Unless central banks and policymakers are willing to deal with a major credit crash, all roads lead back to lower interest rates and more money printing. That’s why we believe now is the time to safeguard your wealth from the demise of fiat currencies with the two ultimate stores of value.

This Debt-Free Mining Royalty Company Sits Back And Rakes It In

The Monetary Revolution Against the Dollar Will Not Be Televised

| Welcome to Porter & Co.! If you’re new here, thank you for joining us… and we look forward to getting to know you better. You can email your personal concierge, Lance, at this address, with any questions you might have about your subscription… The Big Secret on Wall Street… how to navigate our website… or anything else. You can also email our “Mailbag” address at any time: [email protected]. At the end of this issue, you’ll find our model portfolio and watchlist (which is also here) — as well as a “Best Buys” section, where we’ll briefly cover three portfolio names that we think you should consider buying first. Again… we’re excited that you’re with us…and we’re looking forward to a long and fulfilling relationship. If you’re not a member and would like to learn more, click here. |

William Simon was on a secret mission.

And his famously vituperative boss – President Richard Nixon – had made clear that failure wasn’t an option.

Simon, a former Salomon Brothers star bond trader, was no stranger to high-stakes pressure. But in his (inadvertent) role as Nixon’s secret agent, failure meant a lot more than a losing trade or a ding to his bonus – because he’d be negotiating with a government that had no problem cutting off people’s heads (or other body parts).

But it was far more than that: America’s national economic security depended on a clandestine four-day layover Simon would be making in Saudi Arabia, in July 1974.

The story started in the ‘60s, when President Lyndon B. Johnson went on a government spending spree. He radically expanded U.S. government social programs, including Medicaid and Social Security, and then poured even more cash into the Vietnam War. By the early 1970s, all that spending had created an inflationary firestorm.

Watching from the wings, foreign governments like France and Switzerland got spooked.

As part of the Bretton Woods agreement in 1944 that formalized the U.S. dollar as the global reserve currency, foreign governments holding dollars had the option to redeem the U.S. currency for gold. And as the U.S. dollar lost its value in the wake of LBJ’s spending – inflation broke above 2% in 1965 and went up in a nearly straight line to 6% by 1970 – they started cashing out… trading in pallets of dollars for bars of the yellow metal.

France was the first mover, announcing its intention to convert its U.S. dollar reserves for gold in 1965. In May 1971, West Germany exited the Bretton Woods exchange agreement. In June Switzerland redeemed $50 million in gold, and France withdrew $191 million in gold from the U.S. Treasury.

On August 15, 1971, LBJ’s successor, President Nixon, announced that his administration would “temporarily” halt the convertibility of U.S. currency into gold, in order to “stabilize the dollar.”

It didn’t work. And (spoiler alert) it wasn’t temporary.

Inflation soared from 4.4% in August 1971 to 12% December 1974, as the dollar continued its downward slide. Adding fuel to the inflationary fire, the Organization of Petroleum Exporting Countries (OPEC) – a cartel of Middle Eastern oil producers, led by Saudi Arabia, that at the time accounted for more than half of total global oil production – imposed an oil embargo on the U.S. and its allies for their support of Israel during the Yom Kippur war. The embargo sent oil prices up four-fold, and caused a crippling oil shortage and mile-long lines at gas stations around the country.

Without the backing of gold behind its currency, and rocketing oil prices, the U.S. economy went into free-fall. The economy contracted as inflation continued rising… and unleashed the sharpest decline in American living standards since the 1930s.

By July 1974, the stock market was in the midst of a 45% decline, with double-digit inflation and a 5.5% unemployment rate on its way to 9%. The dreaded “stagflation” was in full swing.

That’s where William Simon – former bond trader, learning-on-the-job Uncle Sam bureaucrat, accidental secret agent – came into the picture.

Simon had left his $2 million-a-year job at Salomon Brothers in 1971 when Nixon tapped him to be Treasury Secretary. At the time, Simon didn’t know that the position came with certain… extra duties.

