The Last Time This Happened, Readers Tripled Their Money In a Year

Gold Is Way Up, the Miners Will Be Too

As longtime readers know, for decades now, Porter has recommended investing in high-quality, capital efficient companies as the surest path to wealth in the stock market.

However, in the summer of 2015, Porter encouraged his readers at Stansberry Research to “break the rules.”

Specifically, he recommended they sell some of those high-quality stocks – and invest that capital in what has traditionally been one of the lowest-quality and least capital efficient industries in the world: gold mining.

At the time, the entire precious metals sector was in the midst of a brutal bear market. Gold itself had lost more than 40% of its value over the previous few years. Gold stocks had performed even worse, with the benchmark NYSE Arca Gold BUGS Index (HUI) falling more than 80% and trading at historically cheap valuations – on both an absolute basis and relative to the price of gold and equities.

Given this setup, Porter believed that “mean reversion” in gold stocks was inevitable. He explained the concept in the July 24, 2015, issue of the Stansberry Digest…

As every investor knows, nothing goes up forever…

Every investor who lived through the 1987 market crash, Russia’s 1998 default, the tech wreck of 2000-2002, or the mortgage debacle of 2008 knows that every six to 10 years, something goes awry in the stock market.

It’s obvious. It’s common sense. Trees don’t grow to the sky. Sooner or later, the market “reverts to the mean.”

Just like stocks don’t go up forever, they don’t go down forever, either. Sooner or later, financial markets form a bottom. Sooner or later, the correction or bear market creates such value that it attracts new buyers. And sometimes, for no apparent reason at all, stocks will suddenly shoot higher.

[My friend Meb Faber, the chief investment officer of Cambria Investment Management] decided to study both whole countries (with an investable stock market) and asset classes (types of investments) to determine if they showed any obvious or tradable pattern. What he found is interesting…

Meb studied five major stock markets from 1903 until 2007. He wanted to know what stock prices did on average in these markets after falling for three consecutive years. He discovered that in major stock markets, share prices didn’t often fall three years in a row. Three consecutive years of lower prices almost never happened – those instances occurred less than 3% of the time.

But when markets fell three years in a row, the following bull market was extremely powerful. The average return in stocks during the fourth year was more than 30%. That’s a significant result, something that wouldn’t happen by chance. This big move higher is caused by reversion to the mean, not chance.

When Meb studied asset classes, he found similar numbers. After three years in a row of declining equity prices, the average return in the fourth year was 34%, almost three times higher than the average return of all the years in the study. Again, statistical analysis tells us these are meaningful results, not just chance. They’re proof of mean reversion in equity prices. Buying markets and asset classes that are down three years in a row is a rare and valuable speculation.

History suggested it was simply a matter of time before gold stocks experienced a dramatic share-price rebound, and Porter urged readers to establish a position. More from that issue…

I’m 100% certain that eventually, this downward trend will reverse. And I know that when that occurs, the resulting price increases will be dramatic. I believe average gains in excess of 250% are likely.

Investors smart enough to “hedge” their exposure to the U.S. stock market by establishing a “toehold” in the highest-quality gold and junior gold-mining stocks will likely be far more successful over the next three to five years than investors who don’t…

[What] I recommend that you do is sell about 10% of your existing portfolio… With this 10% of your portfolio, identify eight to 10 gold stocks that you’re certain will be in business five years from now.

Focus on high-quality business models (like royalty companies) and companies with high-quality balance sheets. Focus on great management teams. Buy these eight to 10 names on days when gold gets kicked lower and the stocks sell off even more. Learn to enter “stink bids” – limit orders that are 5% to 7% below the market price. You’ll be surprised how often those bids will get filled in a weak market.

Build this portfolio patiently over the next six months. Be a buyer this fall when other investors are selling for tax-loss reasons. That’ll be the bottom.

As it turned out, Porter was exactly right. The HUI gold index continued to drift lower over the next six months. It finally bottomed in early January 2016, and started to rocket higher almost immediately.

By that August – just over one year after Porter’s recommendation – gold stocks were trading 188% higher. And just as Porter predicted, over the next five years, the HUI would soar more than 250% – easily beating both the S&P 500 (up 64%) and tech-focused Nasdaq 100 (up 143%) over that period – with the best individual gold stocks doing even better.

