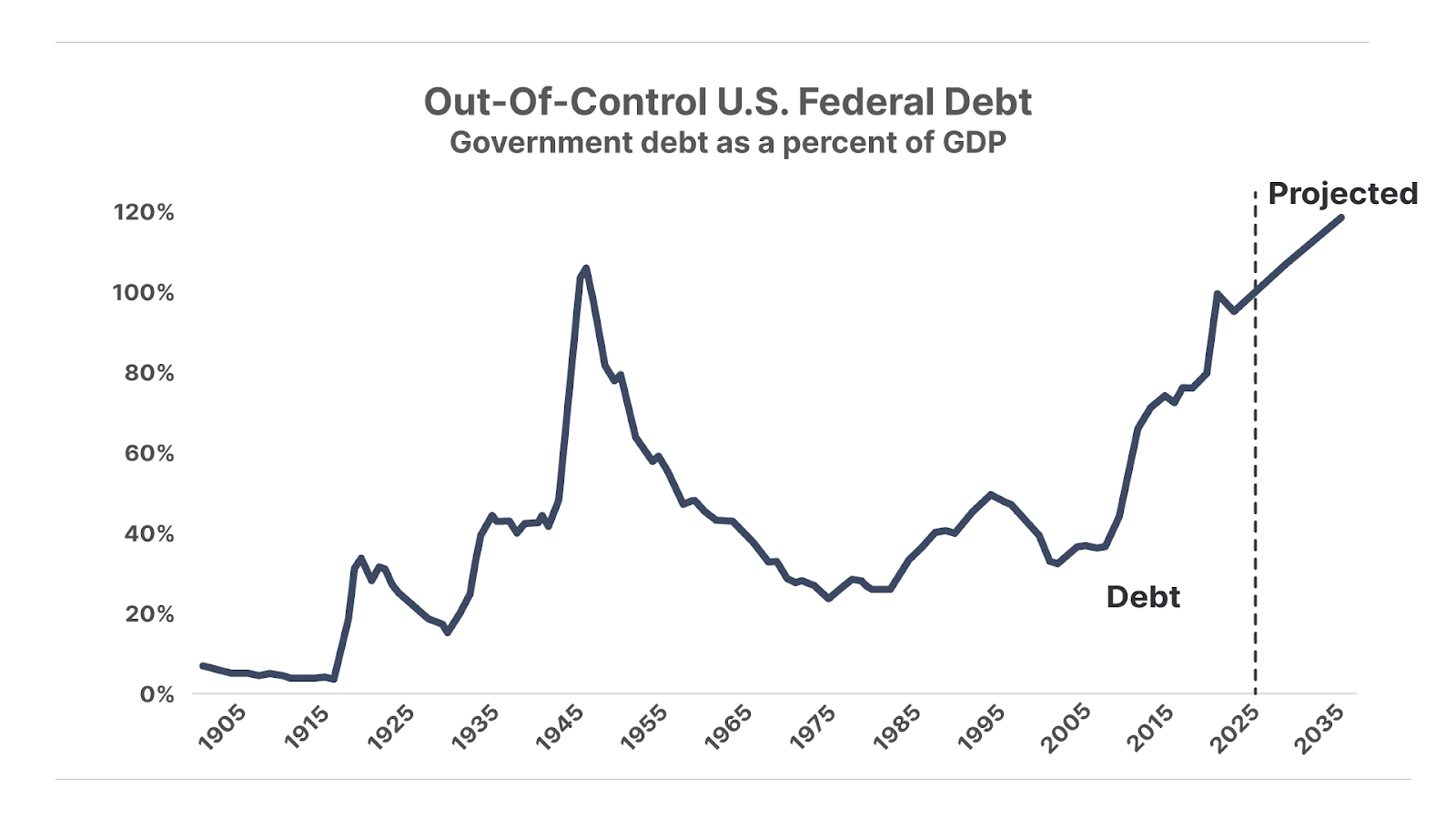

3. Budget office paints dire picture of Uncle Sam’s finances. Despite promises of a leaner government under the Trump administration, the Congressional Budget Office’s latest forecast projects the federal government will add a staggering $22 trillion in debt over the next 10 years. The vast majority of this new debt will come from mandatory spending on Social Security, Medicare/Medicaid, and interest expenses. The Department of Government Efficiency (“DOGE”) has its work cut out for it.