At the height of “stagflation,” Nixon sent William Simon to Europe and the Middle East to press the flesh with the heads of governments.

But a four-day layover in Jeddah, Saudi Arabia, wasn’t on the official agenda. There, Simon had a straightforward but definitely not simple task: create the modern-day petrodollar system.

You likely won’t hear the petrodollar system discussed on “Morning Joe.” But it’s been at the center of both global economics and American foreign policy for the past half century…

Since the U.S. Treasury could no longer back the dollar with gold, Nixon wanted it to be supported by something almost as valuable in the industrialized world: oil. If oil was available from the world’s biggest oil producers only in exchange for greenbacks, there would be enormous sustained demand for the U.S. dollar.

Simon had to convince the Saudi king to exclusively accept U.S. dollars for payment in crude oil – and to push for the same “dollarization” of the oil trade among other OPEC nations.

The second key part of the deal would entail Saudi Arabia funneling its dollar profits back into U.S. Treasury bonds – providing a critical source of financing for ballooning U.S. deficits.

In exchange, America would supply Saudi Arabia with advanced weapon systems, and provide a de facto security guarantee in an implicit military alliance.

Simon left town with his body parts still attached. And it wasn’t long before the Saudis started to take only U.S. dollars for oil – and recycling their profits into U.S. Treasuries. By 1977, one out of every five foreign-owned Treasury bonds was held by Saudi Arabia. The rest of OPEC followed Saudi Arabia’s lead, further fueling demand for dollars.

The 1970s stagflation officially ended in 1980, when inflation peaked at 14.6%. And thanks in no small part to the global dominance of the U.S. dollar, the American economy – albeit with bumps along the way – thrived: From 1980 through last year, the size of the American economy grew roughly eight-fold (in current U.S. dollar terms), to just over $25 trillion.

But the marriage of convenience that Simon brokered is coming under unprecedented strain. And the pressure on the petrodollar is an underappreciated but vital element of the slow unraveling of the dollar’s dominance… fueled by – we’ve seen this movie before – inflation and the anticipated collapse of a debt bubble.

The Fed Has No Choice – It Must Restart The Money Printer

The last decade of zero percent interest rate policy (ZIRP) has infected the American and global financial system with trillions of dollars in assets that only work at rock-bottom interest rates. That is… the meager rates of return on investments made with free money are no longer sufficient in a higher interest rate (and inflation) environment.

As we wrote on March 15, in The SVB Crash Was Just The First Domino:

“… regulators spent the last decade safeguarding against every possible downside scenario, except the one that actually happened: trillions of dollars of low-yielding assets running headlong into a sharp rise in interest rates.”