History Is Rhyming

We don’t share this story simply to tout Porter’s track record. Rather, today – roughly a decade since Porter made this big gold-stock recommendation – we see another huge opportunity in this space. In fact, this setup could prove to be even better than the last one.

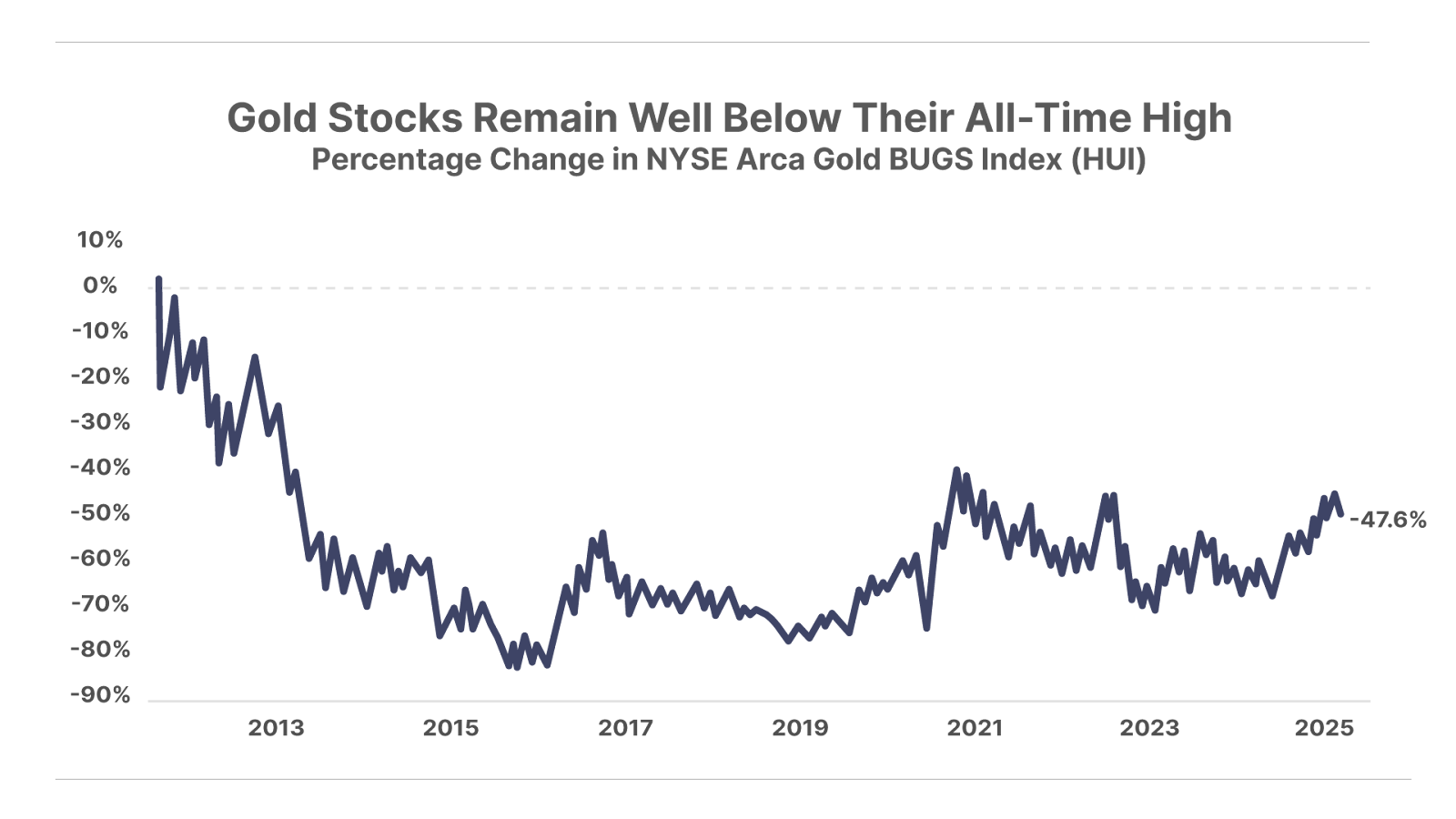

Like in 2015, gold stocks have suffered a brutal bear market over the past few years. The HUI lost as much as 50% of its value after prices peaked in the summer of 2020, before beginning to rebound over the past several months.