And one more thing… Coming Up This Week:

A four-day week packed with earnings. After markets were closed for Martin Luther King Jr. Day today, watch out for two big data releases on Friday: first, the S&P Global Manufacturing/Services PMI data, likely to show further global economic growth for December, with the index expected to give its highest reading in four months. Also on Friday, we’ll get December existing home-sales data: in November, sales were up 6.1% from the year prior, the biggest year-over-year gain since 2021’s post-COVID buying spree. Home sales are historically weaker in December, but Federal Reserve rate cuts may mean that November’s stronger sales continue.

Also on tap are Q4 earnings from about 10% of S&P 500 companies, including Netflix (NFLX), Johnson & Johnson (JNJ), American Express (AXP), and a score of big banks.

In Case You Missed It…

Last week, in The Big Secret, we released our first recommendation of 2025… a capital efficient company whose years of investing in growth has begun to turn a profit, with shares now poised to move higher… If you are not yet a Big Secret subscriber, click here to find out how to see last week’s recommendation, the full portfolio, and all the archives.

In Wednesday’s Daily Journal, Porter wrote about President Donald Trump’s idea of creating an External Revenue Service. Says Porter: “A president threatening to set up a second revenue agency for the federal government isn’t good news. It’s horrifying”… Readers mostly agreed – sending in a blast of emails that we published in Friday’s Journal.

And in Distressed Investing this week, Marty Fridson and his team will provide a market update – looking back at the past year of distressed debt – and a portfolio review, showing 10 of the 14 open positions in the green for a total portfolio return of 25.4%… To learn more about Distressed Investing, contact Lance James, our Director of Customer Care, at 888-610-8895, or internationally at +1 443-815-4447.

Today’s Poll… Where Will The S&P 500 Be At The End Of Trump’s Second Term?

The S&P 500 rose 69.6% from when Donald Trump started his first term as president to when he left office in 2021, and the index rose 55.7% from the beginning of Joe Biden’s four years until today. So now we ask…

At The Peak Of The Cycle, Everyone Is Bullish –

And Everyone Is Wrong

How Emotions Drive The Market

The stock market is cyclical.

The boom of the 1920s – 25% a year from 1922 until 1929 – gave way to the Great Depression.

In nominal terms (before inflation) stocks only went up 3.2% a year between 1930 and 1949. Including the impact from inflation, an investor didn’t produce any gain in stocks from the peak in 1929 until 1954 – 25 years.

Then, in the early 1950s, extremely low stock prices and zero investor interest in the stock market, led to a new boom. Stocks would go up 14.1% annually between 1950 and 1966.

You know what happened next: high valuations (cyclically adjusted P/E (CAPE) ratios in the mid-20s) and extraordinary growth assumptions led to another bust. On February 9, 1966, the S&P 500 closed at a then-record 94.06. More than 16 years later, on August 12, 1982, it stood at 102.42… just 9% higher.

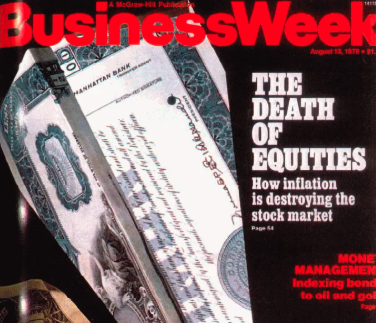

Stocks, accounting for inflation, wouldn’t produce a real return until 1984, an 18-year lull. Investors were so pessimistic, many people believed there would never be a bull market, ever again. BusinessWeek declared “The Death Of Equities” in 1979.

But, once again, low valuations and weak sentiment led to another long boom in the stock market – 15.7% annual growth between 1982 and 1999!

You’ll never guess what happened next…

Outrageous expectations and high valuations led to a long bear market, featuring a maximum drawdown of 60% (!) and zero net real returns for almost 15 years.

Simple question: where do you think we are in this cycle today?

For the last 15 years, since early 2009, stocks have gone up 12.6% a year. Stocks are now trading at the highest CAPE ratio of all-time, except for the year 2000 bubble and the 1844 great railroad bubble – CAPE is the Cyclically Adjusted Price-to-Earnings (P/E) ratio of the S&P 500… it compares the market value of every stock in the S&P 500 to the net income of those businesses, on average, and adjusted for inflation, over the previous 10 years.