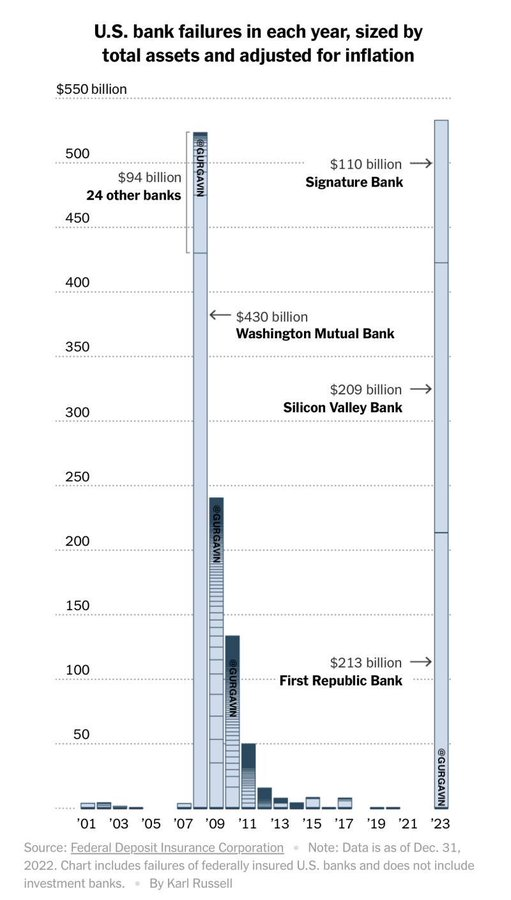

The era of ZIRP filled the global financial system with ticking time bombs, and at today’s higher interest rates, the countdown clock has only a few seconds left. Several large dominoes have fallen since our warning two months ago, including Credit Suisse and First Republic Bank. In the U.S. alone, the size of bank failures so far this year has already exceeded total collapses in 2008, when measured by bank assets and after adjusting for inflation:

And there’s more to come. According to banking expert and Stanford University academic Amit Seru, almost half of America’s nearly 5,000 banks have exhausted their capital buffers (i.e., the amount of shareholder capital available to offset losses in bank loan portfolios). As Seru recently warned in an interview:

“It’s spooky. Thousands of banks are underwater… Let’s not pretend that this is just about Silicon Valley Bank and First Republic. A lot of the US banking system is potentially insolvent.”

Unless central banks and policymakers are willing to deal with a major credit crash, all roads lead back to lower interest rates and more money printing.