It’s also worth noting that despite the big rally in gold stocks between 2015 and 2020, the HUI remains nearly 50% below its all-time high made in late 2011, as well.

And, like in 2015, gold stocks are again trading at extremely cheap valuations.

According to analysis by top natural-resources research firm Goehring & Rozencwajg, at the gold market bottom in 2015, the five largest gold miners in the HUI – Newmont (NEM), Agnico Eagle Mines (AEM), Barrick Gold (GOLD), Gold Fields (GFI), and Harmony Gold Mining (HMY), which together account for more than 40% of the index – had 275 million ounces of proven reserves and a combined enterprise value of $40 billion. That represents a valuation of roughly $150 per ounce of proven reserves.

At the time, that meant investors in these stocks could buy the equivalent of gold in the ground for just 12% of the spot price – roughly half the previous record low valuation of 23% of the spot price, set in 1999.

At their lowest level earlier this year, these companies were valued at just $292 per ounce of proven reserves. That’s twice as high as the 2015 level. But based on the gold price earlier this year – just over $2,400 per ounce – this again represented 12% of the spot price at the time, just like in 2015.

Likewise, at the 2015 bottom, these stocks traded at just 0.70x their net asset value (a common miner valuation metric based on a discounted cash flow model). For reference, at the previous bear market extreme in 1999, these stocks still traded at a premium to their net asset value (1.8x).

Today, even after the recent rally in gold stocks this year – up 29% since January 1 – these companies still trade for less than 0.70x their net asset value – or even cheaper than they were at the 2015 bottom.

It’s a similar story when comparing gold stocks to the overall equity market and gold itself.

For example, at the 2015 bottom, the collective market capitalization of gold miners in the HUI was roughly $55 billion, just under 0.50% of the total market cap of the S&P 500.