The current nominal P/E ratio is 28.7. This is the most expensive P/E ratio I’ve seen in my lifetime.

Sentiment is now so incredibly bullish that even meme coins that are explicitly and conspicuously absent of any intrinsic value (Fartcoin, for example) have seen investors bid their prices up to tens of billions.

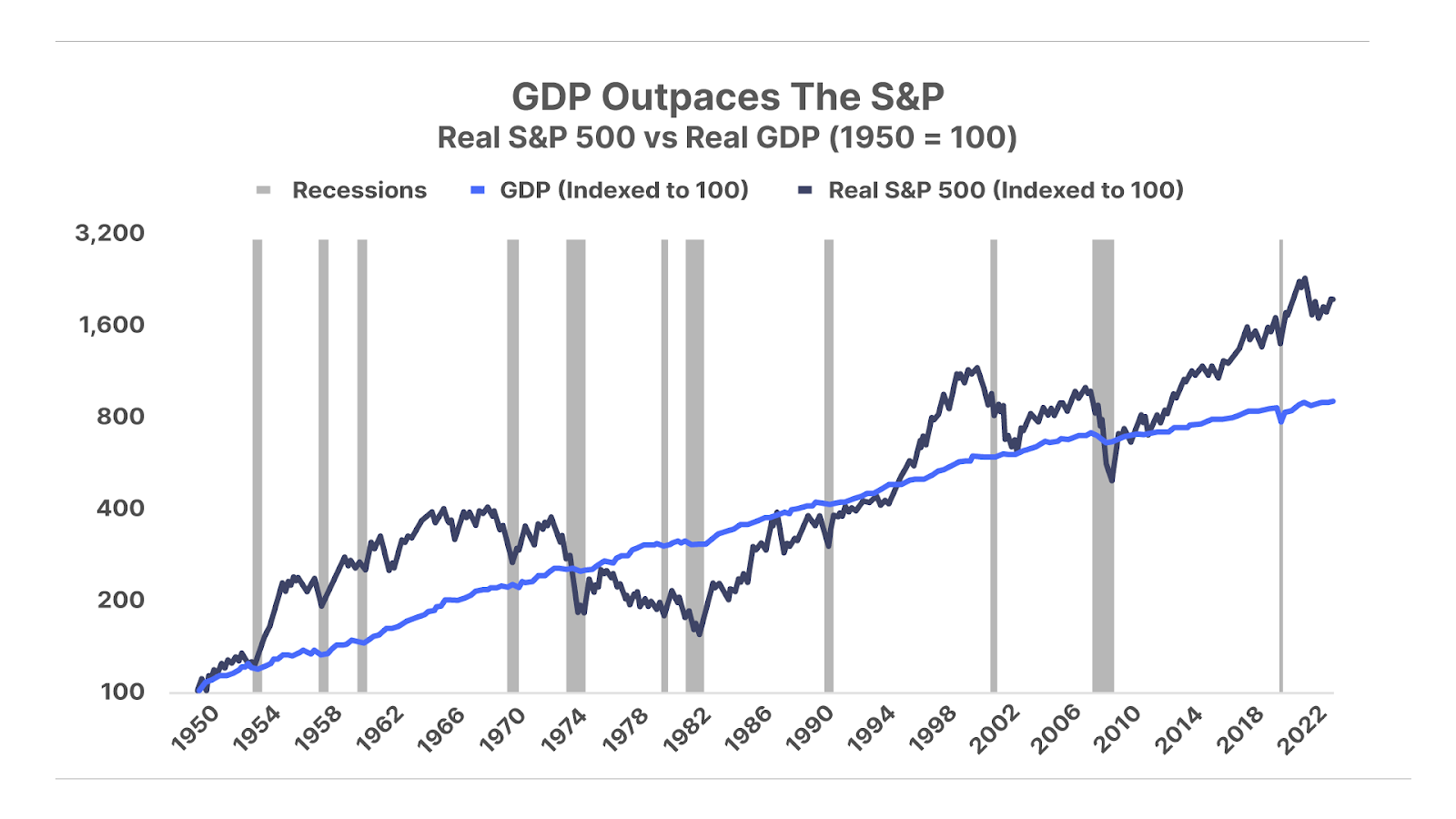

How could this happen, again and again and again? It’s not the fault of the economics. The economics of this situation could not be more clear: corporate earnings cannot grow substantially faster than GDP.