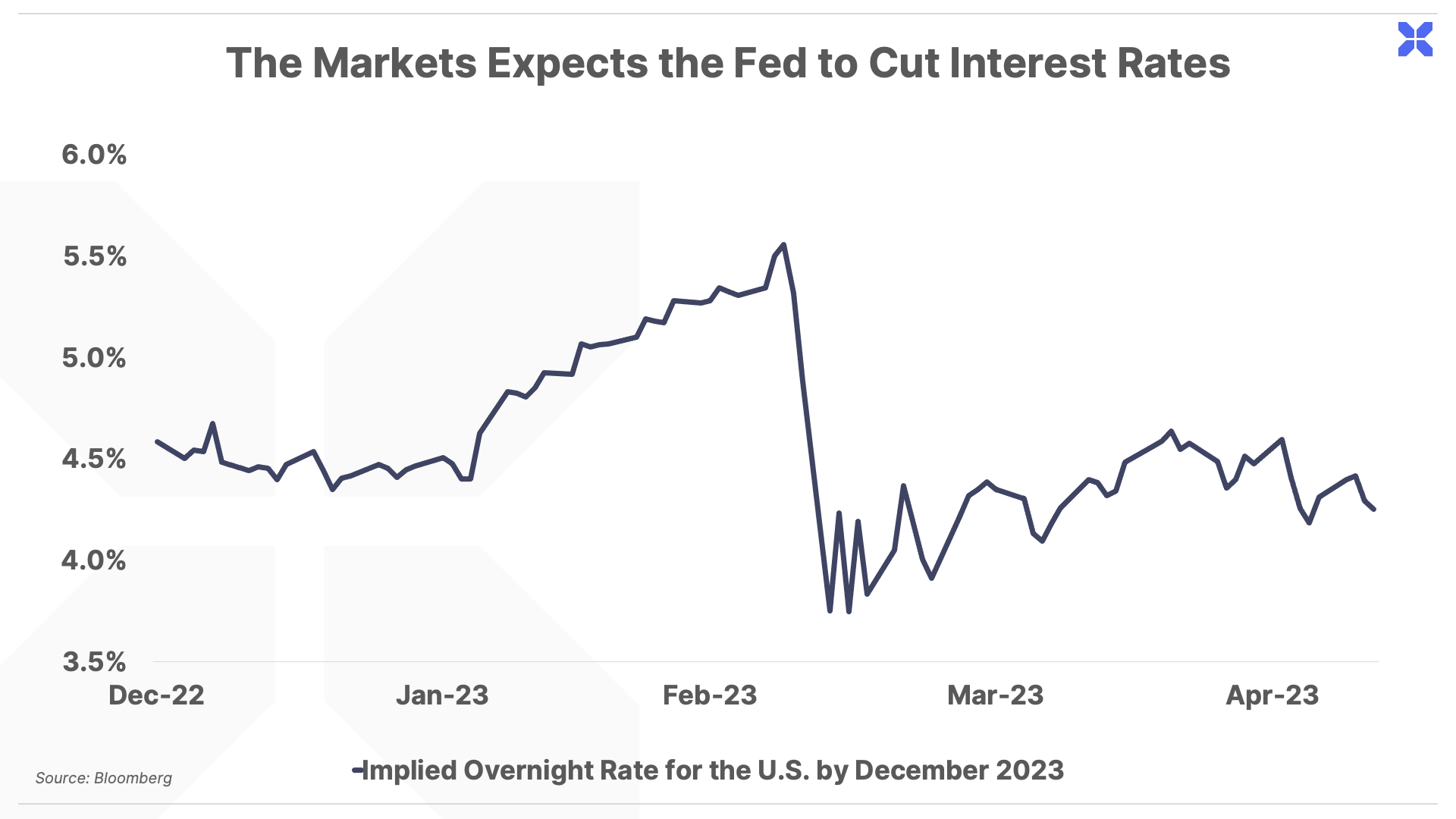

Federal Reserve Chair Jerome Powell maintains that the Fed has no plans to cut rates in 2023, even if inflation reaches the Fed’s 2% target (compared to the current 4.9% annualized rate).

But the market is betting that easy money will return in short order. The chart below shows the recent trading history of the implied Fed Funds rate for December 2023, which shows that traders first started pricing in rate cuts in the wake of the SVB collapse in mid-March. The market now expects the Fed to cut interest rates by 75 basis points (or 0.75%), from 5% today, to around 4.25% by December 2023:

Despite Powell’s public commitment to keep rates “higher for longer”, the market is telegraphing a clear message: the first round of bank failures kicked off by SVB was not an isolated event; it was just the start. And as the financial fallout continues, the Fed will be forced to slash interest rates to bail out the banking system, by re-inflating their underwater bond and loan portfolios.

We expect similar pressure on foreign central banks, which created the same fundamental problems plaguing the U.S. financial system after a decade of ZIRP – trillions of dollars in capital allocated at rock bottom yields, which has become impaired in today’s higher interest rate environment.

That’s why all roads lead back to the only solution: the return of cheap credit and money printing.

Bitcoin’s 80% rally so far this year, and gold approaching new all-time highs, reflect the market pricing in this inevitability.

Looking beyond financial speculators, foreign central banks also appear to be betting on a future of fiat currency debasement. In 2022, global central banks went on a record gold buying spree, in what can best be described as the ultimate hedge against their own failed monetary policies.

During previous easy-money eras, including the past decade of ZIRP, the U.S. dollar was able to do a better job of retaining its global purchasing power thanks in part to the petrodollar system – which allowed America to flood the world with excess currency, without suffering the inflationary consequences. Until now.

A Sharp Veer Away from the Petrodollar

William Simon flew out of Saudi Arabia in 1974 with his neck intact, but in 2018, Saudi journalist Jamal Khashoggi wasn’t so lucky. As we explained in the inaugural issue of The Big Secret on Wall Street, Khashoggi suffered a gruesome beheading under the supervision of Saudi Arabia’s Crown Prince Mohammed bin Salman.

On the 2020 campaign trail, Joe Biden publicly proclaimed that Saudi Arabia should be labeled a “global pariah” for its role in Khashoggi’s death… and since then, America’s relationship with the Saudis has taken a sharp turn for the worse.

Since last October, Saudi Arabia has rebuffed President Biden’s calls for OPEC to increase oil production – and has instead cut production, twice. In February 2023, Saudi Arabian leader Crown Prince Mohammed bin Salman point-blank refused to take a call with Biden.

And the deal that launched the petrodollar era is coming apart at the seams. Last month, the Wall Street Journal reported that Saudi Arabia’s Energy Minister, Prince Abdulaziz bin Salman, is “no longer interested in pleasing the U.S.” and is pursuing an economic strategy “without U.S. dependence.”