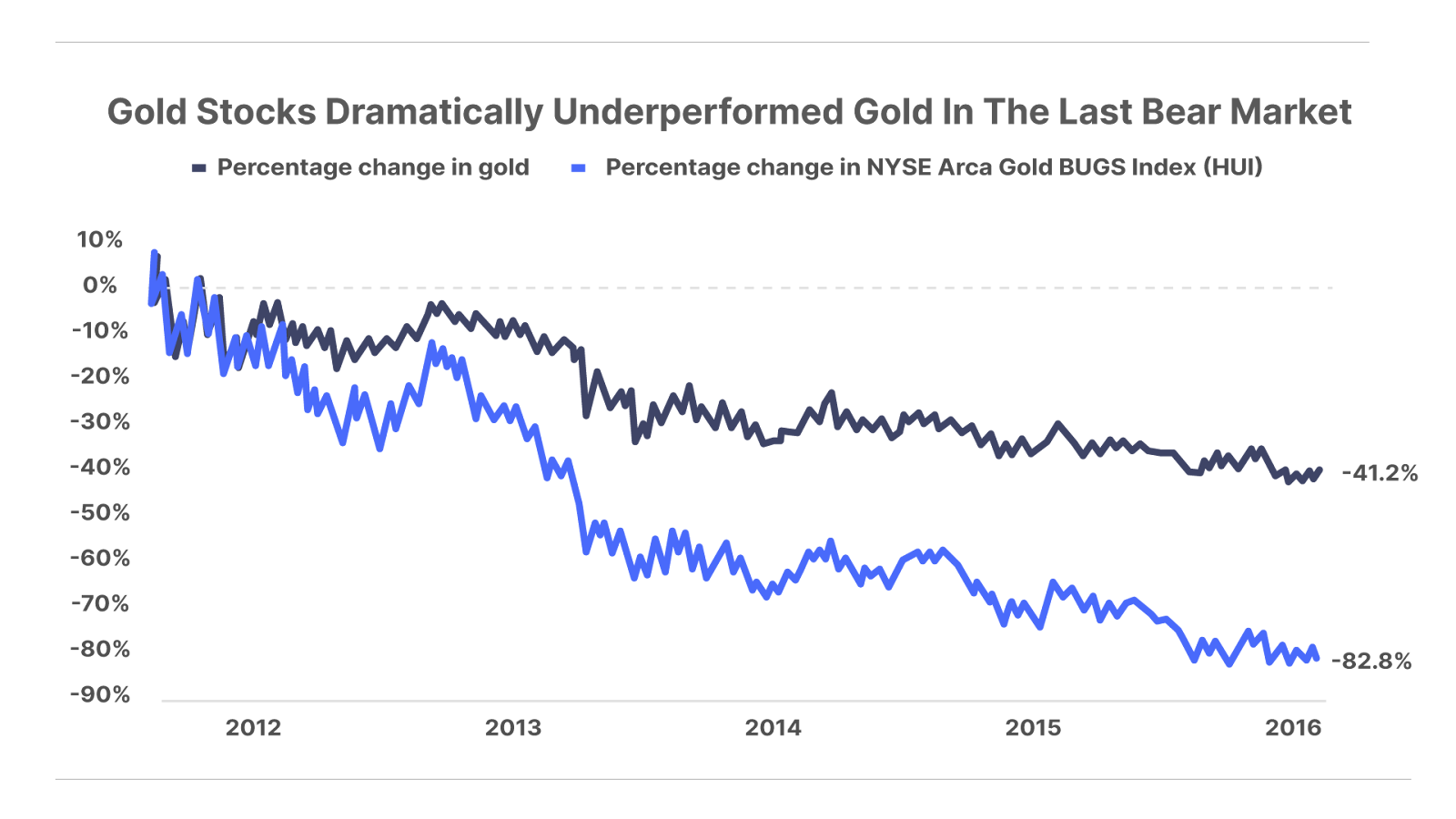

HUI had also underperformed the price of gold by a little over 41 percentage points (down 82.8% versus gold down 41.2%) since the precious metals market peak in late 2011.

Today, even after the rally this year, HUI is currently trading at roughly 0.50% of the total market cap of the S&P 500.