There is no way for all the horses to win more money in the race than the bettors have put into the pot. Most sixth graders would understand this concept because it is blindingly obvious. But investors? Nah – this time is different!

At the current record level of valuations, it is virtually certain that investors buying the S&P 500 – especially the largest and most overvalued stocks – will be woefully disappointed as future returns for at least the next decade will be poor.

Why do investors consistently drive the market forward in these waves of extreme speculation? Nature taught man to recognize patterns. And man’s nature evolved to maximize his emotional responses to those patterns – and to always stay with the herd where it was safe and warm. People seeing the market continue to go higher and higher, year after year, become trained to fear missing out on future gains far more than they fear the loss of their capital. And so the bubble builds.

And, for professional investors, at the top of these market cycles, clients end up demanding that they stay fully invested, or else they will withdraw their capital and invest in the funds that promise to take such risks.

Jean-Marie Eveillard was one of the greatest investors of the last 50 years. He managed the SoGen International Fund (now the First Eagle Fund) from 1978 until 2004. He sold out of Japan in 1988 – just before its bubble collapsed. “Everything was atrociously expensive and accordingly we didn’t belong there anymore.”

By the end of 1997, Eveillard had compounded his fund by more than 16% a year since 1978 – and he never lost money. Well, technically there was a 1.7% decline in 1990, but you get the point: Eveillard knew what he was doing. Few investors have ever produced results this good, for so long a period, in a long-only, unleveraged, stock portfolio. And no one has ever done so with less volatility.

And, because he knew what he was doing, he wouldn’t chase the tech stock bubble in the U.S. As U.S. stock prices became untethered from underlying economic fundamentals, just as he had done during Japan’s bubble, Eveillard famously left the market. By the end of 1996, he held only 22% of his fund in U.S. stocks (although they made up 60% of the global equity index). He held 23% in cash, with another 22% in safe bonds and gold.

In round numbers, he had almost 50% of the fund in things like cash, gold, and short-duration bonds that had firm values that could be converted into major currencies almost immediately. That was a huge “rainy day” fund and an unheard-of asset-allocation strategy for a mutual fund. But, despite this incredible handicap, his fund still appreciated by almost 20% in 1999!

And how did his investors react to his extreme conservatism and his astute risk control? They sold in droves to invest in tech funds at the market top.

Eveillard would lose fully half of investors between 1996 and 2000. “Everyone was abandoning us. But, as one of my partners said, I’d rather lose half of my shareholders than half of my shareholders’ money.”

As you know, U.S. stocks would fall sharply for almost three years from early 2000 until late 2002. Tech stocks declined by more than 80%. And the S&P 500 fell by more than 50%.

Meanwhile, for the five-year bubble period between 1998 and 2003, Eveillard would compound his fund at more than 10% annually.

In 2002 he was named Morningstar’s best-performing manager among 372 diversified global mutual funds. At the end of his career in late 2003, he received the Morningstar Lifetime Achievement Award.

Investing isn’t hard.

It’s managing your emotions that’s so tricky.

Good investing!

Porter Stansberry

Stevenson, MD

P.S. There are always nuances to these big cycles. All of the data above are correct – but they’re measured using the S&P 500, which only tracks the largest 500 companies and is market-cap weighted, which means, the more overvalued a stock becomes, the larger its impact on the index. And that means the S&P 500 Index is most strongly impacted by these kinds of market cycles. But that doesn’t mean that all stocks should be avoided. For example, value stocks continued to compound at 13% a year from 1966 through 1982, while the S&P 500 earned nothing. The lesson? Don’t buy expensive stocks late in the cycle.

Mailbag

Glad you’re keeping busy penning letters again. I’ve been reading your work since 2007 when I made my first investment at just 19.

You are not an ass hole. Mostly.

Thanks for years of interesting insights and keep up the great work.

Matt K.

Good day.

I love to read your articles on investing, which are intelligent, well-written, short and concise, and full of great ideas. “How To Survive A 10-Year Bear Market” is such. I don’t have a lot of investment knowledge and when I read your articles I realize how important it is to have great investment advice such as yours!

Bill S.