The breakdown extends to the oil-for-dollars angle of the deal too. On March 15, the Wall Street Journal reported that Saudi Arabia is considering selling oil to China for Chinese yuan – not dollars. Meanwhile, in response to the ongoing financial sanctions from Russia’s attack on Ukraine, Russia is forging closer ties with China. Earlier this year, the yuan surpassed the U.S. dollar as the most widely used currency for trading in Russia.

China and Russia are working overtime to bring other countries into their sphere of influence. Malaysia became the latest country to join their ranks.

In April, Malaysian Prime Minister Anwar Ibrahim announced that “there is no reason to continue to depend on the U.S. dollar.” That same month, Brazilian President Lula da Silva traveled to China, where he signed $50 billion in new cooperation and investment deals. During the trip, he also announced that de-dollarization is a key priority for the Brazilian economy. According to the Financial Times, Lula made the following comments:

“Every night I ask myself why all countries have to base their trade on the dollar? Why can’t we do trade based on our own currencies? Who was it that decided that the dollar was the currency after the disappearance of the gold standard?”

This is the largest coordinated push against the U.S. dollar since the formation of the petrodollar system in the 1970s. Economist Gal Luft, director of the Analysis of Global Security think tank in Washington D.C., summed up the risks at play:

“The oil market, and by extension the entire global commodities market, is the insurance policy of the status of the dollar as reserve currency… If that block is taken out of the wall, the wall will begin to collapse.”

The bottom line: the U.S. dollar’s value is facing a two-pronged attack: first, from the collapse of the ZIRP debt bubble, and second, from a coordinated foreign move away from the petrodollar.

The mainstream financial media is mum on what is arguably the largest coordinated assault on the U.S. dollar since it became the global reserve currency after World War II. This monetary revolution will not be televised.

That’s why we believe now is the time to safeguard your wealth from the demise of fiat currencies with the two ultimate stores of value: gold and Bitcoin.

An Insurance Policy Against the Demise of the Dollar

It makes sense for every investor to allocate some portion of their investable net worth into physical gold (coins or bullion) as insurance against fiat currency debasement and financial instability.