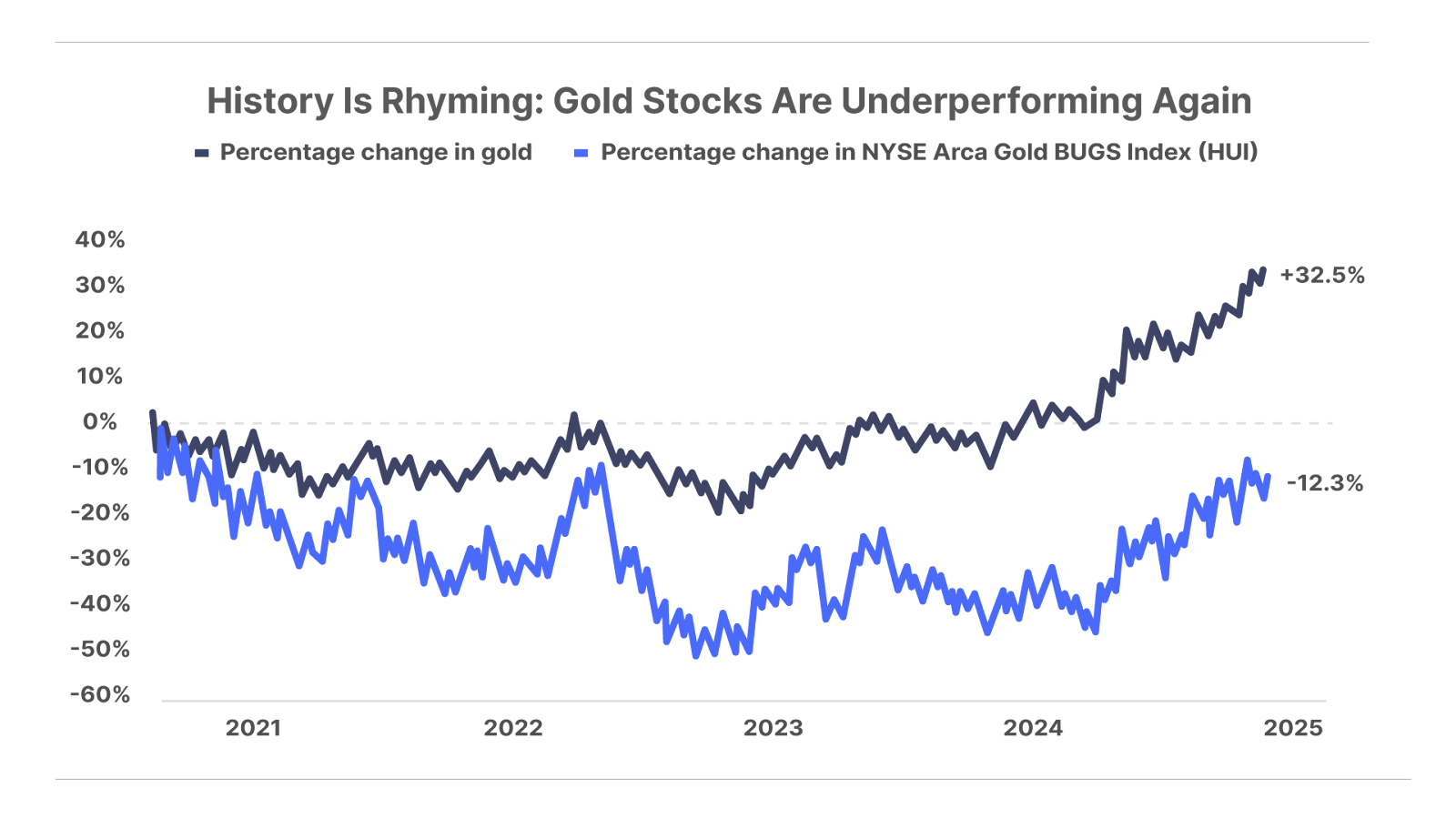

Meanwhile, these gold stocks have again underperformed gold since the previous precious metals peak in late 2020, this time by nearly 45 percentage points.

In other words, on both an absolute and relative basis, gold stocks are currently as cheap – or cheaper – than they were when Porter recommended them in 2015.

How This Time Is Different (In One Important Way)

However, there is one important difference between the setup in gold stocks in 2015 and the setup today. And that has to do with the behavior of gold itself.

In short, in 2015, gold had also suffered through a serious bear market. Though its price held up better than gold stocks, gold fell more than 45% between September 2011 and January 2016.

That isn’t the case this time.

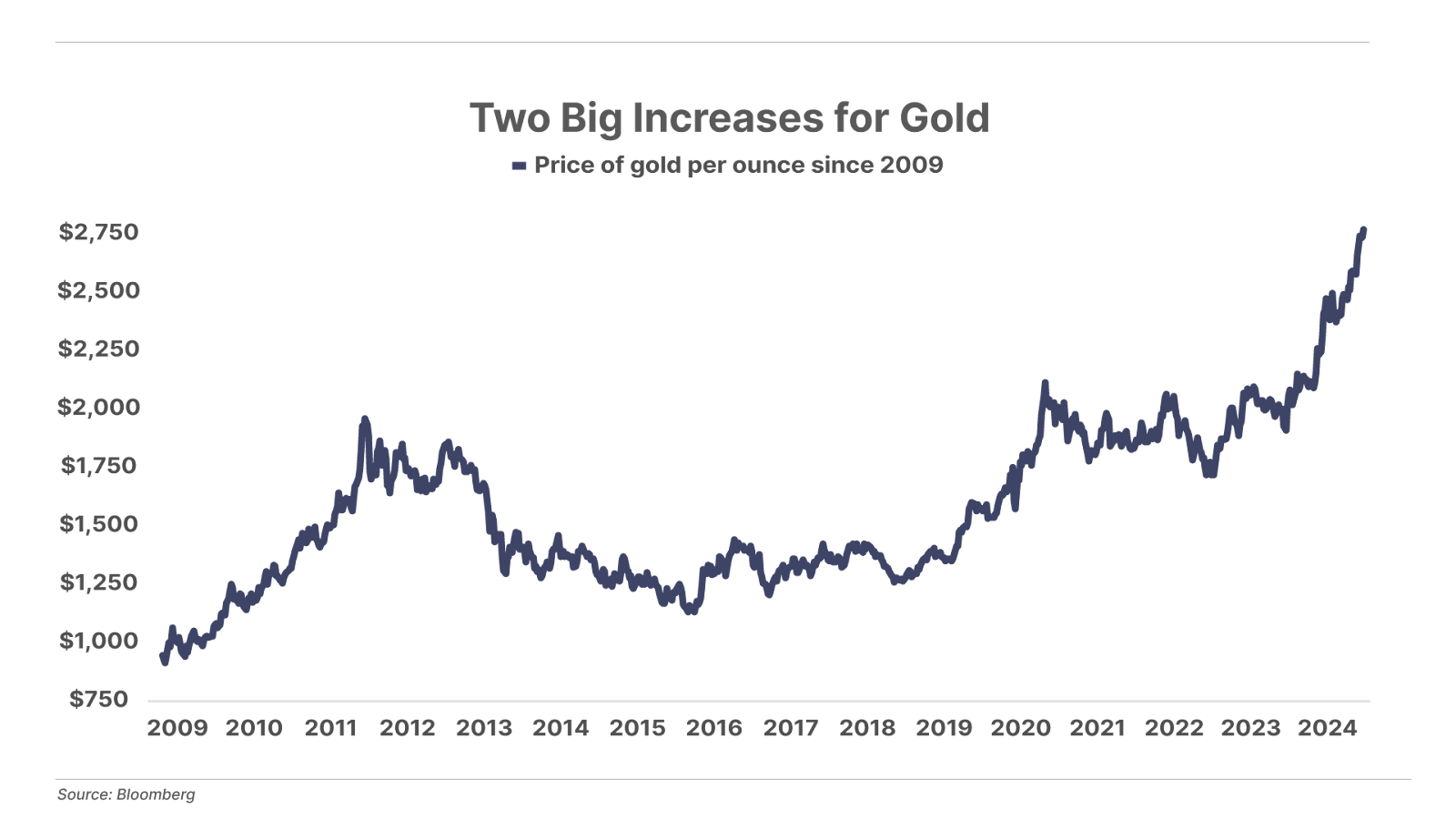

Today, gold is already in a bull market. While gold stocks are trading below both their 2011 and 2020 highs, the price of gold is more than 30% above those prior highs and just made an all-time high today, nearly reaching $2,700 per ounce.

This disconnect is unusual, and most likely due to the intersection of two divergent factors.

The first is interest rates.