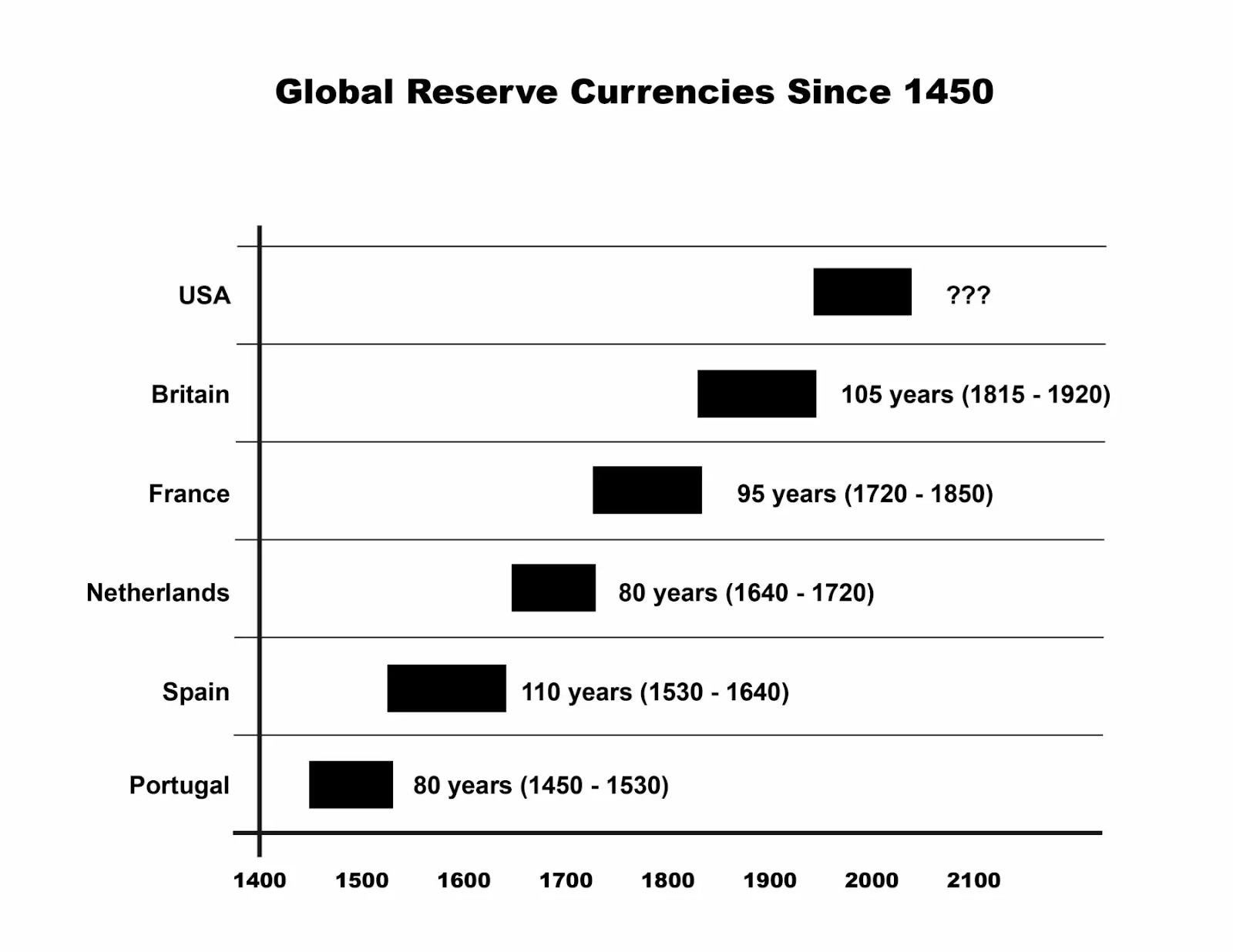

The history of fiat currency is unblemished by success. The following chart shows that the average lifespan for global reserve currencies is roughly 100 years.

The rise of the U.S. dollar to become the dominant currency in the global economy started soon after World War I. Its position at the top was solidified in 1944 with the Bretton Woods accord, which established the rules of the game for the global monetary system.

But now the U.S. dollar is in the final few innings, at most, of being the star pitcher in the global financial system. And let’s not forget: the mighty dollar has lost more than 90% of its purchasing power, as measured by the U.S. consumer price index, over the past 80 years.

Gold, on the other hand, has a 5,000-year history of maintaining its value and preserving wealth.

Holding physical gold will preserve your wealth – but not grow it.

That’s why we’re introducing a business that transforms gold in the ground into a growing profit stream for investors.

We’re not talking about a mining company. Like all forms of resource extraction, gold mining is generally a terrible business. Digging miles into the Earth to explore for and extract physical gold is capital intensive. A substantial portion of profits must go right back into the ground to keep production going, and to continuously replace the depleting asset base of existing mines.

Mining companies spend enormous sums on labor, capital, and finding new reserves – and that’s money that doesn’t go to shareholders. As Warren Buffett’s long-time business partner and right-hand man Charlie Munger once explained…

“There are two kinds of businesses: The first earns twelve percent, and you can take the profits out at the end of the year. The second earns twelve percent, but all the excess cash must be reinvested – there’s never any cash. It reminds me of the guy who sells construction equipment – he looks at his used machines, taken in as customers bought new ones, and says “There’s all of my profit, rusting in the yard.” We hate that kind of business.”

Charlie and Warren would love our pick today – a capital efficient gold company that outperforms both gold and gold mining stocks, offering the ultimate protection against fiat currency debasement.

“The Gold Investment that Works”

This content is only available for paid members.

If you are interested in joining Porter & Co. either click the button below now or call our Customer Care team at 888-610-8895.