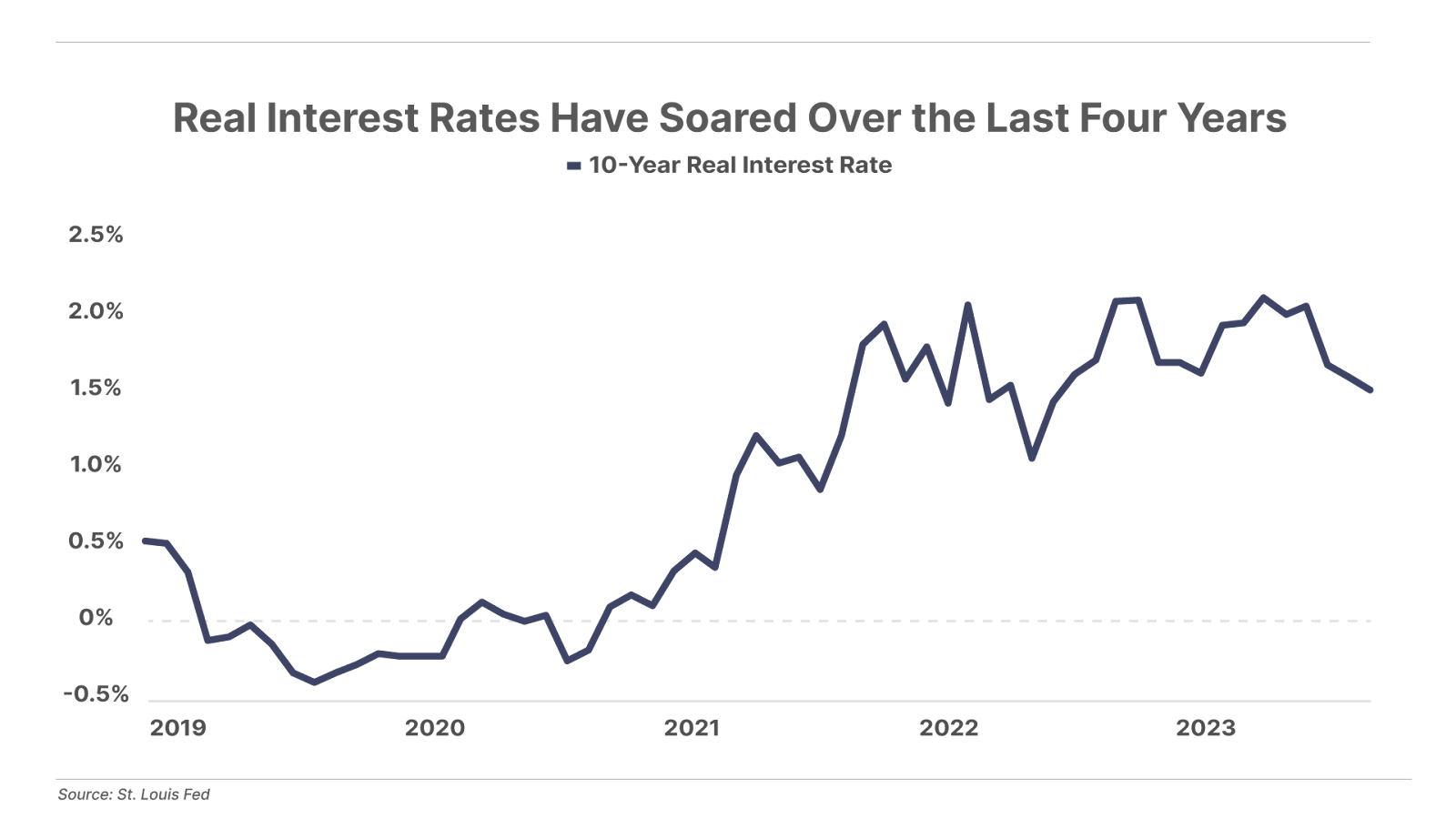

Gold has historically traded inversely to real interest rates (that is, the actual rate of interest after accounting for inflation). Because gold yields nothing, it tends to perform best when real rates are negative or falling (and investors aren’t being properly compensated to hold cash), and it tends to struggle when real rates are positive or rising.

As shown below, 10-year real rates have risen from negative 0.40% in 2020 to as high as 2.1% this year.

Given this historical relationship, we would expect many investors would’ve sold gold over the past few years to take advantage of the higher yields available in cash. And data suggest that is exactly what happened.

Gold exchange traded funds (ETFs) saw outflows equal to 25% of their holdings between 2020 and 2024. And the largest gold stock ETF, the VanEck Gold Miners ETF (GDX), saw outflows representing nearly 20% of its assets over the same period.

The second factor influencing the gold price recently is central bank buying.

While retail investors have been selling gold, central banks have been buying huge amounts of gold for the first time in decades. This is largely a consequence of two recent events: the U.S. confiscation of Russian reserves following its invasion of Ukraine in 2022, and soaring U.S. government deficits.

The confiscation of Russian funds showed foreign buyers of U.S. Treasury bonds that final ownership of these assets is ultimately at the discretion of the U.S. government. Meanwhile, ever-escalating U.S. deficits suggests that those Treasury bonds are virtually guaranteed to lose significant value in real terms (after inflation) in the years ahead.

As a result, foreign central banks have been buying gold as a primary reserve asset in lieu of adding to their existing U.S. Treasury holdings.

Estimates suggest central banks have bought more than 100 million ounces of gold since 2020, dwarfing the sales by retail investors over that period and helping push the price of gold nearly 100% higher.

Unlike retail investors, central bank buyers are only interested in physical gold – not gold miners – which has helped drive today’s historic divergence.

However, as deficits continue to grow – and the yield on cash falls as the Fed cuts rates – it’s simply a matter of time before “mom and pop” investors become interested in owning gold again… and when they do, historically cheap gold stocks could soar like never before.

Paid-up subscribers to The Big Secret on Wall Street already have access to our top gold stock recommendation – a rare, capital efficient gold company that can give you gold mining exposure with far less risk than most mining stocks.

However, if you’re looking for more gold-stock exposure – including the more speculative junior mining companies that can soar hundreds or even thousands of percent in a gold bull market – you won’t find a better guide than veteran resource investor Marin Katusa.

Marin recently sat down with Porter to explain why he believes this gold bull market is just getting started… why his favorite junior gold stocks could soar 500% to 1,000% virtually overnight… and why he’s personally investing millions in two gold stocks in particular. Click here to learn more.

Mailbag

In The Big Secret on Wall Street mailbag, Porter answers letters from readers. He cannot offer individual investment advice, but can respond to general questions.

Please email us at [email protected] to have your questions answered. We’d love to hear from you!

Today’s letter comes from L.J., who writes:

How does the Permanent Portfolio differ from the stocks in The Big Secret on Wall Street model portfolio? Namely the Battleship Stocks and Forever Stocks. Also, if we already invested in these stocks should we divest and put the money into these stocks in Porter’s Permanent Portfolio?

Porter’s comment: The idea of a Permanent Portfolio is based on theories of Harry Browne, who was a legendary free-market economist, author, and two-time U.S. Libertarian Party presidential candidate. These ideas about asset allocation attempt to address the long-term negative externalities of our fiat-currency monetary system. This allocation strategy is designed to protect investors against the inevitable booms and busts of our inflation-driven economy, and thereby allow all investors to protect themselves from the long-term degradation of the U.S. dollar.

What matters then about this approach to investing isn’t so much which specific stocks are in the portfolio (in fact, as we explain in our report, investors can build a Permanent Portfolio with as few as four ultra-low-cost ETFs), but instead the allocations (25% stocks, 25% bonds, 25% gold, 25% cash) and the very long-term approach. The long-term approach is designed to minimize volatility, while achieving almost the same results as the overall stock market.

Just as Ray Dalio at Bridgewater Associates took these ideas and adjusted them based on his experience and worldview (including by adding leverage to juice the results in his Pure Alpha Fund), our team at Porter & Co. has taken Browne’s basic idea and attempted to make it even better, mainly by using property and casualty (P&C) insurance stocks rather than government bonds, and by including gold royalty companies, rather than gold bullion, and Bitcoin.

Likewise, rather than using the S&P 500, we’ve built a portfolio of high-quality, capital efficient “Lindy Forever Companies,” as we call them, that we believe will outpace the market over time. These are companies that have long, proven track records of success.

All of this comes with an important caveat. This is a “permanent” portfolio. If you want to set up a trust for your grandkids or if your heirs won’t know what to buy and hold after your death, this is a great portfolio approach to use. I wouldn’t worry about trying to match exactly the same stocks. If you have, for example, other insurance stocks already, then you can use them to build your permanent portfolio. Again, the strategy isn’t about the particular businesses. It’s about the dynamics of these assets overall and how they relate to each other in a paper-money economy.

Why bother picking individual stocks then? Well, first because the P&C insurance ETF isn’t well designed, and our P&C recommendations in The Big Secret have trounced the ETF going back to 2012 when we began recommending these stocks. And secondly, because I believe (but can’t prove) that the Lindy Effect is real – that is, the longer a company remains in business, the more likely it is to continue to stay in business and perform well – and valuable and will allow us to select much better investments over the long term.

Currently in our Big Secret portfolio, we have a recommended list of stocks that we believe will produce good results in different categories. We rank all of those recommendations by risk 1-5 (with 1 being the least risky and 5 being the most) – so that you can build a portfolio that’s right for you. We offer Porter’s Permanent Portfolio as one example of how you might construct an ultra-high-quality, ultra-low-volatility portfolio that should serve you very well for decades to come.

Porter & Co.

Stevenson, MD

P.S. Next week, Porter will interview financial storyteller Michael Lewis – author of Liar’s Poker, The Big Short, Moneyball, and most recently Going Infinite about Sam Bankman-Fried and FTX – at the Stansberry Conference on October 21-22. Tickets to attend in Las Vegas are sold out. But access to livestream Porter’s discussion with Lewis – and the full lineup of other great speakers – can be purchased here through October 18 (that’s tomorrow).

From the comfort of your own home, you can watch – live, as if you were at the Stansberry Research Conference – great financial thinkers such as futurist and former OpenAI exec Zack Kass, market-analytics master Marc Chaikin, former Texas Gov. Rick Perry, baseball analyst Billy Beane, Retirement Millionaire editor Doc Eifrig, leading real-estate investor Ronan McMahon, and others. In addition to being able to watch live, you also get high-quality video files, summaries, and presentation materials that you can review at your convenience – over and over again… whenever you like…

Of course, the highlight of the conference, which you can watch live, is Porter’s discussion with author Michael Lewis on topics ranging from the bond world depicted in Liar’s Poker to what Lewis learned about crypto markets and what Sam Bankman-Fried was doing with FTX… and with Porter asking the questions, you know it will be a fascinating exchange. Go here to be able to watch Porter interview Michael Lewis, all the other speakers, and receive videos and notes from the entire two days.